You've found a business that looks right on paper. The seller has tax returns, the industry makes sense, and you can already see yourself running it. Then the financing process starts, and the deal suddenly feels less like entrepreneurship and more like a maze of lender questions, underwriting conditions, valuation issues, and legal documents.

That's the point where most buyers stop asking, “Can I buy this business?” and start asking, “How do I get a loan to buy a business?” The actual answer isn't just “fill out an application.” It's structuring the entire transaction so a lender can say yes with confidence.

The SBA SOP is the main source of truth here. It governs how SBA lenders evaluate eligibility, guarantees, ownership, use of proceeds, repayment, and guarantor requirements. If you understand how lenders apply those rules in practice, your odds improve fast.

Table of Contents

- Your Roadmap to Financing a Business Acquisition

- Assessing Your Fundability Before You Apply

- Choosing the Right SBA Loan Program for Your Acquisition

- Building a Lender-Ready Business Acquisition Plan

- Navigating the Deal from LOI to Closing

- Advanced Strategies to Get Your Deal Funded

- Frequently Asked Questions About Business Acquisition Loans

Your Roadmap to Financing a Business Acquisition

A lender doesn't approve business acquisition loans because a buyer is motivated. A lender approves them because the deal is structured to survive scrutiny.

That means four things have to line up at the same time: you, the target business, the purchase price, and the capital stack. Most online guides isolate those issues. Real underwriting doesn't. Underwriters look at all four together.

Here's how that plays out in practice:

- The buyer has to look credible. Your resume, liquidity, debt load, and background have to support the story that you can run the company.

- The business has to cash flow. Clean tax returns and believable normalized earnings matter more than a polished teaser.

- The valuation has to hold up. If the agreed price can't be defended, the lender won't stretch to make the numbers work.

- The deal structure has to be lender-friendly. Equity, seller note terms, guarantees, and use of proceeds have to fit SBA rules and lender policy.

Practical rule: Buyers think they're applying for a loan. Lenders think they're underwriting a transition of risk from seller to borrower.

In the United States, SBA-backed loans are a dominant source of acquisition financing, and the flagship 7(a) program has an average loan size of about $417,316, with many borrowers falling in the roughly $350,000 to $500,000 range. The same source notes that SBA 7(a) loans can go up to $5 million, and SBA-guaranteed loans often carry rates in ranges that compare favorably with many non-government options, which is a big reason acquisition buyers rely on them so heavily (Capital Bank on SBA business loan statistics).

The right way to think about financing is simple. Don't start with the application. Start with the underwriter's objections and remove them before the file ever gets submitted.

Assessing Your Fundability Before You Apply

A buyer can meet SBA eligibility rules and still get declined in credit. That happens every week. The gap is usually in how the deal is put together before the application ever reaches underwriting.

What lenders underwrite first

Lenders review two risk files at the same time. They underwrite the buyer, and they underwrite the business being acquired. A weakness on either side can stall the deal, force a structure change, or kill the file.

In practice, underwriters are asking a harder question than, "Does this borrower qualify?" They want to know whether this specific buyer can step into this specific company, survive the transition, and service debt without the seller in the seat.

That is why fundability starts before the loan package. It starts with deal structure.

A useful framework is the Five C's of Credit:

- Character: credit history, background, judgment, and how clearly you answer diligence questions

- Capacity: whether the company will cover debt service after reasonable adjustments

- Capital: your liquidity, injection, reserves, and overall financial strength

- Collateral: available business assets and any shortfall the lender has to get comfortable with

- Conditions: industry risk, customer concentration, transition risk, and the terms of the acquisition itself

The borrower side of fundability

Lenders do not read your personal financial statement just to tally net worth. They want to verify where your injection is coming from, whether your liquidity survives closing, and whether your personal obligations leave room for the business to breathe.

Relevant operating experience helps, but lenders apply common sense here. A former general manager buying a home services company is easier to finance than a buyer coming from an unrelated desk job with no operator lined up. I have still gotten the second deal approved, but only when the buyer added credibility elsewhere, such as a strong COO candidate, seller transition support, or meaningful direct industry exposure.

Strong borrower files usually include:

- Documented liquidity: bank or brokerage statements that clearly support the required injection and post-close reserves

- Transferable experience: management, P&L responsibility, sales leadership, finance oversight, or hiring authority

- A clear explanation of the acquisition: why this company fits your background and how you will run it on day one

Weak borrower files usually show the opposite:

- Recent large deposits with no paper trail

- A resume that does not connect to the target business

- Heavy consumer debt or thin remaining cash after closing

- Vague plans for who will replace the seller in operations

Service businesses deserve extra caution because margins can look better on paper than they will after transition. If you are reviewing a law firm, accounting practice, or similar operation, operating discipline matters. Even a basic review of streamlining legal practice expenses can help you spot whether the target's cost structure is stable or padded by owner-specific habits that will not carry over.

The business side of fundability

The target company has to support the story. Clean books matter because lenders are underwriting repayment from future cash flow, not from a broker summary or seller confidence.

Start with the financial statements, but do not stop there. Underwriters compare tax returns, interim P&Ls, balance sheets, debt schedules, payroll, and bank activity to see whether the earnings hold together under scrutiny. If the numbers keep changing as questions get more specific, confidence drops fast.

Review these areas before you submit anything:

- Tax return alignment: tax returns should broadly match internal statements and the earnings being presented

- Quality of add-backs: personal expenses, one-time costs, and excess owner compensation must be supportable and reasonable

- Customer concentration: a business that depends on one or two major accounts carries obvious repayment risk

- Payroll normalization: if the seller is underpaying themselves or family members are filling key roles, post-close labor cost may increase

- Balance sheet cleanup: old payables, stale receivables, shareholder loans, and unexplained liabilities can create avoidable credit concerns

- Transition risk: if the seller drives sales, client retention, or technical delivery, the lender will want a believable handoff plan

One point buyers miss is that lenders do not just underwrite cash flow. They also underwrite whether the purchase price is defensible. If the valuation is stretched, every other part of the file has to work harder. This guide to business valuation for SBA loans and how lenders determine acquisition value explains how lenders test price against earnings, assets, and market support.

Underwriters can work with imperfect records. They struggle with records that require a different explanation every time they review them.

Fundability improves when the buyer file, the business file, and the deal terms all support the same credit story. That is the real work before you apply.

Choosing the Right SBA Loan Program for Your Acquisition

Program choice shapes the deal more than buyers expect. I see this mistake all the time. A buyer finds a business, agrees on price, then asks which SBA loan to use. Underwriting usually works in the opposite direction. The lender looks at what is being purchased, how much of the price is goodwill, whether real estate is involved, how the down payment is structured, and whether the seller note strengthens or weakens the file. Then the right program becomes clear.

For most acquisitions, the SBA 7(a) loan is the starting point because it handles operating business purchases well, especially deals driven by cash flow and goodwill. It also fits the way many small business transactions are built. Asset sales, stock sales with the right structure, partner buyouts in some cases, and business purchases with working capital needs usually point back to 7(a).

Why the SBA 7(a) loan usually fits best

A standard 7(a) loan gives lenders the most room to approve a business acquisition that includes intangible value. That matters because many lower middle market deals are not heavy on hard assets. The value sits in recurring customers, contracts, trained staff, location, brand, and earnings history.

The buyer should also expect personal guarantees from anyone who owns 20% or more of the borrowing entity. That is an SBA rule, not a lender preference. If a buyer is surprised by that late in the process, the file is already behind.

The practical reason 7(a) wins so often is flexibility. It can cover the purchase price, certain closing costs, and often working capital if the projections support it. That gives the lender one credit story instead of several partial ones.

A clean 7(a) structure often looks like this: buyer equity injection, seller note if needed, senior SBA loan, and enough post-close liquidity so the business is not starved in month one.

When a 504 loan belongs in the deal

A 504 loan makes sense when the property is a major part of the transaction and the building will be owner-occupied under SBA rules. In that case, the property is not just collateral. It is one of the main reasons to split the structure.

Here is the trade-off. The 504 program can be attractive for the real estate portion, but it is not usually the cleanest tool for buying the operating business itself. If the transaction is mostly goodwill with a building attached, forcing everything into a 504 conversation can slow the process and create unnecessary complexity. In many cases, buyers either use 7(a) for the whole deal or combine structures only when the numbers clearly justify it.

This is one of the places where deal design matters more than rate shopping.

Where SBA Express actually helps

SBA Express is rarely the core financing tool for a full acquisition. The loan size and credit approach make it less useful for a standard business purchase, especially if the deal needs full underwriting around cash flow, transition risk, and goodwill.

Express can still help in narrower situations. I have seen it used for smaller companion needs, short-term working capital around a closing, or a modest acquisition where the structure is simple and the lender has a strong credit appetite. Buyers get in trouble when they treat Express as a faster version of standard 7(a). It is a different tool with different limits.

Match the program to the structure, not the headline rate

The wrong program can weaken an otherwise financeable deal. A business with light equipment, strong cash flow, and a seller willing to carry a standby note usually belongs in a 7(a) discussion. A transaction where the building is a large share of total value deserves a serious look at 504. A small add-on financing need may fit Express.

That decision should happen before the lender sees a scattered package.

If you want the lender review to go smoothly, build your file around the same questions underwriters ask after program selection. A practical business plan for an SBA loan should support the structure you chose, explain the transition, and show how the business carries the debt after closing.

SBA Acquisition Loan Program Comparison

| Feature | SBA 7(a) Loan | SBA 504 Loan | SBA Express Loan |

|---|---|---|---|

| Primary fit | Buying an operating business or business assets, including goodwill | Deals where owner-occupied real estate is a major component | Smaller SBA-backed financing needs with a limited acquisition use case |

| Typical acquisition use | Main program for business purchases | Best when the property is a major part of the transaction | Occasionally useful for smaller or supplemental needs |

| Loan structure | Flexible structure for purchase price, working capital, and some closing costs | Structured around fixed-asset financing, usually with real estate driving the deal | Streamlined compared with standard 7(a), but less useful for full acquisition underwriting |

| Guarantee and terms | Standard SBA 7(a) rules apply | Different structure than 7(a) | Different from standard 7(a) |

| Best for | Most buyers acquiring an existing business | Buyers purchasing a business with significant owner-occupied real estate | Borrowers with a smaller financing gap or narrow supplemental need |

If goodwill and cash flow carry the deal, start with 7(a). If the property is doing a lot of the work in the structure, put 504 on the table early.

Building a Lender-Ready Business Acquisition Plan

A buyer can have strong credit, cash for the down payment, and a signed LOI, then still lose the loan because the file does not explain one basic issue. What happens to this business the day the seller leaves?

Lenders do not approve acquisition loans based on excitement. They approve structure. The acquisition plan has to show that the business will keep producing cash flow after the ownership change, that the buyer can run it, and that the deal terms leave enough room for debt service.

Build the narrative before you upload documents

The strongest acquisition plans answer underwriting questions in the order a credit team will ask them.

Start with the transition. If the seller generated the top customer relationships, handled estimating, or made every hiring decision, the lender will focus there before looking at growth assumptions. If a general manager runs day-to-day operations and the seller is already mostly absent, that lowers perceived risk. Those are very different files, even if the tax returns look similar.

A lender will want clear answers to questions like these:

- why the seller is exiting

- how customers, employees, and vendors will be retained after closing

- what your role will be on day one

- whether any employee is carrying too much of the operation

- what support the seller will provide during the handoff

- what changes you plan to make in the first 12 months, and what you will leave alone

That last point gets mishandled often. Buyers think lenders want a turnaround story. In many acquisitions, lenders want the opposite. They want to see discipline. If the business works now, the safer plan is usually to preserve what works, stabilize the transition, and make changes after you have earned the right to do so.

If you need a practical model, this guide on writing a business plan for an SBA loan is useful because it tracks how lenders review acquisitions, not how startup plans are usually written.

Turn historical numbers into lender-usable projections

Projections start with normalized earnings, not optimism.

That means cleaning up the seller's financials so the lender can see true operating cash flow. In acquisition lending, I look first for owner add-backs that are real, supportable, and likely to continue after closing. Personal auto expense, excess family payroll, one-time legal fees, and discretionary travel may be valid adjustments. A salary reduction usually is not, unless the replacement management plan makes sense and the numbers support it.

Buyers run into difficulties when they treat every expense they dislike as an add-back. Underwriters do not. If an expense is necessary to run the business after closing, it stays. If the seller worked full time and you will need to hire an operator, the file needs to reflect that cost. If the seller note is on full standby under SBA rules for the required period, that can help the structure. If it is payable right away, it puts more pressure on cash flow.

A clean projection should include:

- A base case forecast built from business tax returns and current interim financials.

- Normalization support that explains each add-back and ties it to source documents.

- Transition assumptions for seller training, employee retention, and any customer concentration risk.

- Debt service coverage analysis showing the business can carry the new payment load with reasonable cushion.

- Use of proceeds that matches the purchase price, working capital, closing costs, and any required equity injection.

Keep the assumptions sober. Flat revenue with stable margins will often underwrite better than an aggressive hockey-stick forecast. Lenders have seen too many projections that depend on immediate growth, immediate efficiency gains, and zero transition loss. Those files do not inspire confidence.

Here's a helpful explainer to watch before you finalize your package:

What should be in the file before underwriting starts

A lender-ready file gives the credit team enough to assess the buyer, the business, and the structure without chasing basic documents for two weeks.

That usually includes:

- Buyer documents: Resume, personal financial statement, personal tax returns, government ID, and an explanation of relevant operating or management experience.

- Business documents: Historical tax returns, year-to-date profit and loss statements, balance sheets, debt schedule, aging reports if needed, and payroll detail when staffing is a major underwriting factor.

- Deal documents: LOI or purchase agreement, seller disclosures, proposed allocation of purchase price, entity formation documents, and lease information.

- Narrative documents: Acquisition plan, cash flow projections, transition plan, and a short explanation of why this buyer is a fit for this business.

- Structure support: Evidence of buyer injection, details of any seller note, and clarification on whether standby will be required under SBA guidelines.

- Industry-specific items: Licenses, franchise approvals, contracts, or permits that affect transferability.

One missing item does not kill a deal. A pattern of missing items does. When a file comes in disorganized, lenders start wondering what else is unclear. In acquisition lending, confidence is built before credit approval, not after.

Good acquisition packages do one job well. They make the deal easy to understand, easy to defend in credit committee, and easier to close on time.

Navigating the Deal from LOI to Closing

A buyer signs an LOI on Friday, tells the seller they can close in 60 days, and assumes the hard part is done. By the second week, the lender is asking for missing payroll reports, the landlord has not responded on lease assignment, and the purchase agreement now includes terms credit will not approve. That is how a financeable deal starts slipping.

From LOI to closing, the job is not just to keep the file moving. The job is to keep the deal structured in a way the lender can still defend at approval and at closing. Buyers who treat this period like a document chase usually create their own delays. Buyers who manage it like an underwriting process close faster.

What happens after the LOI is signed

The cleanest transactions move on multiple tracks at once. Diligence, underwriting, legal drafting, and third-party work should start early and stay aligned.

A typical sequence looks like this:

- LOI execution: Buyer and seller agree on price, assets or equity being acquired, diligence timing, and the broad terms the lender will later examine closely.

- Early lender review: The file goes to lenders that fit the industry, collateral profile, and deal size before the parties spend weeks negotiating around a structure no bank will accept.

- Diligence and quality of earnings review: Financial statements, tax returns, leases, payroll, customer concentration, add-backs, and transferability issues get tested against what was represented in the sale process.

- Valuation and lender third-party reports: The lender orders the work needed for credit and SBA compliance.

- Credit approval and loan authorization: Approval comes with conditions, and those conditions usually drive the rest of the closing checklist.

- Closing coordination: Insurance, entity documents, lease assignment or landlord consent, life insurance if required, final injection verification, and funds flow all have to line up.

If you want to see how lenders sequence these milestones in practice, this complete SBA business acquisition timeline from LOI to closing is a useful reference.

Where deals usually slow down

Seller responsiveness is the first problem area. A seller may be honest and still be a mess administratively. If tax returns do not reconcile to internal financials, if payroll reports are incomplete, or if key contracts are not easy to assign, underwriting slows down because the lender has to resolve every inconsistency before signing off.

The second problem is deal drift. I see this often. The LOI starts with a clean asset purchase, a reasonable working capital approach, and a seller note that supports the injection. Then attorneys revise the purchase agreement, the seller pushes for less standby, or the buyer asks to leave more debt in the business. None of those changes look major to the parties. To the lender, they can change repayment risk, collateral position, or SBA eligibility.

Legal timing causes more trouble than buyers expect. Lease assignment, franchise consent, professional license transfers, and entity formation items do not fix themselves in the final week. If the landlord is slow or the franchisor wants its own approval process, the loan can be fully approved and still not close on schedule.

What lenders are watching during this stage

Underwriters are asking a simple question the entire time. Is this still the same deal we agreed to finance?

They are checking for:

- Cash flow consistency: Do diligence findings still support debt service after normalizing expenses and removing weak add-backs?

- Buyer injection: Is the buyer's cash still available, seasoned if needed, and documented clearly?

- Seller note treatment: If the structure relies on a seller note, does it meet the lender's and SBA's standby and subordination requirements?

- Post-closing liquidity: Will the buyer have enough cash left after closing to operate the business without immediate strain?

- Transfer risk: Can the lease, licenses, vendor relationships, and major customer contracts move to the new owner?

- Purchase agreement terms: Do indemnities, holdbacks, consulting arrangements, and working capital language still match what credit approved?

This is why the period between LOI and closing is less about speed than control. Fast deals close when the structure stays clean. Slow deals usually become slow because too many people change terms without checking how those changes hit underwriting.

Most delayed closings come from a stack of small unresolved issues: a missing landlord consent, an unsupported add-back, a seller note drafted the wrong way, or buyer funds that were never documented properly.

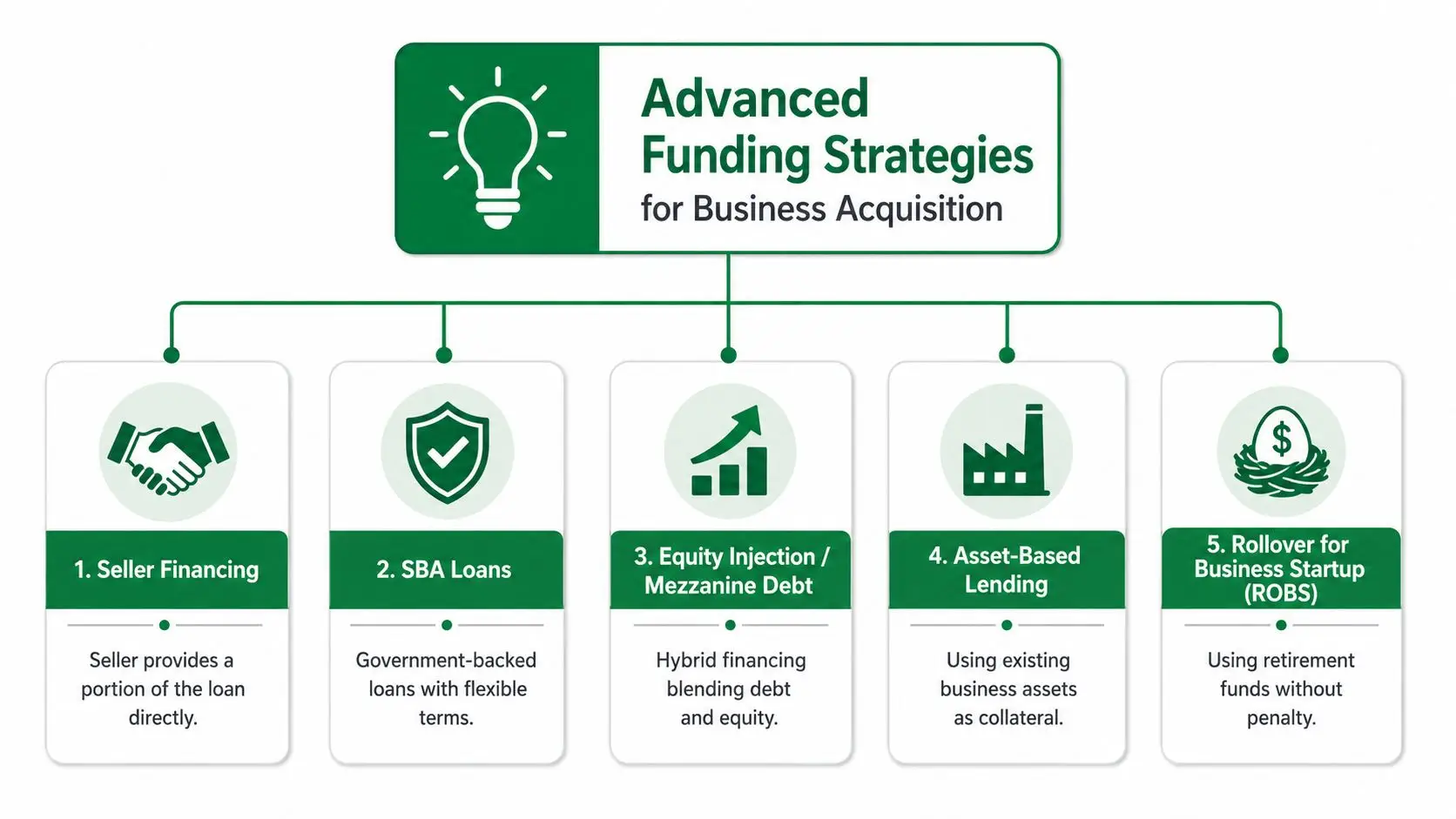

Advanced Strategies to Get Your Deal Funded

Some deals don't fail because the business is weak. They fail because the structure is lazy.

That's where advanced strategy matters. If a buyer is slightly short on liquidity, if the seller wants a higher price than the lender likes, or if the business needs a transition cushion, the answer often isn't “walk away.” The answer is to rebuild the capital stack so the lender sees alignment instead of stress.

Seller notes that help instead of hurt

Seller financing can improve a deal or wreck one. The difference is structure.

Many guides barely explain how to negotiate seller financing without creating lender concerns around subordination. That matters because SBA 7(a) allows seller notes but imposes constraints, and many public-facing resources don't show buyers how to structure scenarios that satisfy both SBA rules and lender risk appetite, as noted by the U.S. Chamber of Commerce discussion of financing an existing business purchase.

A seller note tends to help when:

- It signals seller confidence: The seller keeps risk in the deal.

- It reduces immediate cash strain: The buyer preserves liquidity after closing.

- It fits lender expectations: Terms are documented clearly and don't conflict with SBA requirements.

A seller note tends to hurt when:

- It behaves like hidden senior debt: Lenders don't want surprise repayment pressure.

- It lacks clear standby or subordination language when needed: That creates underwriting friction.

- The seller remains too entangled operationally: Lenders may worry the ownership transfer isn't real.

How blended capital stacks actually get approved

The best capital stacks are simple enough to explain in one minute. If the structure takes twenty minutes to defend, it probably won't survive credit committee.

A lender-friendly blended stack may combine:

- SBA senior debt as the primary acquisition financing

- Buyer equity from documented personal funds

- Seller financing on terms acceptable to the lender

- Investor equity if ownership and guarantee requirements still fit SBA rules

The trap is assuming more layers automatically make a deal stronger. They don't. Every extra participant adds documentation, approval points, and potential compliance issues.

Here's the practical test I use. Ask three questions:

- Can the lender explain the repayment order without opening a spreadsheet?

- Can the buyer still control the company in a way that fits SBA ownership rules?

- Can the business handle the structure without post-close cash starvation?

If the answer to any of those is shaky, the structure needs work.

A creative deal should make underwriting easier, not more theatrical.

Frequently Asked Questions About Business Acquisition Loans

Can I get a loan to buy a business if I am a first-time buyer

Yes. First-time buyers get approved all the time.

A key question is whether the deal is structured in a way that lowers the lender's concern about execution risk. A buyer with no ownership history can still get approved if the file shows relevant management experience, a sensible transition plan, clean financials, and a business that does not depend on one person holding everything together.

I have seen first-time buyers win approvals over repeat buyers for one reason. Their deals were cleaner. If you have led a division, managed a P&L, supervised staff, or sold into the same industry, that experience can carry real weight. If you do not have direct industry experience, lenders usually want to see another layer of protection, such as a strong general manager staying on or meaningful seller transition support after closing.

How much of the purchase can an SBA loan cover

An SBA 7(a) loan can often finance the full business purchase, and in many cases related closing costs as well, if the cash flow, valuation, and structure hold up in underwriting.

That does not mean every buyer gets a zero-down outcome. The lender still decides whether the debt load makes sense for that specific company and that specific buyer. If the tax returns are weak, the add-backs are aggressive, or the purchase price runs ahead of what the business supports, the lender may require more buyer equity, a standby seller note, or a lower purchase price.

Buyers often get confused. They hear that SBA financing can cover a full acquisition and assume approval is mainly about filling out the application. In practice, the structure drives the answer. The stronger the debt service coverage, buyer profile, and deal terms, the more financing flexibility you usually have.

What makes lenders decline an acquisition loan

Most declines come from the same handful of problems, and none of them are surprising once you have sat through enough credit discussions.

A lender says no when the numbers do not tie out, the buyer does not look prepared, or the deal asks the bank to accept risk that should have been fixed before submission.

Common reasons include:

- Seller financials that do not support the stated cash flow

- Debt service that is too thin after normalization

- A buyer background that does not match the operating demands of the business

- Purchase terms that look inflated or poorly documented

- Gaps in diligence, including missing tax returns, unexplained deposits, unsigned agreements, or unresolved legal issues

The pattern matters more than any single flaw. A file with one weakness can still get approved. A file with weak cash flow, a stretched valuation, and a thin buyer resume usually does not.

Can seller financing improve my approval odds

Yes, if the note is structured to support the senior loan instead of competing with it.

Lenders like seller financing when it shows confidence in the business and reduces the amount of outside cash needed to close. They become cautious when the note creates repayment pressure too early or reads like side debt that could disrupt operations after funding. Terms matter. Documentation matters. So does the seller's role after closing.

The best seller notes make the deal easier to approve because they fit the underwriting story. The seller leaves enough skin in the game to reassure the lender, while the repayment terms preserve cash during the early post-close period. A poorly written note does the opposite. It raises questions about control, repayment priority, and whether the business will have enough liquidity once the buyer takes over.

If you are evaluating a business purchase and want help structuring the financing correctly, GoSBA Loans is one option to consider. The firm brokers SBA financing for acquisitions and helps buyers compare lender fit, assemble a lender-ready package, and address the underwriting issues that often decide whether a deal closes or stalls.