You've found a business that makes sense on paper. The seller has decent books, the broker says there's buyer interest, and you can already see how you'd run it. Then financing enters the picture and the deal suddenly feels less like an acquisition and more like an obstacle course.

That's the point where most first-time buyers make the same mistake. They focus on finding a loan product instead of building a file that a lender wants to approve. Those are not the same thing. A loan to buy a business is less about filling out an application and more about proving that the buyer, the business, and the structure work together.

I've seen good deals stall because the buyer was underprepared, overconfident, or relying on a lender to “figure it out.” Lenders don't do that. They reward clean narratives, documented cash, realistic transition plans, and legal documents that don't create new problems. That's also why smart buyers often get legal review early, especially for purchase terms, operating structure, and post-close obligations. If you need that kind of support, this overview of proactive counsel for companies is a useful place to start.

Table of Contents

- Your Blueprint for Financing a Business Purchase

- Decoding Your Loan Options for Business Acquisition

- Building Your Bulletproof Loan Application Package

- Meeting Lender Eligibility and Credit Requirements

- Navigating Lender Selection and Negotiation Strategy

- From Term Sheet to Closing Wires Your Timeline

Your Blueprint for Financing a Business Purchase

A strong acquisition file starts before the loan application. It starts when you decide whether the business is financeable at all.

Lenders don't fund excitement. They fund a transfer of ownership that looks stable after the seller leaves. That means they're asking questions a buyer often avoids early on. Does the business still work without the current owner? Are the financials organized enough to support underwriting? Is the purchase price grounded in reality? Can the buyer explain why they are the right operator for this exact business?

The deal has to work on paper and in practice

First-time buyers often assume the hard part is finding the right bank. Usually, the harder part is presenting a deal that survives scrutiny from credit, underwriting, closing, and counsel.

A practical file usually includes:

- A clear transaction story: Why this business, why now, and why you're capable of operating it.

- A supportable structure: Purchase price, down payment, seller note if applicable, and enough working capital to avoid a stressed first quarter.

- A transition plan: Training, customer handoff, employee continuity, and who handles the business on day one after closing.

- A disciplined buyer profile: Clean personal financial information, documented liquidity, and no confusion about where the injection is coming from.

Practical rule: If a lender has to guess what happens after closing, the deal gets weaker fast.

Fundability is a packaging issue

A lot of buyers are closer to approval than they think. Their problem isn't eligibility. Their problem is presentation.

The best loan packages remove friction. They don't bury weak spots, but they do explain them before the underwriter asks. If there's customer concentration, address it. If your experience is adjacent rather than direct, explain why it transfers. If the seller is staying for transition support, make that specific.

That's the shift that matters. You're not asking a lender to take a chance on you. You're showing that the transaction has been prepared carefully enough that the lender can move with confidence.

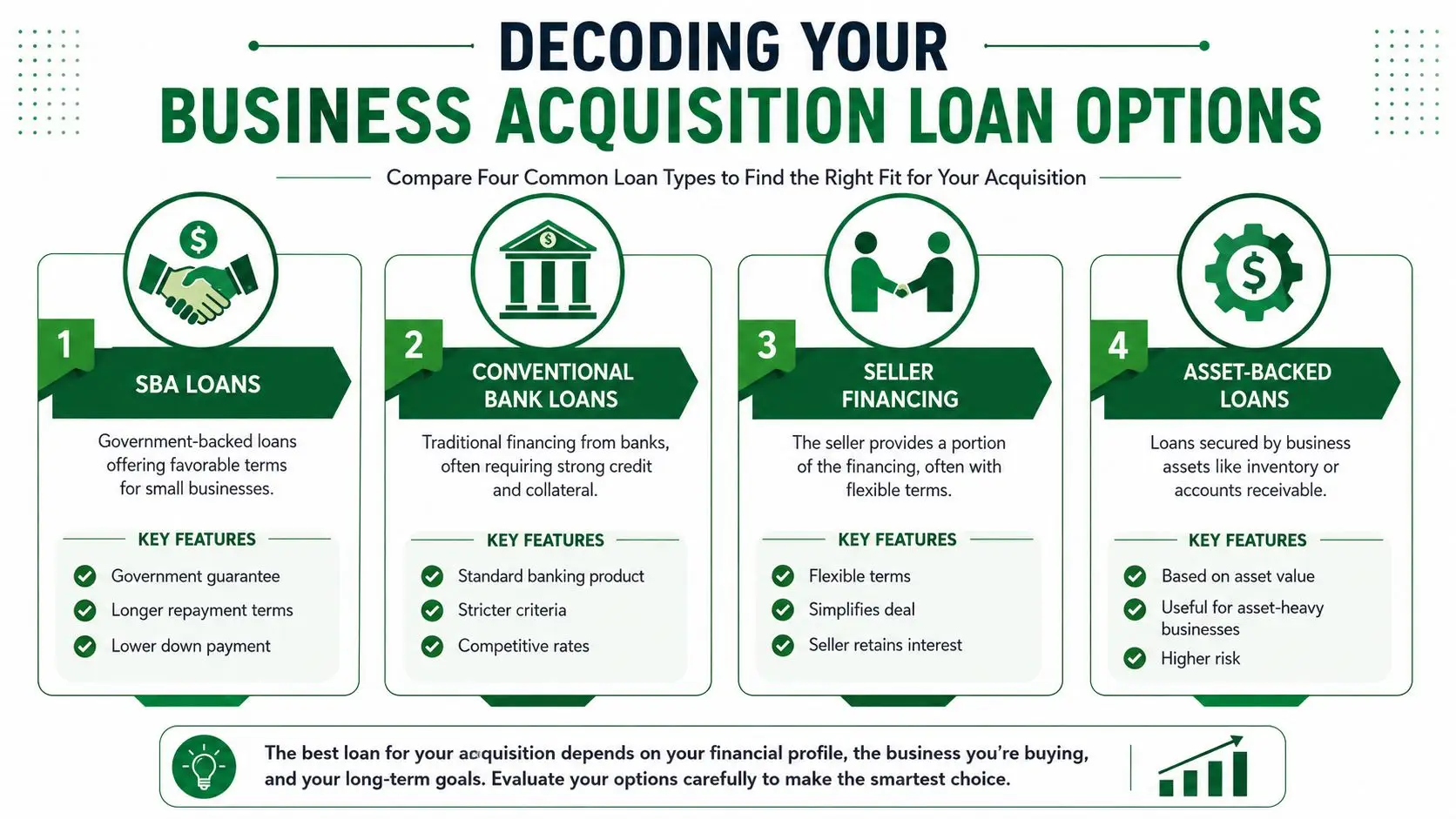

Decoding Your Loan Options for Business Acquisition

The financing structure shapes everything. It affects your cash at closing, your monthly debt burden, your negotiating power with the seller, and whether the deal even gets through credit.

For most small business acquisitions in the U.S., the SBA 7(a) program is the main government-backed route. The SBA states that its loans range from $500 to $5.5 million, and for FY 2023 the average SBA loan amount was about $480,000. In acquisition deals, buyers often use about a 10% down payment, with the SBA-backed loan covering the balance through the approved structure, according to the SBA loan programs overview.

Why SBA 7(a) usually leads the conversation

For acquisition lending, SBA 7(a) is the workhorse because it can fit a wide range of operating businesses. It's often the first place buyers should look when they need a practical loan to buy a business without tying up too much personal cash.

Conventional bank loans can still make sense. They tend to fit stronger borrowers, cleaner industries, and asset-rich businesses. Seller financing can strengthen a deal if the note terms align with lender rules and the seller remains economically committed to the transition. Asset-backed lending works best when the company has enough eligible collateral to drive the loan. It is not a cure for weak cash flow.

If you operate outside the U.S. or want a comparison point for how commercial underwriting is framed in other markets, this page on commercial lending with EHF Mortgages gives useful context on how lenders assess business borrowing requests.

For a deeper breakdown of the SBA structure buyers most often use, review this guide to SBA 7(a) loans.

Business Acquisition Loan Comparison

| Loan Type | Best For | Typical Down Payment | Key Advantage |

|---|---|---|---|

| SBA 7(a) | Most small business acquisitions with solid cash flow | About 10% in many acquisition structures | Government-backed flexibility for change of ownership |

| Conventional bank loan | Strong borrowers and asset-heavy deals | Often 20% to 30% | Traditional bank structure |

| Seller financing | Deals where the seller is willing to support the transition | Varies by structure | Flexible terms and alignment from the seller |

| Asset-backed loan | Businesses with meaningful inventory, receivables, or equipment | Varies by collateral coverage | Collateral-based approach |

How buyers choose the wrong structure

The wrong question is, “What loan can I qualify for?”

The better question is, “What structure gives the lender the cleanest path to yes while leaving enough cash in the business after closing?”

That distinction matters. Buyers lose deals by trying to force one source to do everything. A seller note may improve the stack. Working capital may need to be planned separately. Some structures look cheaper at first but become harder to close because they rely on collateral or underwriting assumptions that don't match the target business.

The best acquisition financing isn't the most creative structure. It's the one an underwriter can defend and a closing team can execute.

Building Your Bulletproof Loan Application Package

A lender doesn't approve documents. A lender approves a story backed by documents.

If the package feels pieced together, the underwriter assumes the transaction is too. The strongest files answer the obvious questions before they're asked and present the buyer as someone who understands both the business and the obligation they're taking on.

A useful benchmark is a 10% to 20% equity injection, with many SBA acquisition deals requiring at least 10% cash or an equivalent mix that can include seller financing on full standby. Conventional acquisition loans often require 20% to 30% down, based on this business acquisition financing overview from F.B. Blake Bank.

What underwriters want to see immediately

The package should make four things easy to verify.

- Who you are as the buyer: Resume, ownership structure, and a short explanation of your operating background.

- What's being purchased: Business summary, purchase terms, seller support period, and any lease or location issues that affect continuity.

- How repayment works: Historical financials, cash flow analysis, and realistic projections.

- Where the cash comes from: Bank statements, source of injection, and any third-party contributions documented clearly.

A due diligence process helps pull these threads together before a lender does it for you. This business acquisition due diligence checklist for SBA loan buyers is a solid working reference.

How to make the file coherent

Buyers often submit all the required items and still create a weak package. The usual reason is inconsistency.

If your resume says you led operations, but your narrative says you'll hire someone else to run the business, underwriting notices. If your projection assumes smooth customer retention but the seller transition plan is vague, underwriting notices. If your equity injection comes from multiple accounts with no explanation, closing notices.

A bulletproof package usually includes:

- A concise buyer memo: One or two pages that explain the deal in plain English.

- Clean financial presentation: Historical business results plus a reasonable post-close view.

- Specific transition details: Seller training, key employee continuity, and customer handoff.

- Documented liquidity: No mystery funds, no last-minute transfers without support.

- A realistic operating plan: Not hype. Not “we'll double revenue.” Just what you'll do first.

Underwriting insight: If the numbers are acceptable but the narrative is sloppy, lenders assume execution will be sloppy too.

This short walkthrough is useful before you finalize the package:

A good package doesn't just reduce questions. It improves lender competition because each bank is reviewing the same organized story instead of trying to reconstruct the deal from scattered files.

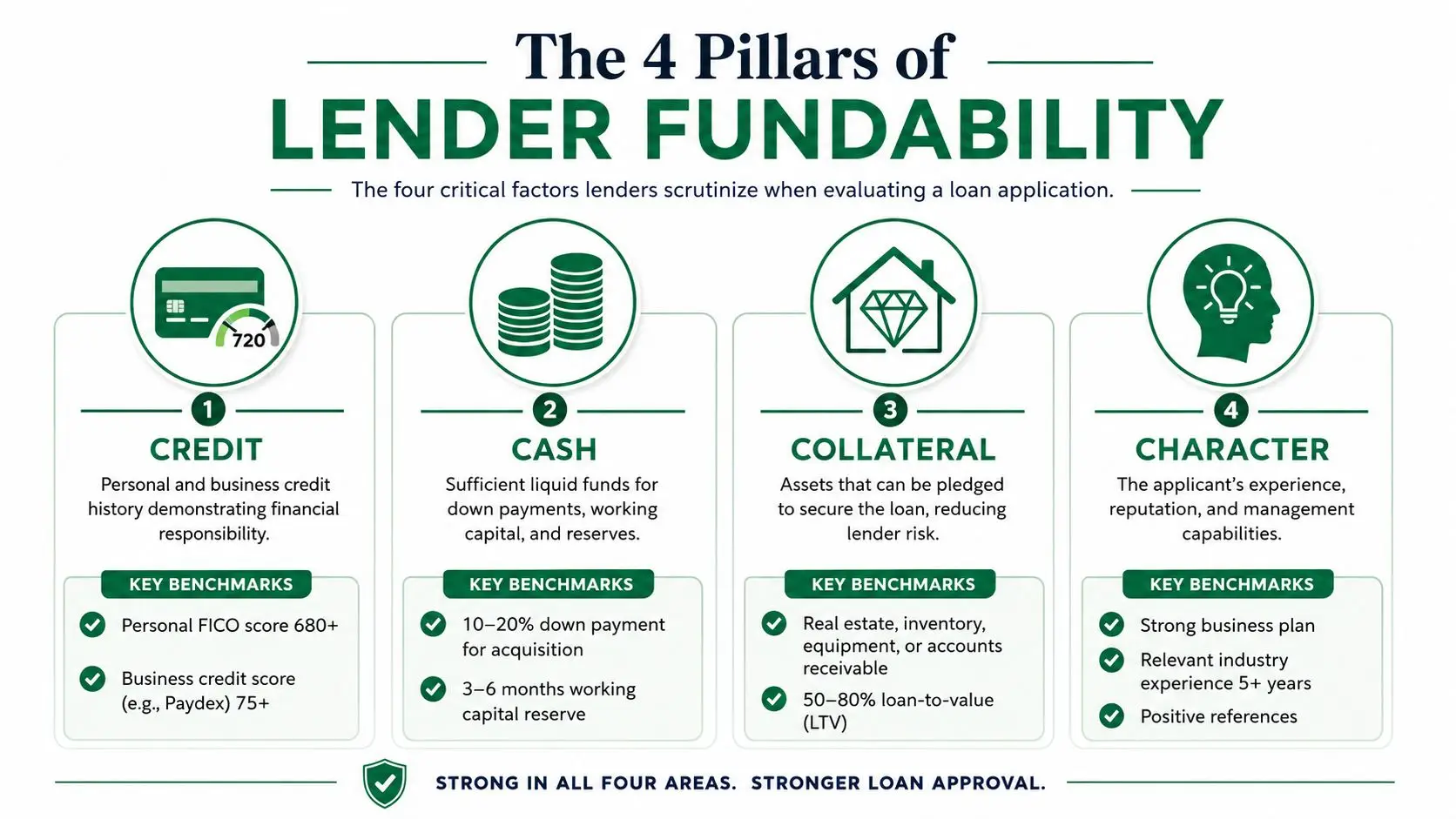

Meeting Lender Eligibility and Credit Requirements

Most buyers think lenders care first about the credit score. In acquisition lending, credit matters, but it's only one part of the file.

The lender is really trying to answer a broader question: is this buyer likely to make the business more stable or less stable after the transfer? That's why the evaluation tends to cluster around credit profile, available cash, collateral position, and the buyer's judgment.

The SBA guarantee helps. The SBA guarantees loans to reduce lender risk, with guarantees on acquisition loans commonly reaching up to 85% in the relevant program context, and the Federal Reserve reported that 37% of small employer firms applied for a loan in 2023, as summarized in this business acquisition loan overview.

The four issues lenders actually care about

Credit

Credit tells the lender how you've handled obligations before. A credit issue doesn't always kill a deal, but unexplained issues do. If there's a prior problem, address it directly and document the resolution.

Cash

The injection matters, but so does what's left after closing. A buyer who uses every available dollar on the down payment creates stress immediately. Lenders prefer buyers who still have room to operate, absorb surprises, and handle working capital needs.

Collateral

Collateral supports the file, but in acquisition lending cash flow usually drives the decision more than hard assets alone. That's especially true in service businesses where value sits in contracts, repeat customers, and operating history.

Character

Many files often separate at this point. Character isn't a vague moral category. In practice, it means management credibility. Can you explain the business? Do you respond quickly? Do your documents line up? Have you thought through employee retention and the seller handoff?

A lender will forgive limited direct industry experience sooner than they'll forgive disorganization, evasiveness, or weak judgment.

How lenders think about repayment risk

Repayment is the center of underwriting. The lender wants to know whether the business can support debt and still function after the ownership change.

That's why buyers should prepare to discuss cash flow carefully, not casually. Even outside acquisitions, lenders rely heavily on repayment coverage analysis. Founders who want a plain-language explanation of that mindset may find these DSCR insights for SaaS founders useful, even though the industry context differs.

What works in practice:

- A conservative narrative: Show how the business continues, not how it suddenly transforms.

- Documented buyer capacity: Explain your role, not just your title.

- Clean money trail: Every dollar in the injection should be easy to source.

- Operational realism: If the seller currently does key work, explain exactly who takes that over.

What does not work:

- Aggressive projections without support

- Vague plans for replacing the owner

- Overstating your experience

- Treating underwriting like a paperwork formality

A fundable buyer doesn't just meet requirements. A fundable buyer reduces uncertainty.

Navigating Lender Selection and Negotiation Strategy

The buyer who takes the first acceptable offer usually overpays somewhere. Maybe it's rate. Maybe it's structure. Maybe it's covenant pressure, weaker flexibility, or a closing process that drags until the seller loses patience.

That's why lender selection is a strategy problem, not an administrative task.

Why one bank is rarely enough

Different lenders like different deals. Some are comfortable with service businesses. Some lean toward franchise resales. Some move well on clean main-street acquisitions but slow down on anything involving multiple entities, investor layering, or seller carry complexity.

That variation is exactly why shopping intelligently matters. Many acquisition deals are solved through layered capital stacks rather than one perfect approval. Public sources note that microloans are capped at $50,000 and are not designed for full acquisitions, while buyers may combine SBA-backed lending, CDFIs, and local programs depending on the gap they need to solve, as discussed in this analysis of capital access for underserved businesses.

A competitive process does three useful things:

- It tests lender appetite early: You learn who likes your deal.

- It strengthens your bargaining position: Terms tighten up when lenders know they're not alone.

- It protects the timeline: If one lender slows down, you're not restarting from zero.

What to negotiate besides rate

Rate matters, but buyers fixate on it too much. In real closings, a deal can become more expensive through structure than through pricing alone.

Read the term sheet for:

- Equity requirement: Confirm exactly what counts toward injection.

- Seller note treatment: Some structures work better than others.

- Working capital expectations: Make sure the business isn't underfunded on day one.

- Closing conditions: Third-party reports, insurance, entity documents, and lease issues can all affect certainty.

- Guarantor requirements: Know who is on the hook and what the lender expects from them.

Negotiation test: If the lender's terms look fine only when everything goes perfectly, they're probably not fine.

This is one area where a broker can materially change the outcome. A brokerage like GoSBA Loans can run lender matching, collect competing term sheets, and manage underwriting communication so the buyer isn't trying to negotiate while also learning the process in real time.

The practical goal isn't more conversations. It's better conversations with lenders who already fit the deal.

From Term Sheet to Closing Wires Your Timeline

Approval momentum can disappear after the term sheet if nobody is managing the details. This phase is where buyers discover that “approved” and “funded” are very different words.

A realistic path from term sheet to wires usually moves through underwriting cleanup, third-party reports, legal documentation, insurance, entity review, and final closing coordination. If you want a more detailed sequence, this LOI to closing timeline for SBA business acquisitions maps the process clearly.

The stages after approval starts

Most closings follow a pattern.

First, the lender clears remaining underwriting conditions. That often means updated statements, clarifications on the purchase agreement, verification of injection funds, and confirmation that the post-close structure still matches what credit approved.

Next come third-party items. Depending on the deal, that may include valuation work, lease review, or property-related diligence if real estate is involved. Then legal and closing teams assemble the final package, coordinate signatures, and schedule funding through escrow or direct disbursement.

Where deals slow down

The delays are rarely mysterious. They're usually operational.

- Missing seller documents: The seller is often slower than the buyer expects.

- Entity cleanup: Operating agreements, formation records, or ownership questions can hold up closing.

- Lease friction: Landlord consent and assignment details can become a major issue late in the process.

- Unclear funding path: If the injection or side financing changes midstream, the lender may need to re-review.

Underserved buyers need one more layer of planning. The useful question isn't whether a general program exists. It's which financing channel fits the buyer's profile and the deal structure. For borrowers outside standard bank credit boxes, practical paths often include CDFIs, SSBCI-supported lenders, and USDA rural programs, while approval still depends on lender underwriting, as noted in this overview of funding paths for minority business owners.

A smooth closing usually comes from one habit: keep every party moving before the deadline forces them to move. Buyers who stay organized, answer quickly, and keep the seller engaged tend to close with fewer surprises. Buyers who go quiet after the term sheet often watch small issues pile into major delays.

If you're preparing a loan to buy a business and want help building a lender-ready package, comparing structures, and coordinating offers from multiple SBA lenders, GoSBA Loans is one option to consider. The right support can make the difference between submitting an application and closing a deal.