Cash problems shut more small businesses down than weak sales ever do. That is why finance management matters to owners, and why it matters even more to lenders.

From an SBA lender's perspective, the question is not whether a business shows profit on paper. The question is whether that profit turns into enough real cash to cover payroll, pay vendors on time, absorb a slow month, and support loan payments without strain. Profit is the scorecard. Cash is the oxygen.

I see this gap all the time. An owner brings in a clean profit and loss statement, but receivables are aging, inventory is soaking up cash, or debt payments already leave little room for error. On paper, the business looks healthy. In underwriting, it looks fragile.

Bankable businesses produce more than revenue. They produce usable cash, reliable records, and financial statements that hold together under scrutiny. If you want a sharper view of how buyers and lenders assess that financial story, this review of small business financial intelligence and custom financial modeling for business buyers offers a useful lens.

Good financial management helps you make better operating decisions. It also does something more important. It makes your business easier to trust, easier to fund, and harder to break when conditions tighten.

Table of Contents

- Why Financial Management Is Your Most Critical Skill

- Building Your Financial Foundation

- Budgeting and Cash Flow Forecasting

- Measuring Health With Financial KPIs

- Choosing Your Growth Fuel Debt vs Equity

- How to Prepare for SBA Financing

- Frequently Asked Financial Management Questions

Why Financial Management Is Your Most Critical Skill

Twenty-nine percent of startups fail because they run out of cash. For an owner seeking financing, that number matters less as trivia and more as a warning. Lenders do not get repaid from paper profit. They get repaid from cash left over after payroll, rent, taxes, debt payments, and the routine surprises that hit every operating business.

That is why financial management sits at the center of fundability. A lender reviewing your file is asking a simple question: does this business produce predictable cash, and does the owner understand how that cash moves? Clean revenue growth helps, but it does not overcome weak collections, thin margins, bloated inventory, or a habit of plugging recurring shortfalls with expensive short-term debt.

Profit and cash are related, but they are not the same tool. Profit is your scoreboard. Cash is your oxygen. A business can show a profit on the income statement and still miss payroll because customers have not paid yet, inventory absorbed too much cash, or loan payments came due before receivables cleared.

I see this mistake often. Owners push for more sales, then wonder why pressure gets worse. If each new dollar of revenue requires upfront labor, materials, or ad spend before cash comes in, growth can tighten the business instead of strengthening it.

From an underwriting standpoint, weak financial management shows up quickly. Hiring ahead of demand, offering loose payment terms, underpricing jobs, or treating the bank account like a rough estimate all leave fingerprints in the statements. Underwriters notice when the story sounds strong but the numbers do not support it.

Three signs usually separate a finance-ready business from one that struggles to get approved:

- Accurate books: Financial statements reconcile, expense categories make sense, and owner spending is not mixed into operations.

- Cash awareness: Management knows what bills are due, what receivables are late, and where pressure points will hit before they become emergencies.

- Decision discipline: The owner can explain which costs produce return, which ones support stability, and which ones should be cut.

If you want a clearer framework for reading your numbers the way a buyer or lender would, this guide to financial intelligence and custom financial modeling for business buyers is a useful next layer.

Good financial management also improves your options. Businesses with clear reporting and steady cash habits are easier to bank, easier to value, and easier to grow without panic. That practical lender-focused view lines up with Everglow's expertise in business finance. The goal is not prettier bookkeeping. The goal is a business that can absorb shocks, qualify for capital, and keep control in the owner's hands.

Building Your Financial Foundation

A business without financial separation is like a house poured on wet concrete. It may stand for a while, but every addition becomes riskier.

The first essential step is account separation. Pursuit's small business finance best practices states that as soon as a business entity is formed, operators should open a dedicated business bank account, use only business-specific debit and credit cards, and avoid mixing personal expenses to preserve legal clarity and accurate bookkeeping. That one move improves tax reporting, owner equity tracking, audit readiness, and lender confidence.

Separate accounts first

If you pay business expenses from a personal card and reimburse yourself casually, your books stop telling the truth. The issue isn't only mess. The issue is credibility. When underwriters see mixed spending, they wonder what else is blurred.

Use this basic setup:

- Operating account: All revenue deposits land here and routine expenses leave from here.

- Business debit or credit card: Use one lane for business purchases only.

- Tax holding account: Move money aside regularly so tax obligations don't ambush cash.

- Owner draw or payroll process: Pay yourself deliberately, not randomly.

If you used personal funds early on, clean it up with proper categorization. An accountant can help reclassify those entries correctly, but the bigger win is stopping the behavior going forward.

The cleanest financial story usually wins. Not because it looks pretty, but because it's easier to trust.

Choose a recordkeeping system you'll actually maintain

Owners love talking about software. Lenders care more about consistency. QuickBooks, Xero, and similar tools can work well if someone is reconciling accounts, categorizing transactions correctly, and closing each month. A neglected system is worse than a simple one maintained properly.

Good recordkeeping should produce:

- Monthly profit and loss statements

- Balance sheets

- Cash flow visibility

- Receivables and payables aging

- A clear trail for owner contributions and distributions

If you're growing and need outside help, it's worth reviewing Everglow's expertise in business finance for a practical planning perspective that connects bookkeeping to broader financial decisions.

The foundation phase is boring by design. That's a good thing. Clean accounts and reliable books don't feel exciting, but they make every later decision better, from forecasting to valuation to SBA underwriting.

Budgeting and Cash Flow Forecasting

Budgeting sets the target. Cash flow forecasting shows whether the business can make payroll, cover debt payments, and stay in control while it chases that target.

Lenders separate those two ideas fast. A budget can show a profitable year and still hide a cash squeeze that threatens loan payments in March, quarterly taxes in June, or inventory buys before a busy season. That gap between paper profit and spendable cash is one of the main reasons otherwise solid businesses look weak in underwriting.

Profit is an accounting result. Cash is oxygen.

A practical budget answers, "What should this business earn and spend if operations go to plan?" A cash flow forecast answers, "When will money hit the bank, and when will it leave?" If receivables land 20 days late, or a large vendor bill hits before collections clear, the forecast catches the problem while there is still time to adjust.

That is why I tell owners to build forecasts from bank behavior, not optimism. Use actual collection patterns. Use actual payroll draft dates. Use actual loan payment dates. Use tax due dates, insurance renewals, annual software charges, and seasonal inventory needs. The more your forecast reflects how cash flows, the more useful it becomes for management and for financing.

A workable forecast should track:

- Cash receipts by expected deposit date: Base this on customer payment habits, not invoice issue dates.

- Payroll and payroll taxes: Wages are only part of the outflow.

- Vendor payments by due date: Monthly totals are too blunt to manage timing risk.

- Debt service: Show principal and interest clearly so fixed obligations stay visible.

- Irregular expenses: Repairs, legal fees, insurance, taxes, deposits, and equipment purchases often cause the surprise.

For owners who want extra ideas on tightening collections, reserves, and payment timing, this guide on strategies for business cash flow is a useful companion.

How to build a practical 13 week forecast

The 13 week cash flow forecast is one of the most useful operating tools a small business can keep. It is short enough to update accurately and long enough to expose pressure points before they turn into missed payments or emergency borrowing.

Build it in weekly columns.

Start with beginning cash. Then list expected inflows by week, based on collections rather than booked revenue. After that, list outflows by week, including payroll, rent, vendors, taxes, credit lines, term debt, and any planned owner distributions. If a payment could hit the account, it belongs in the forecast.

Then stress-test it. Push major customer payments back one or two weeks. Add a repair bill. Increase inventory needs before a busy month. A forecast that only works under perfect conditions is not a management tool. It is a wish list.

Update it every week. That discipline matters. Lenders read it as proof that management understands cash timing, reacts early, and does not confuse sales growth with liquidity.

If you're modeling scenarios for financing or acquisition planning, these SBA loan calculators can help pressure-test payments and capital structure assumptions.

The goal is not precision down to the dollar. The goal is early warning. A business that sees a cash gap six weeks ahead has options. A business that sees it on Friday morning usually pays more for the fix.

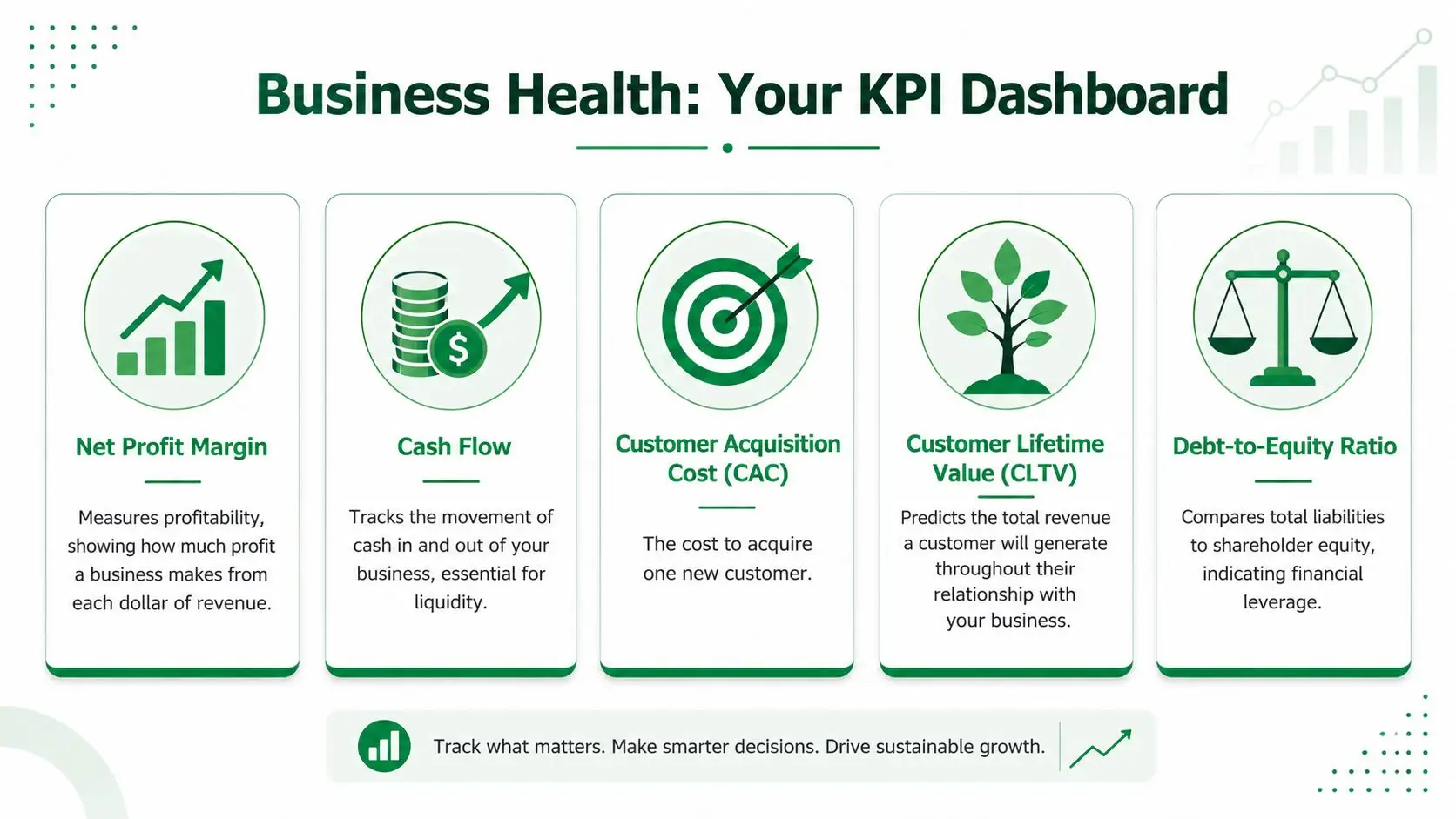

Measuring Health With Financial KPIs

Financial statements are the map. KPIs are the dashboard. Owners need both. A lender reading your file wants to know not only what happened, but what your numbers say about control, consistency, and risk.

One broad warning sign sits above all the others. Vena's small business revenue statistics shows that only 30% of owners finished 2025 with profitability above expectations, down from 57% in 2024, and that a healthy profit margin typically falls between 7% and 10%. Many owners are working hard without converting enough revenue into durable earnings.

What lenders look for in the dashboard

The first KPI most lenders care about is debt service coverage. Even if you don't calculate a formal DSCR every month, you should understand the idea. Can the business generate enough cash to cover its loan payments with room for error? Thin coverage makes underwriting harder because there's no cushion if sales wobble or expenses rise.

The second is profit margin quality. Not just the number, but how it behaves. If margin jumps around wildly, lenders ask why. Pricing inconsistency, bloated labor, discounting to win deals, or poor expense controls often sit underneath.

The third is the cash conversion cycle. How long does cash stay trapped between paying for operations and collecting from customers? In this process, many “profitable” businesses get exposed. Slow collections and inventory drag can make a healthy-looking income statement feel broke.

A few supporting indicators also matter:

- Accounts receivable aging: Old receivables weaken confidence in stated revenue quality.

- Accounts payable discipline: Chronic stretching may signal hidden pressure.

- Debt-to-equity ratio: Useful for understanding how aggressively the business uses debt financing.

- Cash flow trend: Stable operating cash beats erratic spurts.

If you want a practical accounting-oriented primer on using metrics operationally, boost your business with KPIs offers a helpful lens.

Here's a quick visual explainer on the same theme:

How to use KPIs without fooling yourself

Bad KPI habits are common. Owners track vanity metrics, review them too late, or ignore the operational cause behind the number.

A good KPI should force a decision. If it doesn't change behavior, it's just decoration.

Review KPIs monthly at minimum. Tie each one to a concrete question:

- Margin fell. Was pricing weak, labor inefficient, or overhead too high?

- Receivables stretched. Which customers slowed down, and what's the collection plan?

- Cash tightened. Was it seasonality, owner draws, inventory, or debt load?

- Debt increased. Did the borrowed capital produce return, or just buy time?

That's how small business finance management becomes useful. Not as a report stack, but as an operating discipline lenders can believe.

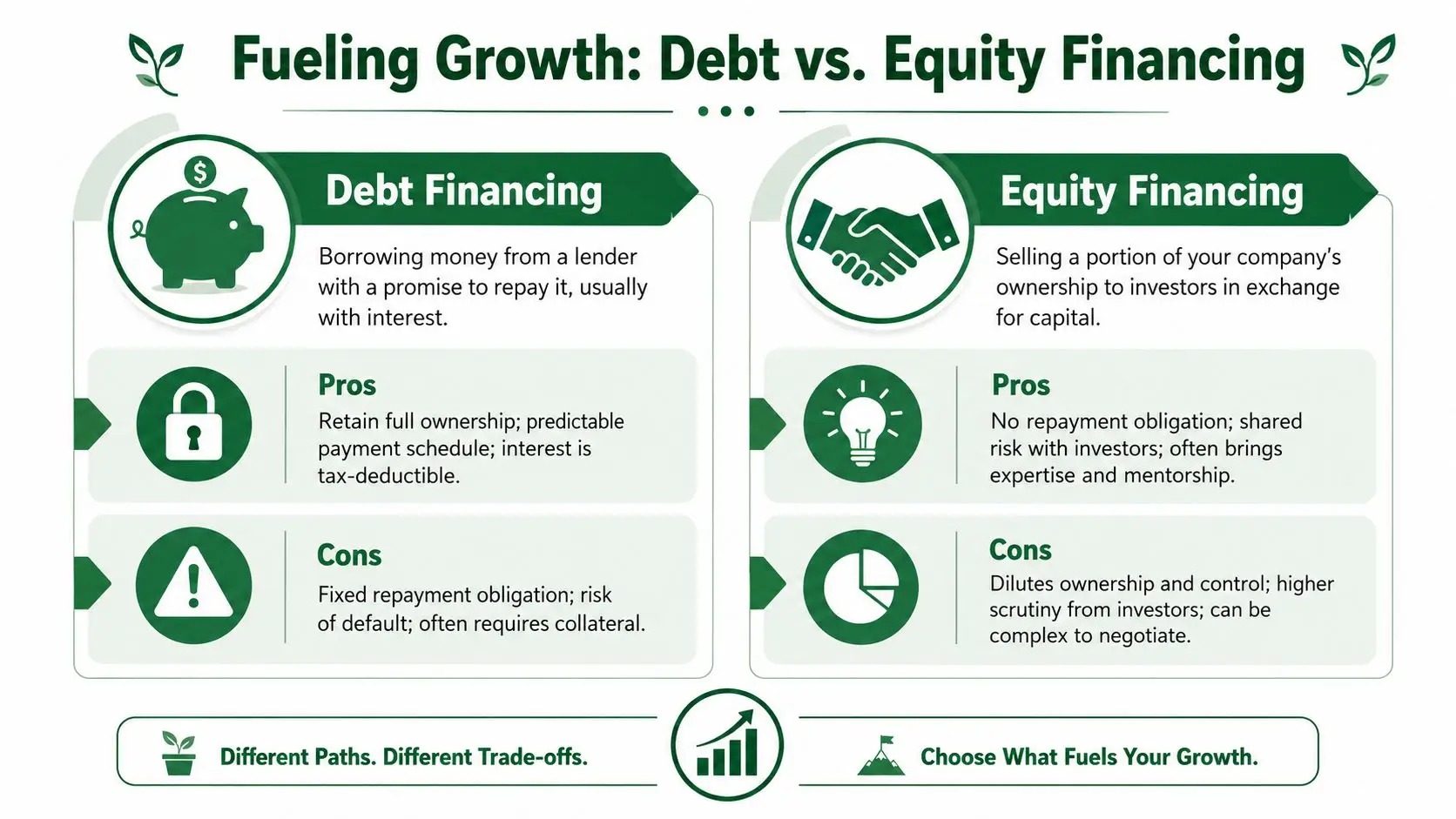

Choosing Your Growth Fuel Debt vs Equity

Lenders decline plenty of profitable businesses for one simple reason. The cash does not support the repayment.

That is the debt versus equity decision. It is not a theory question. It is a fit question.

Debt is rented money. Equity is sold ownership. Debt lets you keep control, but it adds a monthly obligation that shows up whether sales are strong or weak. Equity removes scheduled repayment, but you give up part of the business and often part of the decision-making power that comes with it.

From a lender's seat, debt works best when the business already converts revenue into dependable cash. Equipment purchases, partner buyouts, working capital support, acquisitions, and owner-occupied real estate can all be good debt uses if the business can carry the payment after the money is deployed. Profit on paper is not enough. A borrower needs clean financials, visible repayment ability, and a credible use of proceeds.

Cash flow works like oxygen. Profit can look healthy on paper while the business still struggles to make payroll, cover taxes, buy inventory, and pay the loan on time.

Equity fits a different situation. Early-stage companies, businesses with uneven revenue, and firms choosing to reinvest every available dollar into growth often need patient capital. If the model will not produce stable cash in the near term, fixed loan payments can turn a growth plan into a collection problem.

I tell owners to ask a harder question than "Which is cheaper?" Ask which form of capital matches the speed and reliability of your cash generation. Cheap debt becomes expensive fast if it forces bad operational decisions, delayed payables, or emergency borrowing. Expensive equity can still be the right choice if it buys time to build a model that later qualifies for bank financing.

Debt vs. Equity Financing at a Glance

| Factor | Debt Financing (e.g., SBA Loan) | Equity Financing (e.g., Venture Capital) |

|---|---|---|

| Ownership | You generally retain ownership | You give up a share of ownership |

| Repayment | Fixed repayment obligation | No scheduled repayment |

| Cost structure | Interest and fees | Dilution of future upside |

| Control | Lender oversight is limited to covenants and credit terms | Investors often expect influence or formal governance rights |

| Best fit | Stable businesses with visible repayment ability | High-growth or early-stage businesses with uneven cash flow |

| Main risk | Payment pressure if liquidity tightens | Loss of control and long-term economics |

Owners planning to pursue SBA financing should favor debt only after pressure-testing the file the way an underwriter will. That means current financial statements, tax returns, debt schedules, and a clear use-of-funds story all need to line up. A practical place to start is this SBA loan document checklist for borrowers.

The strongest choice is the one your business can survive, not just the one it can pitch. For established operators, bankable cash health usually points toward debt. For businesses still proving the model, patience often matters more than preserving every point of ownership.

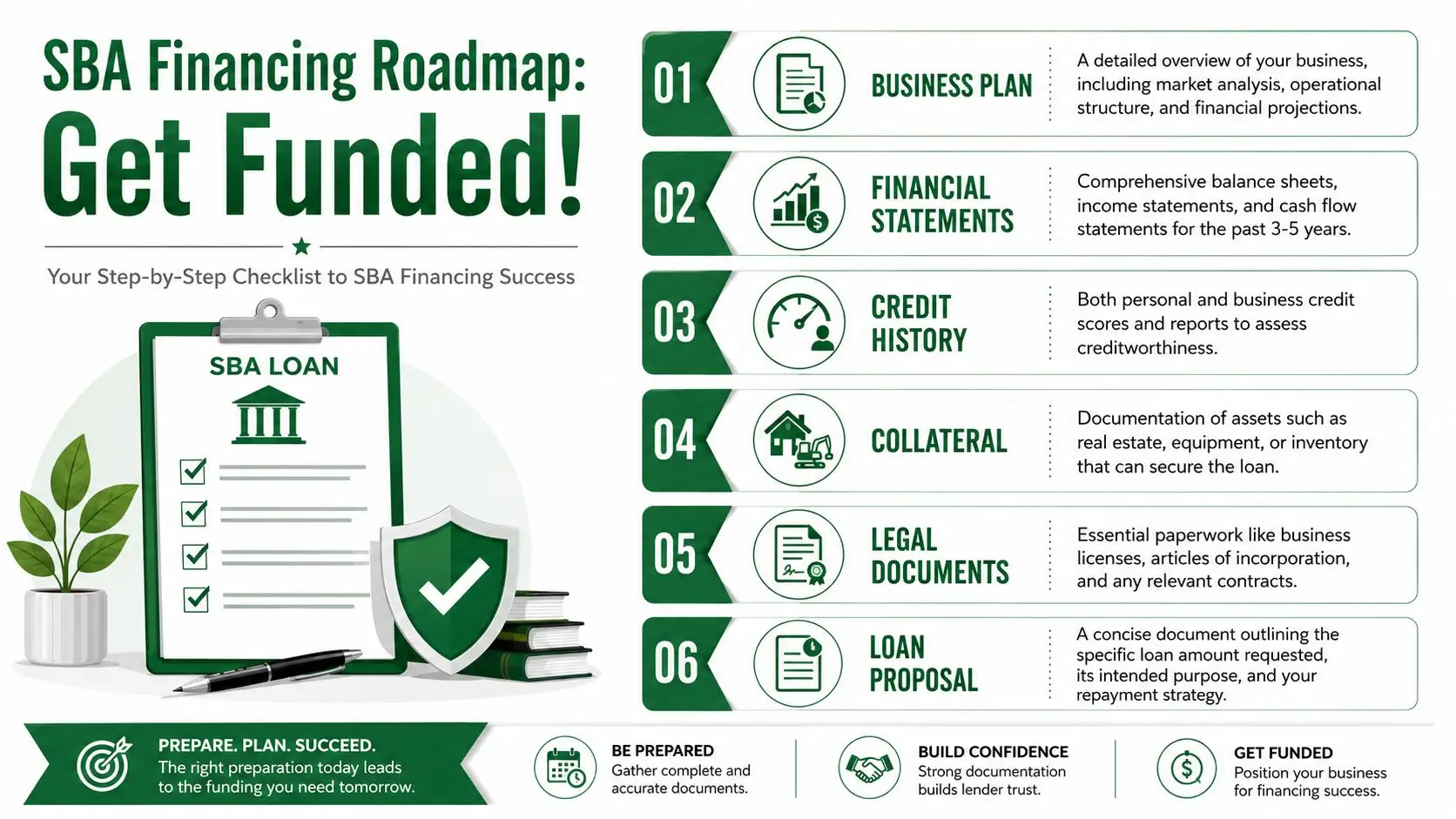

How to Prepare for SBA Financing

SBA financing rewards organized operators. Owners sometimes treat the loan process like a document chase. In practice, approval usually reflects habits built long before the application starts.

The SBA SOP is the main source of truth. It governs how lenders evaluate eligibility, use of proceeds, repayment ability, equity injection, and documentation standards. If you want to be taken seriously, build your file the way an underwriter will read it. That means the narrative, tax returns, interim statements, and projections all need to agree.

Know the structure before you apply

For context, the U.S. Chamber's guide to SBA loans notes that SBA 7(a) loans can go up to $5 million, with variable interest rates typically between 7.5% and 10%. Repayment terms depend on purpose: working capital and equipment loans usually run 7 to 10 years, business acquisitions up to 10 years, and owner-occupied commercial real estate up to 25 years.

Those terms are attractive, but they don't excuse weak preparation. A longer term helps affordability, not credibility. Lenders still want to see repayment capacity, solid management, acceptable credit, and a coherent use of funds.

Your SBA readiness checklist

Strong SBA files usually include the same core components:

- Historical tax returns: These anchor the story. Lenders compare returns to interim statements and explanations from management.

- Current financial statements: Profit and loss, balance sheet, and debt schedule should be current, internally consistent, and easy to follow.

- Cash flow projections: Especially important when the loan supports growth, acquisition, or a turnaround angle.

- Business plan or transaction memo: It should explain what the business does, why the loan makes sense, and how repayment will happen.

- Ownership and legal documents: Entity records, leases, licenses, and organizational documents need to be complete.

- Personal financial information: SBA underwriting looks at the principals, not just the entity.

A lender also looks for signs of operational discipline that don't always appear on a checklist:

- Accurate owner compensation treatment

- Clear explanation for unusual expenses

- Support for add-backs if a business is being acquired

- A sensible post-close cash position

- Realistic assumptions instead of heroic projections

If you're assembling your package, this SBA loan document checklist is a practical reference for the paperwork side.

Owners often think loan readiness begins when they need capital. It usually begins months earlier, when they start closing books cleanly, tracking cash accurately, and building a business that can withstand scrutiny.

Frequently Asked Financial Management Questions

What's the difference between a bookkeeper and an accountant

A bookkeeper records transactions, reconciles accounts, and keeps the day-to-day financial record clean. An accountant interprets the numbers, handles more complex reporting and tax issues, and helps structure decisions correctly.

Small businesses often need both functions, but not always as separate people. Early on, one firm may cover both. The key is making sure the books are accurate before anyone tries to analyze them.

How much cash reserve should a business keep

There isn't one universal number that fits every business. The right reserve depends on seasonality, payroll burden, debt load, customer concentration, and how quickly receivables turn into cash.

The better question is this: how many weak weeks can your business absorb without missing critical obligations? If the answer is “not many,” your reserve policy is too thin.

Can I pay myself from my LLC

Yes, but the method matters. Some owners take draws. Others run payroll, depending on entity type and tax treatment. What matters for financial management is consistency and clean classification.

Random owner withdrawals create confusion in the statements and make lender analysis harder. Pay yourself through a deliberate process that your accountant agrees with.

What's one mistake that hurts fundability fast

Mixing personal and business finances is high on the list. So is giving a lender outdated financials and trying to explain the gaps verbally.

Clean books reduce friction. Messy books create questions, and questions slow approvals.

If you want financing options to stay open, treat your numbers like they'll be reviewed tomorrow. Because eventually, they will.

If you're planning to buy a business, refinance debt, secure working capital, or finance owner-occupied real estate, GoSBA Loans helps borrowers structure cleaner, more fundable SBA loan packages. Their team works across SBA lenders, supports projections and documentation, and guides owners through the process with fewer surprises and stronger execution.