You've likely reached the point where the deal feels real. You found a business you'd buy. The broker sent financials. The seller says they want a serious LOI. Now the financing piece starts to look less like a checkbox and more like the whole transaction.

That's where most first-time buyers get blindsided. They think an SBA lender just wants forms, tax returns, and a decent credit score. In practice, the lender is underwriting a transfer of risk, cash flow, management capability, collateral support, and deal structure all at once. If any one of those pieces is weak, the file slows down or dies.

The good news is that an SBA loan for acquisition of a business remains the strongest financing tool available for many lower middle market and small business purchases. The main source of truth is the publicly available SBA SOP, and the deals that close usually follow that framework closely. The buyers who have the easiest path aren't always the richest or the most experienced. They're the ones who understand how lenders think before they submit the deal.

Table of Contents

- Your Blueprint for Buying a Business with SBA Financing

- Confirming Your Eligibility for an SBA Acquisition Loan

- Structuring Your Deal to Maximize Fundability

- The Complete Acquisition Timeline From LOI to Closing

- Assembling a Bulletproof Financial Package

- How to Navigate Underwriting and Avoid Common Roadblocks

- Frequently Asked Questions About SBA Acquisition Loans

Your Blueprint for Buying a Business with SBA Financing

For business acquisitions, the SBA 7(a) loan is still the workhorse because it gives lenders a framework for financing goodwill, going-concern value, and operating businesses that a conventional loan often won't touch on comparable terms. That matters because most small business deals aren't just equipment and real estate. They're cash flow deals.

The important shift is to stop thinking about SBA financing as a form-filling exercise. It's a deal design exercise. The lender wants to know whether the purchase price is defensible, whether the buyer can operate the company, whether the transition is credible, and whether the post-close business can carry the debt without getting fragile.

A major recent update changed what buyers can finance. A 2023 rule change effective May 11, 2023 allows SBA 7(a) proceeds to be used for a partial purchase of a business or a partial change of ownership, where the program historically only allowed 100% acquisitions. That opens the door for partner buyouts, staged exits, and spin-offs that used to require a different structure.

That change matters in real negotiations. A seller who doesn't want to leave all at once may now fit inside a financeable structure. A partner dispute can sometimes be solved without forcing a full-company sale. Buyers who understand that flexibility can negotiate more intelligently.

If you're still shaping the transaction itself, a solid outside resource is this founder's M&A playbook from Coto & Waddington, Attorneys at Law. It's useful because financing doesn't sit in a vacuum. The LOI, diligence scope, purchase agreement, and closing conditions all affect whether the SBA file is smooth or painful.

Practical rule: The bank doesn't fund excitement. It funds a structure that still makes sense after underwriting strips away optimistic assumptions.

Confirming Your Eligibility for an SBA Acquisition Loan

You can have a signed LOI, a seller who wants to close fast, and clean looking financials, then still lose the deal because the file was never SBA-eligible in the first place. I see that happen when buyers focus on collecting documents but miss the underwriting logic behind them. The lender is testing two things at once. Does the transaction fit SBA rules, and does it still look repayable after the bank strips out optimistic assumptions?

What lenders look at on the buyer side

Banks still use the classic five C's, but on acquisition loans those factors show up in specific ways.

- Character: Full disclosure matters more than polish. A lender can work through an old credit issue, prior business closure, or uneven tax history if it is explained early and documented. What causes real trouble is discovering it late. Many SBA lenders prefer buyers with a personal credit score around 680 or better, which aligns with common lender guidance summarized by Nav's overview of SBA loan requirements.

- Capacity: The buyer does not need direct experience in the exact niche, but the file has to tell a credible operating story. Management, sales, finance, industry adjacency, or prior ownership all help. Underwriters are asking a simple question. Can this person run the company well enough to protect cash flow after the seller leaves?

- Capital: Buyer equity is one of the clearest signals in the deal. The SBA generally expects a minimum 10% equity injection on a change-of-ownership transaction, and the source of that injection matters. If too much of it is borrowed, gifted without documentation, or tied to seller paper that does not meet SBA rules, the structure gets weak fast. The SBA acquisition financing guidance is useful here because it shows how lenders think about cash injection and seller note treatment.

- Collateral: Cash flow drives approval, but available collateral still affects lender comfort. If there is a shortfall, the bank will usually take available business assets and may also require liens on personal real estate when equity is available.

- Conditions: Industry risk, customer concentration, seasonality, pending litigation, and the amount of seller transition support all influence credit appetite. A deal can be SBA-eligible on paper and still be declined by a bank that does not like the risk profile.

First-time buyers get approved all the time. What they do not get is a free pass on credibility. The lender has to believe the transition works in real life, not just in the business broker memo.

What makes a target business SBA friendly

A business can be attractive to a buyer and still be a poor SBA credit. Those are different screens.

Underwriters get comfortable when the target has financials that reconcile to tax returns, earnings that hold up after normalization, and a revenue base that is understandable without long explanations. They also want to know the seller is not the entire business. If every major customer relationship, estimate, or operational decision runs through one owner, the transition risk rises quickly.

Valuation matters here too. If the price is being supported by aggressive add-backs, projected growth, or a multiple that only works in a perfect year, the bank will push back. Buyers who understand how lenders determine acquisition value for SBA financing usually spot this issue before they overpay or sign an LOI that will be hard to finance.

A few target-company issues trigger extra scrutiny right away:

- Messy financial reporting: Interim statements that do not tie to tax returns, unexplained owner distributions, or missing balance sheet detail.

- Concentration risk: Heavy dependence on one customer, one vendor, or one referral source.

- Seller dependence: The owner personally controls sales, technical delivery, licensing, or key employee relationships.

- Compliance problems: Tax arrears, licensing gaps, legal disputes, or environmental concerns.

- Volatile earnings: Big swings in revenue or margin that make repayment harder to underwrite with confidence.

A financeable acquisition is a business an underwriter can verify, not just a business a buyer likes.

Lender fit also matters more than buyers expect. Some banks like blue-collar service companies with repeat revenue. Others are more comfortable with healthcare, distribution, or deals with partial seller rollover. Starting with a lender that regularly handles your industry and deal type can save weeks of friction and prevent a decline that had more to do with bank appetite than with the quality of the deal.

Structuring Your Deal to Maximize Fundability

A lot of buyers focus on the purchase price and miss the bigger issue. Structure is what determines whether the deal is financeable, affordable after closing, and durable if the first year is bumpier than expected.

Why structure matters more than buyers think

From the lender's side, a badly structured deal usually has one of three problems. The buyer is bringing too little real equity. The repayment burden is too aggressive for the company's actual cash flow. Or the purchase price is doing too much work relative to the supportable value.

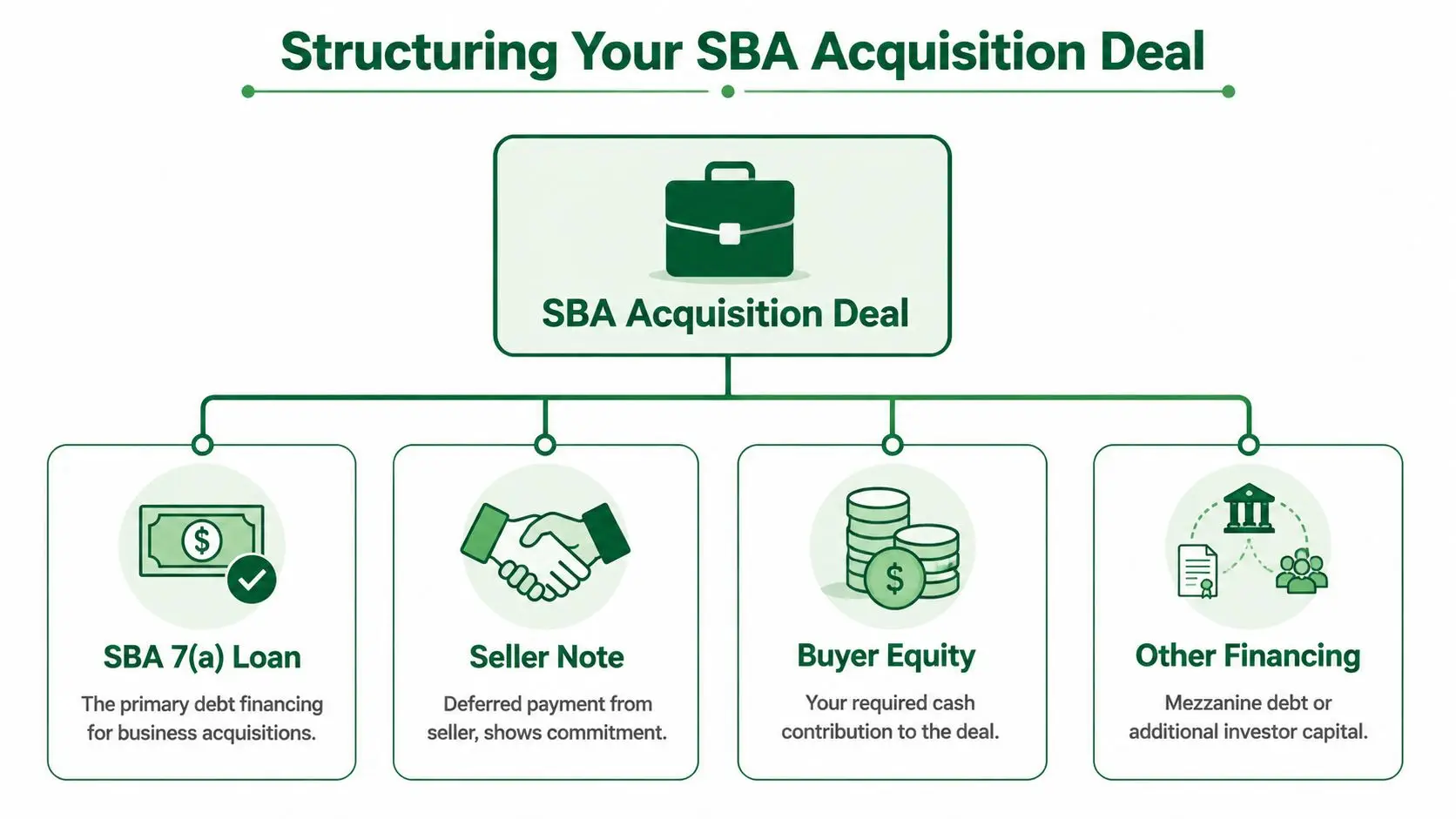

That's why the capital stack matters. The SBA loan may be the anchor, but it rarely tells the whole story. Seller notes, buyer cash, rollover equity, and other financing sources can all affect whether the file feels conservative or stretched.

When real estate is part of the purchase, term length can materially change post-close pressure. For an SBA 7(a) loan used to acquire a business, the maximum maturity is generally 10 years, but if the purchase includes commercial real estate and that real estate is at least 51% of the total purchase price, the maturity can extend to 25 years, according to the Yale School of Management overview of the SBA 7(a) program%20Loan%20Program.pdf).

That's not a minor detail. It can change whether the business has breathing room after closing.

The pieces of a financeable acquisition

A strong structure usually balances four moving parts:

| Component | What it does | What lenders care about |

|---|---|---|

| SBA 7(a) loan | Provides the primary acquisition debt | Cash flow support, eligibility, collateral, and repayment risk |

| Buyer equity | Shows commitment and lowers leverage | Whether the buyer has real skin in the game |

| Seller note | Can bridge valuation or liquidity gaps | Whether terms support the senior debt rather than compete with it |

| Other financing | Fills gaps when the deal needs more flexibility | Whether the total stack still fits SBA rules and credit policy |

Seller notes deserve special attention. In the right transaction, they can help align incentives and solve a gap between what the seller wants and what the lender will support. But not every seller note improves a file. If repayment terms are too aggressive or documentation is loose, the note can create more underwriting concern than value.

Buyers also need to respect valuation discipline. If the agreed price exceeds what the lender and third-party analysis can support, you're no longer structuring a loan. You're trying to finance a disagreement. This guide on how lenders determine what your acquisition is worth is worth reviewing before you lock yourself into a number that the bank may not carry.

The easiest deals to fund aren't always the cheapest. They're the ones where price, terms, cash flow, and transition support each other.

When buyers ask what “works” in practice, the answer is usually this: bring clean equity, leave room in the debt service, document the seller's role carefully, and avoid structures that require everyone to believe the best-case scenario. Underwriters don't approve best cases. They approve deals that survive ordinary problems.

The Complete Acquisition Timeline From LOI to Closing

You sign an LOI on Friday and expect to close in a month. Then the lender asks for clarification on inventory, the seller is late sending interim financials, and counsel finds that the asset list in the LOI does not match the draft purchase agreement. That is how a clean deal turns into a slow one.

SBA acquisition timelines are predictable once you understand what the bank is trying to prove at each step. The lender is not just collecting documents. It is testing whether the deal structure, cash flow, collateral position, buyer profile, and closing conditions still support approval after diligence starts.

To frame the LOI stage properly, this overview of Letters of Intent is useful. A good LOI gives the lender enough clarity on price, terms, included assets, transition support, and timing to decide whether the file is worth underwriting.

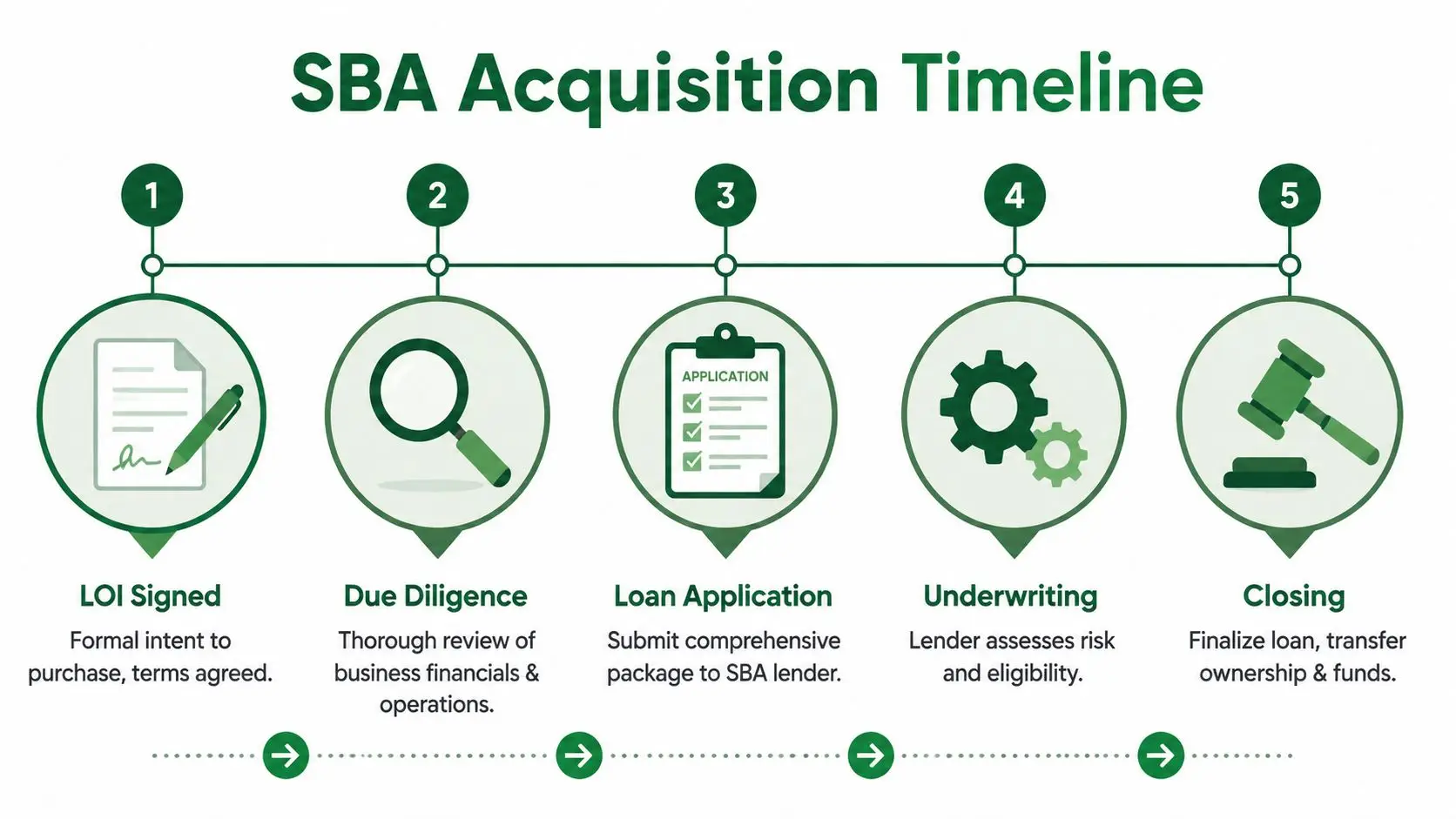

The stages that drive the clock

Most SBA business acquisition deals move through four practical phases: screening, full application, underwriting, and closing. The calendar depends less on the SBA itself than on how quickly the buyer, seller, lender, and third parties can answer the next underwriting question with clean support.

Prequalification

This is the first filter. The lender reviews the LOI, historical business performance, buyer experience, estimated debt service, and any obvious structure problems. If the file breaks here, it is usually because the price is unsupported, the buyer is undercapitalized, or the proposed terms create repayment risk.Application

The file becomes formal. The bank collects borrower forms, seller information, tax returns, interim financials, debt schedules, entity documents, and a draft purchase agreement or LOI. Strong buyers keep diligence moving during this phase, because waiting for the bank to finish first usually adds weeks with no benefit.Underwriting

During underwriting, credit reviews earnings quality, normalizes expenses, checks whether the add-backs hold up, evaluates transferability of revenue, and looks closely at how the buyer will operate after closing. If a lender orders a business valuation, lease review, or other third-party work, those items can become gating conditions.Closing

Approval does not mean money is ready to wire. Closing counsel still has to confirm entity formation, insurance, life insurance if required, lien searches, lease assignments, payoff letters, seller-note terms, and final source and use documentation. A surprising number of deals stall here because one signature page, one landlord consent, or one insurance binder is still missing.

If you want a phase-by-phase checklist, this guide to the complete SBA business acquisition timeline helps buyers line up lender tasks, diligence items, and legal work on the same calendar.

Here's a helpful overview before digging into the details:

Where deals lose time

Delays usually come from mismatches between the deal on paper and the deal the bank is being asked to approve.

A few patterns show up repeatedly:

- LOI terms that are too thin: If the LOI is vague on working capital, inventory treatment, seller transition support, training, or excluded assets, underwriting has to stop and ask basic deal questions later.

- Diligence that starts too late: Buyers who wait for conditional approval before requesting core diligence items give away time they could have used to solve accounting, tax, or operational issues.

- Third-party work ordered late: Valuation, legal review, lease consent, franchise review, and insurance are not last-week tasks.

- Changing numbers: The lender package, quality of earnings adjustments, and purchase agreement need to tell the same story. When EBITDA, add-backs, or source-and-use figures keep moving, credit has to rework the file.

- Seller-side disorganization: Missing tax returns, weak interim reporting, or unclear payroll records can slow an otherwise financeable transaction.

One practical rule helps more than anything else. Run financing, diligence, and legal drafting at the same time.

From the lender's side, responsiveness matters because underwriting is sequential. Credit cannot clear global cash flow if business debt is still unclear. Counsel cannot finalize loan documents if the purchase agreement keeps changing. Closing cannot schedule funding until every prior condition is satisfied. A file with fast answers keeps its place and keeps momentum. A file with partial answers gets pushed back into the queue.

Assembling a Bulletproof Financial Package

The financial package is the most controllable part of the process, and buyers still treat it too casually. They upload documents, answer questions as they come in, and assume the lender will stitch the story together. That's backward. The package should already answer the underwriter's main concerns before the first credit memo is drafted.

A weak package creates doubt. A strong package creates narrative coherence. It tells the bank what the business has done, what the buyer understands, what the deal looks like after closing, and why repayment is realistic.

What belongs in the package

At a minimum, the file needs completeness and internal consistency. A critical failure point is an incomplete package. Lenders frequently reject applications that are missing three years of tax returns, a detailed business plan with financial projections, or a signed Purchase Agreement, as noted by Live Oak Bank's guidance on financing a business acquisition with SBA 7(a).

That sounds obvious, but completeness goes beyond attaching PDFs. The documents need to support each other.

A clean package usually includes:

- Business tax returns: They anchor the lender's historical view of the target.

- Personal tax returns and PFS: These help the lender evaluate the guarantor's financial position and disclosure quality.

- Interim financials: Year-to-date profit and loss statements, balance sheets, and debt schedules help show current trend lines.

- Signed deal documents: The LOI alone may start the process, but the final package needs executed transaction documents as the deal advances.

- Business plan and projections: The buyer explains how the business will be run after closing.

How to make the story underwriter ready

The business plan matters because it turns static history into an operating thesis. But the plan only helps if it's grounded. A lender doesn't want a startup-style manifesto full of market excitement. They want a sober operating plan tied to the actual company being purchased.

Focus your projections on what can be defended:

- Use existing business history as the baseline. If the company has seasonality, customer concentration, or margin variability, reflect it.

- Explain changes clearly. If you expect improvement, tie it to something specific such as pricing discipline, expense normalization, or a defined transition plan.

- Don't hide debt service pressure. The lender will model it anyway.

- Address owner replacement candidly. If the seller has been doing key functions, show how those responsibilities transfer.

A good package also anticipates hard questions. If revenue dipped for a known reason, say so and support it. If margins changed because the seller paid themselves unusually, explain how that affects normalization. If there are one-time expenses, identify them cleanly.

Buyers lose credibility when every projection slopes upward and every risk disappears after closing.

Presentation matters too. Name files clearly. Reconcile totals across documents. Make sure dates, entities, and ownership percentages match. Underwriters notice sloppiness because sloppiness in the package often signals sloppiness in the borrower.

The goal isn't to make the deal look perfect. It's to make it understandable, documented, and believable.

How to Navigate Underwriting and Avoid Common Roadblocks

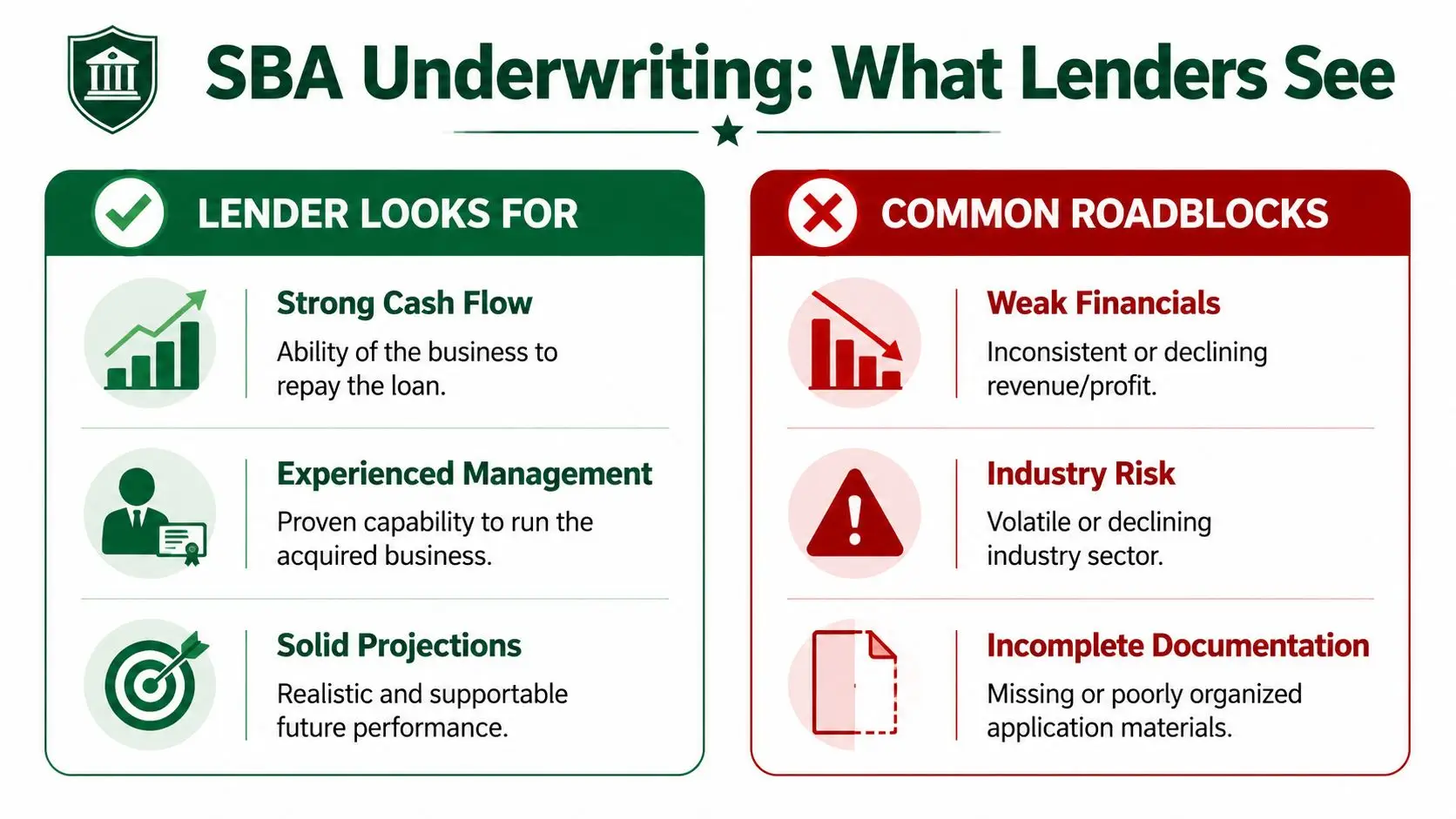

Underwriting isn't the bank checking whether you uploaded enough forms. It's the bank deciding whether it wants to own the risk of this transaction for years. That's why deals that feel straightforward to buyers can still get pushed back hard in credit.

Underwriting is risk control, not paperwork review

The SBA guarantee makes lenders more willing to participate, but it doesn't remove discipline. The SBA guarantees up to 75% of standard 7(a) loans exceeding $150,000, and for a $5 million acquisition loan the lender is exposed to 25% risk, or $1.25 million, according to the SBA 7(a) terms, conditions, and eligibility page.

That guarantee helps. It doesn't make the lender careless.

Banks still underwrite aggressively because they need the file to meet policy, support repayment, and comply with SBA requirements. If a lender gets sloppy, it can create real problems later, especially around guarantee enforceability and internal credit review.

For a useful look at how banks evaluate these files, this guide on how SBA lenders underwrite your deal lays out the logic behind the review process.

Common issues and how buyers can defuse them

A lot of roadblocks are visible before the application goes in. Buyers just don't always know what to look for.

Here are the issues that come up repeatedly:

Unsupported valuation

If the price depends on heroic assumptions, underwriting gets uncomfortable fast. The fix is to pressure-test valuation before the purchase agreement locks in the number.Weak transition planning

If the seller drives all sales, holds all vendor relationships, or carries key licenses informally, the bank will question continuity. Spell out training, introductions, and role transfer in writing.Customer or revenue concentration

Lenders worry when too much income depends on a small base of accounts. Be ready to explain contract durability and relationship depth.Buyer experience mismatch

A strong operator in one field doesn't always translate cleanly into another. The more the acquired business depends on specialized knowledge, the more carefully lenders look at management fit.Incomplete disclosure

Omissions damage trust faster than bad facts. Disclose litigation, tax issues, prior business trouble, or credit blemishes early and explain them plainly.

A separate issue that kills deals is poor diligence. If the buyer hasn't verified the target's financial history, market position, or repayment ability, the lender often discovers those gaps during underwriting anyway. And if the file is missing core SBA forms or they're completed carelessly, delays follow.

Underwriting problems are usually discovered late, but they're rarely created late.

The strongest buyers think like lenders before the lender has to ask. They test the seller's claims. They look for inconsistencies. They identify the soft spots in management, revenue, and transition. When they do that work early, underwriting becomes a confirmation exercise rather than a rescue mission.

Frequently Asked Questions About SBA Acquisition Loans

Practical answers buyers usually need

Can I buy only part of a business with SBA financing?

Yes, if the structure fits current SBA rules. The major rule change referenced earlier opened the door for partial purchases and partial ownership changes, which can help with partner buyouts or phased exits.

What kind of collateral will I need to pledge?

Expect the lender to look for available business assets, intangible collateral, and personal assets when available. Collateral support matters, but cash flow and management fit usually drive the core credit decision.

How long does seller support usually matter to the lender?

Lenders want a transition plan that makes operational sense. The exact length depends on the business, but the more seller-dependent the company is, the more important documented training and handoff arrangements become.

What if the purchase price feels high to the bank?

Then the problem isn't just valuation. It's the financing structure. If the lender can't support the price, you may need to renegotiate, restructure the seller note, increase equity, or revisit what's being acquired.

How much cash do I need to bring in?

The core equity requirement was covered earlier, and it's one of the first things lenders examine because it shows commitment and affects the financial structure at closing.

What documents trip buyers up most often?

Usually the basics that were assembled too late or inconsistently: tax returns, projections, purchase documents, disclosure forms, and personal financial information that doesn't tie out.

Do I need direct industry experience?

Not always. But you do need a credible case that you can run the business. Sometimes that comes from direct industry background. Sometimes it comes from management, finance, sales, operations, or leadership experience that translates well. The burden is on the buyer to make that case clearly.

Should I talk to lenders before the purchase agreement is final?

Yes. Early lender feedback can save weeks of wasted negotiation and help you avoid a structure that looks fine to the parties but doesn't work in credit.

If you're buying a business and want experienced help from LOI through closing, GoSBA Loans can coordinate lender matching, packaging, underwriting support, and closing execution at no cost to the borrower. It's a practical option if you want to compare lenders, tighten your structure, and improve the odds that your SBA acquisition loan closes cleanly.