You're probably in one of two spots right now. You've found a business worth buying, or you already own one and need capital for growth, equipment, refinancing, or real estate. The opportunity is clear. The financing path is not.

That's where most borrowers get stuck. SBA loans can offer excellent structure, but the SBA loan requirements don't read like a practical playbook. They read like policy. Lenders, however, don't approve policy. They approve fundable deals.

The difference matters. A borrower can be technically eligible and still get declined because the file is weak, the cash flow story is sloppy, or the request is structured the wrong way for the use of funds. On the other hand, a borrower with a few rough edges can still get approved if the package is clean, the purpose is sound, and the lender can defend the file under SBA rules.

This guide treats SBA requirements the way underwriters do. Not as a checklist to glance at once, but as a blueprint for fundability.

Table of Contents

- Your Guide to Navigating SBA Loan Requirements

- The Four Pillars of SBA Loan Eligibility

- Key Financial Metrics Underwriters Actually Scrutinize

- Demystifying Collateral and Personal Guarantees

- Choosing Your Path 7a vs 504 vs Express Loans

- The Essential SBA Loan Application Checklist

- How to Maximize Your Fundability and Avoid Pitfalls

Your Guide to Navigating SBA Loan Requirements

Most borrowers start by asking, “Can I qualify?” That's the right question, but it's incomplete. The better question is, “Will a lender view this as a bankable SBA deal?”

That shift in thinking changes everything. The SBA's rules are the floor. Underwriting lives above that floor. A lender wants to know whether the business is eligible, whether the use of funds is permitted, whether repayment is realistic, and whether the file is documented well enough to survive review without constant follow-up.

The SBA Standard Operating Procedure is the source of truth, but it doesn't speak in borrower language. It speaks in lender language. That's why many owners get overwhelmed. They hear terms like guaranty, debt service, collateral shortfall, equity injection, and eligible use of proceeds, but they don't get a practical explanation of what helps an approval move forward.

Here's the plain-English version. Good SBA files usually have four things in common:

- A clear borrower story. The ownership, experience, and business purpose make sense.

- Reliable cash flow. The business can carry the debt without strained assumptions.

- Clean documentation. Tax returns, financials, organizational records, and explanations line up.

- Smart structure. The loan type, term, and collateral fit the asset or business need.

Practical rule: Underwriters don't reward complexity. They reward clarity.

If you treat SBA financing like a paper chase, you'll likely create delays. If you treat it like a credit presentation, you'll make better decisions from the start. That means preparing your numbers before you apply, choosing the right SBA product, and understanding which issues are manageable versus which ones force a lender to say no.

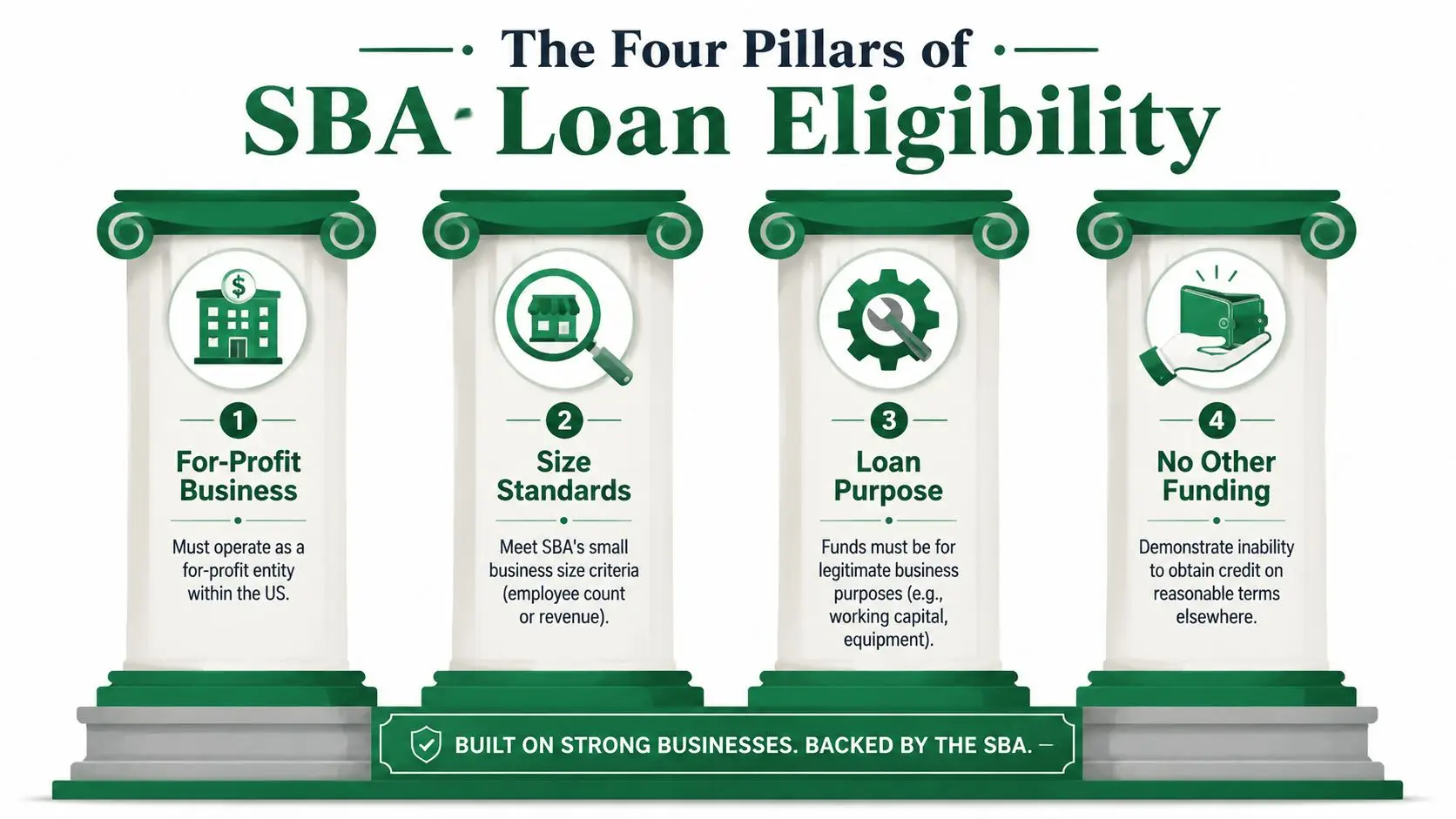

The Four Pillars of SBA Loan Eligibility

A borrower can look strong on paper and still have an SBA file stall fast. I see it when an owner has solid revenue, decent credit, and a real business, but cannot clearly show eligibility, explain the loan purpose, or connect the request to repayment. SBA approval starts with four pillars. If one is weak, the lender has to spend the rest of the file defending it.

Start with the business itself

The first pillar is basic business eligibility. The SBA is for qualifying small businesses. A lender starts by confirming the company fits SBA size standards, operates in an eligible industry, and is structured as a real operating business rather than a passive or ineligible venture. The SBA lays out those size rules by industry in its table of small business size standards.

It serves to answer a simple threshold question: Does this borrower belong in the SBA channel at all? If the answer is no, nothing else in the file matters.

The second pillar is for-profit operating purpose. Lenders want to see a business with a legitimate commercial purpose and a clear revenue model. The owner should be able to explain what the company does, who it serves, how it gets paid, and why the financing supports that operation.

Weak files usually get vague here. “We want flexibility” is not a credit story.

A lender can work with this: “We are buying a service business with recurring contracts, and the loan covers acquisition costs, closing costs, and working capital during the ownership transition.”

The third pillar is eligible and well-defined use of proceeds. SBA financing works best when the request is specific. Working capital, equipment, commercial real estate, partner buyouts, business acquisitions, and certain refinances can all be financeable, but the file improves when the borrower shows exactly where the money goes and what business result it supports.

Underwriters also check whether the structure fits the purpose. Equipment with a shorter useful life, a seasonal working capital need, and an owner-occupied real estate purchase should not all be framed the same way. If the use of funds is vague, the lender starts wondering whether the borrower has a plan at all.

A short explainer is helpful here:

Then prove the file is fundable

The fourth pillar is credit elsewhere and overall fundability. Business owners often misunderstand this rule. It does not mean you must collect denials from every conventional bank first. It means the lender must document why this SBA structure makes sense for this request under SBA rules, including the credit elsewhere test in the SOP.

In practice, eligibility becomes a fundability blueprint. The lender is asking: Is the request reasonable? Is the structure supportable? Does the balance sheet make sense? Owners who understand basic financial presentation have an advantage here. Even a simple grasp of understanding asset vs liability helps borrowers explain what they own, what they owe, and why the business can carry new debt.

Repayment still drives the decision. If cash flow is thin, the lender may reduce the request, ask for more equity, or decline the file even if the borrower checks every basic eligibility box. Owners who want to position the file well should understand how lenders calculate repayment capacity, especially DSCR for SBA loan approval.

The strongest SBA files do more than meet minimum rules. They make the credit decision easy to defend.

That is the main point of these four pillars. Eligibility gets your file in the door. A well-structured, well-explained request gives a lender a reason to say yes.

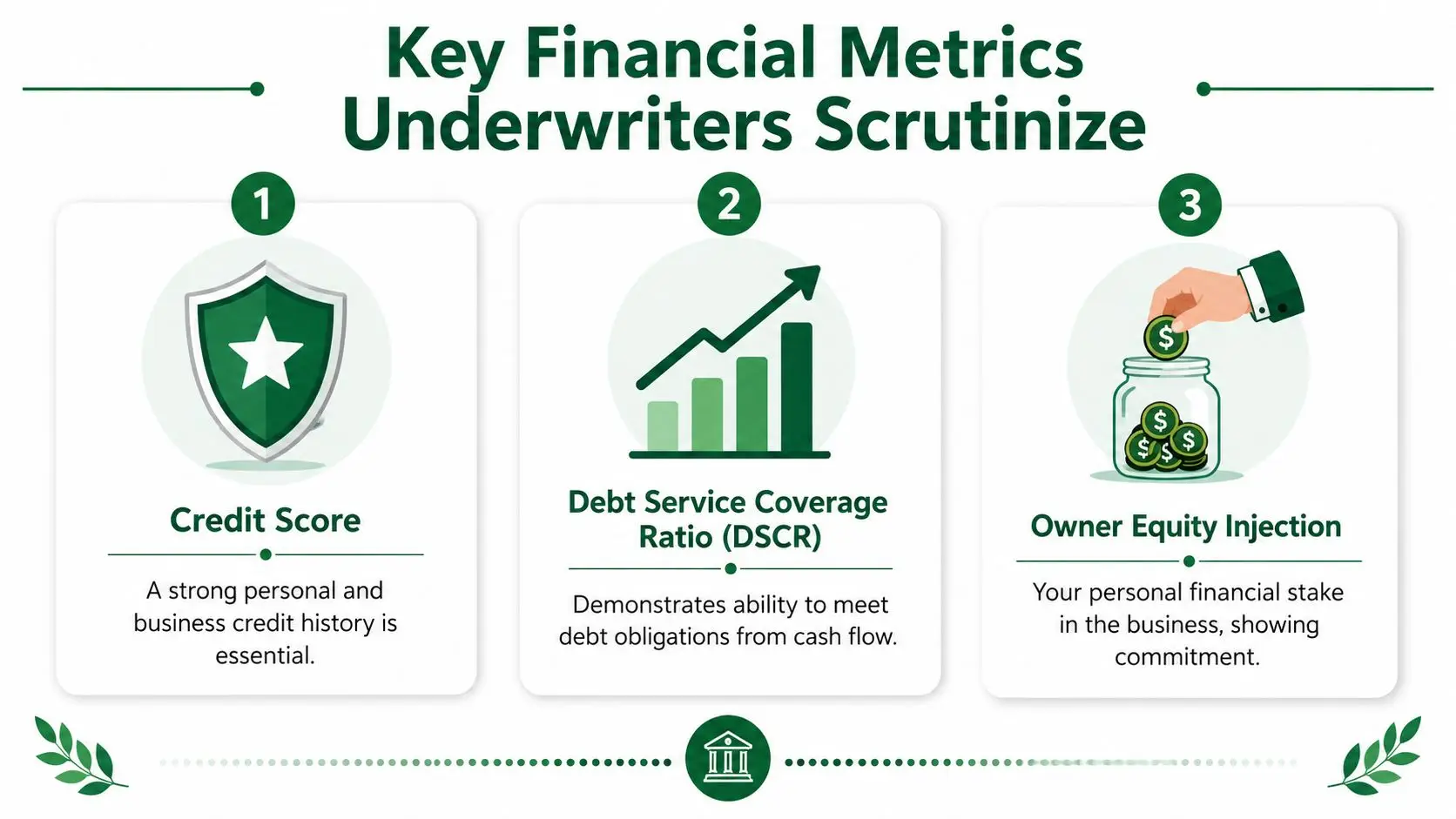

Key Financial Metrics Underwriters Actually Scrutinize

A borrower can look strong on paper and still lose momentum in underwriting once the numbers get stress-tested. This is the point where lenders stop talking about goals and start asking a simpler question. Can this business carry the new payment and still function like a real business when something goes wrong?

Cash flow gets tested first

Cash flow leads the file.

Underwriters usually start with debt-service coverage ratio, or DSCR, because repayment is still the center of the credit decision under SBA rules. They want to see enough operating cash flow to cover all required debt payments, including the proposed SBA loan, with a reasonable cushion. A file with thin coverage can still be discussed, but it becomes harder to defend, especially if the business has uneven revenue, customer concentration, or recent margin pressure.

That cushion matters for a practical reason. Businesses miss forecasts all the time. Receivables slow down. Repair bills show up. Costs rise before pricing catches up. A request that only works in a best-case month is a weak SBA file.

If you want a clearer view of how lenders test repayment capacity, read this guide on what DSCR means for SBA approval before you hand over projections.

Three mistakes come up often in files that stall:

- Pushing add-backs too far. If an expense is discretionary, one-time, or owner-specific, document it clearly. If you cannot prove it, many lenders will not give you credit for it.

- Leaving out existing obligations. Underwriters will include current term debt, equipment loans, seller notes, and often new lease commitments when they size repayment.

- Assuming immediate post-close growth. Expansion may be reasonable, but lenders prefer a base case that works before the upside shows up.

Underwriting lens: A deal should survive conservative assumptions. If repayment depends on everything going right, the structure is weak.

Credit, liquidity, and balance sheet quality still matter

Strong cash flow helps, but it does not erase weak credit habits or a thin personal liquidity position. SBA lenders review personal credit because closely held businesses rise and fall with owner behavior. Repeated late payments, tax issues, unresolved collections, or disorderly debt management raise a different concern. They suggest future payment problems, not just past mistakes.

Liquidity matters for the same reason. Owners do not need unlimited cash, but they do need some room for error. Acquisitions, startups, and expansion requests get more scrutiny here because the business may hit a rough patch before the new debt has had time to produce results. A borrower with no reserve cash and no fallback plan creates a fragile file, even when historical cash flow looks acceptable.

Balance sheet quality is another separator between approvable files and messy ones. Underwriters compare what the borrower says with tax returns, interim financials, debt schedules, and personal financial statements. If assets are overstated, liabilities are missing, or related-party debt is described inconsistently, confidence drops fast. Borrowers who need a refresher before filling out those forms should review understanding asset vs liability.

A lender's checklist is usually straightforward:

- Does historical cash flow support the proposed payment?

- Does the owner's credit history show responsible handling of obligations?

- Is there enough liquidity to absorb normal business volatility?

- Do the financial statements, tax returns, and personal disclosures line up?

A file does not need to be perfect. It does need to be coherent, supportable, and easy for the lender to explain in credit memo form. That is the blueprint. The numbers have to make sense on their own, and they have to hold together under questions.

Demystifying Collateral and Personal Guarantees

Borrowers often fixate on collateral because it feels tangible. The bigger issue is usually the combination of collateral, repayment ability, and guarantee support. An SBA lender wants all three aligned, but they don't carry equal weight.

What fully secured really means

For 7(a) lending, the SBA says a loan is considered fully secured when the lender takes security interests in the assets being acquired, refinanced, or improved, plus available fixed assets up to the loan amount, according to the SBA's guidance on 7(a) loan types, collateral, and terms.

That language is important because many borrowers assume a collateral shortfall automatically kills the deal. It often doesn't. What the lender wants is a lien position on the available business assets and, where applicable, other available fixed assets. The practical question isn't “Is there perfect collateral?” It's “Has the lender taken what the SBA expects the lender to take?”

The asset being financed also affects term. Most 7(a) maturities are 10 years or less, but if the loan finances real estate or equipment with a useful life beyond that, the term can extend up to 25 years, based on the SBA's 7(a) term rules. That's why owner-occupied real estate and equipment-heavy projects often cash-flow better on paper than working-capital requests of similar size.

Why guarantees matter so much

A personal guarantee isn't just a form to sign at closing. It tells the lender that the owner stands behind the obligation beyond the business entity itself. In practical underwriting, that matters because small businesses can change quickly. A guarantor gives the lender another layer of recourse and another reason to believe the borrower will stay engaged when business conditions tighten.

Here's what borrowers get wrong. They assume collateral replaces repayment strength, or that strong cash flow makes guarantees irrelevant. Neither is true. Lenders still care most about repayment from operations. Collateral is a secondary source. Guarantees reinforce accountability.

If repayment depends on liquidation, it was a weak credit decision to begin with.

Good borrowers deal with this head-on. They disclose available collateral early, explain any gaps without spin, and understand that a guarantee is part of the SBA framework, not a sign the lender distrusts them personally.

Choosing Your Path 7a vs 504 vs Express Loans

A lot of SBA frustration starts with choosing the wrong product. Borrowers ask for “an SBA loan” as if it's one thing. It isn't. The right structure depends on what you're buying, what you're refinancing, how flexible the proceeds need to be, and how much lender discretion the deal requires.

How to match the program to the project

The 7(a) program is the workhorse. It's usually the right place to start for business acquisitions, partner buyouts, working capital, certain refinances, and mixed-use projects where proceeds don't fit neatly into a single fixed asset bucket. For most 7(a) loans, the SBA guaranty is 85% for loans of $150,000 or less and 75% for loans above $150,000, and the standard maximum loan amount is $5 million, according to the SBA's 7(a) terms, conditions, and eligibility guide.

That split matters in real underwriting. Smaller 7(a) loans can be easier for lenders to stomach because the guaranty is stronger. Once the request rises above that smaller-loan tier, the lender keeps more risk and usually becomes stricter on cash flow quality, structure, and borrower profile.

The 504 program is different. It's best suited for owner-occupied commercial real estate and major equipment. If the primary goal is to buy or improve long-term fixed assets, 504 often deserves a hard look because the structure is built around those assets rather than broad business-purpose flexibility.

The Express option is for speed and smaller requests, not for every borrower. SBA Express loans are capped at $500,000 and receive a 50% guaranty, while Export Express uses a 90% guaranty structure within the same cap, as outlined by the SBA in its 7(a) program terms. That lower standard Express guaranty can make some lenders more selective even though the process is designed to move faster.

SBA Loan Program Comparison

| Feature | SBA 7(a) Loan | SBA 504 Loan | SBA Express Loan |

|---|---|---|---|

| Best use case | Broad business purposes, including acquisitions, working capital, refinance, and real estate | Owner-occupied real estate and major equipment | Smaller financing needs where faster turnaround matters |

| Flexibility of proceeds | High | Narrower, focused on fixed assets | Moderate |

| Standard size reference | Up to $5 million under the SBA's standard 7(a) framework | Structure varies by project and fixed-asset use | Capped at $500,000 |

| Guaranty structure | 85% at $150,000 or less, 75% above that | Different program structure than standard 7(a) guaranty discussion | 50% standard Express guaranty |

| Typical borrower fit | Buyers and owners needing a versatile structure | Businesses buying property or heavy equipment for operations | Borrowers with smaller, simpler requests |

A practical approach to this:

- Choose 7(a) when you need flexibility.

- Choose 504 when the project is clearly tied to long-term fixed assets.

- Choose Express when the need is smaller and speed is a major priority.

Borrowers get in trouble when they force a project into the wrong box. A lender can fix some structural issues, but not all of them.

The Essential SBA Loan Application Checklist

A strong SBA application feels organized before underwriting even begins. That doesn't mean fancy. It means complete, internally consistent, and easy to review. The fastest way to create friction is to make the lender hunt for missing pieces.

What every lender wants early

Most lenders will ask for the same core categories up front, even if the exact forms vary by bank.

- Personal borrower documents. Personal financial statements, personal tax returns, identification, and background details for the principals.

- Business financial records. Business tax returns, profit and loss statements, balance sheets, debt schedules, and business bank statements.

- Entity and legal records. Formation documents, operating agreements or bylaws, licenses, leases, and ownership breakdowns.

- Use-of-funds support. Purchase agreements, equipment quotes, refinance statements, or a clear breakdown of working-capital need.

- Narrative support. A business plan, acquisition memo, or operating summary that explains the request in plain English.

What matters is not just having the documents. It's whether the documents agree with each other. If tax returns say one thing, the interim financials say another, and the borrower summary says something else, the file slows down immediately.

A practical fix is to build a lender folder before you ever apply. Label files clearly. Use consistent entity names. Reconcile dates. If your accounting team exports messy reports, clean them before sending them out.

For businesses that process large invoice volumes, operations often get cleaner when accounts payable data is standardized before financials are prepared. This guide to invoice OCR for AP teams is a useful resource if you're trying to reduce manual document cleanup before packaging a loan request.

What borrowers often forget

The missing pieces are rarely dramatic. They're usually small credibility leaks.

A disorganized file tells the lender the business may be disorganized too.

Common omissions include:

- Ownership detail. Lenders need a clear view of who owns what.

- Debt explanations. If there are notes payable, explain them.

- Large deposits or transfers. Be ready to show what they were.

- Projection support. If you submit forecasts, tie them to assumptions a lender can follow.

- Deal timeline items. In acquisitions, sellers, brokers, and landlords all create documents that should be assembled early.

Borrowers who prepare the package as if they're answering credit questions before they're asked usually move faster and with fewer revisions.

How to Maximize Your Fundability and Avoid Pitfalls

A borrower walks into a bank asking for $650,000 to buy a business. Tax returns are profitable. The credit score is acceptable. On paper, the deal clears the basic SBA screens. Then underwriting starts asking harder questions. Why does cash flow dip in the off-season? Why is customer concentration missing from the summary? Why does the requested amount include a cushion the borrower cannot explain clearly?

That is where approvals get won or lost.

Meeting SBA loan requirements gets you into the review pile. Fundability is what moves your file toward a credit memo a lender can defend. The difference is not usually one dramatic flaw. It is whether the full package gives the lender confidence in repayment, management judgment, and deal structure.

What strengthens a file

Strong SBA files have a clear credit story. The borrower can explain the use of funds, the repayment source, and the logic behind the structure without wandering. If the request is for an acquisition, explain the transition plan, seller involvement, and how the business performs under new ownership. If the request is for working capital, show exactly what pressure the capital relieves and how that converts into stronger cash flow.

Conservative underwriting assumptions also help. Borrowers get in trouble when they push every add-back, assume immediate growth, or gloss over obvious issues like seasonality, customer concentration, or margin compression. A lender has already seen those risks. Addressing them directly makes the file stronger because it shows management understands the business the way a credit officer does.

Lender fit matters more than many borrowers realize.

A good file can still die in the wrong shop. Some SBA lenders like partner buyouts and acquisitions. Some want owner-occupied real estate with clean historicals. Some are much more comfortable with smaller working capital requests, especially when the structure and guaranty make the credit easier to support. Matching the deal to lender appetite saves weeks of back-and-forth and avoids unnecessary declines.

Borrowers from underserved markets may also find receptive lenders when the deal is packaged well and presented to institutions that actively serve those segments. The edge is not in checking a demographic box. The edge is in sending a well-supported request to a lender whose program priorities match the deal.

What kills momentum

Underwriting usually slows for predictable reasons:

- Aggressive add-backs. If every expense is framed as discretionary, the lender will recast cash flow more conservatively and question management credibility.

- Unexplained blemishes. Prior late payments, tax issues, or short-term losses are often workable if they are disclosed early and explained well.

- Vague use of funds. “General business purposes” is weak unless the file shows what the money does and how repayment improves.

- Structure mismatch. Requesting the wrong SBA product, the wrong term, or more money than the business can justify creates avoidable friction.

- Weak transition planning. In acquisitions, lenders want to know who keeps customers, trains staff, and protects revenue after closing.

Another common mistake is asking for the maximum amount before proving the minimum amount needed. Borrowers assume a larger request gives them room. Underwriters often see it as weak planning. A right-sized request with a clear purpose is easier to approve than a padded request built around “just in case.”

The practical move is to review your file the way a credit committee will. Can a lender explain this deal in two minutes? Do the numbers support the ask after normal underwriting adjustments? Are the risks identified and answered before the lender has to ask?

If the answer is yes, your odds improve fast.

If you want help structuring an SBA deal before you waste time with the wrong lender, GoSBA Loans can help you assess fundability, package the file properly, and find the SBA lending path that fits your business, acquisition, or real estate project.