You've found a business you want to buy. The seller says cash flow is solid. Your broker wants proof of funds. The bank asks for tax returns, a personal financial statement, projections, a resume, a debt schedule, and an explanation for every unusual line item. Then someone mentions SBA rules, lender overlays, standby seller notes, and debt service coverage.

That's when most first-time buyers realize the hard part isn't deciding to use SBA financing. The hard part is getting the deal structured, packaged, and presented in a way a real SBA lender will approve.

An SBA loan broker helps with that gap. Not just by introducing you to banks, but by shaping the transaction before it reaches underwriting. That matters because SBA lending is big, active, and competitive. In fiscal year 2024, the SBA approved about $56 billion in guaranteed loan volume across its core programs, and about 70,000 loans were approved in the 7(a) program alone, according to this SBA lending volume overview. There are many lenders in the market, but they don't all like the same deals.

Table of Contents

- Why You Need a Specialist for SBA Financing

- What an SBA Loan Broker Really Does

- The Borrower Journey with an SBA Broker

- SBA Broker vs Going Direct to a Bank

- Understanding SBA Loan Broker Fees

- How to Choose the Right SBA Loan Broker

- Frequently Asked Questions About SBA Brokers

Why You Need a Specialist for SBA Financing

SBA financing looks simple from a distance. The government guarantees part of the loan, so buyers assume the process is standardized. It isn't.

The SBA sets the framework, but the money comes from lenders. Each lender still has its own credit appetite, industry preferences, documentation habits, and tolerance for deal complexity. One bank may like a service business with recurring revenue. Another may prefer collateral-heavy deals. A third may avoid first-time buyers unless the operating history is unusually clean.

That's why a specialist matters. A good SBA loan broker doesn't just ask whether your deal is “bankable.” They ask which bank is most likely to like your exact file, and what needs to change before submission.

A weak SBA deal often isn't dead. It's just being shown to the wrong lender, in the wrong format, with the wrong narrative.

For business buyers, that difference is expensive. A poor first submission can waste weeks, trigger avoidable underwriting questions, and weaken your bargaining position with the seller. A strong first submission can tighten the story from day one.

A specialist is especially useful if you're buying a business for the first time, using a seller note, needing working capital in the total project cost, or trying to understand whether 7(a), 504, or another SBA path fits the transaction. If you're still learning the basics of acquisition financing, this guide to an SBA loan to buy a business is a helpful companion.

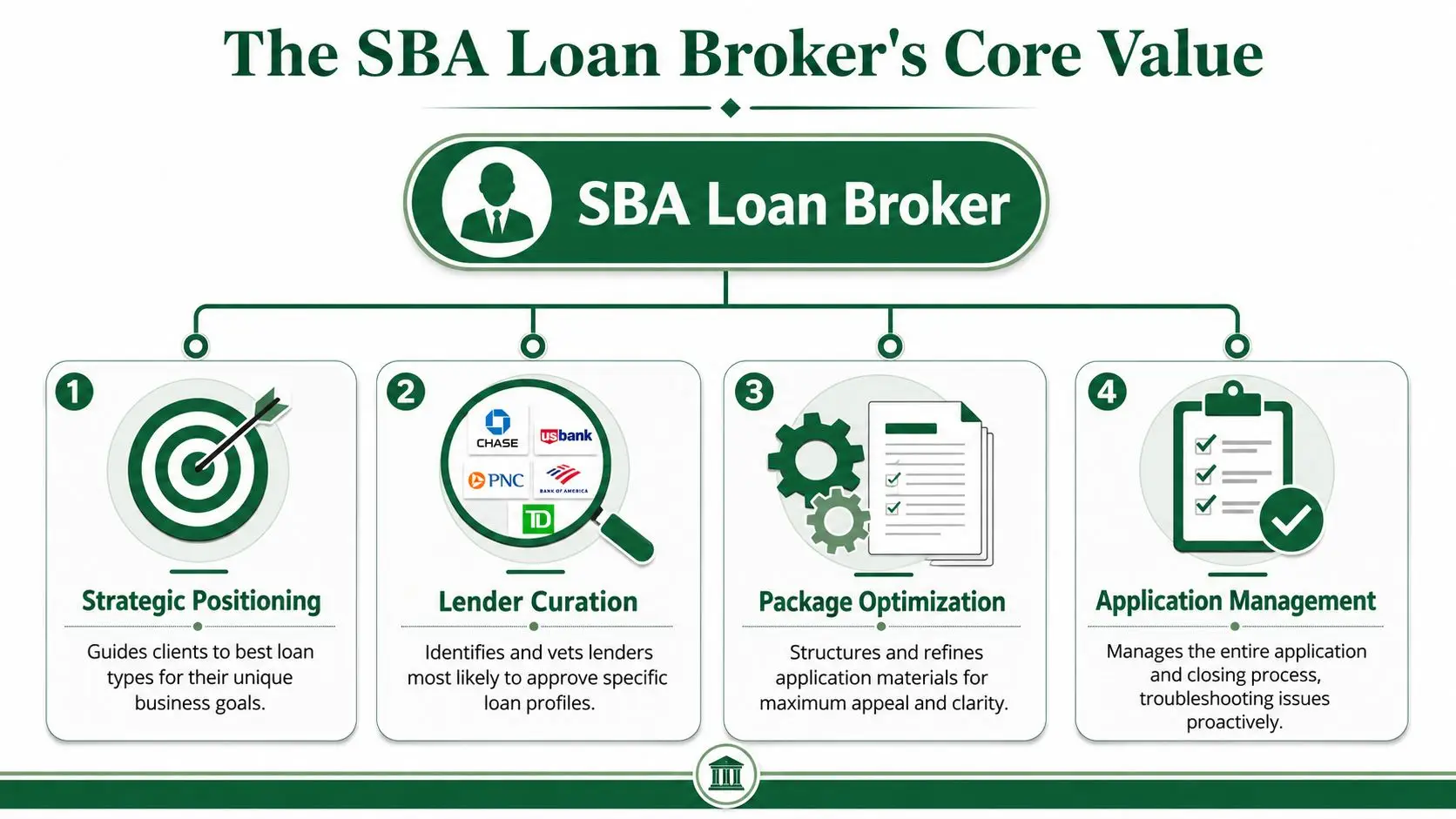

What an SBA Loan Broker Really Does

A real SBA loan broker influences approval odds long before any file reaches a bank. The work is part credit strategy, part deal structuring, and part process control. For a first-time buyer, that usually matters more than merely getting introduced to a lender.

The broker's job starts with reading the transaction the way an SBA underwriter and credit officer will read it. That means finding weaknesses early, before they become decline reasons or expensive delays. In practice, the broker is shaping how the deal will be viewed under SBA SOP rules and under a specific lender's own credit preferences.

They shape the deal before it goes out

The first job is strategic positioning. A good broker pressure-tests the structure, not just the borrower.

That includes questions like:

- Does normalized cash flow support the proposed payment, or are the add-backs too aggressive?

- Does the buyer's background fit the business, especially if this is a first acquisition?

- Is the equity injection documented correctly, with a clean paper trail for sourced funds?

- Is the seller note written in a way the lender can credit properly, especially if it affects required equity?

- Do the uses of proceeds match SBA rules and lender expectations, including working capital, closing costs, and any standby requirements?

These details change outcomes. I have seen otherwise solid acquisitions stall because the projection was too optimistic, the seller note was documented incorrectly, or the buyer's experience was not explained in a way credit could get comfortable with.

They package the deal for the right lender

The second job is lender selection with intent. That is different from shopping the file around.

A disciplined broker narrows the list based on deal size, industry, collateral position, buyer experience, turnaround speed, and how a lender handles issues like partial standby seller notes or limited post-close liquidity. For borrowers weighing their options, this breakdown of a business loan broker vs direct lender helps clarify where that value shows up.

Then the broker builds the credit package to answer obvious questions before underwriting asks them. That package usually includes a borrower narrative, sources and uses, business financials, interim statements, debt schedule, buyer financial statement, tax returns, and projections tied to a real operating story.

A weak package creates avoidable friction. A strong one gives the lender a clear path to yes.

Practical rule: If an underwriter has to guess how the business covers debt service, where the injection came from, or why the buyer can run the company, the file is not ready.

They manage the file like a live transaction

The third job is execution. During this stage, many deals wobble.

Once the application is in, the file has to stay consistent across term sheets, underwriting, SBA review, and closing. Small errors cause real delays. Ownership percentages do not match between documents. Bank statements expire. Lease terms conflict with loan maturity. Insurance language is wrong. Third-party reports come in late. A broker keeps those items from turning into a two-week delay that puts the purchase agreement under pressure.

Strong brokers also help tighten projections and supporting materials when the business is financeable but the presentation is weak. That is insider work. The value is not just access to lenders. The value is knowing how lenders read SBA files, what they worry about first, and how to structure the deal so it survives credit scrutiny.

The Borrower Journey with an SBA Broker

The SBA process feels less intimidating when you see it as a sequence instead of a mystery. Most transactions move through the same broad stages. The borrower provides the facts and core documents. The broker turns those materials into a financeable file and keeps the process controlled as new questions appear.

A visual overview helps before you get into the details.

Phase one strategy and package build

The first conversation should be blunt. What are you buying, what do the financials look like, how much cash are you bringing, what experience do you have, and what problems already exist in the deal?

From there, the broker starts assembling the lender package. For a 7(a) acquisition or working-capital transaction, the SBA program can finance up to $5 million, with terms of up to 10 years for most uses and up to 25 years when real estate is involved, according to the SBA lender program overview. The SBA also notes that lender interest rates are negotiated subject to SBA maximums, which is why lender selection affects total borrowing cost.

Your job in this phase is simple, but not easy. Produce complete documents. That usually means tax returns, personal financial statement, resume, debt schedule, business financials, purchase terms, and bank statements. Incomplete submissions are one of the fastest ways to slow the process down.

The broker's job is to turn those materials into a file that reads cleanly. That often includes tightening the projections, clarifying add-backs, and making sure your narrative matches the numbers. If your bookkeeping is messy, fix that before underwriting starts. Clean records matter, and these accounting and bookkeeping insights are a useful reminder of how quickly poor documentation can become a lending problem.

Phase two lender fit and term sheet strategy

Once the file is solid, the broker narrows the lender list. This is not random shopping. A thoughtful submission plan matters.

One lender may move faster on change-of-ownership deals. Another may be stronger on partner buyouts. Another may be cautious about customer concentration or a short lease term. The broker's value is in knowing where your file has the highest probability of landing well.

What you should expect at this stage:

- A clear lender thesis. Why these lenders, and why now.

- A realistic discussion of terms. Not every term sheet will look the same.

- A candid risk review. If there's a weak point, it should be identified before formal underwriting.

- A plan for seller communication. Loan timing has to match the purchase timeline.

Later in the process, this short explainer is worth watching if you want a practical look at how SBA loan execution works in practice.

Phase three underwriting and closing control

After a lender issues interest, the substantive work begins. Underwriting will ask follow-up questions. They'll want explanations, revised schedules, updated statements, and third-party items. Some requests are routine. Some reveal that the lender didn't fully understand the file on the first pass.

A broker earns their keep by filtering noise, framing responses properly, and keeping every party aligned, including the buyer, seller, lender, insurance contact, landlord, and closing professionals.

Most SBA closings don't fail because of one dramatic issue. They drift off course because small issues sit unresolved for too long.

By closing, the borrower should understand exactly what is being funded, what conditions remain, and what cash is due. If any of that feels unclear near the finish line, the process hasn't been managed tightly enough.

SBA Broker vs Going Direct to a Bank

Going direct can work. Using a broker can work too. The right path depends on the deal, the borrower, and whether you already have a bank relationship that fits the transaction.

The practical difference is this. Going direct means you're betting on one lender's appetite and one banker's interpretation of your file. Using a broker gives you broader market feedback and usually stronger deal framing.

For many borrowers, the cash requirement is where the difference becomes visible. In SBA financing, down payments can be as low as 10%, and in 504 projects a private lender can provide a senior lien covering up to 50% of project cost, as outlined in this SBA financing overview for commercial real estate brokers. Structure matters because small changes in equity, standby debt, or project composition can affect both approval odds and cash needed at closing.

Where a direct bank approach works

If you already have a strong relationship with an active SBA lender, going direct can be efficient. That's especially true when:

- Your deal is straightforward and doesn't need much structuring.

- Your financials are clean and easy to underwrite.

- The bank already knows you as a depositor or borrower.

- The banker has real SBA experience, not just general commercial lending experience.

That said, many borrowers assume their local bank “does SBA” when what they really mean is the bank has done some SBA deals before. That's not always enough for an acquisition file with complexity.

Where a broker usually adds leverage

A broker tends to add the most value when the deal needs positioning, when lender fit is uncertain, or when timing matters.

| Factor | Using an SBA Loan Broker | Going Direct to a Bank |

|---|---|---|

| Lender options | Access to multiple SBA lenders with different credit preferences | Usually one institution and one credit box |

| Deal structuring | Helps shape equity, seller note treatment, projections, and package presentation | Advice depends on that bank's appetite and banker experience |

| Term competitiveness | Can compare offers and execution styles across lenders | Limited to one lender's proposal |

| Time and effort | Broker coordinates submissions and follow-ups | Borrower manages more of the process directly |

| Approval certainty | Better when the file needs matching to the right lender | Better when the bank is already an obvious fit |

| Cost visibility | Borrower should ask exactly how the broker is compensated | Simpler relationship, but no market comparison |

If you're weighing both models, this comparison of a business loan broker vs direct lender gives a useful decision framework.

Understanding SBA Loan Broker Fees

The first question many borrowers ask is the right one. How does the broker get paid?

In many SBA brokerage relationships, the model is lender-paid at closing, similar to how a specialized recruiter operates. The candidate doesn't pay the recruiter to get introduced to the employer. The employer pays for a successful placement. In lending, that often means the lender pays the broker if the transaction closes.

How the model usually works

That arrangement can be efficient for borrowers because it removes an upfront advisory bill in many cases. But don't stop at “it's lender-paid.” Ask for the actual explanation in plain English.

You want to know:

- Who pays the fee

- When it's paid

- Whether the borrower owes anything separately

- Whether the broker works with multiple lenders or only a narrow group

- Whether all offers will be shown to you

A credible broker should answer those questions directly, without hedging.

How to judge alignment

The main concern is bias. If the lender pays the broker, will the broker steer you toward the lender that pays more rather than the lender that fits best?

That's a fair question. The practical safeguard is process. A good broker creates competition, explains the trade-offs among offers, and lets the borrower choose. If a broker won't explain compensation or won't show multiple options when the file clearly supports them, be cautious.

Ask less about whether a broker charges a fee and more about whether their process gives you real lender choice.

If you want the rule framework around this topic, review these SBA broker and agent fee rules.

How to Choose the Right SBA Loan Broker

Not every broker is built for acquisition lending. Some are good at small working-capital requests. Some are general commercial finance intermediaries who occasionally touch SBA. Those aren't the same thing.

If you're buying a business, you need someone who understands cash flow acquisitions, seller notes, buyer experience narratives, and the difference between a file that is merely complete and a file that is financeable.

What to screen for first

Start with a practical checklist.

- Acquisition experience. Ask whether they regularly handle change-of-ownership deals, not just equipment or working capital.

- Program fluency. They should be able to explain when 7(a), 504, or a smaller-dollar alternative fits.

- Lender depth. You want a broker with a real lender network, not one or two favorite outlets.

- Packaging ability. If they can't explain how they handle projections, add-backs, and memo writing, they may only be forwarding documents.

- Underwriting discipline. Listen for SOP familiarity and credit logic, not sales language.

- Communication style. If they're vague in the first call, they'll probably be vague when the lender starts asking hard questions.

A good broker also knows when to say no. That's a positive sign. If every deal sounds “easy” to them, you're probably hearing a pitch, not analysis.

Questions worth asking in the first call

These questions cut through marketing fast.

What kinds of SBA deals do you handle most often?

A strong answer is specific. They should mention business acquisitions, partner buyouts, owner-occupied real estate, or another clear lane. A weak answer stays broad.How do you decide which lenders see my file?

You want to hear about fit, credit appetite, and deal profile. You don't want to hear “we send it everywhere.”What usually causes SBA acquisition files to stall?

Good answers mention documentation gaps, weak projections, unresolved seller-note issues, lease problems, or inconsistent financials.Who helps prepare the package?

If they rely entirely on you to organize and explain everything, that's a warning sign.How do you handle underwriting questions once the file is submitted?

A strong broker acts as quarterback. A weak one just forwards emails.How are you compensated, and will I see all lender options?

The answer should be immediate and clear.When would you tell a borrower not to use a broker?

This is an underrated question. Honest brokers can describe situations where a direct bank relationship may be the better path.

The best interviews feel less like a sales call and more like a credit discussion. That's what you want.

Frequently Asked Questions About SBA Brokers

Can a broker help if my credit is borderline

Sometimes, yes. But a broker can't turn a weak file into a strong one by force of personality.

What they can do is identify whether the underlying issue is credit, liquidity, experience, documentation, or deal structure. Borderline borrowers often get declined for the reason the lender writes down, but the actual problem may be somewhere else in the package. A good broker will tell you which issue is fixable and which one isn't.

What if my deal is very small

Small deals can still be financeable, but not every small deal belongs in a standard 7(a) search. For very small requests, SBA Microloans are capped at $50,000 and are delivered through intermediaries, while mission-oriented lending channels have been used to reach underserved borrowers, as described in this discussion of Microloans and Community Advantage-style access.

That matters because some borrowers need a different path, not a smaller version of the same one. A capable broker should tell you when a mission lender, microloan intermediary, or other smaller-dollar route is the better fit.

Is my information secure with a broker

It should be, but you should ask. Your file will likely include tax returns, bank statements, ownership documents, and personal financial data. Ask how documents are collected, stored, shared with lenders, and removed when no longer needed.

If the answer is casual, move on.

What's the difference between a broker and a loan packager

A loan packager usually focuses on assembling documents and preparing the submission file. An SBA loan broker typically does more. That often includes lender selection, term sheet comparison, underwriting support, and closing coordination.

Some firms do both under one roof. The key question isn't the label. It's whether they only prepare paperwork or actively guide execution from strategy through funding.

If you're buying a business, refinancing debt, or financing owner-occupied real estate, GoSBA Loans is one option to consider for SBA brokerage support. Review whether its lender network, packaging help, and process fit your deal, then compare that against other advisors or a direct-bank approach before you decide.