A lot of owners reach the same point at roughly the same time. Sales are there, demand is real, and the next move is obvious. Take the bigger space, add the second location, buy the machine, hire the crew, carry more inventory, or purchase the building instead of renting it. Then the plan stalls because the cash required to grow is larger than what the business can comfortably pull from retained earnings.

That's where business expansion financing stops being an abstract finance term and becomes an operating decision. The issue usually isn't whether growth is possible. It's whether the financing structure fits the business you already have, the expansion you're planning, and the way lenders underwrite risk.

Owners often come in thinking they need “a loan.” What they usually need is a specific kind of capital, matched to a specific use of funds, on terms the business can support without straining liquidity. That's a very different question, and it's the one lenders are answering.

Table of Contents

- Financing Your Next Growth Phase

- Debt Equity and Mezzanine Financing Explained

- Common Debt Instruments for Business Expansion

- How SBA 7(a) and 504 Loans Fuel Growth

- Understanding Lender Underwriting Criteria

- Preparing Your Business for a Successful Application

- Building Your Capital Stack and Choosing a Partner

- Frequently Asked Questions About Expansion Loans

Financing Your Next Growth Phase

A manufacturer outgrows its current shop because lead times are slipping. A medical practice wants to open a second location because patient demand is already there. A contractor sees more work coming in but can't take it without trucks, staff, and working capital. These are healthy problems, but they still need capital.

Expansion financing works best when the business has already proven the base model. The lender is not betting on a dream. The lender is looking at an operating business that has traction and needs outside capital to move into its next phase without draining cash reserves.

That matters because growth financing is not some edge case in commercial lending. The U.S. small business lending market is estimated at $1.4 trillion, and the outstanding value of small business loans at depository institutions rose from $173 billion in 1995 to $368 billion in 2019, with another $300 billion when commercial real estate loans are included, according to the Bipartisan Policy Center's small business financing market analysis. That tells you something important. Businesses borrow to expand every day, across working capital, equipment, and real estate.

The real problem is usually structure

Most owners don't fail because there's no capital available anywhere. They struggle because the first structure they consider is often the wrong one.

A long-term real estate project shouldn't be forced into a short-term working capital product. A staggered hiring and inventory buildout often doesn't belong in a rigid lump-sum loan. A major fixed-asset purchase shouldn't leave the operating company starved for liquidity right after closing.

Expansion debt should support the business after closing, not just get the deal done on closing day.

When owners understand that, better decisions follow. They stop asking only, “Can I get approved?” and start asking the better question, “What kind of financing matches this expansion?”

Debt Equity and Mezzanine Financing Explained

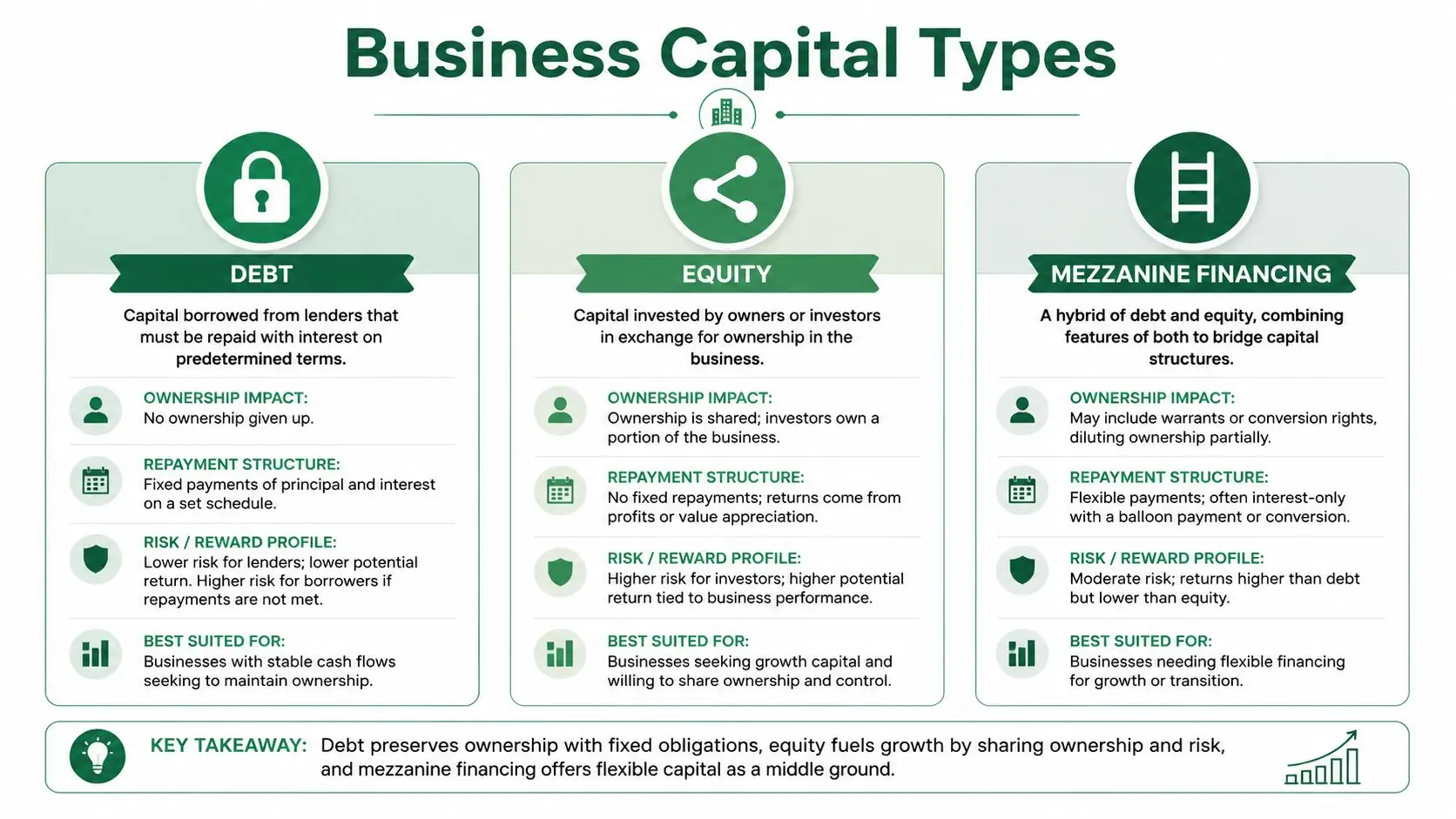

Most growth capital falls into three buckets. Debt, equity, and mezzanine financing. If you understand the trade-off in each one, you'll make better expansion decisions and avoid a lot of expensive mistakes.

How each capital type changes control and risk

Debt is the simplest to grasp. You're renting money. The lender gives you capital, and you agree to pay it back under a defined repayment schedule. If the business performs well, you keep the upside after making payments. If the business struggles, the payment obligation remains.

Equity is different. You're selling a piece of the business in exchange for capital. There may be no scheduled monthly principal payment, but you've brought in an owner or ownership-like stakeholder who expects returns, influence, or both. Equity can preserve cash flow in the short run, but it changes control and future economics.

Mezzanine sits in the middle. It's a hybrid structure that behaves partly like debt and partly like equity. In practical terms, it often shows up when a business needs more capital than senior lenders want to provide, but the owner doesn't want to give away as much ownership as a full equity raise would require.

Here's the cleanest way to understand it:

| Attribute | Debt Financing | Equity Financing | Mezzanine Financing |

|---|---|---|---|

| Repayment | Scheduled principal and interest | No standard loan repayment schedule | Usually debt-like, sometimes with equity-style features |

| Ownership dilution | None | Yes | Limited or conditional |

| Control impact | Lower | Higher | Moderate |

| Cost profile | Predictable but fixed obligation | No monthly debt service, but ownership is sold | Often more expensive and more negotiated |

| Best use case | Proven cash flow and defined repayment ability | High-growth or cash-constrained situations | Deals that need a gap filled between senior debt and owner equity |

| Lender or investor focus | Repayment reliability | Enterprise upside | Both downside protection and upside participation |

When each option makes sense

For most established small businesses pursuing expansion, debt is still the first place to look. It preserves ownership and works well when the company can show durable cash flow. That's especially true when the expansion has a clear use of funds, such as tenant improvements, equipment, inventory, or an owner-occupied building.

Equity makes more sense when current cash flow won't comfortably support new debt, or when the growth plan has a longer runway before it turns into stable earnings. The trade-off is that equity is rarely just money. It often comes with governance expectations, reporting obligations, and strategic influence.

Mezzanine is less common in smaller deals, but it matters for businesses that are too complex for plain senior debt and not a clean fit for venture-style capital. It can solve a capital gap, but it raises the importance of deal structuring and partner selection.

Practical rule: If you can fund expansion with affordable debt that the business can reliably service, that usually preserves the most long-term value for the owner.

Common Debt Instruments for Business Expansion

Owners get in trouble when they choose a loan product by rate alone. Lenders start with a different question. Does the structure match the use of funds, the repayment source, and the useful life of what is being financed?

That match matters more than most owners expect. A lender may like the business and still decline the request, or trim the amount, if the debt structure puts unnecessary pressure on cash flow.

Term loans for defined projects

A term loan fits expansion projects with a clear budget and a clear finish line. Typical examples include a facility buildout, a new location opening, a planned inventory buy tied to a launch, or a one-time operating investment that should pay back over a known period.

The appeal is simple. You receive a lump sum, put it to work, and repay it on a fixed schedule. From an underwriting standpoint, that works best when management can show where the money goes, when the project will be completed, and how existing or projected cash flow will cover the payment.

The common mistake is using a term loan for expenses that will hit in stages over six to twelve months. If the business borrows the full amount up front but spends it slowly, interest starts running before the capital is producing much return.

Lines of credit for uneven timing

A business line of credit works better when the expansion will unfold in waves rather than one closing date. Hiring ahead of revenue, rolling out marketing by market, carrying larger inventory for seasonal demand, or covering contract-driven working capital are all examples.

You draw only what you need, and interest applies to the outstanding balance instead of the full approved amount. That gives the business more control over timing and preserves flexibility if the expansion plan shifts.

Lenders still want discipline here. They usually look for a credible borrowing base, a clean pattern of account activity, and a realistic path to paying the line down. A revolving line used to fund long-term assets often becomes a refinancing problem later, especially if the bank expects periodic cleanup.

Equipment financing for asset-backed purchases

Equipment financing is often the cleanest option when expansion depends on machines, vehicles, production equipment, medical devices, or other revenue-producing hardware. The collateral is identifiable, the use of funds is specific, and the lender can underwrite the purchase against a tangible asset instead of a broad growth story.

That does not make it automatic. The lender still needs to see that the equipment fits the business model and that the payment lines up with the income the asset is expected to produce. I tell owners to evaluate equipment debt on three levels:

- Match the term to the asset's useful life. A short amortization on equipment that should generate value for years can strain monthly cash flow for no good reason.

- Preserve liquidity for the ramp-up period. If the purchase also requires operator training, inventory, installation, or delayed customer billing, keeping some cash on hand usually matters more than making the largest possible down payment.

- Show the revenue case in plain terms. Lenders respond well to specific explanations. More units per hour, lower labor cost, better margins, new contract capacity, or replacement of unreliable equipment all help the file.

For larger fixed-asset projects, it also helps to understand how SBA 504 loans for fixed-rate financing for real estate and major equipment are structured. If the purchase is primarily equipment-focused, this overview of SBA financing for equipment acquisition is also useful for setting borrower expectations before you apply.

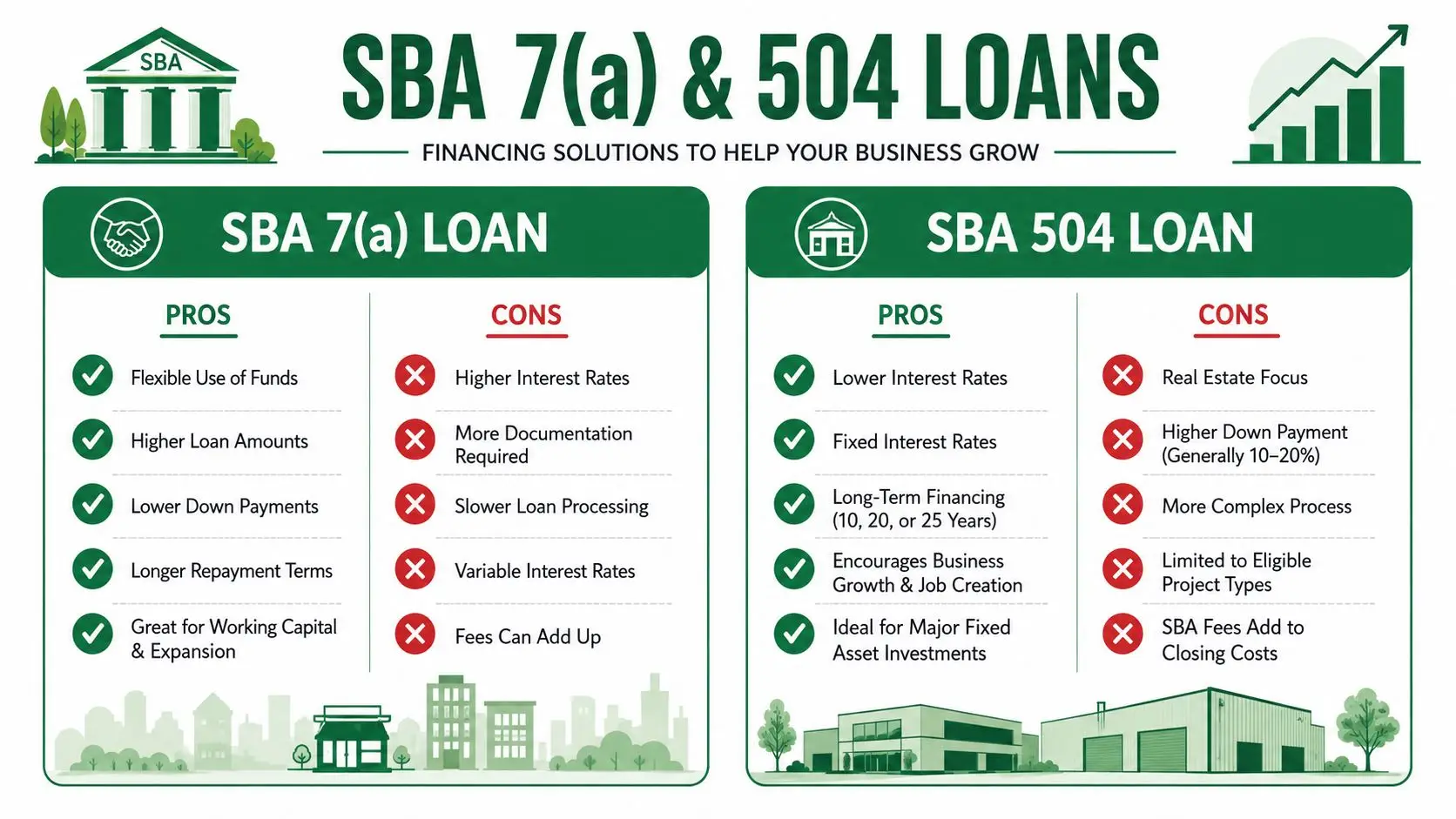

How SBA 7(a) and 504 Loans Fuel Growth

A common expansion scenario looks like this. The business is profitable, the owner has a clear use for the funds, and the bank still hesitates because the request does not fit cleanly inside conventional credit policy. The project may need a longer term, the collateral may not fully cover the loan, or the use of proceeds may combine real estate, equipment, and working capital. SBA financing often works because it gives the lender a structure that can pass credit where a conventional request stalls.

That distinction matters. Owners often shop for “an SBA loan” as if the programs are interchangeable. Underwriters do not view them that way. They start with use of proceeds, collateral position, repayment source, and whether the project fits program rules under the SBA SOP. If those pieces do not line up, a strong business can still get declined.

Why SBA structures work when conventional loans fall short

SBA lending gives banks room to approve deals that are sound but outside normal credit guardrails. That usually shows up in three places:

- Longer repayment terms: Lower monthly debt service can make an expansion payment fit actual business cash flow.

- Flexible collateral treatment: A shortfall in collateral does not automatically end the conversation if repayment strength is there.

- Broader use of proceeds: A single structure can often cover several parts of a growth project instead of forcing the owner to patch together separate loans.

The best files still win on repayment, not on the guarantee alone. A lender wants to see a business that already performs well enough to carry debt, plus a project that has a clear business purpose. “We need capital to grow” is weak. “We are opening a second site with signed lease terms, defined build-out costs, a staffing plan, and cash reserves for ramp-up” is underwritable.

When 7(a) fits better than 504

SBA 7(a) is usually the better option when the expansion includes mixed uses of funds. That can mean a new location with tenant improvements, equipment, inventory, soft costs, and working capital all in one request. It can also fit partner buyouts, debt refinance tied to expansion, or a business acquisition with post-close operating needs.

From an underwriting standpoint, 7(a) works best when the lender can trace each use of proceeds to a practical operating result and see that the full payment fits the company's cash flow. Flexibility helps, but it also creates more questions. If the request includes several moving parts, expect the lender to press harder on assumptions, timing, and contingency planning. This guide to SBA 7(a) loans in 2026 including requirements and qualification issues is a useful reference if you want to understand how lenders frame those questions.

If the project is centered on machinery or production equipment, owners should also review practical guidance on SBA financing for equipment acquisition from Noreast Capital Corporation. Equipment requests often look straightforward, but approvals still depend on installation timing, useful life, vendor documentation, and whether the business can support the payment before the asset reaches full output.

When 504 is the sharper tool

SBA 504 is more specialized, and that is exactly why it can be so effective. It is built for owner-occupied commercial real estate and major fixed assets. If the project is primarily a building purchase, a facility improvement, or large equipment tied to long-term operating capacity, 504 often gives the cleaner structure.

Lenders like 504 when the asset is central to the business and the expansion case is easy to document. The project has a defined cost. The collateral is identifiable. The use of proceeds is narrow. The fixed-rate component can also help a borrower protect cash flow against future rate pressure, which matters on larger projects with long payback periods.

The trade-off is reduced flexibility. A 504 loan is not the right tool for a broad working-capital request or a project that mixes too many soft costs and operating expenses. Borrowers get into trouble when they try to force a 504 structure onto a deal that really belongs in 7(a).

The practical rule is simple. Use 7(a) when growth requires a flexible business-purpose loan. Use 504 when growth is driven by a fixed-asset investment that should be financed on long, stable terms. That is how lenders sort these requests, and borrowers who present the deal the same way usually move through underwriting with fewer surprises.

Understanding Lender Underwriting Criteria

Owners often think underwriting is about the business plan presentation. It isn't. Underwriting is a credit decision built around evidence, consistency, and repayment logic.

Lenders commonly review personal credit, time in business, annual revenue, cash flow, financial statements, and collateral because underwriting capacity is driven by stable historical performance and documented repayment ability, according to NerdWallet's business expansion loan guidance. That same guidance makes the core point clearly: lenders are pricing the probability that new cash flow will service principal and interest.

Cash flow durability is the center of the file

A lender will usually trust documented history more than a forecast. That doesn't mean projections are unimportant. It means projections only work when they sit on top of a business that already shows operating discipline.

If you want to think like an underwriter, start with one question: how durable is the current cash flow?

Durable doesn't mean perfect. It means the business shows enough stability that the lender can reasonably believe repayment will happen even if the expansion takes time to ramp.

Here's what weakens a file quickly:

- Inconsistent financial reporting: Numbers that don't tie across tax returns, P&Ls, and bank statements.

- Thin explanation for cash swings: Revenue volatility without a documented reason.

- Credit issues with no narrative: Past problems that are ignored instead of addressed directly.

- Expansion logic without repayment math: A big vision but no clear path showing how debt service is covered.

A borrower who wants to strengthen this part of the file should also understand how to develop company credit. It won't replace cash flow, but stronger business credit habits can make the file cleaner and more credible.

The five underwriting questions behind the paperwork

Underwriters may use different templates, but most of the file boils down to five practical questions that mirror the classic Five C's of Credit.

| Underwriting question | What the lender is really checking |

|---|---|

| Can this owner be trusted to perform? | Character, credit history, responsiveness, and disclosure |

| Can the business repay the debt? | Capacity, recurring cash flow, and debt service support |

| Is the owner financially committed? | Capital invested and willingness to share risk |

| If the deal struggles, what support exists? | Collateral and fallback security |

| Does the request make sense in context? | Conditions, industry risk, and use of funds |

For a deeper look at how lenders think through this process, this explanation of how SBA lenders underwrite your deal is worth reading.

A strong application tells one coherent story. The tax returns, interim statements, credit profile, and use of funds all point in the same direction.

Preparing Your Business for a Successful Application

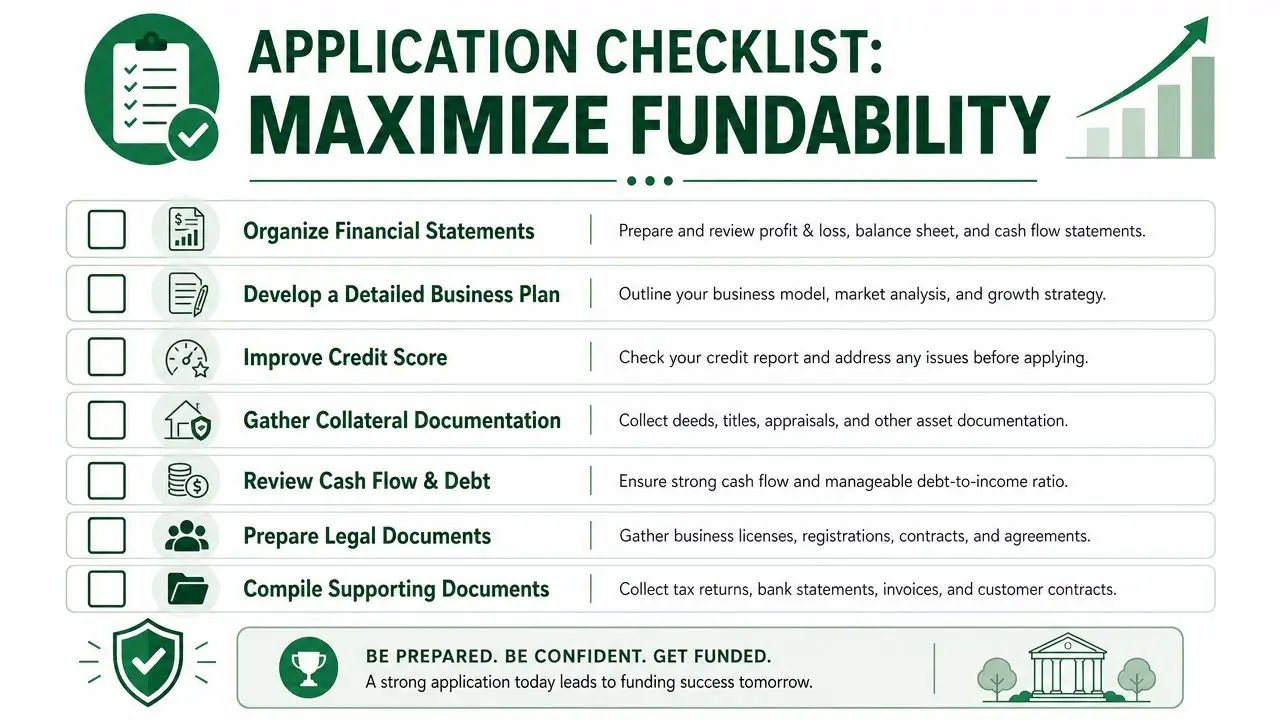

A good financing request is built before the application is submitted. That's where many approvals are won or lost.

In 2023, 46% of small businesses seeking loans were funding expansion, but only 34% of SBA loan applicants received full approval, according to Credit Suite's small business lending statistics and trends roundup. If you're competing for lender attention, a clean and fully prepared package matters.

Build a lender-ready file before you apply

Start with the documents lenders almost always ask for. If these are incomplete or inconsistent, the process slows immediately.

Business financial statements

Prepare current profit-and-loss statements, balance sheets, and business tax returns. Make sure interim statements reconcile to the story you're telling about current performance.Personal financial information

Most expansion lenders, especially in SBA lending, will evaluate the owner as well as the company. Personal tax returns, a personal financial statement, and explanations of any major liabilities should be ready.Bank statements and liquidity support

Lenders want to see actual operating behavior, not just accrual results. Bank activity often confirms whether revenue, expense patterns, and liquidity are consistent with the file.Use of funds breakdown

Don't submit “expansion” as the only explanation. Break it down. Equipment, buildout, inventory, soft costs, real estate, refinance, contingency, working capital. Precision helps underwriters get comfortable.

After the numbers are in order, add context. This short video is a useful overview for owners who want a practical framing of the loan-prep process before they talk to lenders.

Turn the expansion story into an underwritable plan

The best applications explain not only what the owner wants to do, but why the financing structure makes sense.

Use this checklist when shaping the narrative:

- Define the project clearly: What exactly is being funded, and why now?

- Show operational readiness: If you're opening a site, who will run it? If you're buying equipment, who will use it and how quickly will it be integrated?

- Present realistic projections: Forecasts should connect to current revenue patterns, known contracts, backlog, or capacity constraints. Aggressive projections hurt more than conservative ones.

- Address weaknesses upfront: If there was a bad year, a credit event, or a temporary decline in margins, explain it early and document the recovery.

- Match the debt to the asset: Short-term needs should stay short. Long-term assets should be financed with patience.

What lenders want to see: a borrower who understands the project, knows the numbers, and has already done the organizational work that reduces execution risk.

Building Your Capital Stack and Choosing a Partner

A common expansion scenario looks like this: the project is sound, revenue is real, and the borrower still cannot get the full request from one lender on clean terms. That usually means the issue is not the business. It is the structure.

Lenders do not approve expansion financing in a vacuum. They look at total project cost, available equity, collateral position, repayment ability, and how each dollar in the deal behaves if the plan runs late or sales ramp more slowly than expected. In practice, many good deals close only after the capital stack is adjusted to fit those credit realities.

What a capital stack looks like in practice

A workable stack might include owner injection, senior debt, and a seller note or standby note for an acquisition, partner buy-in, or site expansion. Another might combine an SBA loan with outside equity so the business can keep enough cash on hand for payroll, inventory, and the first few months of execution.

Good structure solves specific underwriting problems.

A well-built capital stack usually does three jobs:

- Preserves operating cash: Owners often want to put in as little cash as possible. Lenders want to see enough equity to show commitment and reduce risk. The right stack protects day-to-day liquidity without making the deal look thinly capitalized.

- Matches repayment to the asset: Equipment, real estate, tenant improvements, and working capital should not all be financed the same way. A lender will notice when short-term debt is carrying long-term assets.

- Clarifies who stands where: Senior lenders care about lien position, repayment priority, and whether subordinate debt is on standby when required. If those pieces are vague, underwriting slows down fast.

Equity can help, but it is not cheap. It reduces payment pressure and can strengthen a file when cash flow is tight, but it also dilutes ownership and often adds another voice to major decisions. Owners considering that route can use the Gritt.io investor database to identify potential investors before deciding whether outside capital belongs in the deal.

How to choose the right financing partner

Product fit matters. Partner fit matters just as much.

A conventional bank may price well and move efficiently if the request falls inside its credit box. A community lender may be better when the deal needs more context or local market judgment. A broker is often useful when the request involves multiple use-of-funds categories, a partial injection from another source, or lender-specific SBA preferences.

That is the practical value of a firm like GoSBA Loans. It operates as an SBA loan brokerage, helping borrowers match with participating lenders and organize the package around the actual transaction structure. That can save time when one lender is comfortable with business acquisitions, another prefers owner-occupied real estate, and a third is more flexible on goodwill, startup costs, or partner buyouts.

Before choosing a financing partner, ask direct questions:

- What types of expansion transactions have they closed recently?

- Do they understand SBA standby requirements, injection rules, and debt refinance limits when those apply?

- Will they help structure the request before submission, or only collect documents?

- Can they explain why a lender would say no, not just why one might say yes?

The last question matters most. A useful advisor understands credit policy from the lender's side and can spot problems early, before you spend weeks on a file that was never going to clear underwriting.

Frequently Asked Questions About Expansion Loans

Do I need strong current cash flow to qualify?

Usually, yes. Expansion financing is still debt, and debt needs repayment support. Lenders may like the growth story, but they underwrite the ability to repay from documented performance and a credible plan.

Can I get financing if my personal credit isn't great?

Sometimes, but weak personal credit creates more friction. It doesn't automatically kill the deal. What matters is whether the issue is isolated, explainable, and outweighed by strong business performance and overall file quality.

Will collateral decide the entire approval?

Not by itself. Collateral matters, especially in asset-heavy deals, but it usually isn't the whole decision. A lender would rather see durable cash flow and a sensible structure than rely only on collateral as the backup plan.

What's the best loan for expansion?

There isn't one universal answer. A line of credit fits uneven working capital needs. A term loan fits a defined project. SBA 7(a) works well for mixed-use expansion. SBA 504 is often better for long-term fixed assets like owner-occupied real estate or major equipment.

Should I apply before I have all my documents together?

No. That's one of the easiest ways to waste time and weaken the file. Incomplete applications create avoidable follow-up, inconsistent narratives, and lender fatigue.

Is expansion financing only for large companies?

No. Many small businesses need growth capital, but the key issue is fundability, not size by itself. A smaller business with clean records, durable cash flow, and a well-framed request can be more financeable than a larger company with messy books and no clear use of funds.

If you're planning an expansion and want help figuring out whether SBA 7(a), 504, a line of credit, or a blended structure fits the deal, GoSBA Loans can help you evaluate lender fit, organize the package, and understand how the request is likely to be viewed in underwriting before you commit to a path.

Authored using Outrank tool