Most advice about using an SBA loan to buy a business is too shallow to help you close.

It usually sounds like this: get prequalified, gather documents, put down money, wait for approval. That's not wrong. It's just incomplete. Buyers lose deals because they treat SBA financing like a paperwork exercise when it's really a risk presentation to a bank that has to believe two things at once: the business will support the debt, and you will run it well after the seller leaves.

That distinction matters more than any online checklist. The SBA rules create the frame, but lenders still decide how comfortable they are with your deal, your background, your liquidity, and your structure. A buyer with average credentials and a well-built file often gets farther than a strong buyer with a sloppy package. A clean narrative beats a pile of PDFs.

I've found that the strongest acquisition borrowers think like operators and underwriters at the same time. They don't just ask, “Can I qualify?” They ask, “Where will the lender hesitate, and how do I answer that before credit asks?” That's the mindset that gets deals funded.

If you're still sorting through the broader legal and practical issues around borrowing, this short guide on advice for business loans is a useful companion because it frames borrowing as a decision with legal and structural consequences, not just a rate quote.

Table of Contents

- Beyond the Paperwork An Introduction to Strategic SBA Financing

- Choosing the Right SBA Loan for Your Acquisition

- Decoding SBA Eligibility and Underwriting Criteria

- Your Equity Injection Strategy Down Payment and Collateral

- Mastering the Deal Structure Seller Notes and Investor Stacks

- Navigating the Timeline and Common Acquisition Pitfalls

- The Complete SBA Acquisition Document Checklist

- Your Next Steps to Secure Funding

Beyond the Paperwork An Introduction to Strategic SBA Financing

Buyers lose SBA acquisition deals for reasons that never appear on the checklist.

On paper, the 7(a) program is flexible enough to finance a business purchase, certain debt refinance, real estate improvements, and working capital, with loan sizes that can support many lower middle-market acquisitions, as noted earlier. In practice, flexibility is not what gets a deal approved. Lender confidence does.

After more than 100 acquisition financings, the pattern is clear. The borrowers who get to closing fastest present the file the way a credit officer reads it, not the way an applicant fills it out. They understand that underwriting is less about submitting forms and more about removing reasons for hesitation.

The lender's practical approval test

A lender is usually trying to answer four questions well before legal documents are final:

- Will cash flow hold after the seller leaves? Recurring customers, depth in management, and clean financial reporting matter more than a polished narrative.

- Does the buyer fit this specific business? Direct industry experience helps, but lenders also fund buyers with adjacent operating backgrounds if the transfer story is credible.

- Does the structure create stability after closing? Good deals leave room for normal mistakes, seasonality, and a slower-than-expected handoff.

- Can the bank trust the file? If tax returns, P&Ls, add-backs, and the purchase agreement tell slightly different stories, credit starts assuming the worst.

This is the part many buyers miss. Banks do not fund effort. They fund clarity.

A buyer can have a strong resume and still lose momentum fast if the file shows weak judgment. Common examples include aggressive add-backs with no support, financial statements that do not tie to tax returns, unexplained revenue dips, or a letter of intent built around terms the lender will not accept. Once doubt enters the file, the bank slows down, asks for more conditions, or starts pushing for a lower loan amount.

Good borrowers anticipate those questions before the first underwriter call. They explain customer concentration before it is flagged. They address margin compression before anyone asks. They show why the transition plan is realistic, why the business can service debt in an average month, and why the post-close cash position will not be too thin. That is the unwritten part of SBA acquisition lending.

For buyers trying to sharpen their package before talking to lenders, this outside advice for business loans is directionally useful. The lender-side standard is tougher. The file has to make credit comfortable enough to defend the deal internally.

Strategic SBA financing means presenting a transaction the way a bank wants to approve it. Clean story, credible assumptions, and no loose ends that force the lender to solve the deal for you.

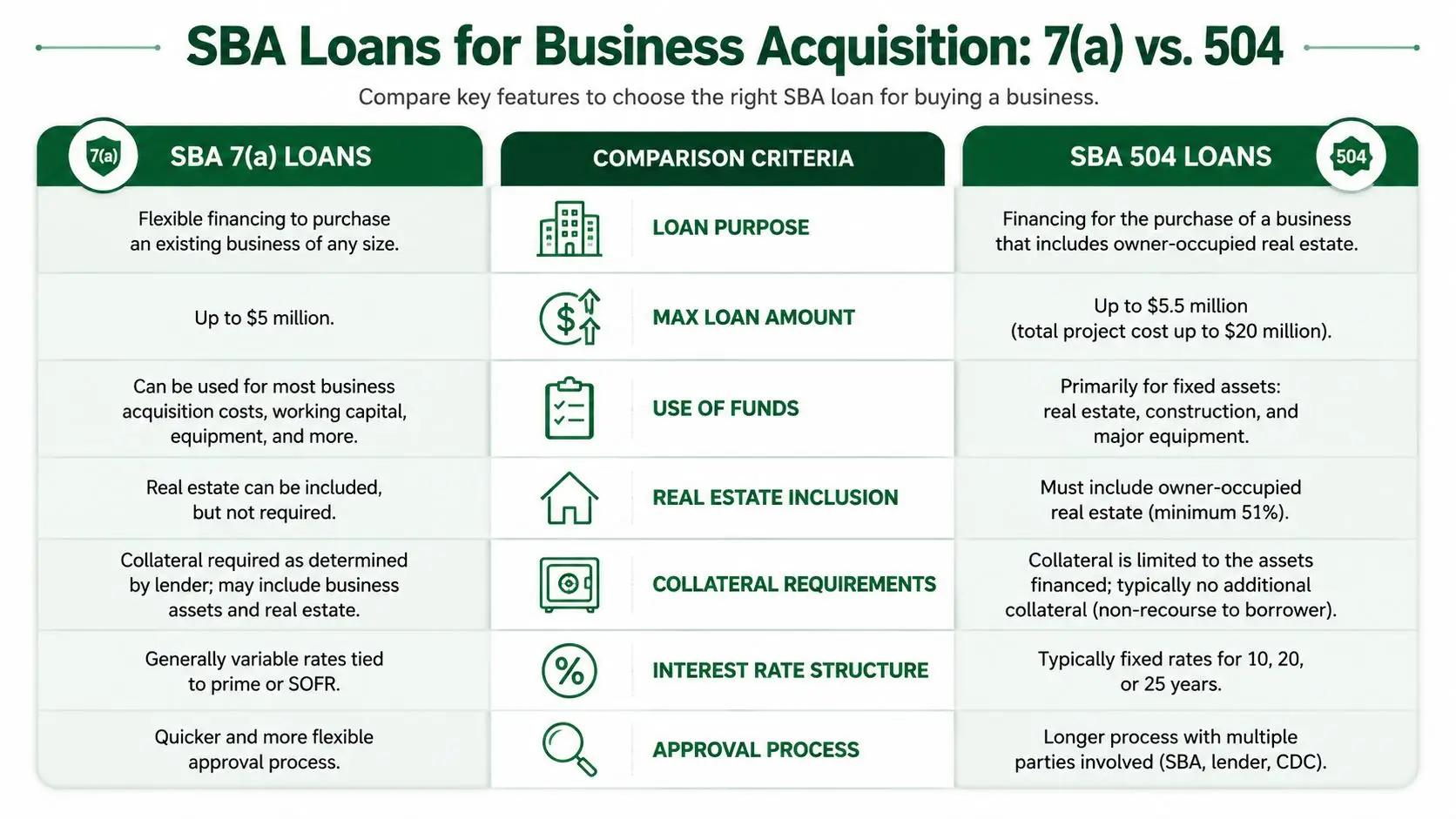

Choosing the Right SBA Loan for Your Acquisition

Buyers spend too much time comparing SBA products like they are shopping for rates. That is not how acquisition lenders look at it. The core question is simpler: which structure gives credit the cleanest path to approve your specific deal with the fewest post-approval surprises?

For most business purchases, that answer is 7(a). In actual lending conversations, 504 only becomes the lead option when the building or heavy equipment is doing a large share of the collateral and economic work. If the business value sits mostly in recurring customers, contracts, workforce, brand, and cash flow, lenders usually steer back to 7(a) fast.

Where 7(a) usually wins

A 7(a) acquisition loan is built for operating businesses. That matters because most lower middle market deals are not asset purchases in the practical credit sense. They are cash flow purchases with some furniture, fixtures, equipment, and maybe receivables around the edges.

That distinction changes everything. A bank can use 7(a) to finance goodwill, support a change of ownership, include working capital, and sometimes clean up debt that makes the transition harder. Those are the parts of the deal that often decide whether the business stays stable in the first six months after closing.

In lender committee, these are the transaction types that usually fit 7(a) best:

| Acquisition type | Why 7(a) often fits better |

|---|---|

| Service business | Enterprise value is often tied to cash flow, not hard assets |

| Existing business with working capital needs | Proceeds can support operations after closing |

| Seller transition-dependent deal | Underwriting can focus on earnings continuity and handoff plan |

| Purchase that includes debt refinance | The structure is usually more flexible |

There is also a practical lender point buyers miss. The SBA guaranty improves a bank's willingness to take acquisition risk, but it does not make a weak deal financeable. I have seen lenders approve a service business with light collateral and strong normalized cash flow under 7(a), then decline a real-estate-heavy deal because the tenant mix, environmental file, or occupancy issue made the transaction harder to defend.

Personal recourse also matters more than many first-time buyers expect. If you are signing an SBA acquisition loan, assume the bank will require full borrower support and make sure you understand the personal guarantee definition before you negotiate final terms.

Later in the process, it helps to hear a lender explain the broad shape of the product. This short video gives a useful overview.

Where 504 becomes the better tool

504 works best when the property involved is carrying a major part of the transaction. That usually means an owner-occupied building, significant fixed assets, or both.

In those cases, 504 can preserve buyer liquidity and spread the capital stack in a way some borrowers find attractive. The trade-off is narrower use of proceeds, more real-estate-driven diligence, and less room for the messy parts of an acquisition that show up in actual deals. Appraisals, environmental reports, occupancy rules, and project structure can all slow a closing.

That is why 504 is often better for a company buying its facility, or for an acquisition where the property is central and the operating business is straightforward. It is usually a poor fit for deals with large goodwill, meaningful transition risk, or a need to finance post-close working capital.

A blunt rule I use with buyers is this: use 504 when the building is one of the main reasons the deal works. Use 7(a) when the business itself is the reason the deal works.

How buyers should decide

Start with what the lender has to underwrite, not what sounds cheaper on a term sheet.

Ask four practical questions:

- Is most of the purchase price tied to earnings and goodwill? That usually points to 7(a).

- Is real estate a major part of the collateral and deal value? 504 deserves a serious look.

- Do you need working capital included so the business is not cash-starved on day one? 7(a) is usually the better tool.

- Will property reports, appraisal issues, or occupancy questions create closing risk? If yes, price that delay into your decision early.

The unwritten rule is that simpler stories get funded faster. Buyers who match the SBA product to the true driver of value in the acquisition give the lender fewer reasons to hesitate.

Decoding SBA Eligibility and Underwriting Criteria

Eligibility is the easy part. Underwriting is where acquisition loans get approved, restructured, or declined.

Buyers spend too much time on SBA checklists and not enough time on the questions a credit officer has to answer internally: Will this business service the debt after the handoff, does the borrower look capable of running it, and is there enough margin for error if the first six months are uneven? Those are the unwritten rules. A file that answers them cleanly moves. A file that does not gets stuck in credit, even when it checks every box on paper.

Cash flow gets the first real vote

In acquisition lending, cash flow coverage drives the conversation. Lenders still review credit, collateral, and global cash flow, but the core issue is simple: can the business make the proposed payment and still absorb a normal amount of post-close disruption?

A weak file usually falls apart in one of three places:

- Aggressive add-backs: If the earnings story depends on owner perks, one-time expenses, and optimistic savings all stacked together, underwriters start discounting the whole model.

- Unexplained volatility: A soft quarter is not fatal. A soft quarter with no explanation, no customer detail, and no recovery pattern is.

- Thin post-close coverage: If debt service only works in the seller's hands and not the buyer's first year, the lender sees execution risk, not just math.

I have seen good businesses struggle in underwriting because the buyer treated recast earnings like a sales pitch. Credit teams do not underwrite the upside case. They underwrite the version of the deal that still works if revenue slips, margins compress, or a manager leaves right after closing.

Experience matters, but relevance matters more

Lenders do not require buyers to have owned the exact same type of company before. They do require a credible path from your background to this business.

That distinction matters. A corporate operator with P&L responsibility, hiring authority, and multi-site management experience can often get a deal through on a business they have not owned before. A buyer with a strong income and no operational track record will face a much harder review, especially if the target depends on sales management, technical knowledge, or owner relationships.

The strongest management story usually includes a few concrete facts:

- Transferable operating experience: managing teams, budgets, vendors, or service delivery at a similar scale

- A believable transition plan: seller support, retained managers, or a defined handoff for customer relationships

- Clear understanding of the business model: how the company gets customers, where margins come from, and what could go wrong after closing

Ambition does not carry a file. Competence does.

Liquidity is one of the quiet approval factors

A lender can live with a buyer who is not wealthy. A lender gets nervous when the buyer is putting every available dollar into the closing and has nothing left for payroll surprises, receivables delays, or equipment issues.

That is why post-close liquidity gets more attention than buyers expect. Underwriters want to see cash left after the injection, not just proof that the injection exists. If the business hits a rough patch in month two, the bank wants evidence that the borrower can support operations without missing payments or draining the company immediately.

This is also why guarantor analysis is so important. In almost every SBA acquisition, the owners will sign a personal guarantee. If you want a plain-English overview before reviewing loan documents, this guide to personal guarantee definition covers the basics.

What credit committees actually look for

The cleanest files make four points easy to defend:

| Underwriting concern | What lenders want to see |

|---|---|

| Cash flow | Conservative earnings adjustments and enough coverage after debt |

| Management | Relevant experience tied directly to the target's operating model |

| Liquidity | Cash reserves left after closing, not a buyer tapped out on day one |

| File quality | Clean disclosures, matching numbers, and no unresolved surprises |

Collateral still matters, but in goodwill-heavy acquisitions it rarely rescues a weak credit story. Character matters too. Undisclosed tax issues, inconsistent resumes, unexplained late payments, or sloppy financial packages create doubt fast.

One practical point gets missed all the time. The buyer who is easiest to approve is not always the buyer with the highest net worth. It is often the buyer whose deal structure, liquidity position, and operating background make the lender's memo easy to write. If you need a clearer view of how lenders evaluate cash down, standby notes, and buyer funds, this guide to SBA equity injection for acquisitions fills in the parts borrowers usually miss.

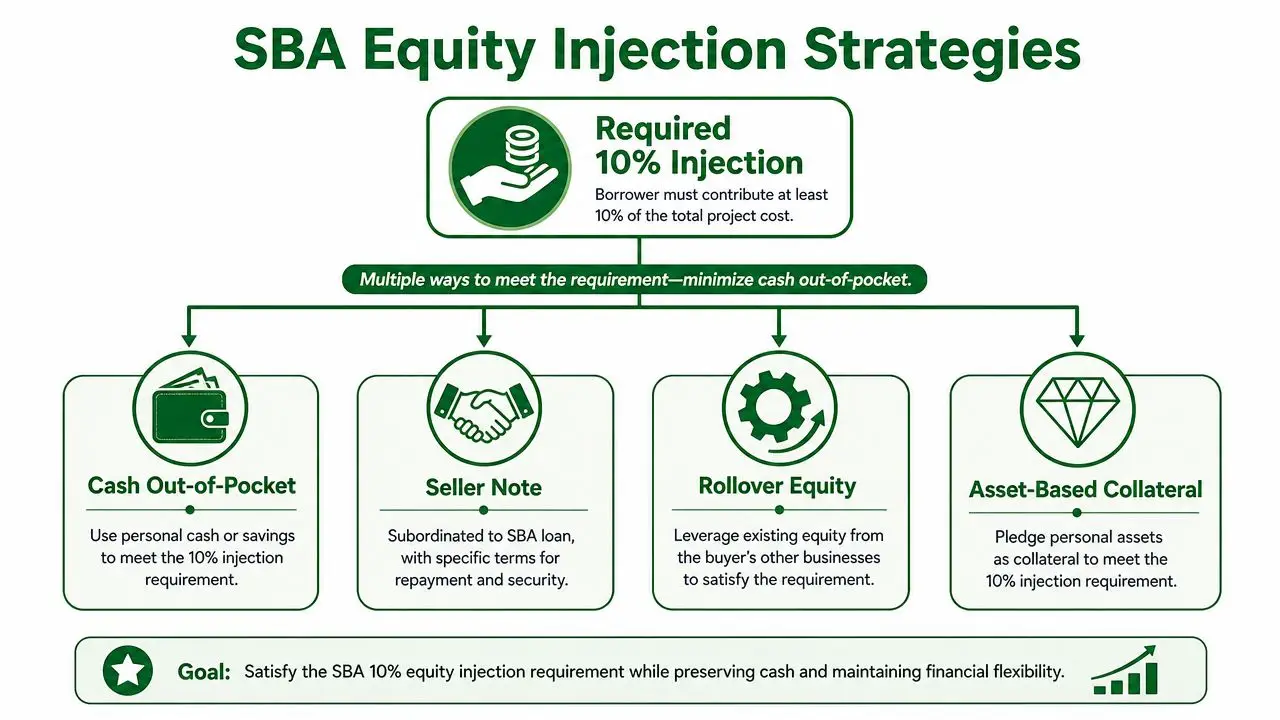

Your Equity Injection Strategy Down Payment and Collateral

Most buyers start with the wrong question. They ask how little cash they can bring. The better question is how to satisfy the lender's equity requirement without weakening the business on day one.

SBA acquisition rules require the buyer to inject at least 10% of the total project cost, and a seller note can count toward up to half of that required equity if it is on full standby for the life of the loan, which can enable a 5% cash down payment structure, according to this summary of SBA loan statistics and acquisition rules.

That rule creates flexibility, but only if the note is structured correctly.

How the equity injection really works

The cleanest acquisition files usually use one of three approaches:

- All cash injection: Simplest for underwriting. Least flexible for the buyer.

- Cash plus standby seller note: Most common way to reduce buyer cash outlay.

- Additional outside equity: Useful when the buyer wants more liquidity left after closing.

The standby point is where buyers and sellers often get confused. A seller note doesn't help your injection requirement just because it exists. It must be subordinated in a way the lender accepts. If the seller expects immediate principal payments, that note usually won't function as equity support.

A practical framework for thinking about it:

| Equity source | Helps satisfy injection | Typical underwriting reaction |

|---|---|---|

| Buyer cash | Yes | Best received |

| Seller note on full standby | Yes, within allowed limit | Helpful if documented correctly |

| Seller note with active repayment | Usually not for injection treatment | Creates more scrutiny |

| Unclear gift or borrowed down payment | Depends on structure and documentation | Often problematic |

For a deeper breakdown of acceptable structures, this guide on SBA equity injection for acquisitions is a useful reference.

Collateral is not the same as down payment

Buyers also confuse collateral with equity. They aren't the same thing.

Your down payment shows commitment and decreases the financial risk. Collateral gives the lender additional security if the deal fails. A bank may still look for liens on available business and personal assets even when the equity injection is fully satisfied.

That matters in practice because some buyers can fund the injection but still get surprised by collateral requirements. If business assets don't fully secure the loan, lenders often want available personal collateral information early. Waiting until late underwriting to discuss that issue creates unnecessary delays.

A cash-efficient structure is good. A cash-efficient structure that leaves you undercapitalized is not.

The best equity strategy isn't the one with the lowest check at closing. It's the one that gets approved and leaves enough room to run the company after the wire hits.

Mastering the Deal Structure Seller Notes and Investor Stacks

Simple deals are easier. That doesn't mean complex deals can't close.

Many acquisitions need more than buyer cash plus one SBA loan. Sellers want a price that maximizes the financing available. Buyers want to preserve liquidity. Sometimes outside investors are part of the picture. Sometimes another lender is involved. The trick is building a structure that still looks stable to the senior SBA lender.

What makes a structure lender-friendly

A good acquisition capital stack does three things well. It keeps senior debt service manageable, avoids conflicting repayment pressure right after closing, and makes each party's role obvious.

That's why seller notes can be helpful. They can bridge valuation gaps and show seller confidence in the business. But they only help if they don't overburden the company. A seller note with aggressive repayment can turn a workable deal into a thin one fast.

Investor money can also improve a deal, but only when it comes in cleanly. Lenders want to understand who owns what, who controls the borrower, and whether any investor rights create friction with SBA rules or with the operating authority of the primary guarantor.

Three structures tend to be more workable than buyers expect:

- Straight SBA senior debt plus buyer equity: Best for clean, ordinary transactions.

- SBA senior debt plus standby seller note: Good when the seller is motivated and underwriting needs cushion.

- SBA senior debt plus outside equity plus seller participation: Useful for larger or more competitive deals, if control and guarantees are clear.

Where investor equity helps and where it creates friction

Outside investors solve one problem and create another.

They can strengthen liquidity, alleviate debt burden, and make a buyer's personal balance sheet less of a limiting factor. But they also introduce governance questions. Who controls the operating entity? Who guarantees the debt? Who can force distributions? What happens if performance slips?

That's why “more capital” is not automatically “better structure.” Banks don't like ambiguity. If investors are passive and documentation is clean, the file is easier. If the cap table starts looking like negotiated politics, credit gets slower.

A few lender-minded principles matter here:

| Capital component | Helps the file when | Hurts the file when |

|---|---|---|

| Seller note | Terms support transition and cash flow | Repayment pressure starts too early |

| Investor equity | Control is clear and documents are simple | Ownership and authority are messy |

| Additional debt piece | Roles are coordinated and liens are understood | Priority disputes are unresolved |

Buyers looking at standby seller paper often benefit from reviewing the mechanics in this guide to SBA seller note rules and 5 percent down structures.

A practical way to think about complex stacks

Forget the jargon for a moment. Every layered acquisition structure has to answer the same lender question: after closing, who gets paid, in what order, and from what cash flow?

If that answer is simple, you have a chance. If it takes a whiteboard and three caveats, expect friction.

One issue buyers hear about in larger or more engineered transactions is a pari passu concept, where another institutional lender may share the senior lien position alongside the SBA lender in a coordinated structure. That can work in the right scenario, but it's not a default answer and it has to be built carefully. It's usually for deals where a plain vanilla capital stack doesn't solve the financing need.

The best complex deal still feels simple when explained to credit.

That's the test I'd use on every draft structure. If a senior underwriter can understand the ownership, repayment order, seller support, and operating control in a few minutes, the deal is probably built well enough to move.

Navigating the Timeline and Common Acquisition Pitfalls

The published SBA timeline often differs from the actual timeline.

What decides whether an acquisition closes in 45 days or drifts past 90 is rarely the bank alone. It is usually one of four things. The seller's financials are sloppy, the buyer is slow to answer underwriting questions, the legal documents do not match the approved structure, or a third-party report shows up late and forces everyone to wait.

What actually happens between LOI and funding

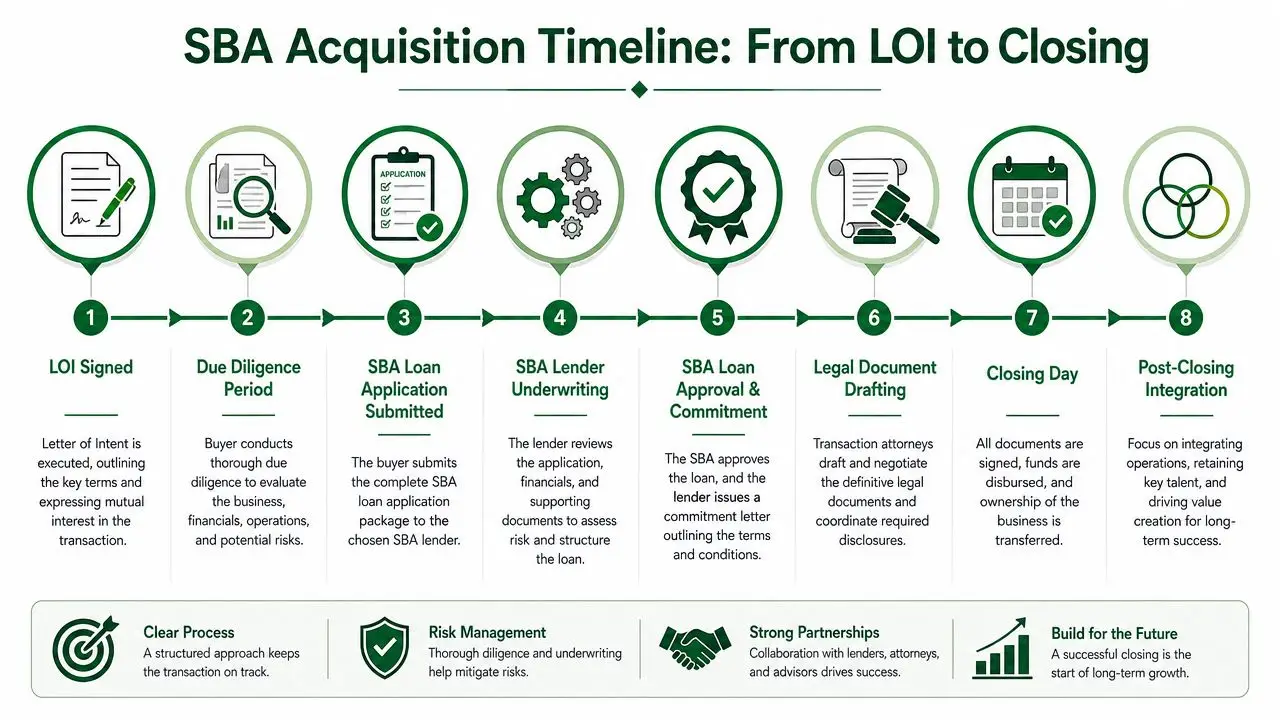

From a lender's seat, the clock starts at LOI because that is when the deal either gets organized or starts to unravel. A clean LOI with clear price, asset versus stock terms, training period, working capital expectations, and seller support can save weeks later. A vague LOI creates re-trades, credit questions, and legal revisions.

A typical file moves through these stages:

- LOI is signed. The buyer and seller set the basic economics and control terms.

- Prequalification review begins. The lender tests whether the borrower, target, and deal structure fit credit standards.

- The full file is submitted. Tax returns, interim financials, buyer financials, background information, and the draft purchase agreement start the substantive underwriting process.

- Underwriting starts asking harder questions. Expect focus on cash flow durability, add-backs, customer concentration, industry risk, and post-close liquidity.

- Third-party reports are ordered. Valuation, lease review, environmental work, or franchise review often become the pacing item.

- Loan approval is issued with conditions. Approval is not the finish line. It is a list of items that still must be satisfied.

- Legal documents are drafted and matched to credit approval. Small inconsistencies here can stall closing.

- Final conditions are cleared and funds are disbursed. Insurance, entity documents, landlord consent, life insurance if required, and source of equity are common last-mile items.

The unwritten rule is simple. Credit can live with a tough deal faster than it can live with a confusing one.

I have seen strong businesses delayed for three weeks because the buyer changed entity ownership after approval and did not tell the lender until counsel started drafting documents. I have also seen average deals close on time because the buyer got every diligence item in quickly, answered questions the same day, and kept the seller focused.

Where acquisitions actually get stuck

Buyers often assume underwriting is the hard part. It often is not. The bigger problem is file drift. The facts keep changing while the lender is trying to approve a fixed transaction.

Common delay points include:

- Messy financials: Interim statements do not tie to tax returns, or the seller has too many personal expenses buried in the P&L.

- Weak response times: Underwriters send a list on Monday and get partial answers the following week.

- Lease and landlord issues: Assignment terms, renewal options, or landlord consent come in late.

- Valuation gaps: The agreed purchase price is above what the independent valuation supports.

- Legal mismatch: The purchase agreement, note terms, and loan approval do not say the same thing.

- Ownership changes: Investors, spouses, or partners are added late and trigger new review.

Lenders do not like surprises after approval. Every surprise creates one more round of review, and every round costs time.

The costs buyers miss

The most common budgeting mistake is treating the down payment as the full cash requirement.

In practice, buyers also need money for legal work, lender fees, third-party reports, insurance, deposits, and operating liquidity after closing. On a lower middle market deal, it is common for transaction costs and required cash reserves to feel manageable at LOI and much tighter a week before funding.

Post-close liquidity matters more than many buyers expect. The first payroll hits fast. Receivables can slow during ownership transition. A seller may have managed inventory tightly before closing, leaving the buyer to refill stock in month one.

The buyers who close cleanly usually keep a real cushion, not just enough cash to satisfy the formal injection requirement.

For a practical breakdown of what each stage usually looks like, review the complete SBA business acquisition timeline from LOI to closing.

When SBA is the wrong tool

SBA financing is strong, but it is not automatically the best fit.

Some transactions should not go through an SBA process at all. If the seller needs a very fast close, if ownership is unusually complex, if the target has a regulatory or licensing issue that will take time to resolve, or if the buyer cannot document income and liquidity cleanly, another financing path may make more sense.

These situations often fit better elsewhere:

- Seller-financed deals: Useful when speed matters and the seller is willing to carry meaningful risk.

- Conventional bank debt: Better for strong borrowers buying strong companies who want fewer program restrictions.

- Investor-led structures: Better when the cap table is too layered or negotiated control rights do not fit SBA rules.

The lender-side question is not whether SBA can be forced onto the deal. It is whether the transaction still looks bankable after world delays, document requests, and closing conditions show up. That is the standard that gets deals funded.

The Complete SBA Acquisition Document Checklist

A lender does not fund a pile of PDFs. A lender funds a story that holds up under stress.

That is the unwritten rule behind every SBA acquisition file. The checklist matters, but approval usually turns on whether the documents line up cleanly enough for an underwriter and credit officer to believe two things. The business can service the debt after the ownership change. The buyer can run it without creating new risk in the first six to twelve months.

That standard is stricter than the public checklist suggests.

Documents that explain the business

The business file has to do more than show revenue and profit. It has to show consistency.

These are the documents lenders usually study first:

- Business tax returns: Underwriters compare filed returns to the earnings being presented in the deal. If add-backs are aggressive or the seller's books do not match the returns, expect pushback.

- Year-to-date interim financials: Current profit and loss statements, balance sheets, and debt schedules show whether the business is still performing near the level used to support debt service.

- Purchase agreement or asset purchase agreement: This tells the lender what is being acquired, how the purchase price is allocated, what liabilities stay behind, and whether the terms create closing risk.

- Business plan or transition memo: This helps explain customer retention, management transition, hiring plans, and any expected changes after closing.

The common failure point is not missing paperwork. It is contradiction.

If the tax returns support one level of cash flow, the interim statements show a slowdown, and the buyer memo assumes quick growth after closing, the lender has a problem. In practice, that usually leads to more conditions, a lower loan amount, or a pass.

Documents that explain the buyer

Acquisition lending is still character and capacity lending. A buyer with clean personal finances and relevant operating experience will get more credit for a thin deal than a buyer with a strong target and a weak personal file.

The core personal documents are familiar, but lenders read them more closely than many buyers expect:

| Document | What the lender is looking for |

|---|---|

| Personal tax returns | Stable income, clean reporting, and no unexplained swings |

| Personal financial statement | Post-close liquidity, contingent liabilities, outside debts, and asset quality |

| Resume | Management experience that fits the target business |

| Purchase document | Clear ownership percentages and buyer obligations at closing |

The personal financial statement gets heavy scrutiny. I have seen deals slow down over a retirement account the borrower could not access, a rental property with hidden debt service, or a large “other asset” with no backup. Liquidity on paper is not the same as usable cash at closing.

Send final versions whenever possible. Drafts with open edits, inconsistent numbers, or unsigned terms create extra review rounds and invite new lender conditions.

Third-party items that delay funding

Third-party reports are where clean deals start to slip.

A valuation often becomes necessary when goodwill makes up a large part of the purchase price. Real estate deals can trigger environmental work. Legal documents, landlord consents, franchise approvals, license transfers, and corporate records also stall more closings than buyers expect.

The usual problem areas are:

- Valuation timing: If the agreed price is ahead of trailing cash flow, the valuation gets more attention and may not support the number in the LOI.

- Environmental reports: Real estate, auto-related businesses, manufacturing, dry cleaning, and certain older properties draw more scrutiny.

- Entity and legal documents: Articles, operating agreements, stock ledgers, leases, and consent requirements often arrive late or contain terms the lender cannot accept.

- Licensing and transfer approvals: Healthcare, contracting, transportation, and franchise deals often need approvals that run on their own timeline.

Experienced buyers do not wait for the lender to ask for every one of these items. They identify them early and assign responsibility. Seller gets this. Buyer gets that. Attorney handles the rest. That simple discipline can save weeks.

A strong SBA acquisition package reads like one file prepared by one person, even though five or six parties usually touched it. Numbers match across returns, financials, and the purchase agreement. Explanations are short and specific. Open issues are identified early instead of surfacing three days before closing.

That is what gets a deal through underwriting without unnecessary friction.

Your Next Steps to Secure Funding

A successful SBA loan to buy a business comes down to fit, structure, and preparation. The right target business matters. So does the way you present the deal, support the cash flow, explain your background, and preserve liquidity after closing.

If you're serious about getting funded, start by pressure-testing the deal before you submit it. Look at the lender's likely objections first. Tighten the structure, clean up the documents, and treat underwriting like a negotiation over risk, not an upload portal.

If you want experienced help structuring and placing an acquisition loan, GoSBA Loans helps buyers compare lenders, shape workable capital stacks, and move from LOI to closing with fewer surprises.