Most advice on how to buy a company with no money is wrong in the way that matters most. It treats financing like a slogan instead of a structure. In the SBA world, structure is everything.

If you want the straight answer, here it is. You can't buy a business with zero buyer contribution in a standard SBA 7(a) change-of-ownership deal. The SBA SOP is the source of truth, and it doesn't support the fantasy version. What it does support is a low money down acquisition that can be assembled in a compliant way if the target cash flow is strong, the seller cooperates, and the capital stack is built correctly.

That distinction matters because buyers don't lose deals over motivation. They lose them over mechanics. They chase businesses they can't qualify for, negotiate seller notes that don't meet underwriting standards, or assume a bank will overlook a weak file because the business "looks solid." It won't.

Table of Contents

- The No Money Down Myth vs The Low Money Down Reality

- The Three Pillars of a Leveraged Acquisition

- Your Playbook for the SBA 7(a) Acquisition Loan

- How to Structure a 5 Percent Down Capital Stack

- Your Negotiation and Due Diligence Priorities

- Timeline Risks and Why an Expert Broker Matters

The No Money Down Myth vs The Low Money Down Reality

The phrase buy a company with no money gets clicks because it promises a loophole. In real SBA lending, there isn't one.

The hard rule is simple. The SBA explicitly mandates that the minimum down payment from the borrower must be at least 10% of the total business cost, and that equity injection requirement is not optional, as explained in this discussion of SBA acquisition funding rules. That means a literal zero-dollar close doesn't fit the standard playbook.

What buyers can do is build a compliant low-cash structure using other people's money. That usually means some combination of senior bank debt, seller participation, and in some cases outside equity. The buyer's job isn't to invent a clever phrase. It's to assemble a file a lender can approve.

Why the internet gets this wrong

A lot of online advice mixes together different deal types and calls them all "no money down." That's sloppy. An earn-in for a service business isn't the same as an SBA-financed stock or asset acquisition. A rollover isn't the same as a standby seller note. An internal succession plan isn't the same as a third-party purchase.

If you're pursuing an SBA 7(a) change of ownership, the better question isn't "How do I avoid all cash in?" The better question is, "How do I get to the lowest buyer cash contribution the SOP and the lender will accept?"

Practical rule: Stop chasing zero. Chase a structure that closes.

What low money down actually looks like

In practice, a low money down deal means you still respect the equity injection requirement, but you don't necessarily fund all of it with cash sitting in your checking account. That's where deal structure matters. If you want a plain-English breakdown of acceptable injection sources, this guide to SBA 7(a) down payment sources is useful.

That shift in thinking changes how you search for deals. You stop looking for any business you "like" and start looking for one that supports substantial external funding. The business must be profitable, the historical cash flow must survive lender scrutiny, and the seller has to be realistic about how the transaction gets financed.

A buyer who understands that early has an edge. They submit cleaner LOIs, ask sharper questions, and avoid dead-end deals that look attractive until the lender opens the file.

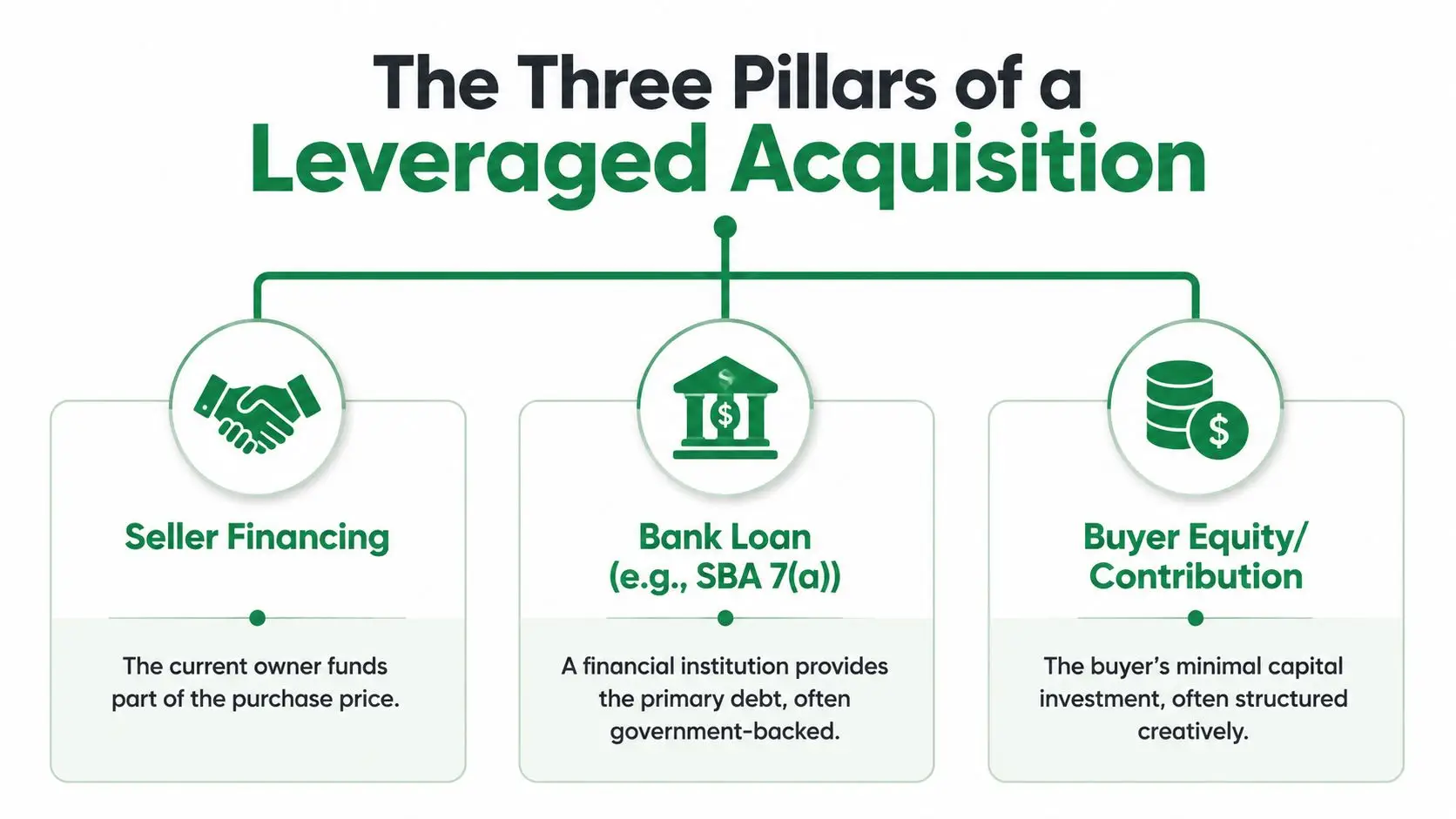

The Three Pillars of a Leveraged Acquisition

A low-cash acquisition works when three funding sources line up. Miss one, and the deal usually falls apart.

What seller financing really does

Seller financing isn't just a concession. It's a signal.

When a seller carries part of the deal, the lender reads that as confidence in the business and in the transition. Sellers agree to it for practical reasons. It can widen the buyer pool, keep a deal alive when cash is tight, and help bridge valuation disagreements without cutting headline price.

The mistake buyers make is treating seller financing as one generic concept. It isn't. The note terms drive whether the paper helps the deal or hurts it. In an SBA context, the lender cares about standby, payment timing, and how the note interacts with debt service.

The bank loan is the engine

For most small-business acquisitions, the SBA 7(a) loan is still the workhorse. It allows lenders to fund up to 90% of total project cost, including purchase price, working capital, and closing costs, according to this overview of SBA acquisition leverage mechanics.

That substantial financing is what makes the whole model viable for first-time buyers and owner-operators. If you want a broader comparison of how acquisition debt is typically layered, the Business Loan Warrior guide is a helpful outside reference because it frames SBA financing alongside other acquisition loan options instead of pretending one product fits every deal.

Buyer equity still matters

Even in a debt-heavy transaction, lenders want to see that the buyer is invested. Not just emotionally. Financially.

That contribution can come from personal cash, eligible assets, outside investors, or a carefully structured stack that reduces the buyer's direct cash burden. But the buyer still has to show commitment, liquidity, and the ability to manage the business after closing.

A weak buyer contribution doesn't just affect approval. It changes how every lender in the market prices risk on the file.

Where earn-ins fit

An earn-in is a different animal, but it deserves attention because it's becoming more common in service businesses. Emerging earn-in acquisitions, where the buyer trades sweat equity for ownership over 12 to 24 months, have seen a 35% increase in adoption as owners face retirement fatigue, according to this review of earn-in acquisition trends.

That structure can work well when the business value depends more on operations, client retention, and management continuity than on hard assets. It doesn't replace the SBA route for a standard third-party acquisition. But for the right service business, it can be a legitimate path for a buyer whose main currency is execution rather than cash.

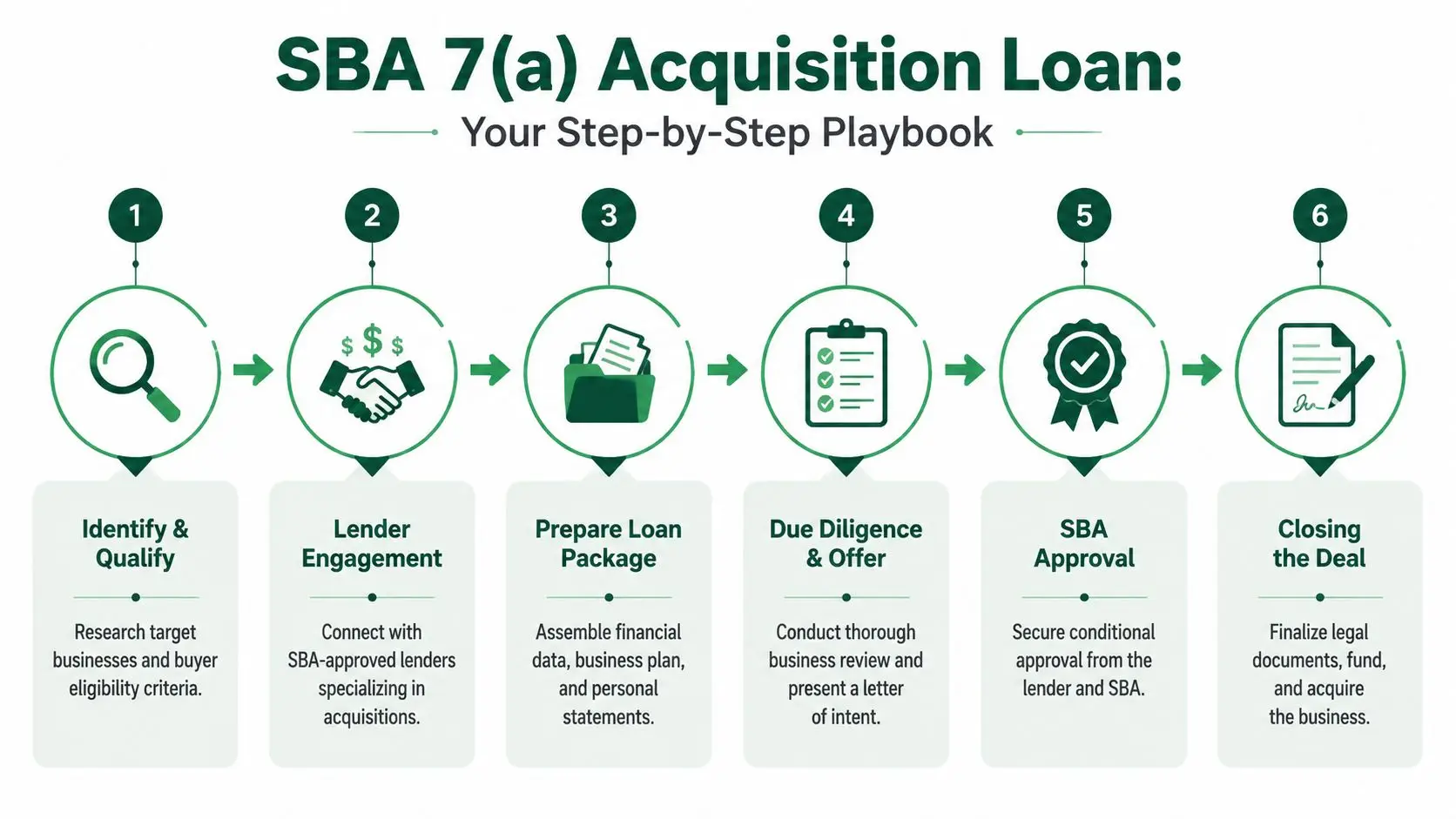

Your Playbook for the SBA 7(a) Acquisition Loan

“No money down” is the wrong target. The correct target is an SBA-compliant deal where the buyer brings the minimum cash the SOP requires and structures the rest correctly.

What the SOP allows

Under SBA SOP 50 10 8, a complete change of ownership still requires a 10% equity injection, and at least 5% must come from the buyer's own cash or eligible assets, as summarized in this explanation of SBA 7(a) ownership-change requirements. That is the rule that turns this from a “buy a company with no money” pitch into a real 5% down acquisition plan.

In practice, the bank funds the senior debt. The buyer covers at least half of the injection. The remaining portion can sometimes come from a seller note if the note is written to satisfy SBA and lender policy. For a broader technical reference on eligibility, pricing, and underwriting mechanics, see this 2026 SBA 7(a) loan guide.

The ownership piece also trips people up. Standard SBA 7(a) business acquisition loans are generally built around a 100% change of ownership, as outlined in this complete SBA acquisition guide. If the seller wants to keep a meaningful equity stake after closing, the file often stops fitting the plain-vanilla structure many buyers assume will work.

That is why internet advice about “creative” partial buy-ins usually falls apart once a lender reads the purchase agreement.

What full standby means in practice

Seller paper only helps if it meets the standby rules the bank will accept. For a seller note to count toward the required injection in many SBA acquisition deals, lenders commonly want full standby for 24 months, consistent with SBA policy discussions covered in the SOP and lender guidance. The standby treatment is also discussed in the RNC M&A financing guide, which is useful for comparing how acquisition capital stacks are structured across funding types.

Full standby means no principal and no interest payments during the standby period. If the seller expects monthly payments right after closing, that note may still exist, but it usually will not help reduce the buyer's cash requirement.

I see this issue derail deals more than bad credit does. A buyer gets comfortable with a 5% cash plan, signs an LOI, pays for diligence, and then learns the seller note is amortizing from month one. At that point, someone has to fill the gap with cash, a gift, an investor, or a re-trade.

The clean approach is simple. Get the seller-note terms aligned before underwriting starts. If the note is supposed to support injection, document standby clearly in the LOI and make sure counsel drafts it that way in the purchase package.

How to Structure a 5 Percent Down Capital Stack

A 5% down acquisition is usually not a "no money down" deal in disguise. It is a tightly documented SBA structure where the buyer brings part of the injection in cash and the seller fills the rest with note terms the lender and the SOP can accept.

Use a simple example.

Example capital stack for a 2M acquisition

| Source of Funds | Standard 10% Down Deal | 5% Down Deal |

|---|---|---|

| Purchase price | $2,000,000 | $2,000,000 |

| SBA loan | $1,800,000 | $1,800,000 |

| Buyer cash injection | $200,000 | $100,000 |

| Seller note counted toward injection | $0 | $100,000 |

What the table tells you

The buyer is not borrowing more from the bank. The SBA loan amount stays the same in this example. The difference is that half of the required injection comes from the buyer's cash and half comes from seller paper that is structured correctly.

That distinction matters because buyers often focus only on the check they need to bring to closing. Underwriting does not stop there. The lender still has to get comfortable with post-closing cash flow, management fit, global liquidity, and whether the business can carry the new debt load at the note rate being quoted.

In practice, I underwrite these deals in two passes. First, I confirm the stack is SBA-compliant. Second, I test whether the business still supports debt service with room for error. If coverage is thin, a 5% structure does not fix the deal. It just gets the file to a decline faster.

A clean 5% stack usually has four features:

- The buyer contributes the required cash at closing.

- The seller note is drafted in a form the lender will count toward injection.

- The purchase agreement, note, and standby terms match each other.

- The cash flow still works after adding SBA debt service.

Interest rate pressure is part of the math. SBA 7(a) acquisition loans are commonly variable-rate loans, and payment sensitivity can change quickly when rates move. The SBA publishes current 7(a) loan program details and rate framework, and lenders will size the deal based on their own credit box, including debt service coverage expectations.

That is why a 5% plan needs to be built backwards from underwriting, not forwards from optimism.

For a broader look at how buyers mix bank debt, seller paper, and other financing sources in acquisitions, the RNC M&A financing guide is a useful outside read. If you want the SBA-specific version, this guide to seller note rules for 5% down acquisitions covers the standby and injection mechanics in more detail.

Underwriting lens: Ask whether the company still services debt comfortably after closing, not whether the down payment looks manageable on paper.

Your Negotiation and Due Diligence Priorities

In a low money down deal, the most important negotiation point often isn't price. It's whether the seller will sign paper the lender can live with.

Negotiate standby before you negotiate vanity terms

Buyers waste time arguing over small headline wins while ignoring the one term that determines whether the capital stack works. If the seller won't agree to standby treatment that fits lender requirements, the rest of the negotiation is mostly theater.

Good framing helps. Explain that seller participation expands the financing path and increases certainty of close. Many sellers care less about carrying paper in the abstract than they do about whether the buyer can get funded.

Use a short list when you negotiate:

- Standby first: Confirm whether the seller will accept a note that fits SBA and lender standards before refining less important legal points.

- Transition support second: Clarify how the seller will help during handoff so the lender sees continuity, not disruption.

- Price third: Keep valuation discussion tied to cash flow and fundability, not ego.

Underwrite the business like the lender will

Due diligence for an SBA-backed acquisition isn't just about confirming inventory, leases, or customer lists. The lender is trying to determine whether the business can absorb acquisition debt without breaking.

One important screen is the target's existing debt levels. The business's balance sheets must show a debt-to-worth ratio of no greater than 9:1 prior to the change of ownership, or the file can be disqualified, according to this explanation of SBA business acquisition loan requirements.

That should change what you ask for early. Pull the historical financials, review normalization carefully, and test whether the business still holds up after realistic debt service. Don't rely on seller narratives.

A basic diligence package should include:

- Balance sheet review: Check debt levels, working capital position, and any liabilities that don't show up clearly in summary materials.

- Cash flow support: Verify the earnings that will support the proposed debt load.

- Required forms and reports: Make sure the borrower package is complete and lender-ready. This SBA acquisition due diligence checklist is a practical reference for what buyers should gather before underwriting gets serious.

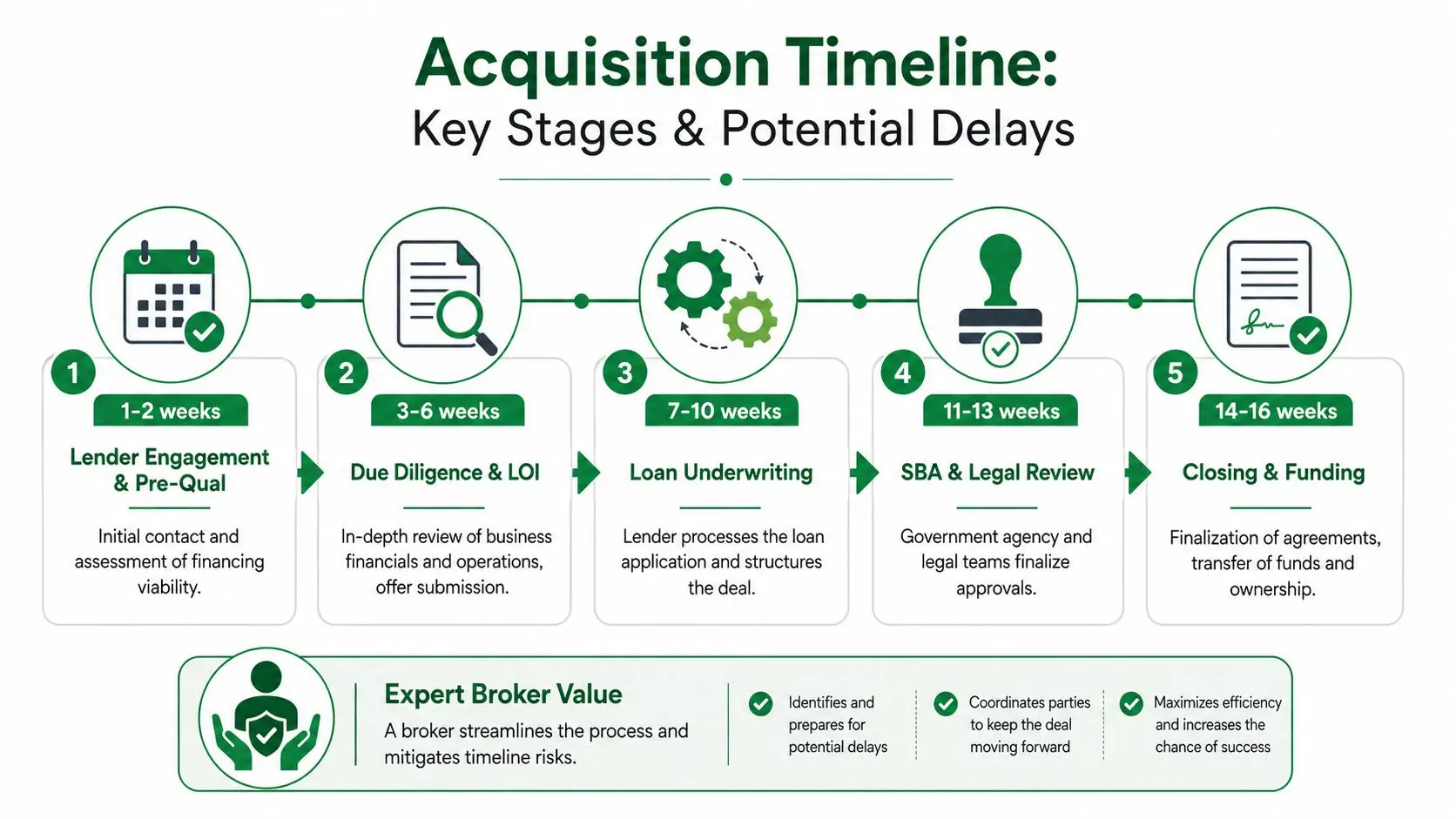

Timeline Risks and Why an Expert Broker Matters

Low-money-down acquisitions usually do not fail because the buyer lacks ambition. They fail because the deal gets out of sequence.

A clean SBA acquisition file can move at a reasonable pace. A messy one drifts for weeks, then dies in underwriting, legal, or closing. The problem is not usually one dramatic issue. It is a series of small misses: outdated financials, a seller note drafted the wrong way, a valuation ordered too late, insurance not lined up, or a lease assignment that the landlord sits on until the last minute.

I see the same choke points repeatedly:

- Borrower package problems: missing personal financial statements, unexplained credit issues, tax return gaps, or a resume that does not support the operating story the lender is trying to approve

- Seller responsiveness: delayed year-to-date financials, weak add-back support, unresolved tax balances, or inconsistent answers between the CIM, LOI, and underwriting package

- Third-party timing: business valuation, lease review, insurance, entity formation, and closing counsel all take time, and none of them improve when ordered late

- Structure mistakes: equity injection sourced incorrectly, seller standby language that does not match SBA requirements, or rollover funds that are not documented cleanly

The structure issues are the ones that waste the most time because they often surface after the buyer has already paid for diligence. Under the SBA's current SOP, a buyer trying to get to 5 percent down has very little room for sloppy drafting. If the seller note is supposed to count toward part of the equity injection, the standby terms have to be right. If they are not, the lender will treat that note as debt service pressure instead of equity support, and the file can stop right there.

Cash flow still decides the file. But timing decides whether the file even gets to credit approval.

A good broker helps before submission, not just after a lender asks for more items. That means stress-testing the capital stack against SBA rules, spotting documentation problems early, and matching the deal to lenders that specialize in change-of-ownership transactions. A buyer can read SOP guidance and still miss how lenders apply it in practice. That is the practical value of working with an SBA loan broker for business acquisition financing.

One example. A buyer signs an LOI on a service business with 10 percent seller carry, plans to use retirement funds for the rest, and assumes the note solves the down payment problem. Two weeks later, underwriting asks whether the seller note is on full standby for the required period, whether the rollover funds are fully documented, and whether the post-close business still meets debt service coverage after normalizing payroll correctly. If those answers are not ready, the timeline slips fast.

An expert does not make a weak deal bankable. An expert keeps a bankable deal from breaking for preventable reasons.

That is what matters here. Buyers chasing a "buy a company with no money" story usually need tighter execution, cleaner documents, and a structure that fits SBA rules from the start.