You're probably staring at a deal that looks good on paper. The seller says the phones ring nonstop, the techs are loyal, and the maintenance base is solid. Your broker says it's a strong candidate for SBA financing. Your lender asks for normalized cash flow, customer concentration, EPA documentation, and a transition plan. Suddenly, buying an HVAC business stops feeling like a simple acquisition and starts feeling like an underwriting exercise.

That's the right way to look at it.

If you want to buy an HVAC company in 2026, don't start with the asking price. Start with fundability. A deal that can't survive SBA underwriting usually isn't a good deal. A deal that passes lender scrutiny, survives due diligence, and keeps technicians after closing gives you a real shot at owning a durable business instead of inheriting a mess.

Table of Contents

- Why an HVAC Business is a Top Acquisition Target in 2026

- Sourcing and Valuing Your Target HVAC Business

- The Ultimate HVAC Due Diligence Checklist

- Structuring the Deal and Securing SBA Financing

- From Closing to Your First 90 Days as Owner

- Frequently Asked Questions About Buying an HVAC Business

Why an HVAC Business is a Top Acquisition Target in 2026

HVAC is attractive for one reason that matters more than any sales pitch. People don't postpone heating and cooling problems forever. Units fail. Systems age out. Buildings still need service. That creates repeat demand, replacement demand, and recurring maintenance revenue if the business is run properly.

The opportunity is real

The scale of the market alone should get your attention. The global HVAC market is projected to surge from USD 524.9 billion in 2025 to USD 1.2 trillion by 2035, and the U.S. services market is projected to reach $35.8 billion by 2030 according to GM Insights' HVAC market analysis. The same source notes that 90% of U.S. homes already have HVAC systems, which is exactly why replacement and maintenance matter so much.

That installed base is what makes this industry lender-friendly when the company has recurring revenue and decent books. You're not betting on a brand-new category. You're buying into a mature service business tied to equipment that already exists in homes and commercial buildings.

Electrification also matters. The market is shifting, and buyers who understand heat pump demand, replacement cycles, and service mix will have a better long-term position than buyers who think this is just a furnace-and-AC business.

For a sense of how lenders think about the space, review the best HVAC and plumbing SBA lenders. The right lender won't just like the industry. They'll understand the cash flow pattern behind it.

The risks are just as real

This isn't a passive business. It's operationally heavy, labor-dependent, and unforgiving when leadership is weak.

The best HVAC acquisition targets aren't the businesses with the loudest growth story. They're the ones that can survive underwriting, absorb debt, and keep producing after the seller steps back.

If you're buying an HVAC business, assume the problem isn't demand. The problem is execution. Dispatch failures, sloppy job costing, weak collections, bad inventory controls, and owner dependence destroy value fast. A growing market won't save an operator who can't keep technicians, price work correctly, or manage service agreements.

Treat HVAC as a strong acquisition category with hard edges. That mindset will keep you disciplined when sellers oversell “potential” and underdocument reality.

Sourcing and Valuing Your Target HVAC Business

You find a seller with solid revenue, a clean-looking CIM, and a price that seems workable. Then the SBA lender asks three basic questions. How much of the revenue repeats, how much depends on the owner, and how cleanly the financials support cash flow. If you cannot answer those fast, you do not have a real target yet.

That is the right frame for sourcing. Do not shop for HVAC businesses the way retail buyers shop for listings. Shop for deals that can survive underwriting.

Where financeable HVAC deals come from

Brokered deals give you speed. You get a package, a process, and enough information to screen the business quickly. That helps if you want volume. It also creates a problem. Sellers and brokers often set price off top-line revenue or a flattering SDE number before anyone has tested whether the earnings hold up under SBA review.

Off-market sourcing takes more work and usually produces thinner initial information. I still like it better for many HVAC buyers. You can ask better questions earlier, get closer to the owner's real transition plan, and shape seller note terms before the deal gets over-marketed. That matters because SBA lenders care about continuity after close. If the business falls apart when the seller leaves, the loan is harder to place.

My recommendation is simple. Use both channels, but screen every deal with lender logic from day one. If a target cannot show clean tax returns, segmented revenue, and a believable post-close transition, move on.

What actually drives value

HVAC sellers love to talk about total sales. Lenders do not lend against excitement. They lend against cash flow that is documented, durable, and likely to continue after ownership changes.

Start with SDE if the business is small. Then get stricter. Break revenue into service, maintenance agreements, replacements, new construction, and larger project work. A service-heavy company with a real maintenance base usually gets better pricing and better loan reception than an install-heavy company living off one hot season and a few referral relationships.

Customer mix matters too. Industry operators at ServiceTitan explain that buyers value recurring maintenance revenue, strong customer retention, and a diversified book of business because those factors improve predictability and reduce transition risk in HVAC acquisitions, as outlined in ServiceTitan's HVAC valuation guide.

Use that standard when you screen targets:

- Recurring maintenance revenue: Service agreements support cash flow consistency and give lenders more comfort.

- Revenue split by line of business: Service and replacement revenue usually underwrite better than project-driven installation revenue.

- Customer concentration: A business tied to one builder, property manager, or commercial account deserves a lower valuation.

- Seller dependence: If the owner prices jobs, handles key relationships, and solves dispatch problems personally, the business is worth less.

- Financial cleanup risk: If the books do not separate add-backs, personal expenses, and one-time costs clearly, expect value to compress.

If you want a practical companion piece on pricing logic, Pipeline On's guide to HVAC business value is worth reading. It keeps the focus where it belongs: earnings quality, not vanity metrics.

HVAC Business SDE Multiples by Revenue Source

| Primary Revenue Source | Typical SDE Multiple | Perceived Risk |

|---|---|---|

| Service agreement heavy | Higher | Lower |

| Balanced service and installation | Mid-range | Moderate |

| Installation heavy and project-driven | Lower | Higher |

| Owner-dependent mixed revenue | Lower | Higher |

Use that table as a first-pass filter, not a pricing formula.

A multiple is only as good as the cash flow behind it. If the seller's SDE depends on underpaid family labor, deferred truck replacements, or an owner who still sells every major job, your real multiple is lower whether the seller likes it or not.

Practical rule: If a seller cannot show recurring revenue, customer retention, and clean earnings by service line, value the deal conservatively or walk away.

Before you discuss price seriously, compare your number to how lenders will review it. This SBA business valuation guide from GoSBA Loans explains how lenders and valuation providers test acquisition value, cash flow support, and purchase price reasonableness.

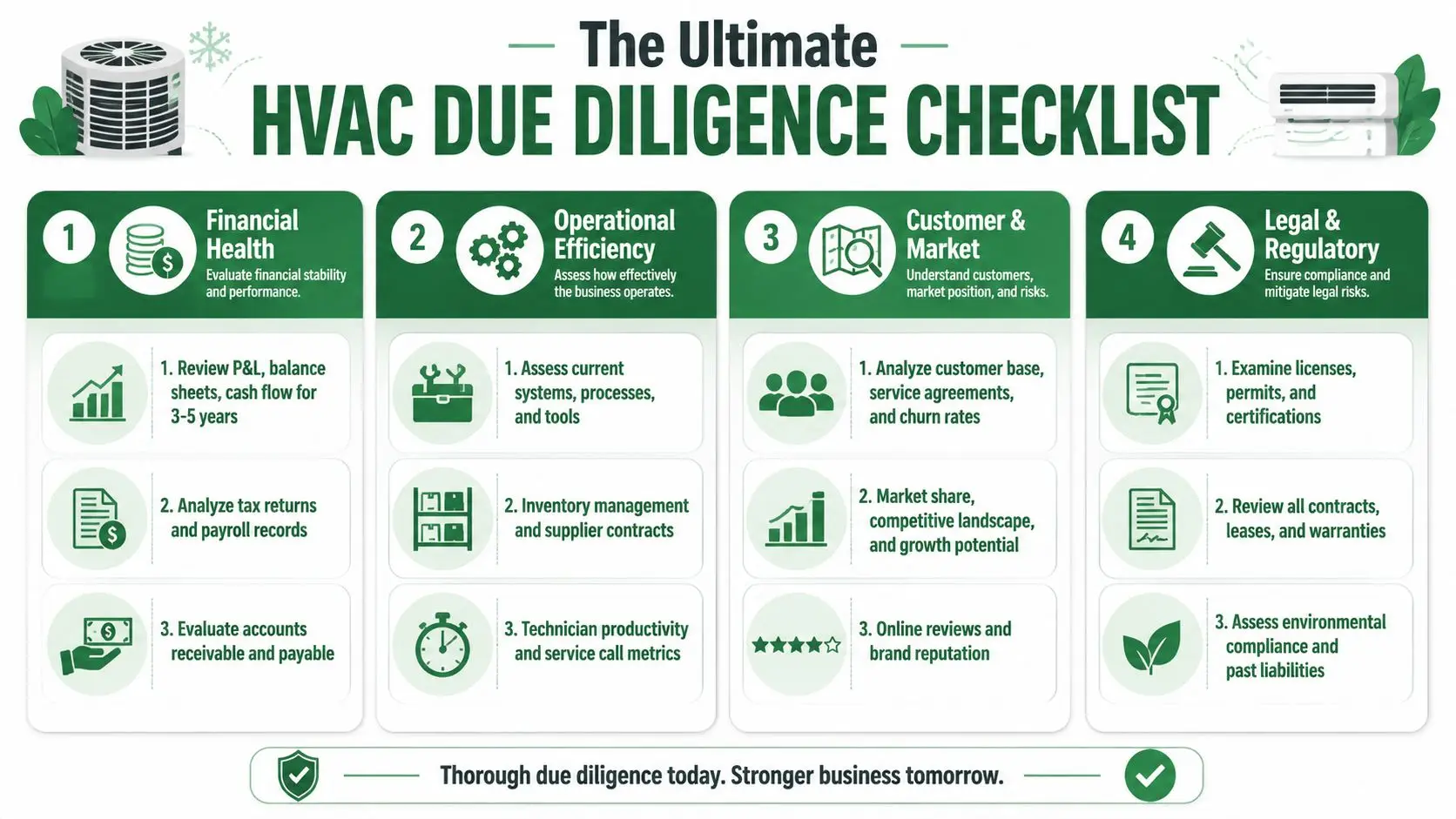

The Ultimate HVAC Due Diligence Checklist

You sign an LOI on Friday. By Monday, your lender asks for tax returns, aging reports, payroll detail, customer concentration, lease terms, licenses, and a clear explanation of how the seller's cash flow survives after the owner leaves. That is the diligence test in an HVAC acquisition. If the file does not hold up under SBA underwriting, the deal is weak no matter how good the story sounds.

Buyers get in trouble when they treat due diligence like a generic checklist. HVAC deals live or die on service mix, technician stability, licensing, truck and inventory condition, and whether recurring maintenance revenue is real. Your job is to verify what a lender will underwrite, not what a broker wrote in the teaser.

Financial records that lenders will trust

Start with the documents that support repayment. You need 3 to 5 years of tax returns, profit and loss statements, balance sheets, year-to-date financials, payroll reports, and a seller earnings adjustment schedule that makes sense, according to Acquisition Stars' guide to buying an HVAC business. If the seller cannot break out service, replacement, installation, and maintenance agreement revenue cleanly, expect the lender to question both cash flow quality and valuation.

Run a hard reconciliation. Internal financials should match filed tax returns. Payroll should match the technician roster. Credit card statements and bank statements should support any large add-backs. If the seller calls half the expense base “discretionary,” assume it is not.

Use a lender-first review:

- Revenue reconciliation: Match monthly sales in the P&L to tax returns and merchant or bank deposits.

- Margin by service line: Compare gross margins on service, install, and maintenance. Wild swings usually mean bad job costing or messy books.

- Accounts receivable aging: Old receivables belong in your haircut to working capital, not in your valuation.

- Deferred revenue and prepaids: Maintenance plans create future labor obligations. SBA lenders will want that understood before closing.

- Capital expenditure reality: If trucks, tools, or warehouse equipment are overdue for replacement, adjust your cash flow expectations now.

For a practical framework, use this M&A due diligence checklist for SBA-backed acquisitions.

Operational checks that actually matter

A decent P&L can hide a fragile operation. I see this constantly. The seller still approves pricing, handles angry customers, dispatches around callouts, and closes replacement jobs. That company will feel very different 30 days after closing.

Trace the work from first call to cash collection. Review call intake, dispatching, field invoicing, financing offers, maintenance renewals, quoting, and install scheduling inside the actual software the team uses. If the business runs on memory, text messages, and one office manager's notebook, your transition risk is high and your lender should hear that early.

Ask direct questions and verify the answers:

- Who sells replacement jobs over a certain dollar amount?

- Who manages permits and inspection follow-up?

- Which technicians produce the highest revenue, and are they under contract or free to leave?

- How many customers come from maintenance agreements versus one-time jobs?

- What happens operationally when the seller is out for a week in peak season?

If the seller says the team can handle it, prove it with dispatch records, CRM workflows, maintenance renewal reports, and technician performance data.

Legal, licensing, and inventory problems that kill deals late

First-time buyers often lose time and money when navigating the acquisition process. HVAC is licensed, permit-driven, and operationally dependent on compliance. If you wait until drafting to check license transferability, qualifier requirements, EPA certification records, or local permit history, you are already behind.

Confirm exactly which entity holds each license, who the qualifying party is, and whether a change of ownership triggers a new application, a notice filing, or a gap in operating authority. Review service agreements for assignment restrictions. Check leases for landlord consent. Pull UCC searches so you know whether trucks, equipment, or receivables are already pledged.

Inventory also gets mishandled. As noted earlier in the Acquisition Stars source, buyers need a defined inventory valuation method and should remove obsolete stock from the deal economics. Shelves full of outdated parts are not working capital. They are cleanup.

Review these items with your attorney, accountant, and lender before you remove contingencies:

- Licenses and certifications: Confirm HVAC contractor licensing, EPA records, permits, and transfer rules by state and municipality.

- Inventory aging and usability: Separate active truck stock and fast-moving warehouse parts from dead stock.

- Service contract terms: Check renewal dates, cancellation language, prepaid amounts, and transfer rights.

- Vehicle and equipment title: Verify what is owned, financed, leased, or personally held by the seller.

- Open claims and disputes: Ask for warranty claims, workers' comp history, pending litigation, and customer refund issues.

Good HVAC diligence is boring. Keep it that way. If a file is clean enough for an SBA lender to underwrite confidently, you usually have a deal worth buying.

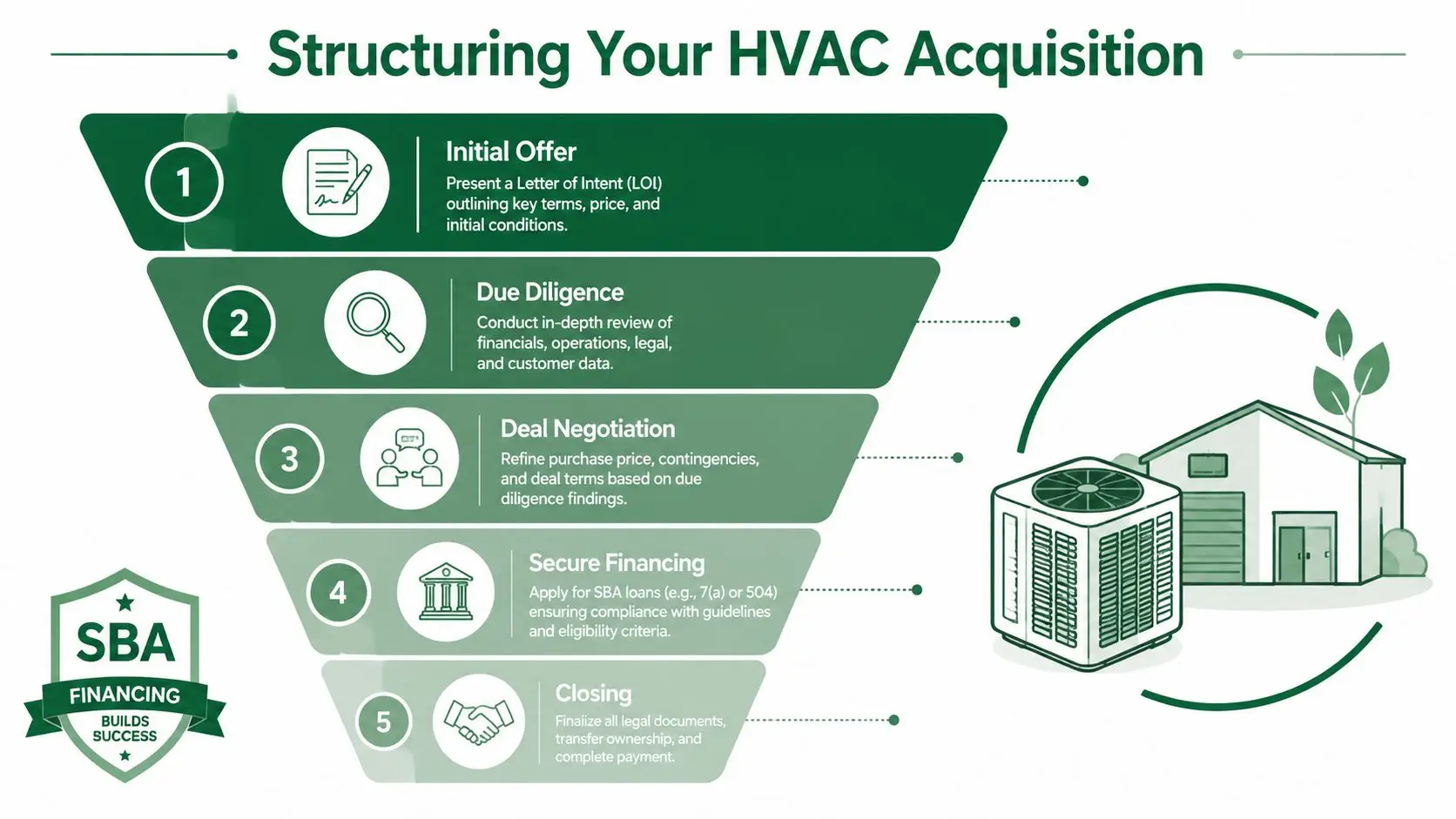

Structuring the Deal and Securing SBA Financing

You sign an LOI on Friday. By Tuesday, your lender tells you the seller note is wrong, the working capital language is vague, and the transition plan is too thin for credit approval. That is how HVAC deals die. The problem usually is not the business. The problem is a structure that looked fine to a broker and fails under SBA underwriting.

Start with the loan, then build the purchase around it.

Build the deal so the lender can say yes

For SBA 7(a) change-of-ownership loans above $500,000, the buyer typically needs to inject at least 10% equity into the total project cost. The SBA lays out program terms, guaranty limits, and eligibility rules on its official 7(a) loan program terms and conditions page. If you do not know where that 10% is coming from before you negotiate price, you are not ready to make an offer.

In HVAC acquisitions, the cleanest structure is usually straightforward. Buyer cash. SBA senior debt. Seller note on full standby when needed. Full standby matters because a properly documented seller note can help satisfy part of the required equity injection under SBA rules if your lender accepts that structure.

Price is only one part of fundability. The lender also has to get comfortable with debt service coverage, post-close liquidity, and whether the business can survive the ownership transition without a revenue drop.

That means your LOI should answer four questions clearly:

- What exactly is being bought: assets, stock, or membership interests

- How much working capital stays in the business at closing

- Whether the seller is carrying a note, and whether it will be on full standby

- How long the seller will stay involved after closing

If those terms are vague, underwriting gets messy fast.

What SBA lenders actually focus on in HVAC deals

HVAC businesses can finance well under SBA because the model is understandable. Recurring maintenance revenue helps. Replacement demand helps. Established dispatch history helps. But lenders still kill deals for the same reasons over and over.

First, cash flow has to support the new debt after a realistic owner salary. Add-backs need to be defensible. If the seller runs personal expenses through the business, document them. If the deal only works by stripping out every questionable expense, the deal does not work.

Second, transition risk has to be contained. HVAC companies often depend heavily on the owner for sales, estimating, or technician retention. If the seller disappears at closing, expect your lender to push hard on continuity. A signed consulting agreement with defined duties is better than vague promises about being "available if needed."

Third, the working capital position has to make sense. Buyers regularly overpay for a business and then starve it of cash the day they take over. Payroll, fuel, inventory replenishment, insurance, and slow collections do not wait because you used every dollar for the down payment.

Use this checklist when you structure the file for credit:

- Purchase price allocation: Match the allocation to tax strategy and lender expectations early, not a week before closing.

- Equity injection: Show the exact source of the buyer's cash and document any seller standby note correctly.

- Debt service coverage: Underwrite the business on actual run-rate performance, not on the seller's best month.

- Transition agreement: Put the seller's training period, compensation, and responsibilities in writing.

- Working capital: Define a target amount or a peg so the business is not underfunded on day one.

- Closing timeline: Build in enough time for underwriting, appraisal if needed, life insurance, entity docs, and landlord or franchisor consents.

A lender-friendly structure is usually a buyer-friendly structure too.

If you want a practical overview of how lenders review these transactions, read this SBA business acquisition loan guide. Then make sure the business can produce timely financials, service agreement reports, and job-level margin data in one place. Buyers who achieve total control for your HVAC company with better software usually have an easier time defending projections and managing the handoff after closing.

One more recommendation. Do not get cute with earnouts, aggressive seller consulting fees, or side agreements that change the economics after the fact. SBA lenders review the full transaction. If the structure looks engineered to avoid policy, expect delays, rewrites, or a decline.

Creative deals are fine. Fundable deals are better.

From Closing to Your First 90 Days as Owner

Day one after closing feels great for about six minutes. Then your phone starts buzzing. A customer wants an update on an install. A dispatcher needs approval on a schedule issue. A lead tech wants to know whether compensation is changing. This is the part buyers underestimate.

The first ninety days decide whether the business keeps its value.

Days 1 to 30 stabilize the business

Your first job isn't fixing everything. Your first job is preventing unnecessary loss.

The HVAC industry faces a skilled labor shortage of 110,000 technicians in the U.S., which remains the number one operational challenge for owners, according to ServiceTitan's HVAC industry statistics. That's why technician retention has to be your first operational priority.

Meet every employee quickly. Talk to the top technicians first, then dispatch, then office staff. Tell them what is not changing immediately. If people think a new owner is about to disrupt pay, schedules, or culture without understanding the business, they'll start returning recruiter calls.

Also contact your top customers. Not with a generic mass email. Use direct outreach for accounts that matter most. You're trying to preserve trust, not announce a branding exercise.

Days 31 to 60 learn the operating rhythm

Now you get into the machinery of the business. Ride along on service calls. Sit with dispatch. Review open estimates. Watch how maintenance agreements are renewed and how invoice collections happen.

If the company lacks operating visibility, fix that before you chase growth. A good field management platform can help you centralize scheduling, service history, invoicing, and inventory. If you're evaluating software options after closing, this resource on how to achieve total control for your HVAC company gives a practical overview of what stronger operational control should look like.

Here's what you're listening for in this phase:

- Technician frustration: Poor routing, bad parts availability, and messy handoffs usually show up fast.

- Customer pain points: Delayed callbacks and missed updates kill confidence.

- Cash flow friction: Slow billing and weak collections create avoidable stress.

Days 61 to 90 make only the changes that matter

By this point, you should know the difference between cosmetic improvements and real bottlenecks. Make a small number of changes with visible value. Don't launch a total overhaul because you're eager to “put your stamp on it.”

Good first moves include tightening estimate follow-up, improving dispatch accountability, and setting a simple weekly review cadence around booked jobs, open receivables, and service agreement renewals. Bad first moves include changing compensation plans too early, replacing software without preparation, or layering in corporate reporting nobody needs.

For a broader transition checklist, the business acquisition first 90 days guide is worth keeping nearby during the handoff.

Keep the business steady long enough to understand it. Most value destruction in acquired service companies comes from rushed changes, not from moving too slowly.

Frequently Asked Questions About Buying an HVAC Business

Do I need HVAC industry experience to get approved

Not always, but lack of industry experience raises the bar everywhere else. If you're not an HVAC operator, the lender will look harder at your management plan, seller transition, and who will run day-to-day operations. A strong general manager, service manager, or retained seller can offset a thin personal background.

What won't work is pretending the business runs itself. HVAC is operational. If your plan is absentee ownership from day one, expect lender resistance and post-closing headaches.

What is a working capital adjustment at closing

It's the mechanism that makes sure the business is delivered with a normal level of short-term operating assets and liabilities. In HVAC, that usually means looking closely at accounts receivable, usable parts inventory, and obligations tied to prepaid service agreements.

Sellers often focus on purchase price while buyers end up funding the gap if receivables are weak or inventory is overstated. Therefore, you want the LOI and purchase agreement to define the methodology clearly, especially around obsolete parts and what counts as good inventory.

What financial ratio matters most to SBA lenders

For acquisition approval, SBA lenders focus heavily on Debt Service Coverage Ratio, or DSCR. The borrower must show that projected cash flow can cover the new debt, and the minimum threshold is 1.10:1, according to Lendio's SBA 7(a) loan explanation.

That number is simple, but it drives real decisions. If the deal only works with aggressive add-backs, unrealistic cost savings, or fantasy growth, the DSCR will expose it. A lender may still like the industry and still decline the deal.

My advice is straightforward. Underwrite your own DSCR before you spend heavily on third-party reports. If the cash flow barely clears the requirement on a best-case basis, renegotiate price or structure. Don't hope underwriting will save a weak acquisition thesis.

If you're buying an HVAC business and want a lender-ready structure before you waste time on the wrong deal, GoSBA Loans can help you map the financing, pressure-test the cash flow, and coordinate the SBA process from LOI through closing.