Most advice on how to become an SBA loan broker gets the job wrong from the start. It treats the role like a lightweight sales business. Find leads, submit files, collect a fee.

That's not how durable SBA brokerage works.

In practice, this job sits much closer to credit packaging, compliance management, lender matching, and transaction coordination than generic loan sales. If you want to last in this niche, you need to understand SBA program rules, the lender's underwriting workflow, the boundary between brokering and lending, and the discipline required to move a file from inquiry to funding without avoidable friction.

Table of Contents

- The Reality of Being an SBA Loan Broker

- Mastering SBA Programs and Compliance

- Building Your Network of Lender Partners

- Designing Your Brokerage Operations and Workflow

- Executing Your Client Acquisition Strategy

- Understanding Revenue Models and Fee Structures

- Navigating Common Pitfalls and Key Questions

The Reality of Being an SBA Loan Broker

A real SBA broker is not the lender. That distinction sounds obvious, but it causes more confusion than it should.

The SBA's own guidance explains how to become an SBA lender, but that's different from building a brokerage. Most generic broker guides also blur the line between a broker, a lender, and a Lender Service Provider. If you miss that boundary, you can build the wrong business model from day one. The SBA framework is centered on lenders and guarantee eligibility, which is why a broker needs a compliance-first operating model and a lender-partner strategy, not just sales ability, as outlined in the SBA guidance for becoming a lender.

A broker originates opportunities, screens them, helps structure the request, packages the file, and manages communication. A lender underwrites, approves, closes, disburses, services, and, if necessary, liquidates the loan. An LSP may handle operational functions for a lender under its own arrangement, which is a different role again.

Practical rule: If you can't clearly explain which tasks belong to the broker and which belong to the lender, you're not ready to present yourself to either borrowers or bank partners.

That's why the popular “just connect borrowers to capital” advice falls apart in the SBA world. SBA files are documentation-heavy. Eligibility issues can surface late. Ownership structure, guarantor requirements, use of proceeds, and closing conditions all matter. A weak broker creates drag. A strong broker removes it.

For a grounded picture of the day-to-day role, this guide on what an SBA loan broker does is useful because it frames the job as execution, not just referral.

What the job really feels like

You'll spend less time “selling money” than most newcomers expect, and more time doing work like this:

- Pre-screening the deal: Is the borrower even a fit for SBA financing?

- Cleaning up the story: Does the file make sense to credit, not just to the entrepreneur?

- Controlling the document flow: Missing items don't just annoy underwriters. They stall momentum.

- Managing expectations: Borrowers often underestimate how much detail lenders need.

- Choosing the right lender: A poor lender match can waste weeks.

The brokers who last are usually calm, organized, and hard to rattle. They know that credibility comes from sending files that are complete, financeable, and appropriately placed.

Mastering SBA Programs and Compliance

You can't learn how to become an SBA loan broker by memorizing a few talking points about “small business funding.” You need product fluency.

That matters because SBA lending is large, structured, and program-specific. In fiscal year 2024, SBA-backed lending reached approximately $56 billion in total guaranteed loan volume, and the core programs are 7(a), CDC/504, and Microloan according to this SBA lending volume summary. If you want borrowers and lenders to take you seriously, you need to know where each request belongs before you ask anyone for a credit look.

Know the programs well enough to triage fast

At minimum, you should know the broad fit of the major programs:

| Program | Best fit | Key limit from verified data |

|---|---|---|

| SBA 7(a) | Acquisitions, working capital, refinancing, real estate | Up to $5 million |

| CDC/504 | Fixed assets such as owner-occupied real estate and equipment | Projects can reach $5.5 million |

| Microloan | Very small financing needs | Cap is $50,000 |

| SBA Express | Smaller, faster-turn requests when the file fits | Capped at $350,000 |

Those numbers shape your intake. A borrower asking for acquisition financing and post-close working capital usually points you toward 7(a). A borrower financing owner-occupied commercial property or equipment may fit 504 better. A very small request may belong in Microloan territory. A time-sensitive smaller request may call for Express if the lender likes the file.

If you're still learning the broader business-lending side, this discussion on starting a business lending brokerage is a helpful complement. Just don't mistake general commercial lending knowledge for SBA specialization.

Compliance knowledge is part of sales

In SBA brokerage, compliance isn't a back-office topic. It's part of origination.

Lenders evaluate issues such as eligibility, repayment ability, collateral, ownership, and the SBA's credit elsewhere rule. Owners with 20% or more equity must provide a personal guaranty under the verified guidance provided in the source material above. If you don't surface those issues early, you don't have a pipeline. You have a queue of future declines.

A practical intake call should answer questions like these:

- Use of proceeds: Is the money for acquisition, working capital, refinance, equipment, or real estate?

- Ownership map: Who owns what, and who will need to guarantee?

- Industry fit: Is the borrower in an industry the target lender will consider?

- Basic repayment logic: Does the request make sense on a lender's terms?

- Urgency: Does the timeline fit standard SBA processing or a smaller Express-style path?

A new broker usually overestimates the value of lender access and underestimates the value of clean eligibility triage.

The more precisely you can sort a deal before submission, the more trust you build with lenders. And that trust compounds.

Building Your Network of Lender Partners

A new broker often thinks the hard part is finding lenders. It isn't. The hard part is becoming the kind of broker lenders want to hear from twice.

Most banks already have more inbound opportunities than they can pursue. What they need is not another person emailing rough scenarios. They need someone who understands their credit box, respects process, and sends opportunities that are already filtered.

What lenders actually want from a broker

Lenders look for predictability. If you present yourself as a source of complete, financeable deals, you become useful quickly.

That means your pitch to a lender partner should sound less like “I can bring you volume” and more like this:

- I pre-screen for fit: I won't send requests outside your appetite.

- I gather documents early: You won't have to chase basic items after the first review.

- I understand structure: I know when a file belongs in 7(a), 504, or a non-SBA lane.

- I manage the borrower: I keep communication organized and expectations realistic.

- I stay in the deal: I don't disappear after the introduction.

That last point matters. Some brokers act like lead vendors. Serious SBA lenders prefer originators who can help shepherd the transaction.

For borrowers, that same lender-network value often shows up in better execution and fit, which is why this explanation of how SBA brokers get better terms is worth reviewing.

How to vet a lender relationship

Not every SBA lender is the right partner for your model. Some are strong on acquisitions. Some move better on owner-occupied real estate. Some are responsive until term sheet, then slow down badly in closing. You won't learn that from a marketing brochure.

Ask direct questions:

What deal types do you prefer?

Industry, use of proceeds, and transaction size matter.How much packaging do you expect from the broker?

Some lenders want a full credit-ready file. Others will tolerate rougher intake.How do you handle communication during underwriting?

A lender who goes silent creates problems you'll wear with the client.What closes smoothly, and what tends to stall?

This tells you whether the bottleneck sits in credit, closing, or documentation.When do you decline fast?

Good lenders usually know their own no-go patterns.

The best lender relationships aren't broad. They're specific. You know exactly which kinds of files to send and which not to.

Build a focused panel, not a random list. A smaller group of reliable lender partners usually outperforms a giant contact sheet full of weak relationships.

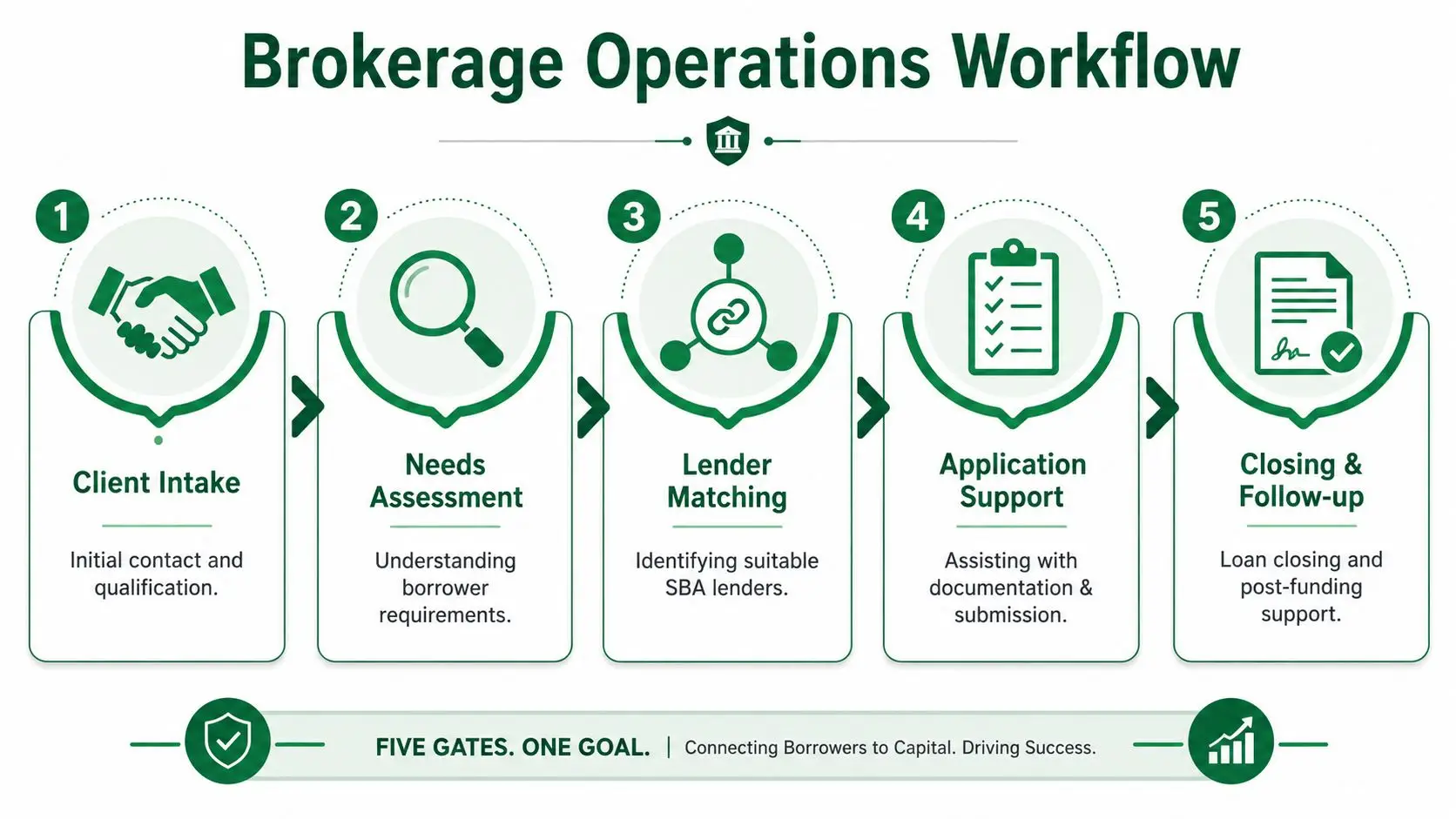

Designing Your Brokerage Operations and Workflow

An SBA brokerage is an operations business disguised as a finance business. If your workflow is sloppy, your borrower experience will be sloppy too.

The cleanest framework is a five-gate process: pre-qualification, application, underwriting, packaging and closing, and funding. That structure mirrors the lender's document-driven path and is described clearly in this overview of the SBA loan process and lender workflow.

Build around the five gates

Treat each gate as a separate standard of readiness.

Pre-qualification is where you decide whether the deal deserves time. You're checking fit, use of proceeds, ownership, urgency, and obvious eligibility issues.

Application is where you convert a conversation into a file. At this stage, many brokers already lose control because they let document requests stay vague.

Underwriting is not the time to discover basic facts. If ownership percentages, guarantors, business financials, or transaction structure are still unclear here, you're behind.

Packaging and closing is where approved deals still die. Insurance, entity documents, lease items, purchase agreements, proof of injection, and identity documents all need to line up.

Funding is the final handoff, but it still requires coordination. A borrower who thinks approval means money arrives automatically is going to need guidance.

Your package should reduce lender work

That's the core operational test. If your file creates unnecessary follow-up, lenders will remember.

The verified SBA-related guidance in the provided source material highlights the practical filters that matter most: business and industry eligibility, ownership and character, credit profile, financial capacity, collateral, and the credit elsewhere test. It also notes that for 20%+ owners, an unconditional personal guaranty is required, and that closing files often need items such as purchase agreements, insurance, lease documents, landlord subordination, down-payment proof, licenses, corporate documents, and KYC/CIP IDs, all discussed in this lender-facing summary of SBA loan requirements.

A workable operating stack usually includes:

- A CRM: To track stage, lender placement, follow-ups, and referral sources.

- A secure document portal: Email attachments create version chaos.

- Checklists by transaction type: Acquisition, working capital, and real estate files don't need the same packet.

- A lender matrix: Appetite, responsiveness, and file preferences in one place.

- A closing tracker: So conditions don't get lost after approval.

Here's the operational mistake I see most often. New brokers collect documents reactively. Experienced brokers collect them in anticipation of the next gate.

If the underwriter is the first person asking for an item that you should have gathered during intake, your process is too loose.

One practical option for teams that want a full-service brokerage model is GoSBA Loans, which presents itself as coordinating lender matching, underwriting support, and closing assistance across multiple SBA lenders. Whether you build that internally or adopt a similar discipline, the point is the same. The workflow has to be deliberate.

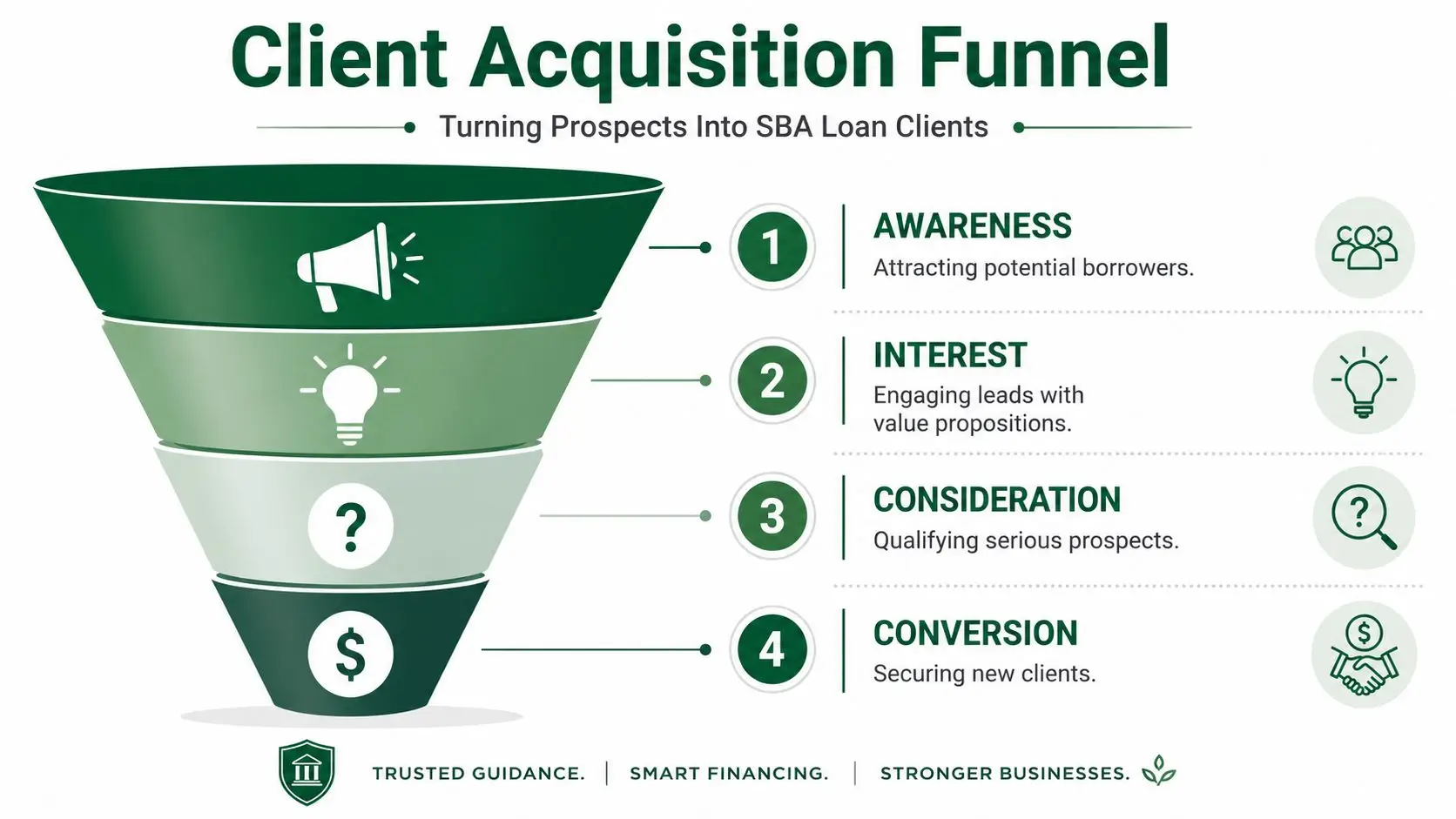

Executing Your Client Acquisition Strategy

Most weak SBA marketing has a volume problem and a quality problem at the same time. It attracts broad interest, but not many financeable borrowers.

That's why client acquisition in this niche works better when it starts with trust-based channels and problem-specific content, not generic “get business funding fast” messaging.

Start with a visual funnel, because the stages matter.

The best referral channels are trust-based

The strongest referral partners usually already sit near a financing event. They know when a borrower is serious, and they care whether the deal closes.

Good examples include:

- Business brokers: They often need a financing partner who can assess buyer bankability early.

- M&A advisors: They value brokers who understand acquisition structure and can work cleanly alongside deal counsel.

- CPAs: They can spot clients who are expanding, refinancing, or buying out a partner.

- Commercial real estate professionals: They surface owner-occupied deals where SBA financing may fit.

Each channel behaves differently. Business brokers can send highly motivated buyers, but many will be first-time borrowers who need education. CPAs usually send fewer referrals, but the clients may arrive with cleaner records. Real estate channels can produce strong opportunities, but timing tends to be compressed.

A referral source doesn't stay loyal because you're friendly. They stay loyal because you respond quickly, give honest feedback, and don't waste their client's time.

This video gives a useful look at the broader dynamics around prospecting and positioning in this market:

Content works when it qualifies, not when it only attracts

A broker's website should pre-sell your process. That means writing pages and articles around actual borrower intents such as buying a business, refinancing debt, funding working capital, or purchasing owner-occupied real estate.

LinkedIn also works well if you use it like a relationship platform, not a cold-pitch machine. Comment intelligently on transaction topics. Publish short breakdowns of common SBA mistakes. Show that you know how deals move.

Lead forms matter too. The wrong form invites noise. The right form filters for deal type, timeline, use of proceeds, and whether core documents exist. If you want a smart primer on form strategy and qualification signals, discover how Orbit AI improves lead quality.

The mistake to avoid is chasing everyone. A focused niche position, such as acquisition financing, partner buyouts, or owner-occupied real estate, is easier to market and easier for referral partners to remember.

Understanding Revenue Models and Fee Structures

The money side of this business sounds simple until you live through a delayed closing. Then you learn quickly that fee structure and cash flow are not the same thing.

The core reality is that SBA approvals commonly take 30 to 90 days, according to this discussion of SBA loan brokering timelines. That timeline shapes everything. If your business can't survive a longer cycle, your model is fragile no matter how attractive your compensation looks on paper.

Two common ways brokers get paid

Most brokerage revenue discussions fall into two buckets.

Lender-paid compensation means the lender pays the broker under its own arrangement. This can simplify the client conversation, but it usually comes with lender-specific rules and process expectations.

Borrower-paid fees put the fee agreement directly with the client. That gives you more control over the commercial arrangement, but it also raises disclosure and expectation-management issues.

A comparison helps:

| Model | Strength | Trade-off |

|---|---|---|

| Lender-paid | Cleaner for some borrowers, integrated with lender relationship | Less control over the compensation framework |

| Borrower-paid | Clear direct engagement with the client | Harder sales conversation, stronger need for documented value |

Whichever route you choose, learn the applicable SBA-related disclosure and agent-fee rules before you invoice anyone. This overview of SBA broker and agent fee rules is a good starting point.

Cash flow discipline matters more than headline fees

The operational lesson is simple. Don't build your business like a quick-turn lead shop.

The verified source above makes the deeper point well: broker value is increasingly in packaging, speed, and error reduction, not simple lender matching. That means your fees have to be justified by work that borrowers and lenders can see.

A few practical rules help:

- Keep fixed overhead light: Long cycles punish vanity spending.

- Track deals by stage: A “full pipeline” means little if most files are still soft inquiries.

- Document your scope: Clients should know whether you're advising, packaging, introducing, or staying through closing.

- Reserve time for hard deals: Acquisition transactions often need more hands-on work than straightforward owner-user real estate files.

The brokers who earn well in this niche usually aren't the loudest marketers. They're the ones who can get complicated files through process without drama.

Navigating Common Pitfalls and Key Questions

New brokers usually don't fail because they can't find a borrower. They fail because they underestimate the precision this work demands.

A few problems show up early and repeatedly.

Mistakes that hurt new brokers early

- Calling yourself a lender when you're a broker: That confuses clients and creates compliance risk.

- Submitting files too early: A fast bad submission is slower than a careful one.

- Working with every lender the same way: Each lender has its own appetite, pacing, and tolerance for incomplete files.

- Ignoring state-level issues: Generic national advice won't replace legal guidance on your specific licensing and operating requirements.

- Skipping insurance review: If you're handling advisory and packaging work, get competent advice on protections such as errors and omissions coverage.

The fastest way to damage your reputation is to promise certainty in a process that depends on lender credit judgment and complete documentation.

You also need emotional discipline. Some deals will be declined. Some will die in diligence. Some borrowers will disappear after you do real work. That's part of the business. Strong brokers review what happened, tighten intake, and improve lender fit instead of blaming the market.

Questions new brokers ask for good reason

Can you start part time?

Yes, but only if you're realistic. SBA deals need responsiveness. If your day job keeps you from handling document collection, lender follow-up, and client communication promptly, part-time turns into poor service.

How much capital do you need to start?

That depends on your operating model, tools, legal setup, and marketing choices. Keep the setup lean. Spend on process, compliance guidance, and secure systems before you spend on branding flourishes.

What if a packaged deal gets declined?

Treat the decline as diagnostic material. Was it eligibility, structure, industry fit, repayment logic, guarantor weakness, or documentation quality? Good brokers turn declines into sharper lender placement and sharper intake standards.

Do you need to know the SBA SOP?

Yes. You don't need to perform like outside counsel, but you do need working fluency in the rules that affect eligibility, guaranties, use of proceeds, and lender expectations. If you ignore the SOP, you'll eventually package avoidable problems.

Is this mostly a referral business?

No. Referrals help, but execution keeps them coming. The market rewards brokers who can organize a file, guide a borrower, and reduce friction for the lender.

The clearest answer to how to become an SBA loan broker is this: learn the rules, build lender trust, run tight operations, and treat every file like a credit process, not a lead.

If you want to see how a full-service SBA brokerage operates in practice, GoSBA Loans is a useful reference point. Borrowers, referral partners, and newer brokers can review its educational resources to better understand lender matching, packaging support, fee rules, and the mechanics of getting SBA deals from inquiry to closing.