You've got a business under LOI, the seller wants proof you can close, and every lender conversation seems to produce a different answer. One bank asks for more collateral. Another wants cleaner financials. A broker tells you SBA is the obvious path, but can't explain how to structure the equity, the seller note, and the closing timeline so the file gets approved.

That's where most first-time buyers get stuck. They think the hard part is finding a loan to buy a business. It usually isn't. The hard part is building a deal that a lender can underwrite with confidence, then keeping that deal intact through closing.

A funded acquisition usually comes down to four things. The target has to show understandable cash flow. The buyer has to look credible as the future operator. The capital stack has to make sense. And the paperwork has to arrive complete, consistent, and early. If one of those breaks, timelines slip and approvals get shaky.

Table of Contents

- Your Guide to Financing a Business Purchase

- Mapping Your Primary Financing Options

- Passing the Underwriting Test

- Assembling a Bulletproof Loan Application

- Structuring the Deal to Maximize Fundability

- Your Lender Selection and Closing Roadmap

Your Guide to Financing a Business Purchase

The cleanest way to think about a loan to buy a business is this: lenders aren't financing your excitement. They're financing a transaction with a borrower, a target company, and a repayment story they can defend.

That's why business acquisition financing feels different from working capital or equipment lending. You're not just asking for money. You're asking a lender to believe that the business will keep performing after ownership changes, that you can run it, and that the deal terms won't unravel halfway through diligence.

Start with sources and uses

Before you talk to lenders, turn the purchase into a sources-and-uses schedule. Total up the acquisition cost, subtract the equity you have available, and identify the amount that needs to be financed. That sounds basic, but many buyers skip it and start shopping lenders with a rough idea instead of a structure.

Lenders underwrite closed transactions, not vague intentions. They want to see how the purchase price, working capital needs, fees, and any related transaction costs fit together. If the business also includes real estate, partner buyout elements, or seller financing, those pieces need to be mapped early, not introduced late.

Practical rule: If you can't explain your capital stack in a few clear lines, your lender can't defend it in credit committee.

Understand what the lender is really buying

A lender will usually review three files at once:

- The borrower file. Your background, liquidity, tax returns, personal financial statement, and operating experience.

- The company file. Historical performance, current financials, bookkeeping quality, and whether the seller's records hold up.

- The transaction file. LOI or purchase agreement, allocation details, timelines, and any side agreements that change risk.

The technical core is straightforward. As TEDC's acquisition loan guide notes, lenders typically expect a signed LOI or purchase agreement, 2 to 3 years of business and personal tax returns, current financial statements, bank statements, personal financial statements, and a written explanation of why the buyer can operate the business successfully. The same guidance flags weak bookkeeping and unclear cash flow as common deal-killers.

What works and what usually fails

A workable file is coherent. The buyer has relevant experience, the seller's numbers reconcile, and the purchase price can be defended. The loan request also matches the deal. If the business needs working capital right after closing, the structure accounts for that instead of pretending day-one cash needs don't exist.

What usually fails is less dramatic. It's incomplete seller records. It's buyer resumes that don't connect to the target. It's a last-minute attempt to change deal terms after underwriting starts. Most bad outcomes in acquisition lending come from avoidable sloppiness, not exotic credit issues.

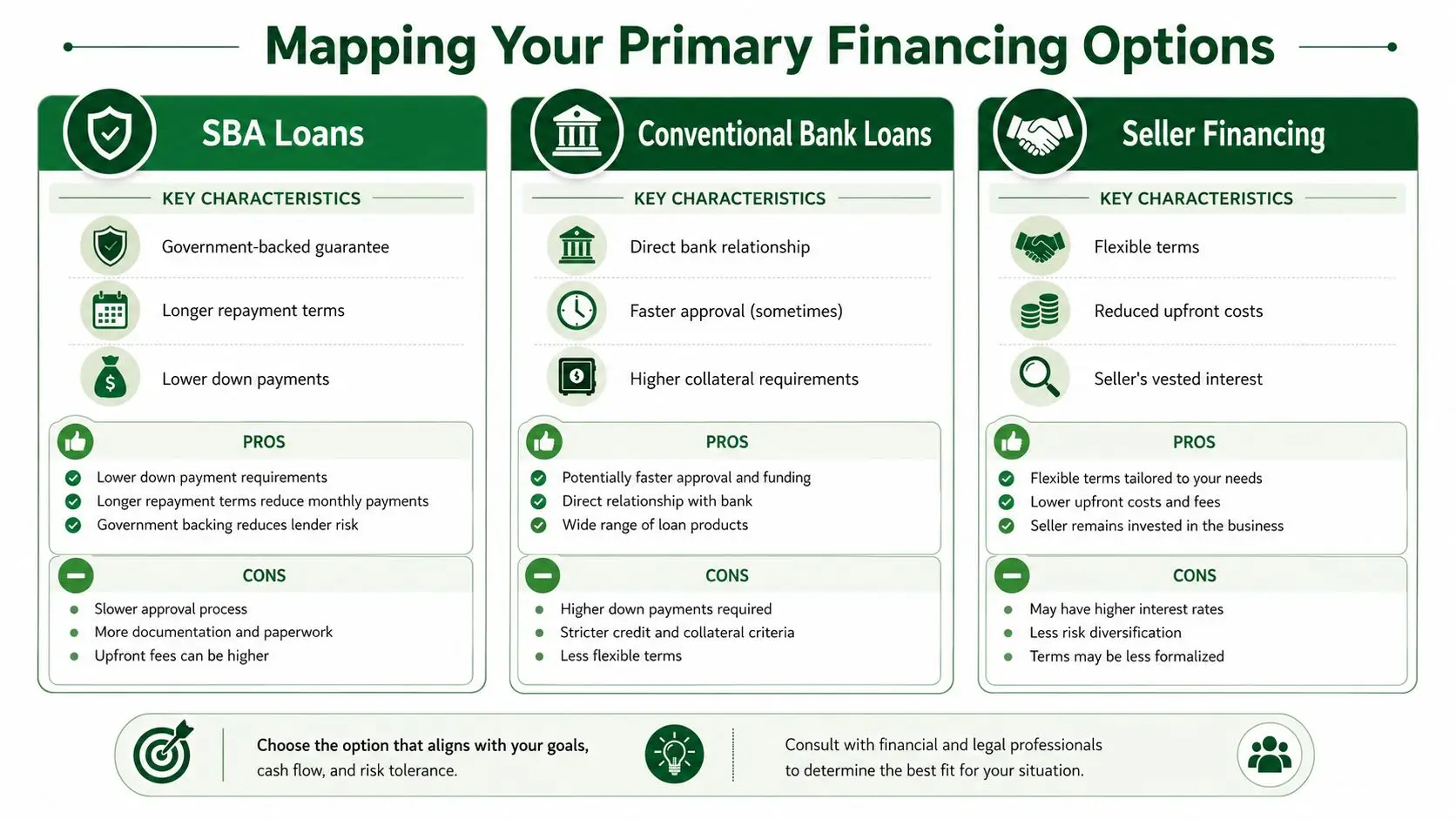

Mapping Your Primary Financing Options

A first-time buyer often starts by asking, “Which loan should I get?” The better question is, “What capital stack gives this deal the best shot at approval and a stable first year after closing?” That is how lenders look at it, and it is how buyers should look at it too.

Three funding sources show up in small business acquisitions again and again: SBA 7(a), conventional bank debt, and seller financing. The mistake is treating them as separate menu items. In real deals, they often work together. A good structure matches the target's cash flow, the buyer's liquidity, the amount of goodwill in the price, and the lender's credit box.

Why SBA 7(a) sits at the center of most small acquisitions

For lower middle-market and Main Street acquisitions, SBA 7(a) is usually the starting point because it gives buyers room to finance goodwill, working capital, and in some cases real estate in one package. The SBA loan programs page confirms that 7(a) loans can be used for business acquisitions and other general business purposes, which is exactly why they show up so often in change-of-ownership transactions.

That flexibility matters. Many acquisition targets are valuable because of recurring cash flow, customer relationships, and operating history, not because they come with enough hard collateral to support a conventional loan on its own. SBA 7(a) can accommodate that reality better than most bank-only structures.

Buyers who want a more detailed explanation of eligibility, structure, and lender expectations should review this SBA 7(a) loan guide for business acquisition borrowers.

One caution from the field. SBA flexibility does not mean lenders stop caring about deal quality. If the business has inconsistent books, customer concentration, or a seller who wants aggressive terms, the file can still stall. The program helps good deals get done. It does not rescue weak ones.

How conventional bank loans compare

Conventional bank financing can price well and close efficiently when the deal is unusually clean. That usually means a strong buyer, a target with solid financial reporting, limited volatility, and enough collateral support or balance-sheet strength to make the bank comfortable without an SBA guaranty.

Banks also tend to have less patience for gray areas. Heavy goodwill, uneven earnings, thin buyer liquidity after closing, or an industry the bank does not like can push the deal out of the conventional channel fast. In those cases, SBA is often the practical answer, not because it is easier, but because it fits acquisition risk better.

| Financing path | Best fit | Main strength | Main weakness |

|---|---|---|---|

| SBA 7(a) | Buyers acquiring operating businesses with strong cash flow but limited hard collateral | Flexible use of proceeds and terms built for acquisitions | More documentation and tighter procedural requirements |

| Conventional bank loan | Very strong borrowers buying highly bankable companies | Competitive bank relationship and simpler structure in the right file | Less tolerance for goodwill-heavy or imperfect deals |

| Seller financing | Transactions with valuation gaps, buyer liquidity pressure, or a seller willing to support the handoff | Can reduce cash needed at close and improve lender comfort | Terms must be structured carefully to work with senior debt |

Seller financing is often part of the approval strategy

Seller financing is not just a fallback for buyers who cannot raise enough cash. Used correctly, it can improve the file. A seller note can reduce the senior lender's exposure, show that the seller believes the business will perform after closing, and help bridge a valuation gap without forcing the bank or SBA lender to stretch.

The details matter. Lenders will look closely at whether the note requires immediate repayment, whether it is on standby, and whether the payment terms create pressure on early cash flow. A poorly structured seller note can hurt approval just as easily as a well-structured one can help it.

Tax problems can also complicate this part of the stack. If either side has unresolved liabilities that could interfere with closing or post-close cash flow, this guide for business tax challenges is worth reviewing before terms are finalized.

Choose the stack that fits the deal

The right financing choice usually follows a clear pattern:

- Start with SBA 7(a) if the purchase price is driven mainly by earnings and goodwill, the buyer needs flexibility, or the transaction includes working capital needs at closing.

- Use conventional debt if the bank already likes the industry, the business is exceptionally clean, and the deal does not need SBA-style flexibility.

- Add seller financing when it improves day-one liquidity, supports valuation, or gives the senior lender more confidence in the transition.

Good buyers do not chase a loan product by name. They build a structure that works for underwriting, works for the seller, and still leaves the business with enough breathing room after the deal closes.

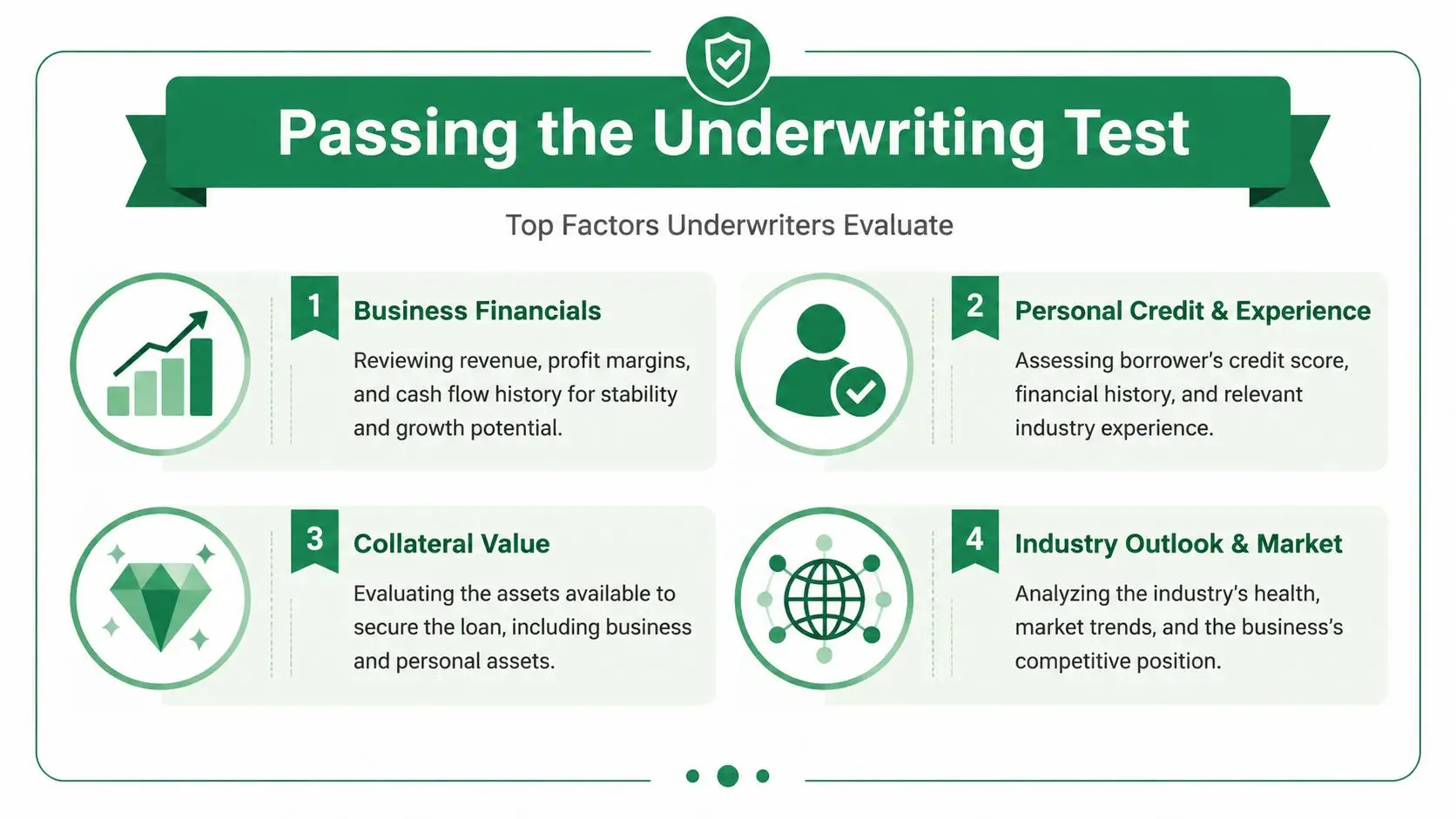

Passing the Underwriting Test

Underwriting is where optimistic deal talk gets replaced by evidence. An underwriter's job is to answer a simple question: if this business changes hands, is repayment still likely and well-supported?

That answer rarely turns on one issue. It comes from the interaction between the company's financial story, the buyer's credibility, the collateral picture, and the transaction itself.

Cash flow is the first test

The target company has to produce understandable, supportable cash flow. Not “promising.” Not “trending in the right direction.” Underwriters want to see records that tie together cleanly enough to support debt service analysis.

If the seller's books don't match tax returns, or if revenue appears concentrated in relationships tied only to the seller, the file gets harder fast. Owner-dependent operations, messy add-backs, and unexplained swings in performance create doubt. Doubt slows approvals.

A useful way to prepare is to read a lender-focused explanation of how SBA lenders underwrite your deal. It helps buyers see why seemingly small inconsistencies trigger major questions.

The buyer still matters, even in a cash-flow deal

A strong company won't carry a weak buyer profile forever. Lenders still need a believable operating handoff. If you've managed teams, owned P&L responsibility, worked in a related sector, or built transferable leadership experience, package that clearly.

What hurts buyers is assuming lenders will “figure it out.” They won't. If your experience is indirect, explain why it still matters. If you're retaining key staff after closing, make that visible. If the seller transition will be important, define it early and consistently.

Personal issues can quietly derail approval

Tax problems, unresolved liens, or major personal financial disorder can turn a good acquisition into a difficult credit. Those issues don't always kill a file, but they need to be addressed directly and early. If a buyer has outstanding tax complications, a practical resource is this guide for business tax challenges, which outlines resolution paths owners often need before or during financing.

Underwriter's view: A problem explained early is manageable. A problem discovered late looks like concealment.

What underwriters flag first

These tend to draw the fastest scrutiny:

- Unclear earnings quality. If the target's cash flow depends on adjustments no one can document, the lender loses confidence.

- Weak transition planning. If customers, staff, or vendors are tied too closely to the departing owner, continuity risk rises.

- Borrower mismatch. A buyer with no visible path to operating the business makes the file harder even if the target is decent.

- Document inconsistency. Different numbers in the LOI, tax returns, and lender intake package force rework.

A lot of buyers over-focus on credit score and under-focus on narrative consistency. Underwriters notice that gap immediately. They're asking whether the entire file holds together, not whether one isolated metric looks good.

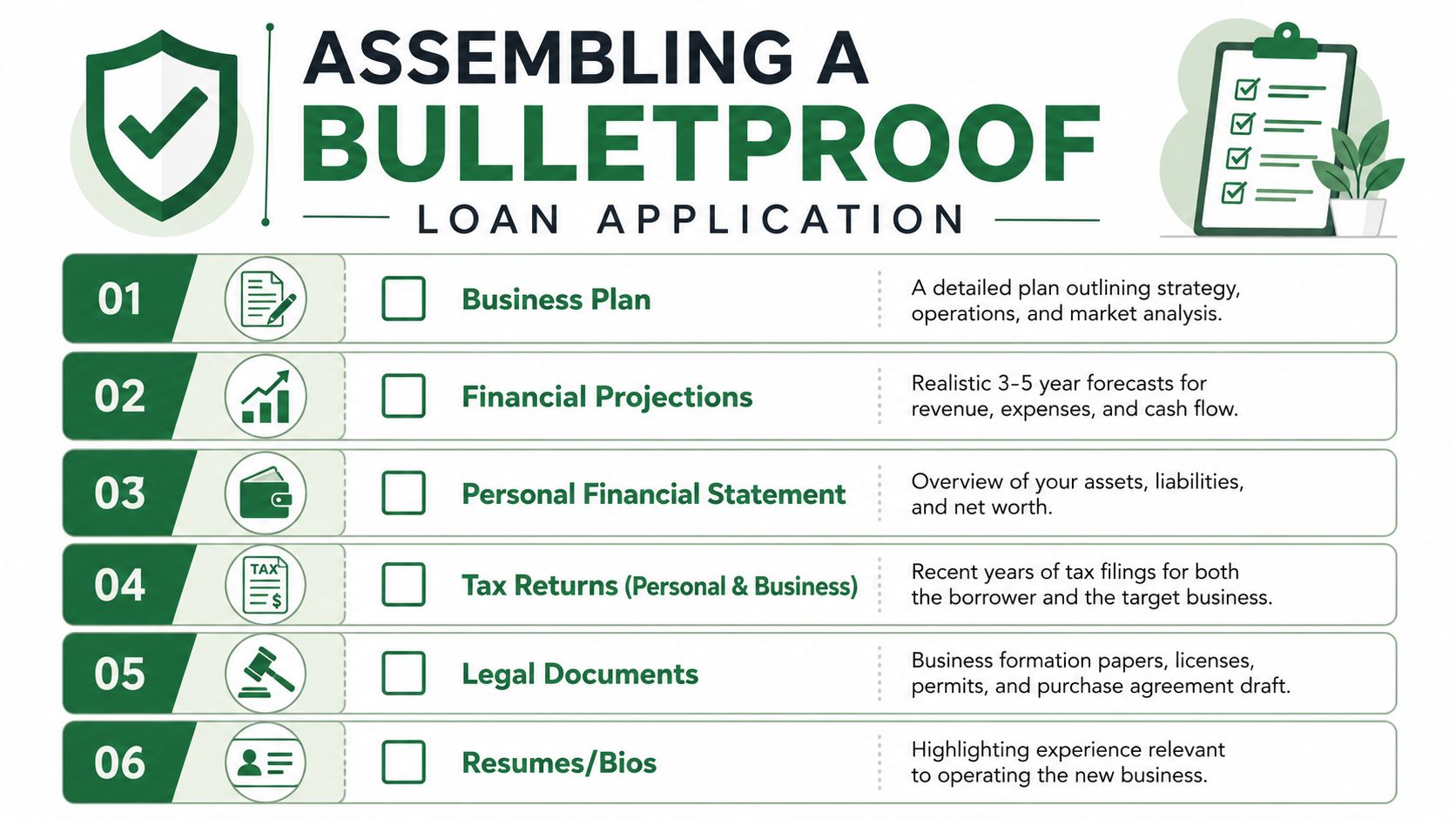

Assembling a Bulletproof Loan Application

A strong application doesn't feel like a dump of PDFs. It reads like a well-supported case file. Every document should answer a lender's question before the lender has to ask it.

That's why organization matters almost as much as content. If an underwriter has to hunt through mismatched file names, stale statements, and unsigned drafts, your deal feels riskier even when the core business is solid.

To orient yourself, start with the checklist below.

Build the package in the order lenders think

Lenders usually review the file in a practical sequence. Transaction documents first. Historical financial support next. Then buyer support. Then any explanatory narrative that ties the package together.

As noted earlier from TEDC's business acquisition lending guidance, lenders typically require a signed LOI, 2 to 3 years of business and personal tax returns, current financials, and personal financial statements, and weak bookkeeping plus poor cash-flow documentation are common reasons deals stall. The fastest way to lose momentum is to submit half the file and promise the rest later.

Here's the basic package most buyers should prepare:

- Signed LOI or purchase agreement. This tells the lender what is being bought and on what terms.

- Business tax returns and current financials. These establish the historical and current earnings story.

- Personal tax returns and personal financial statement. These help the lender assess guarantor strength and liquidity.

- Bank statements and supporting schedules. These help verify available funds and operating stability.

- Buyer resume and operating rationale. This explains why you're the right next owner.

- Deal explanation memo. This connects the business, the buyer, and the structure in plain English.

If you need help completing one of the most scrutinized borrower documents, this walkthrough on the SBA personal financial statement is worth reviewing before submission.

Tell the story behind the paperwork

A loan package works better when it includes a short written explanation that answers practical questions:

- Why this business?

- Why are you qualified to run it?

- What changes after closing?

- What remains stable?

- Where does repayment come from?

That memo doesn't need to be fancy. It needs to be disciplined. If the business relies on one manager who is staying, say so. If the seller is providing a transition period, explain it. If the target's records had cleanup work done before marketing, address that openly.

This video gives a useful overview of how buyers can think about acquisition financing and preparation:

The mistakes that create avoidable delays

Most delays come from ordinary, preventable issues:

- Missing signatures. Draft LOIs, unsigned statements, and incomplete schedules force rework.

- Stale financials. If the deal has moved on but the numbers haven't, underwriting pauses.

- Unexplained discrepancies. If the purchase price in one document doesn't match another, expect immediate questions.

- Overstated confidence. Don't paper over weak records. Acknowledge gaps and show how they've been addressed.

Send documents as if the person reviewing them has never seen the deal before and has no patience for detective work.

That mindset alone improves speed more than most buyers expect.

Structuring the Deal to Maximize Fundability

Most buyers think financing is a lender problem. It's usually a structure problem. A bank can only approve what the transaction allows. If the deal is put together poorly, even a good business becomes hard to finance.

Fundable structures have one trait in common. Everyone's role is clear. Buyer equity is defined. Seller participation is documented. Working capital needs are realistic. Side agreements don't contradict the senior loan request.

Build the capital stack on purpose

A business purchase often needs more than one funding source. Senior debt may cover the core financing. Seller financing may help bridge a gap. In more specialized cases, buyers may need local programs, CDFIs, or guarantee support when the transaction includes property, a partner buyout, or a structure that doesn't fit cleanly into one lender's box.

Public-sector guidance shows that SBA lending can be blended with other channels in more complex deals. The Illinois Treasurer's overview of its business loan guarantee program and related capital pathways highlights how SBA 7(a) and 504 financing may be paired with state guarantee programs and CDFI loans, especially when buyers are navigating property, partner buyouts, or underserved borrowing situations.

That matters because not every good acquisition is a plain-vanilla asset-light purchase. Some include real estate. Some involve a family transition. Some need a layered approach because one capital source alone won't close the gap.

What lenders like in a structure

In practice, lenders respond well when the structure does three things:

- Shows committed buyer equity. The buyer has real skin in the deal and enough liquidity left after closing.

- Uses seller financing thoughtfully. The seller note supports the deal instead of creating repayment pressure too early.

- Preserves operational stability. The business has enough breathing room after closing to operate normally.

A common mistake is forcing the transaction to the maximum debt the spreadsheet can tolerate. Lenders look beyond spreadsheet tolerance. They ask whether the business will still feel stable after debt service, ownership transition, and ordinary surprises.

Real-world complications that need planning

Some acquisitions are financeable only because the buyer anticipates the side issues early.

For example:

| Deal complication | What buyers often miss | Better approach |

|---|---|---|

| Owner-occupied property | Treating the real estate as an afterthought | Address property financing and term implications at the start |

| Partner buyout | Assuming it underwrites like a third-party purchase | Prepare clear ownership, valuation, and transition documentation |

| Blended capital stack | Mixing lender pieces without sequencing | Define who funds what, and when, before term sheets are issued |

Insurance is another issue buyers push too far down the list. If the acquisition involves leases, property, vehicles, or bonding needs, get clarity early. A practical reference point is this guide to Florida All Risk Insurance for small businesses, which helps owners think through coverage and bond requirements that can affect lender and landlord readiness.

The most fundable deal is rarely the most aggressive one. It's the one that still looks stable after everyone signs.

Good structure reduces lender anxiety. Reduced lender anxiety improves both approval odds and execution speed.

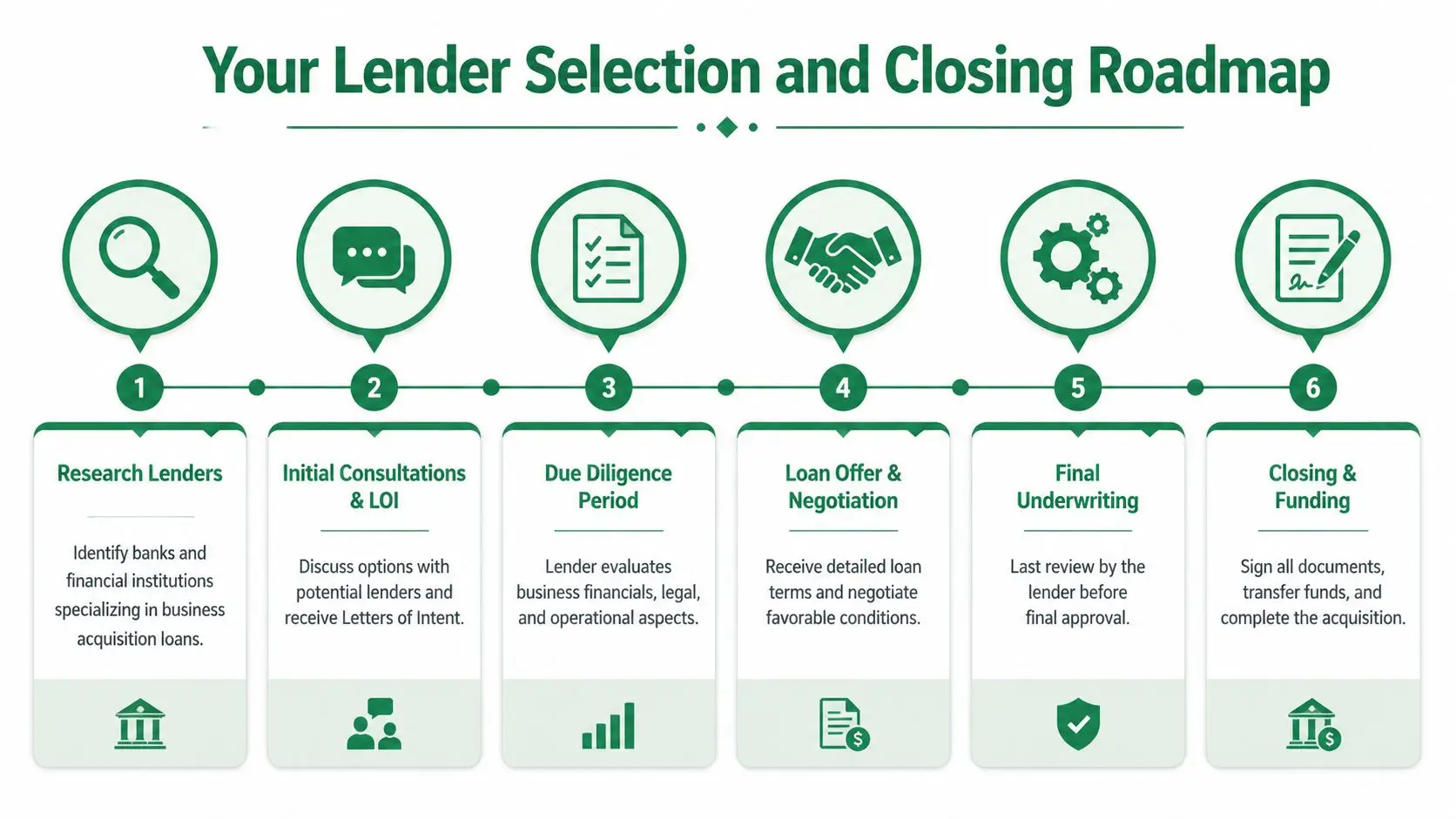

Your Lender Selection and Closing Roadmap

You can have a sound business, a reasonable valuation, and enough cash to close, then still lose the deal because the lender was wrong for the file.

I see this often with first-time buyers. They pick the bank with the best name, not the bank that closes acquisition loans every month. Then the file stalls when underwriting asks basic deal-structure questions late, or the closing team treats the purchase like a one-off exception.

Choose the lender by deal fit

A lender is not just a rate quote. It is a process, a credit box, and a closing team.

For an SBA acquisition, lender fit usually comes down to four questions:

- Do they regularly finance business purchases? A lender that mostly does commercial real estate or working capital may struggle with goodwill, seller transition risk, and add-backs.

- Can they handle your capital stack? Some banks are comfortable with seller notes on standby, partial equity injections, partner buyouts, or a real estate component. Others are not.

- Who makes the credit calls? A responsive local originator helps, but what matters is where underwriting sits and how quickly that team gives clear conditions.

- How disciplined is their closing process? Good lenders coordinate with borrower counsel, seller counsel, the landlord, and insurance early. Weak lenders wait until the last week.

If you are speaking with lenders after LOI, ask direct questions and listen for specifics:

- How many acquisition loans did you close recently?

- What would stop this deal from fitting your SBA credit box?

- Will the seller note need full standby, and for how long?

- Do you require a business valuation immediately, or after initial credit approval?

- Who orders third-party reports and who tracks closing conditions?

Those answers tell you more than a logo ever will.

Match the lender to the structure you built

This section is where buyers either gain momentum or create friction for themselves. A lender that likes clean cash flow may be slow on a turnaround story. A lender that is comfortable with heavy goodwill may get nervous if the lease has only two years left. A bank that likes owner-occupied real estate may still be a poor choice for an asset-light service business with customer concentration.

The structure has to match the bank.

If your deal includes SBA 7(a) financing, seller standby, and buyer equity from two sources, choose a lender that already knows how to document that stack. If the acquisition also includes commercial property, confirm early whether the lender wants one package, parallel approvals, or a different loan product for the property. Those choices affect timing, required reports, and closing sequence.

Keep the file clean once underwriting starts

Many delays are self-inflicted. Buyers revise the purchase agreement midstream, the seller misses document requests, or someone waits too long to address insurance, lease consent, or entity setup.

A cleaner closing usually follows this sequence:

- Lock the economics early. Keep purchase price, seller note terms, working capital expectations, and transition support stable once the file is in underwriting.

- Submit one consistent document set. The lender, valuation analyst, and closing team should all be working from the same LOI, tax returns, interim financials, and ownership information.

- Clear third-party items early. Common trouble spots include landlord consent, business valuation, life insurance if required by the bank, and proof that licenses can transfer or be reissued.

- Stay on top of seller deliverables. Corporate records, debt payoff letters, franchise approvals, and trailing financial support often come from the seller side, not the bank.

- Answer conditions fast and completely. Partial responses create extra review cycles and waste days.

One late change can force a new credit review.

What a controlled closing looks like

A good closing is rarely fast by accident. It is organized.

The lender identifies fit early. The buyer provides a complete package. The seller cooperates. Counsel on both sides knows the financing timeline. Insurance, entity documents, and banking resolutions are ready before closing week. SBA-specific items, including equity injection sourcing and standby documentation for any seller note, are handled before anyone starts talking about signing dates.

That is the roadmap. Approval is only one checkpoint. Funded deals come from aligning the capital stack, the lender, and the closing process before small issues turn into credit issues.

If you're looking for a lender match instead of guessing which bank can close your deal, GoSBA Loans helps buyers compare SBA lenders, structure acquisition financing, and manage underwriting through closing. It's a practical option when you want guidance on capital stack design, lender selection, and getting from LOI to funded purchase with fewer surprises.