You're probably in one of two spots right now. Your business is doing well enough that rent feels painful, or your lease is coming up and the landlord is asking for more money, more term, and more control over your future than you're comfortable giving. You've built a real company, but the building still belongs to someone else.

That's usually the moment owner-occupiers start looking seriously at commercial real estate acquisition. Not because they woke up wanting to become real estate investors, but because they're tired of writing large rent checks for space they can't fully control, can't improve on their terms, and can't build equity in. For an operating business, buying property can change all three.

This decision sits inside an enormous market. One estimate places the combined value of U.S. commercial real estate at about $15.5 trillion, with office and retail alone representing nearly $5 trillion in value, according to commercial real estate market figures compiled by FNRP. That scale is exactly why small mistakes get expensive fast. Even a modest owner-user purchase deserves disciplined underwriting, tight deal structure, and financing that fits the business instead of straining it.

This guide is written from the owner-occupier's seat. The focus isn't generic investing theory. It's how a business owner should think about buying the building they'll use, and how SBA financing changes the way you search, negotiate, underwrite, and close.

Table of Contents

- Introduction From Tenant to Owner

- Laying the Groundwork for Your Acquisition

- Evaluating and Valuing the Property

- Financing Your Acquisition with SBA Loans

- Navigating Underwriting and Third-Party Reports

- The Final Mile Closing and Post-Acquisition

- Frequently Asked Questions about CRE Acquisition

Introduction From Tenant to Owner

Business owners usually don't move toward ownership because it sounds exciting. They move because renting starts getting in the way. The landlord controls renewals, controls major improvements, and often controls whether your business can stay in a location you've spent years making valuable.

Owning changes that conversation. You can build around your operation instead of around lease restrictions. You can plan longer-term improvements. You can stop treating occupancy as a pure expense and start treating it as part of your balance sheet strategy.

The mistake first-time buyers make is assuming the purchase process works like a residential closing with a bigger number attached. It doesn't. A commercial real estate acquisition for an owner-user is really three deals happening at once. You're buying a property, proving your business can carry the debt, and fitting the transaction into lender and SBA rules at the same time.

Practical rule: The best building is not the one you like most. It's the one your business can operate in efficiently, finance cleanly, and hold without choking cash flow.

That's why financing can't be an afterthought. If you're using SBA 7(a) or 504, the loan program affects what kind of property makes sense, how much renovation you can fold in, how much liquidity you should preserve, and even how you write the initial offer. Owner-occupiers who understand that early usually move faster and make fewer expensive revisions later.

A solid acquisition process starts before touring listings. It starts with knowing what your business needs, what the SBA will allow, and what structure gives you the highest chance of closing without overreaching.

Laying the Groundwork for Your Acquisition

The cleanest deals usually begin with the least glamorous work. Before you call on a property, define what your business is buying.

A surprising number of buyers start with, “I want to own instead of rent.” That's fine as motivation, but it's not enough to evaluate a building. You need a usable brief that tells your broker, attorney, CPA, and lender what fits and what doesn't.

Build a property needs checklist

Write this down before you tour anything:

- Operational fit: How much usable space do you need now, and what parts of the layout are essential for your business?

- Occupancy plan: Will your company occupy the required portion at closing, and can you document that use clearly?

- Location logic: Where do your staff, customers, vendors, or delivery routes need you to be?

- Physical constraints: Ceiling height, parking, power, loading, plumbing, HVAC, visibility, specialized buildout, and access all matter.

- Expansion path: Can you grow into vacant space, add a shift, or reconfigure the layout without major disruption?

- Zoning and use: Don't assume your business use is permitted just because the building “looks right.”

That checklist keeps emotion from taking over. It also protects you from buying a building that works for the broker's brochure but not for your company's day-to-day operations.

Assemble the right deal team

This isn't a one-person project. Each advisor solves a different problem.

- Commercial real estate broker: Finds inventory, gets market color, helps position offers, and spots issues in pricing or seller posture.

- Real estate attorney: Reviews the purchase contract, title matters, survey issues, entity structure, and closing documents.

- CPA: Evaluates tax treatment, entity implications, and how the purchase affects the business financially.

- SBA loan broker or lender specialist: Screens the deal for program fit, lender appetite, owner-occupancy issues, equity structure, and third-party report requirements.

If one person says they “handle all of it,” be careful. In commercial real estate acquisition, overlap creates blind spots. The attorney is not your lender strategist. The broker is not your environmental advisor. The CPA is not your deal negotiator.

Buyers get into trouble when nobody owns the financing narrative early. The property may be solid, but if the lender can't get comfortable with occupancy, cash flow, or structure, the deal still dies.

Source deals with financing in mind

Off-market opportunities can be excellent, but they aren't automatically better. A key advantage is often seller flexibility, not price alone. Some off-market sellers will tolerate a longer diligence period, discuss seller-note structure, or stay pragmatic when repairs come up.

If you're selling another investment property as part of a broader strategy, it helps to model tax consequences before you commit. A tool like 1031 exchange calculations can help frame the conversation with your CPA when exchange timing or equity planning affects your purchase path.

A few sourcing habits work well for owner-users:

- Target properties your business can occupy. Don't chase buildings that only work if you become a full-time landlord.

- Ask brokers about stale listings. Sellers with older listings are often more realistic on structure.

- Call owners directly in your trade area. Especially if your business needs a specialized building type.

- Screen for SBA friction early. Environmental history, mixed-use issues, excess vacancy, and heavy deferred maintenance can complicate approval.

The groundwork phase is where most avoidable mistakes happen. Not because the issues are complicated, but because buyers rush into tours and offers before they know what they can finance and what they need.

Evaluating and Valuing the Property

A property can be attractive and still be wrong for an owner-occupier. That's the central discipline here. You aren't underwriting the deal the way a passive investor buying a leased asset would. You're underwriting a building as a business tool, a collateral asset, and a financeable transaction.

Start with operational value, not investor jargon

Cap rates get discussed constantly in commercial real estate, but for many owner-users they're a weak starting point. If you're buying a building primarily to operate your business, the first questions are different.

Does the space reduce occupancy risk? Does it support revenue-producing operations? Does it require major immediate capital expenditure? Can it appraise and finance cleanly? Can your company comfortably service the debt after closing?

That doesn't mean income analysis is irrelevant. It matters a lot if the property has other tenants, excess space, or future lease rollover. Underwriting gets more complex when future income is unstable. Models need to account for lease expirations, renewal probability, market rents at rollover, downtime, and tenant improvement or leasing commission costs, which makes scenario analysis more useful than a simple going-in cap rate, as noted in this guidance on property underwriting for commercial real estate acquisitions.

For owner-users, valuation usually leans more heavily on:

- Comparable sales

- Replacement or cost logic for specialized buildings

- Functional utility for your business

- Expected repair and retrofit burden

- Any supportable rental value from excess space

If the building has physical issues, get serious eyes on it early. A resource like expert pre-purchase property assessments is useful as a reminder of how much can hide behind a clean walkthrough.

Do fast underwriting before you spend real money

Before you order reports or pay legal fees, do a quick filter. I like buyers to answer these questions first:

| Question | Why it matters |

|---|---|

| Can the business occupy the required portion? | SBA eligibility and loan structure can hinge on this. |

| Does the monthly payment appear workable? | A building that strains operations isn't a win. |

| Are there obvious repair or environmental flags? | Some properties become expensive before you even close. |

| Is the asking price defensible versus nearby sales? | A low appraisal can force more equity into the deal. |

| If there's rental income, how durable is it? | Lease rollover can erase the “bargain.” |

A lot of buyers overpay because they underwrite to hope. They assume a vacant suite will lease quickly, a short-term tenant will renew, or deferred maintenance is “manageable” without pricing it in.

If valuation questions are tying into a broader acquisition or lender review, this guide to business valuation for SBA loans and how lenders determine value is a useful companion. Property value and business strength often get evaluated together in owner-user financing.

Write an LOI that protects you without scaring off the seller

The letter of intent is where good buyers separate themselves from impulsive ones. A strong LOI is not just about price. It allocates risk before lawyers start billing.

Focus on these terms:

- Due diligence period: Long enough to complete inspections, financing review, and third-party reports.

- Financing contingency: Especially important with SBA financing and lender-driven conditions.

- Earnest money structure: Reasonable up front, with clear timing on when it goes hard.

- Access rights: You need inspection access, contractor access, and document access.

- Seller deliverables: Rent roll, operating statements, service contracts, permits, certificates, plans, and any environmental history.

- Repair and credit language: Don't leave every issue for the purchase agreement if you already know there may be problems.

A seller takes your offer more seriously when your LOI shows you know how the deal will close, not just what number you want to pay.

A practical example. Suppose you're buying a mixed-tenant building and your business will occupy the main suite after closing. The seller pushes for a short diligence window and hard earnest money early. That sounds aggressive, but if appraisal, environmental review, or lease analysis turns up a problem, you've boxed yourself in. A better approach is often a staged deposit with enough time to complete the lender-required work before your exposure increases.

That balance matters. Too soft, and the seller doubts you. Too hard, and you absorb risks the reports haven't even uncovered yet.

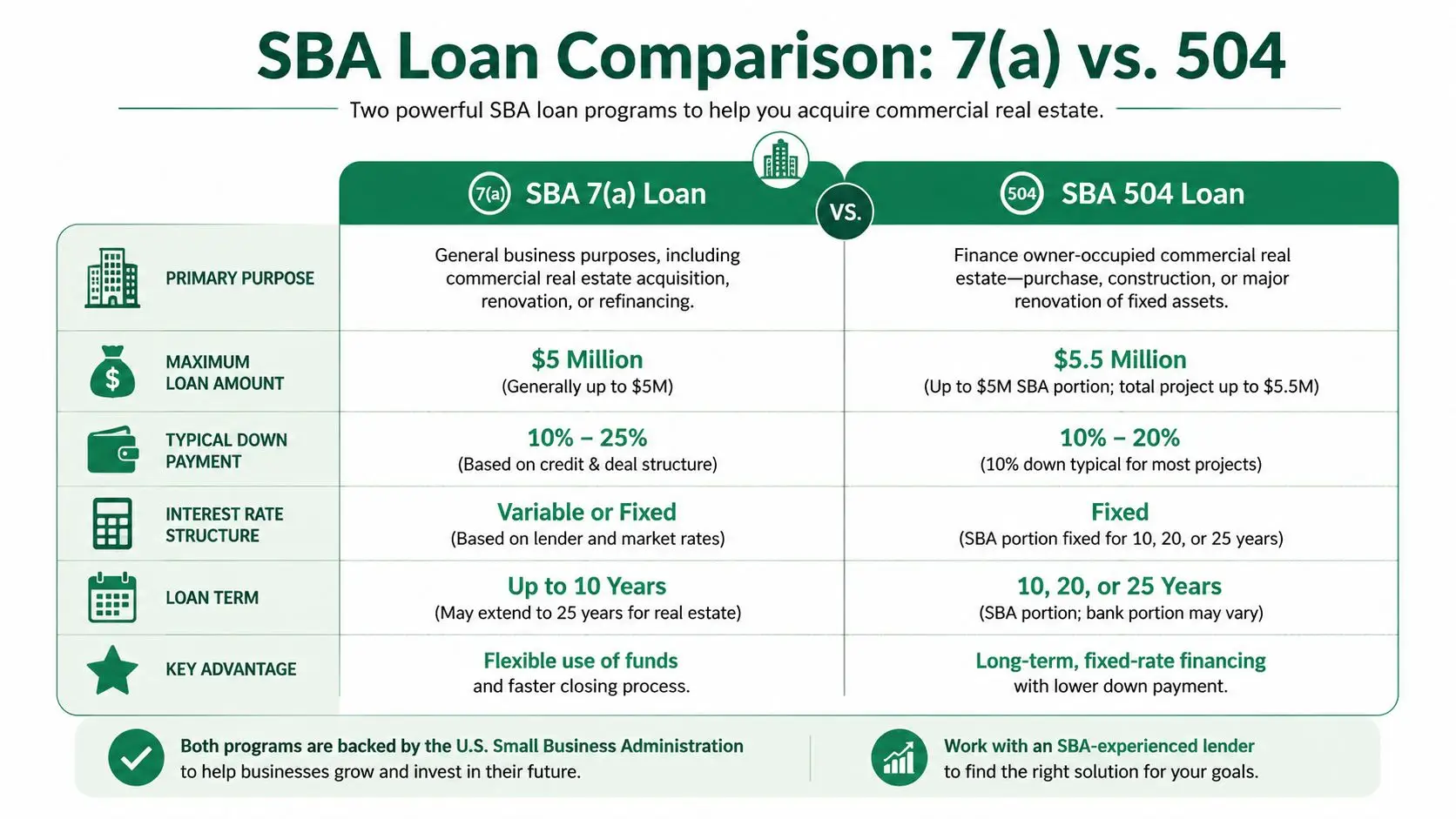

Financing Your Acquisition with SBA Loans

For owner-occupiers, financing isn't one chapter of the process. It's the frame around the whole deal. The property you pursue, the way you negotiate, the cash you keep in reserve, and the speed of closing all change depending on whether the transaction fits better under SBA 7(a) or SBA 504.

How 7(a) and 504 really differ

Both programs can work for owner-occupied commercial real estate. They just solve different problems.

| Feature | SBA 7(a) | SBA 504 |

|---|---|---|

| Best fit | Flexible acquisitions with mixed needs | Real estate and heavy fixed assets |

| Use of proceeds | Broad, often including business purposes beyond the building | Primarily owner-user real estate and eligible fixed assets |

| Rate structure | Often more flexible but can vary by lender and structure | Commonly attractive for buyers who want predictable fixed-rate exposure on the CDC portion |

| Structure | Typically one primary lender loan with SBA guaranty | Usually bank first lien plus CDC second lien |

| Best use case | Purchase plus working capital, light improvements, or more complex structure | Turnkey property where low equity injection and long-term payment stability matter |

The practical question isn't “Which program is better?” It's “Which program fits the deal I'm doing?”

When 7(a) is usually the better tool

Use 7(a) when the building purchase is tied closely to the business's broader needs.

Common examples:

- You need to buy the property and preserve cash for operations.

- The building needs improvements that are integral to moving the business.

- The deal includes equipment, closing costs, or other eligible business expenses.

- The structure needs flexibility because the transaction isn't perfectly clean.

That flexibility is why many first-time owner-users end up in 7(a). It can be a better fit when the challenge isn't merely acquiring a building. It's acquiring a building without starving the company right after closing.

A lot of borrowers focus too heavily on debt and overlook the core issue. The strongest structure is often the one that leaves enough liquidity for inventory, payroll, transition costs, and normal surprises after move-in.

Here's a deeper primer on SBA real estate loans using 7(a) and 504 if you want the mechanics side by side.

A quick walkthrough helps here:

When 504 is usually the better tool

504 tends to shine when the property is the centerpiece and the project is relatively straightforward.

It often fits buyers who want:

- A property the business can occupy without major structural complexity

- A long-term hold mindset

- Payment predictability

- A capital stack designed around owner-user real estate rather than broader business liquidity

This is often the cleaner answer for a stable company buying a building that's ready to function with limited drama. If the property is right, the occupancy plan is clear, and you don't need the same level of proceeds flexibility, 504 can be a strong match.

The wrong SBA program doesn't always kill the deal. Sometimes it just makes the deal unnecessarily tight, slow, or cash-hungry.

What tighter credit changes in practice

Financing conditions matter more than many sellers realize. The Federal Reserve's 2025 Senior Loan Officer Opinion Survey showed that banks continued tightening standards for commercial real estate lending, a market condition highlighted in this discussion of commercial property acquisition and current lending conditions. In practice, that means buyers should care about closing certainty as much as headline financing percentage.

That shows up in real decisions:

- A borrower may choose the lender with the clearest path to approval, not just the flashiest initial quote.

- A seller note on standby may solve a gap more effectively than forcing a conventional structure that drags.

- A lower leverage outcome may be preferable if it materially improves speed and lender confidence.

- A buyer may need broader lender coverage because one bank's comfort with property type, tenant mix, or industry risk can differ sharply from another's.

What doesn't work in this market is casual financing. If you wait until after the LOI to discover occupancy issues, weak debt service coverage, or property-specific concerns, you lose time and negotiating advantage. Strong owner-users line up the financing strategy early and let that strategy shape the acquisition from day one.

Navigating Underwriting and Third-Party Reports

Once you have a term sheet, the deal feels real. It also gets much more invasive, as the lender stops discussing your transaction in general terms and starts verifying whether the borrower, the business, and the property all work together under credit policy and SBA rules.

What underwriting is actually testing

For an owner-user purchase, lenders usually look at two engines of repayment. First, the operating business. Second, the property as collateral and as a place where that business can function successfully.

That's why underwriters request so much. They're trying to understand global cash flow, management stability, existing debt obligations, ownership structure, historical performance, and whether the property introduces avoidable risk. If the business is healthy but the building has environmental baggage, that's a problem. If the building is great but the business can't support the debt, same result.

Expect document requests around:

- Business financials: Tax returns, year-to-date profit and loss, balance sheet

- Borrower financials: Personal financial statement, tax returns, liquidity evidence

- Entity documents: Organizational docs, leases, ownership records

- Property records: Rent roll, operating statements, tax bills, insurance, permits, plans

- Narrative support: Business history, use of proceeds, occupancy plan, explanation of any weak spots

If environmental questions come up, SBA-specific standards matter. This overview of SBA environmental requirements for commercial real estate is a good reference point because many first-time buyers underestimate how much property history can affect timing.

The reports that decide whether your deal survives

The main third-party reports usually include the following:

| Report | What it answers | What can go wrong |

|---|---|---|

| Appraisal | Is the purchase price supported by market value? | Low value can require price cuts or more equity |

| Phase I ESA | Are there signs of environmental contamination risk? | Recognized environmental conditions can trigger more review |

| Property Condition Assessment | What repairs or deferred maintenance exist? | Unexpected capital needs can change the deal economics |

| Title and survey | Does legal ownership match reality on the ground? | Easements, encroachments, or title defects can delay closing |

For buyers who want a broader checklist mindset, this article on mastering real estate acquisition due diligence is a useful supplement.

Here's what matters in practice. A low appraisal doesn't always end the deal, but it forces a decision. Renegotiate the price, bring in more equity, or challenge the value if there's a legitimate basis. A Phase I that flags concern doesn't automatically mean contamination exists, but it can trigger further investigation and delay. A PCA with serious roof, HVAC, or structural findings can change whether the building still makes sense for your business.

Don't treat third-party reports as lender paperwork. They're often the first honest look at what you're really buying.

What to have ready before the lender asks

Underwriting slows down when borrowers answer every request one document at a time. It moves better when you package the file before the requests start.

Prepare a closing folder with:

- Three years of business tax returns

- Current interim financials

- Personal tax returns for guarantors

- Personal financial statements

- A concise business overview

- Purchase contract or LOI

- Entity formation documents

- Current lease, if you're relocating from rented space

- A simple explanation of how the property will be occupied

- Any known bids for repairs or improvements

Buyers who stay organized usually get better lender engagement because the file reads as manageable. Buyers who drip information in late force the lender to underwrite through uncertainty, and that almost always creates more conditions.

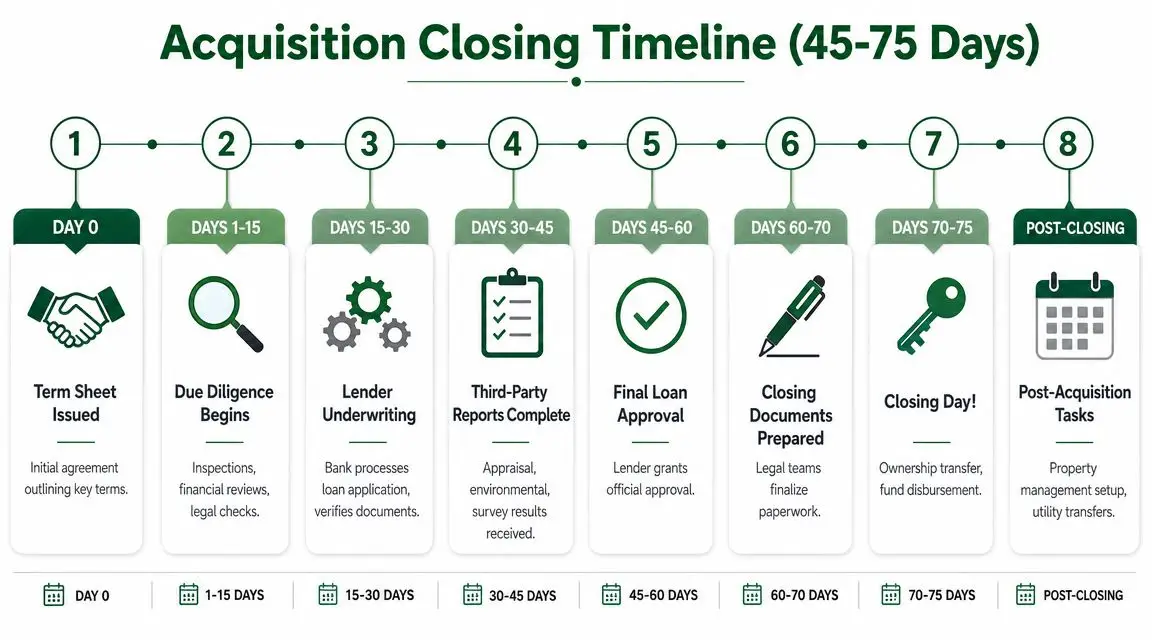

The Final Mile Closing and Post-Acquisition

Buyers often assume the hard part is over during the last stretch. In reality, timing problems surface at this point. Documents have to line up, title has to clear, lender conditions have to be satisfied, and every party has to move in the same direction.

What usually happens between approval and funding

A typical owner-user SBA closing often runs on a sequence that looks familiar even when the details change:

- Term sheet accepted

- Due diligence opens

- Third-party reports are ordered

- Underwriting issues conditions

- Approval moves to closing

- Title and legal documents are finalized

- Closing statement is balanced

- Funds disburse and ownership transfers

The friction points are rarely dramatic. They're administrative. Insurance isn't bound correctly. The operating entity on the purchase contract doesn't match the borrowing entity. A survey issue appears late. A repair credit isn't documented clearly. Someone assumed the title company would handle a prorated expense item that still needs seller approval.

Review the closing statement carefully. Property taxes, utilities, rent, deposits, and other prorations need to be accurate. If there are tenants in place, make sure security deposits, prepaid rents, and service contracts are transferred or credited correctly.

Common last-mile mistakes

Some closing problems are hard to predict. Most are not.

- Going quiet late in the process: If the lender, attorney, broker, and title company aren't communicating, small issues turn into missed dates.

- Changing structure midstream: New entities, ownership changes, or revised occupancy plans can restart approvals.

- Underestimating move-in costs: Furniture, equipment relocation, cabling, signage, permits, and minor repairs add up quickly.

- Ignoring post-closing admin: Utilities, insurance updates, lease notices, property tax mailing addresses, and vendor transfers need attention right away.

One habit helps more than anything else. Keep a live closing checklist and assign every item to a person, not a group. “Attorney to confirm title objection resolution” gets done. “Team to handle title issue” often doesn't.

After closing, the work becomes operational. Recordkeeping, occupancy compliance, maintenance planning, and any funded improvement work all need to happen cleanly. A building is only an asset if the business can use it without chaos.

Frequently Asked Questions about CRE Acquisition

The U.S. commercial real estate industry is massive. IBISWorld estimates $1.6 trillion in industry revenue in 2026 and about 3 million businesses operating in the space, according to IBISWorld's U.S. commercial real estate industry outlook. For owner-occupiers, that means there's plenty of opportunity, but also plenty of room to make the wrong financing or property decision.

Can I finance renovations as part of the purchase

Yes, often you can, but the right structure depends on the scope and how the funds will be used. If the project needs a building purchase plus improvements and possibly some business flexibility around the edges, 7(a) is often the first place to look. If the project is more squarely tied to fixed-asset occupancy and long-term use, 504 may also fit. The key question is whether the improvement plan is well defined, documented, and acceptable to the lender.

How much of the building does my business need to occupy

SBA owner-occupied financing is built around actual business use, not passive investment. In practical terms, the property must be primarily occupied by the operating business in a way that satisfies SBA eligibility standards. This needs to be clear from the floor plan, the use description, and the loan narrative. If the deal only works because most of the building is leased to others, it may not be the right SBA transaction.

Can I buy more space than I need and lease the rest

Often, yes, if your business still meets the occupancy requirement and the excess space is reasonable within the program rules. This can work well when you want room to grow and the tenant income helps offset carrying cost. Where buyers get into trouble is overbuying. If the building is materially larger than your real operating needs, the transaction can start looking more like an investment property than an owner-user acquisition.

If you're weighing an owner-occupied purchase and want help pressure-testing the structure before you commit, GoSBA Loans can help you compare SBA options, understand lender requirements, and improve closing certainty without adding brokerage cost to the borrower.