You found a business that makes sense on paper. The seller accepted the broad terms. You can see yourself running it. This is the point where many buyers relax too early.

The financing stage decides whether the deal closes, how much cash you keep after closing, and how much pressure the business carries on day one. A loan to buy a business isn't just a funding tool. It's the framework that shapes your risk, your monthly obligations, and your room to operate once the ink dries.

That's the good news too. This isn't a niche corner of lending. The U.S. small-business financing market is a mature $1.4 trillion ecosystem, with depository-institution small-business loans growing from $173 billion in 1995 to $368 billion in 2019, plus an estimated $25 billion in online-lender credit outstanding in 2019 and another $300 billion in commercial real estate loans, according to the Bipartisan Policy Center's overview of the small-business financing market. Buyers who understand that market stop thinking in terms of “Can I get a loan?” and start asking the better question: “How should this deal be structured so a lender wants it?”

That's the shift that matters.

Table of Contents

- Your Next Step After Finding the Perfect Business

- Choosing Your Financing Path The Loan Options

- Qualifying for Your Business Acquisition Loan

- Assembling Your Lender-Ready Application Package

- Structuring the Deal to Maximize Fundability

- The Acquisition Timeline From Term Sheet to Close

- Common Pitfalls and Pro Negotiation Tips

Your Next Step After Finding the Perfect Business

A signed LOI feels like progress because it is. But it's also where weak deals start to break apart. Buyers often assume the hard part was sourcing the business, getting access to financials, and agreeing on price. In reality, that work only gets you to the starting line.

The next step is proving that the deal is financeable on terms you can live with. Those are not the same thing. A business can be attractive and still be hard to finance if the structure is wrong, the seller is inflexible, the cash flow story is messy, or the buyer hasn't framed the transaction the way lenders need to see it.

What lenders care about isn't mystery. They want to know who is buying, what they're buying, how the debt gets repaid, and what happens if the projections don't go as planned. Buyers who win financing quickly don't just submit paperwork. They present a coherent transaction.

The cleanest acquisition files tell one consistent story from LOI to closing. Price, terms, buyer background, and cash flow all support each other.

That's why the financing strategy should start before you send the full package to any bank. If the seller note is structured badly, if the working capital need isn't accounted for, or if the purchase agreement doesn't match the loan request, you've already created friction.

What strong buyers do early

- Pressure-test the deal structure: They ask whether the proposed price, note terms, and post-close cash needs work under lender scrutiny.

- Match the lender to the transaction: A general commercial lender may be fine for some deals, but acquisitions usually move better with lenders that regularly underwrite business purchases.

- Treat financing as part of negotiation: They don't separate purchase terms from loan terms because each affects the other.

A loan to buy a business works best when the buyer treats it as part underwriting exercise, part deal architecture. That's the mindset that gets files approved and closes transactions with fewer surprises.

Choosing Your Financing Path The Loan Options

The financing path changes the entire personality of the deal. It affects how much cash you bring in, how much flexibility you have after closing, and how much negotiating power you need from the seller.

For many small business acquisitions, the anchor option is the SBA program. The SBA states its loan programs can range from $500 to $5.5 million, and it says those loans may be used for “establishing a new business or assisting in the acquisition, operation or expansion of an existing business.” The Federal Reserve reported the average SBA loan amount was about $480,000 in FY 2023, which is one reason SBA lending sits at the center of many acquisition transactions. Those details appear on the SBA funding programs and loans page.

Where SBA fits

SBA-backed acquisition loans usually make the most sense when the buyer wants longer repayment terms, lower cash outlay than a conventional bank would typically require, and a structure that can accommodate intangibles like goodwill.

Conventional bank loans can work well too, especially when the buyer is very strong, the target has clean financials, and the bank has real comfort with the industry. But conventional credit usually gets tougher when goodwill makes up a meaningful share of the price, or when the buyer needs more flexibility in the capital stack.

Seller financing is not a standalone replacement in most deals. It's a strategic layer. It can bridge a valuation gap, show lender confidence in the business, and reduce the amount of cash the buyer has to bring.

If you're comparing acquisition debt with liquidity tools used after closing, it also helps to understand how financing choices affect operations. Teams that want to improve cash flow for CFOs often look at receivables financing separately from acquisition debt, because the wrong mix can leave a business carrying too much debt even if the purchase loan itself was approved.

How the options compare in practice

| Feature | SBA 7(a) Loan | Conventional Bank Loan | Seller Note |

|---|---|---|---|

| Typical role in acquisition | Primary senior financing for many small business purchases | Primary financing for stronger borrowers and cleaner deals | Supplemental financing layer |

| Loan size reference | SBA programs range from $500 to $5.5 million | Varies by bank and transaction | Negotiated between buyer and seller |

| Average size reference | About $480,000 in FY 2023 for SBA loans | No verified comparable figure provided | No verified comparable figure provided |

| Best use case | Goodwill-heavy acquisitions, first-time buyers with solid profiles, longer-term amortization needs | Borrowers with strong balance sheets, strong collateral, and very bankable targets | Bridging a gap in equity or valuation |

| Main trade-off | More documentation and tighter process discipline | Less forgiving structure if the deal has complexity | Terms depend entirely on seller flexibility |

| What lenders focus on | Cash flow, buyer profile, deal structure, full package | Buyer strength, collateral, business quality | Whether note terms support the senior loan |

One mistake I see often is buyers choosing the lender before choosing the structure. That's backwards. The right sequence is: design the deal, identify the underwriting story, then target lenders that fit that story.

For a deeper look at program fit, eligibility, and lender expectations, this guide to SBA 7(a) loans in 2026 requirements rates and how to qualify is a useful reference point.

Practical rule: If the seller won't cooperate on terms and the business has thin room for debt service, financing gets harder fast no matter how attractive the business looks.

Qualifying for Your Business Acquisition Loan

Lenders don't underwrite an acquisition the same way they underwrite a simple working capital request. They're evaluating a transfer of ownership, not just a request for money. That means they're looking at you and the business at the same time.

Lenders underwrite two borrowers

The first borrower is obvious. It's you. Lenders want to know whether you've managed people, budgets, operations, or client relationships in a way that translates into ownership. Direct industry experience helps, but execution experience matters too. A buyer with solid leadership history and a clear operating plan usually presents better than a buyer who says, in effect, “I'll figure it out.”

The second borrower is the business itself. The lender has to believe the company's historical earnings can support the new debt after normalizing the financials and reviewing the transition risk. That's why lenders dig into contracts, lease terms, inventory quality, customer concentration, and the overall consistency of the earnings picture.

The practical workflow for an SBA-style acquisition loan reflects that dual review. Borrowers choose the loan program and lender, submit a full package that includes forms such as the borrower application and personal financial statement, and then the lender evaluates the target company's ability to service debt while reviewing the buyer's investment and diligence materials, as outlined in this SBA loan to buy a business overview from FBLake Bank.

What makes a file feel bankable

A lender-ready borrower usually has most of these elements lined up:

- Relevant management depth: You don't need a perfect mirror image of the seller's background, but you do need a believable plan for running the business on day one.

- A stable personal profile: Clean financial conduct, reasonable liquidity, and an explanation for any blemishes matter more than polished talking points.

- Real money in the deal: Lenders want to see that the buyer has something at risk and understands the consequences of the transaction.

- A target with understandable earnings: If the business needs excessive add-backs or has inconsistent books, the underwriting story weakens.

- A transition plan: Training, handoff support, and continuity with staff, customers, and vendors often matter more than buyers expect.

Buyers get declined for weak narratives as often as for weak numbers. If the lender can't see how ownership transfers without disruption, the file feels riskier.

The strongest applications also avoid overreaching. If the price assumes flawless future execution, if the buyer has no operating backup, or if the acquisition vehicle is poorly planned, the lender starts to question the whole transaction. A loan to buy a business gets approved when the buyer, business, and structure reinforce each other.

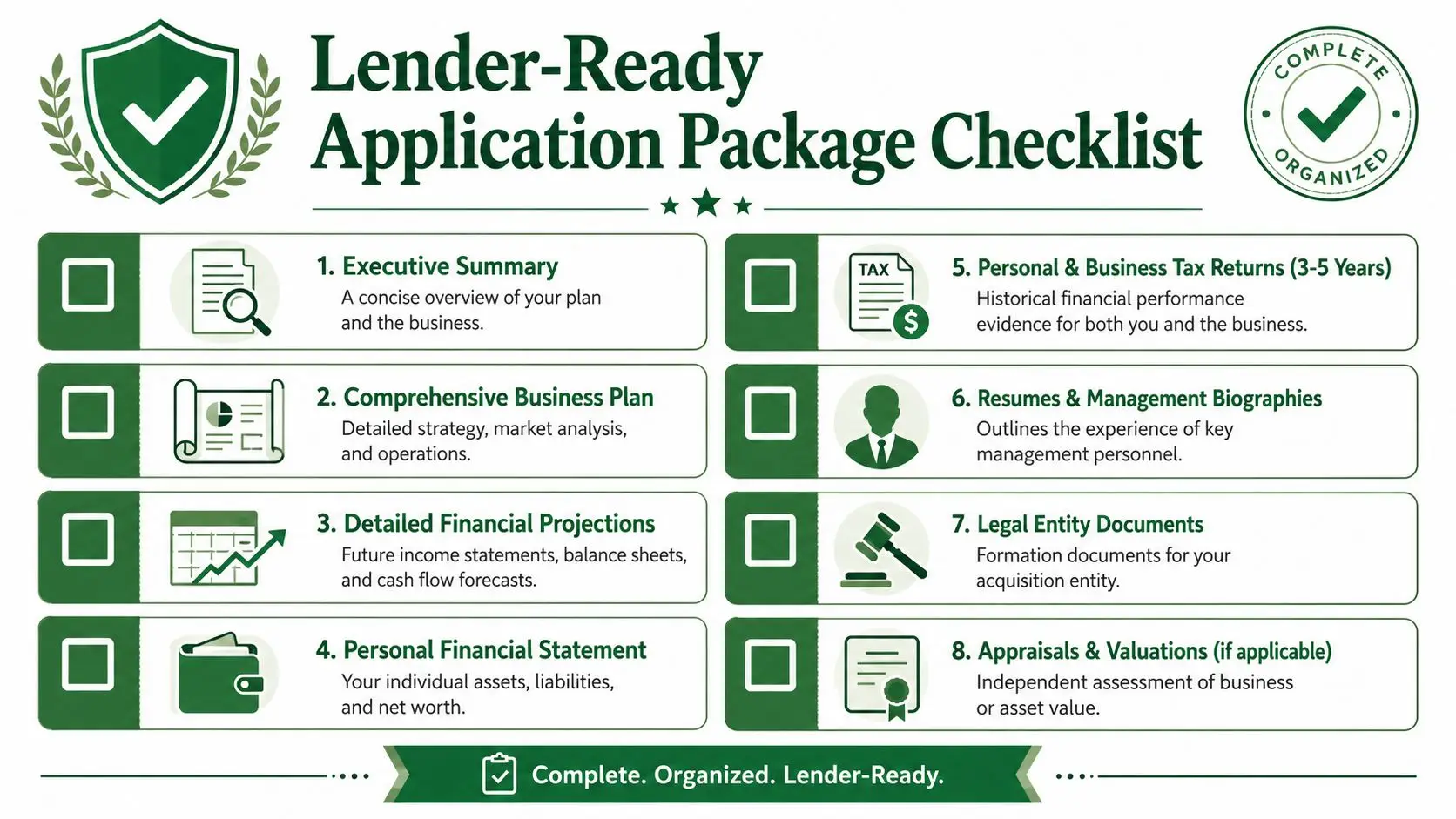

Assembling Your Lender-Ready Application Package

The fastest way to slow down underwriting is to send an incomplete file. Lenders can work quickly when the package is coherent. They stall when they have to chase basic items, reconcile conflicting numbers, or ask what the transaction even is.

Build the file before the lender asks

At minimum, I want buyers thinking about the package in layers.

The first layer is the deal file. That includes the LOI, a draft purchase agreement when available, a breakdown of sources and uses, and a plain-English explanation of what is being bought. Asset purchase or stock purchase. Working capital included or excluded. Seller transition support. Any consulting agreement. Any seller note. If those points aren't clear, the lender can't underwrite efficiently.

The second layer is the borrower file. That's your personal financial statement, resume, background explanation if needed, entity documents for the buying entity, and anything else that helps a lender understand your capacity to own and operate the target.

The third layer is the business file. Historical tax returns, interim financials, debt schedule, and supporting documents for major business obligations all belong here.

A complete file matters because underwriting can move fast once the lender has everything. One lender source says underwriting can be done in as quickly as 24 hours once the file is complete, although acquisition financing more broadly often takes several weeks to a few months from start to finish, according to National Funding's explanation of the underwriting process.

Here's a useful due diligence reference if you want a working checklist for the target itself: business acquisition due diligence checklist for SBA loan buyers.

What strong submissions have in common

A strong package doesn't just contain documents. It answers lender questions before they're asked.

- Executive summary: This should explain who you are, what you're buying, why the business fits your background, and how the debt gets repaid.

- Financial projections: These need to be grounded in the actual business, not fantasy growth. Conservative assumptions are easier to defend than aggressive ones.

- Personal financial statement: Lenders use this to verify liquidity, obligations, and overall financial discipline.

- Tax returns and interim financials: These support the earnings story and help the lender test consistency.

- Entity and legal documents: These keep closing counsel from having to clean up preventable issues late in the process.

This video gives a practical overview of how buyers should think about the file and financing process before submission.

Sloppy files create a hidden tax on the transaction. Every missing statement, unexplained transfer, or mismatched version of the purchase price costs time and confidence.

The best application packages feel boring in the right way. Everything is labeled. The numbers tie. The story is clear. Underwriters like files that don't make them guess.

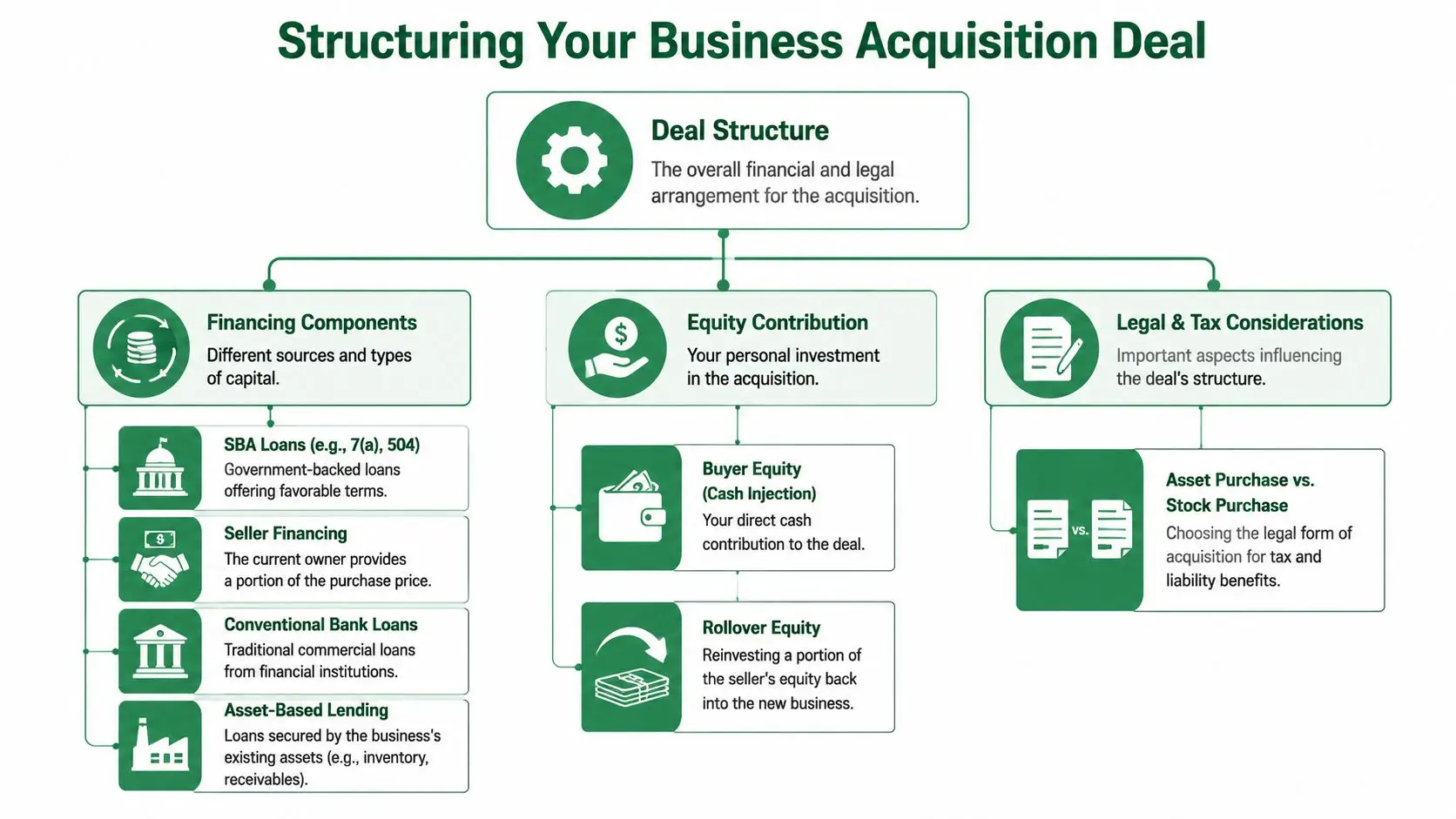

Structuring the Deal to Maximize Fundability

Most buyers spend too much time negotiating price and not enough time negotiating structure. Price matters, but lenders often have an easier time with a well-structured higher-quality deal than with a poorly structured cheaper one.

The best structures solve three problems at once. They reduce the buyer's immediate cash burden, protect the senior lender's position, and keep the seller economically tied to a successful transition when appropriate.

Seller notes investor equity and smart stacking

Seller financing is one of the most useful tools in acquisition lending because it can make a borderline deal financeable. But not every seller note helps. Some hurt.

A lender wants the seller note to support, not compete with, the senior loan. If the seller expects aggressive repayment right away, or if the note terms put pressure on early cash flow, the structure may look weaker than if the seller had reduced the price. A properly subordinated seller note can show confidence from the seller and preserve buyer liquidity. A badly drafted one can become a closing problem.

Investor equity can also be useful, especially when the buyer is operationally strong but wants to preserve cash. The key is alignment. Lenders need clarity on who owns what, who guarantees what, who controls the business, and whether the investor structure creates governance issues after closing.

Here's what usually works better:

- Seller note with clear subordinated terms: This tells the lender the seller is still invested in a successful handoff.

- Buyer equity that is clearly sourced: If funds are coming from savings, gifts, or investors, document the source early.

- Simple cap table design: Complicated ownership structures create legal and underwriting friction.

- Real post-close liquidity: Don't drain every dollar into the closing table and assume the business will self-fund every surprise.

What usually doesn't work is overengineering. Buyers sometimes try to stack too many moving parts into one deal. Multiple investors, unclear repayment side agreements, messy intercreditor issues, and unresolved legal structure questions make lenders nervous for good reason.

If you're working through asset purchase versus stock purchase issues, reps, warranties, and deal paper, this guide on understanding asset acquisition legalities is worth reviewing alongside your attorney.

When pari passu and collateral structure matter

Pari passu structures can help in the right transaction, especially when two lenders share senior lien position or when part of the deal needs to be split in a way that still keeps the capital stack workable. But they only help if the lenders are aligned and the collateral package is clear.

Collateral becomes a real issue when a business purchase includes equipment, receivables, inventory, real estate, or a meaningful goodwill component. Buyers often misunderstand this part. They assume collateral either fully solves the lender's concern or doesn't matter at all. Neither is true. In acquisition lending, collateral supports the file, but cash flow and structure still drive the approval story.

For a practical look at lender expectations around pledges and business assets, review SBA collateral requirements and what you need to pledge for an SBA loan.

One useful option in this market is a broker that can place complex structures across multiple SBA-focused lenders. For example, GoSBA Loans works on SBA acquisition financing and can coordinate lender matching, underwriting support, and structures that may include seller notes, investor-heavy stacks, or pari passu components.

The right structure makes the lender's risk easier to understand. The wrong structure makes everyone feel like there's a side deal they haven't found yet.

A loan to buy a business becomes much easier to place when the structure is simple enough to explain and strong enough to survive scrutiny.

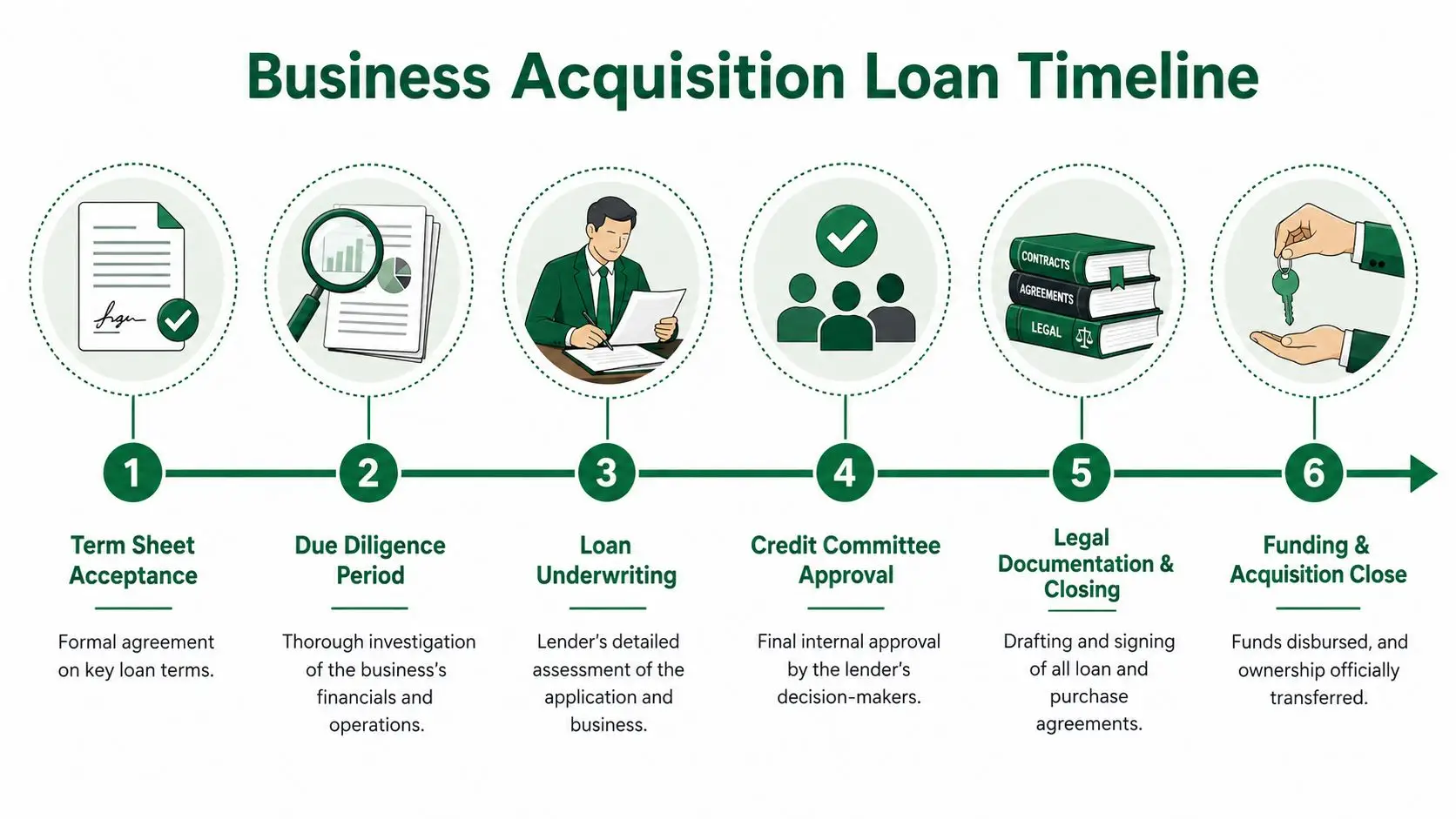

The Acquisition Timeline From Term Sheet to Close

Once you have a lender term sheet in hand, the deal becomes a project management exercise. Good closings rarely happen because everyone “moves fast.” They happen because the right items get handled in the right order.

What happens first

After term sheet acceptance, the lender usually moves into formal underwriting while the buyer and seller continue diligence and legal drafting. At this stage, buyers often underestimate the importance of responsiveness. If the lender asks for clarifications, updated statements, revised purchase terms, or supporting documents, delays compound quickly.

At the same time, third-party work often starts. That may include valuation, legal review, and property-related reports if real estate is part of the transaction. These items tend to matter because they affect not only underwriting but also closing counsel's ability to finalize documents.

A clean acquisition timeline usually looks like this:

- Term sheet accepted

- Underwriting file opened

- Diligence and third-party reports ordered

- Credit approval issued with conditions

- Legal documents drafted and cleared

- Funds disbursed and ownership transfers

What usually slows closings down

The biggest delays are usually not mysterious. They are avoidable.

- Incomplete diligence responses: Missing contracts, tax documents, or payroll records create repeated back-and-forth.

- Purchase agreement changes late in the process: If buyer and seller renegotiate key terms after underwriting is advanced, the lender may need to revisit approval.

- Entity problems: Incorrect ownership docs, missing resolutions, or unclear guarantor structure can delay legal.

- Third-party report lead times: These often sit on the critical path even when everything else is ready.

A useful rule is to treat the lender, attorney, accountant, and seller as one closing chain. If one party goes quiet, the whole process drifts.

Closings stall when buyers wait for requests instead of driving the checklist themselves.

The buyers who close more smoothly usually keep one master list with owners and deadlines attached to each item. That sounds basic because it is. Acquisition finance rewards basic discipline.

Common Pitfalls and Pro Negotiation Tips

Most failed deals don't die because the business was impossible to finance. They die because the buyer let avoidable weaknesses stay in the file too long.

Mistakes that kill good deals

The first mistake is assuming the lender will “figure out” a messy structure. They won't. If the seller note is unclear, the working capital ask is unsupported, or the investor arrangement is poorly documented, the lender reads that as execution risk.

The second mistake is choosing a lender that doesn't regularly handle acquisitions. Commercial lending experience is not the same as acquisition lending experience. A lender can be excellent at owner-occupied real estate or general business credit and still be clumsy with goodwill-heavy purchases, transition support, and seller carry structures.

The third mistake is negotiating only purchase price and ignoring business terms that affect financeability. Transition support, consulting periods, training, lease assignment, customer handoff, and non-compete terms can all matter to underwriting because they affect continuity.

The biggest financing mistake is treating the seller note as an afterthought. If it isn't negotiated correctly up front, the buyer usually ends up bringing more cash or rewriting the deal under pressure.

Good negotiation is less about “winning” line items and more about preserving closeability. I'd rather see a buyer secure a cooperative seller note, a realistic transition plan, and clean legal documents than grind out a lower headline price that makes the lender uncomfortable.

A few negotiation habits consistently help:

- Ask for transition support in writing: Verbal promises from the seller don't help underwriting or operations.

- Negotiate structure before legal drafting gets deep: It's cheaper and cleaner to solve financing points early.

- Leave room for lender requirements: If the LOI is too rigid, every lender condition feels like a renegotiation.

- Protect post-close liquidity: Don't negotiate yourself into a deal where every available dollar goes to the seller.

Underserved markets need a different approach

Location matters more than many buyers realize. Financing a business in a rural, low-income, or otherwise underserved market often requires a wider search for capital because access is structurally weaker in those communities. Borrowers in those markets may need to look beyond conventional banks and consider sources such as CDFIs, USDA-backed options, SBICs, and state-level programs, as described in this overview of capital access challenges in underserved markets.

That doesn't mean those deals can't close. It means the capital stack may need to be built differently. In underserved geographies, the question often isn't just whether the borrower qualifies. It's whether the borrower has found the right combination of lender appetite, local program support, and seller flexibility.

If you're trying to finance a business purchase and want help structuring the deal before it gets stuck in underwriting, GoSBA Loans can help you compare SBA lender options, tighten the package, and build a cleaner acquisition financing strategy around the transaction you're purchasing.