You've found a FedEx route for sale, the cash flow looks real, and the seller's timeline is moving faster than your bank. That's where most buyers hit the same wall. The business may be attractive, but buying it still requires a lending structure that fits an asset-light operation and an underwriter who understands route economics.

A FedEx SBA loan can solve that problem, but only when the deal is packaged correctly. Buyers who approach this like a standard small business purchase often get stuck on avoidable issues: weak liquidity, vague projections, poor documentation, or a business plan that never explains who will run the routes day to day.

The good news is that route acquisitions are financeable. The less comfortable truth is that approval usually turns on lender filters that many public guides barely mention. If you want to know whether a FedEx SBA loan is realistic for your deal, focus less on the broad question of eligibility and more on the quality of your loan file.

Table of Contents

- Financing Your Future with a FedEx Route

- Why SBA Loans Are a Top Choice for FedEx Routes

- SBA 7(a) vs SBA 504 for Your FedEx Business

- Are You Eligible for a FedEx SBA Loan

- Required Documents for Your Loan Application

- Real-World FedEx SBA Loan Scenarios

- Your Next Steps to Secure Financing

Financing Your Future with a FedEx Route

A FedEx route purchase usually starts with speed. A listing appears, an advisor sends a teaser, or a broker brings you a deal that looks like a fit. Then reality shows up. You need enough capital to close, enough cash left over to operate, and a lender willing to underwrite a business that doesn't come with heavy real estate collateral.

That's why SBA financing sits at the center of so many route acquisitions. It's not just another loan option on a menu. For many buyers, it's the financing structure that makes the purchase possible without forcing an oversized down payment or a short repayment window that strains cash flow from the start.

What buyers usually get wrong

Many first-time buyers ask one question too early: “Can I use an SBA loan to buy a FedEx route?” The practical answer is often yes. The underwriting question is more important: can you qualify, and does the deal hold up under lender review?

That shift matters. Lenders don't approve these files because the route exists. They approve them when the borrower shows liquidity, understands the operation, and presents a package that makes the handoff from seller to buyer feel controlled.

A strong file usually does three things well:

- Shows operational command through a route-specific business plan, not a generic acquisition summary.

- Explains the transition so the lender can see how drivers, fleet oversight, and day-to-day management will continue after closing.

- Protects working capital so the buyer isn't walking into ownership with no margin for repairs, payroll timing, or early operational friction.

A route can be a solid business and still be a weak loan file. Those are not the same thing.

The buyers who close most smoothly usually start preparing before they have perfect answers. They organize personal financials, review seller records early, and build projections that match the realities of dispatch, staffing, and vehicle maintenance. That work doesn't just help approval. It helps you avoid buying a route that only looks good in a summary sheet.

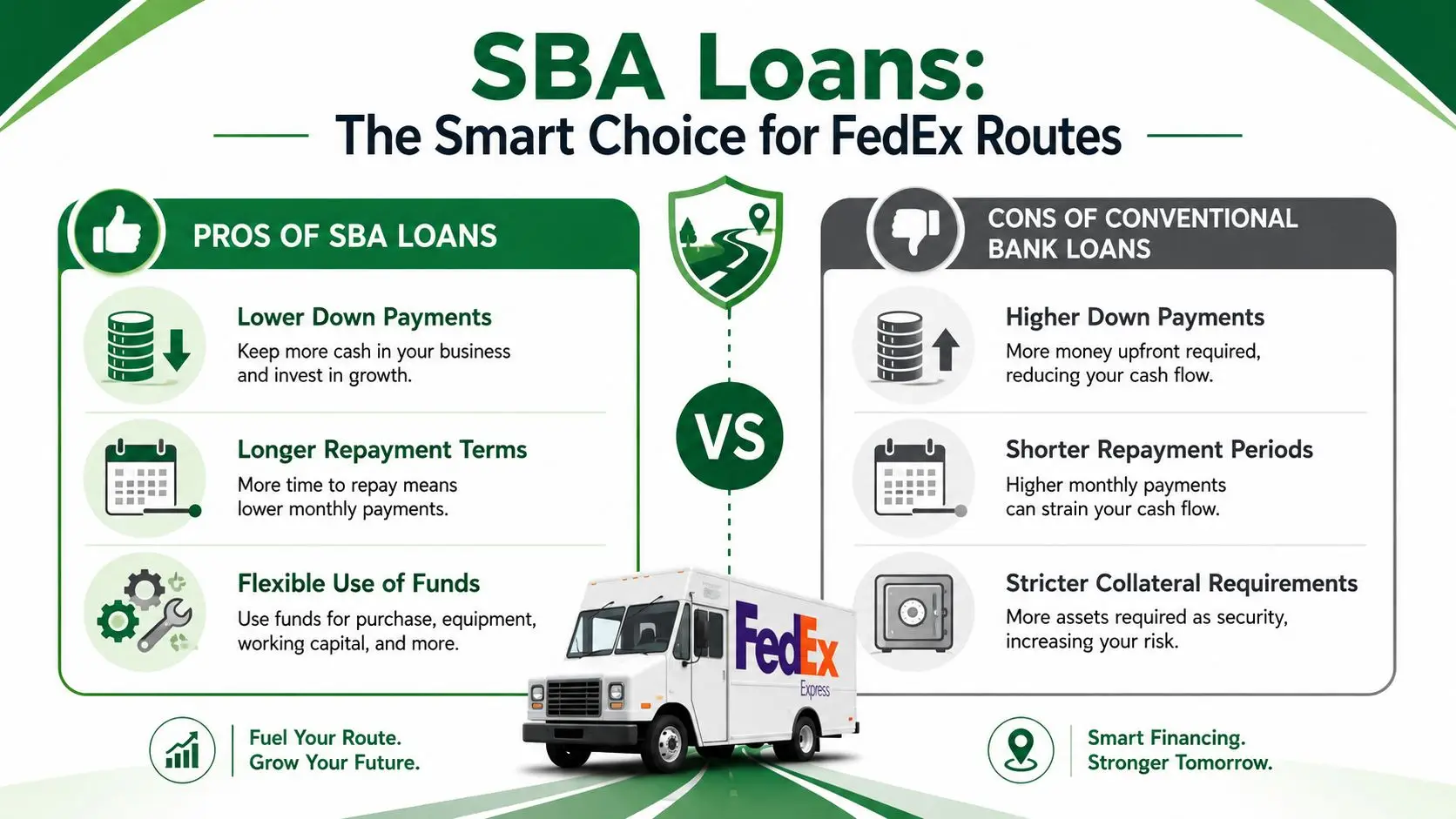

Why SBA Loans Are a Top Choice for FedEx Routes

Conventional lending often fits businesses with hard collateral. FedEx route businesses usually aren't built that way. The value sits in contracts, operational performance, management continuity, and the ability to keep trucks and drivers moving. That difference is exactly why SBA financing has become such a common fit for this niche.

Why conventional lenders hesitate

A traditional bank likes deals it can explain with collateral coverage. Route businesses often don't provide enough of that on their own. Buyers may end up being asked to support the loan with personal assets because the business itself may not have enough hard assets to satisfy the lender's risk model.

That creates a real trade-off. Conventional debt can work in some cases, but it often comes with tighter structure and a larger cash requirement up front. According to Windsor Advantage guidance on FedEx route financing, SBA loans for acquiring FedEx routes typically require 10% to 20% down, while conventional loans often require 25% or more. The same source notes that the SBA 7(a) program offers up to $5 million in financing with a standard 10-year repayment term, and that more than $83.8 million has been processed for FedEx route buyers through the SBA 7(a) program since 2010.

What the SBA structure changes

Lower required equity matters, but term length matters just as much. Route operators need room for driver hiring, fleet maintenance, and the normal friction that comes with taking over an existing operation. A longer fully amortizing structure gives the business more breathing room than a shorter acquisition loan.

Here's the practical comparison buyers should think about:

| Financing point | SBA 7(a) for routes | Conventional acquisition loan |

|---|---|---|

| Upfront cash need | Often lower | Often higher |

| Repayment term | Usually longer for this use case | Often shorter |

| Fit for asset-light businesses | Better | Often harder |

| Working capital preservation | Stronger | Usually tighter |

This doesn't mean SBA is automatically easy. It means the structure is better matched to the business model.

Practical rule: If the route only works on paper because you're stretching cash at closing, the problem isn't just the lender. It's the deal structure.

If you're comparing lenders, it helps to start with firms that already work in transportation and courier finance. A curated list of courier and delivery SBA lenders can save time because lender appetite in this niche isn't uniform.

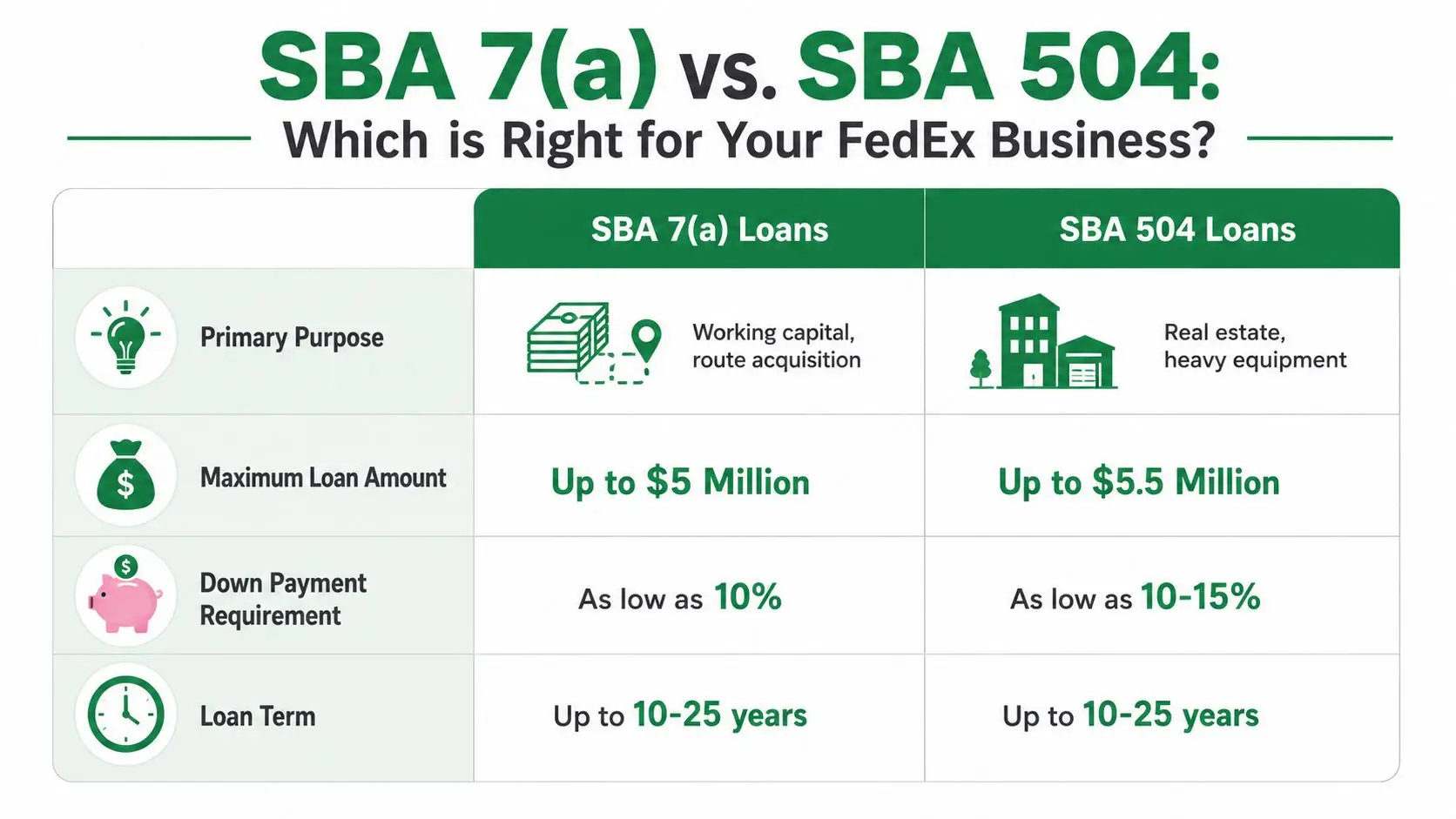

SBA 7(a) vs SBA 504 for Your FedEx Business

Most buyers looking for a FedEx SBA loan need clarity on one point. They don't need every SBA program. They need the right one.

For route acquisitions, SBA 7(a) is the program that usually belongs at the center of the conversation. It's flexible enough to handle the purchase of a business and the operating realities tied to that purchase. SBA 504 is different. It's a specialized product that typically makes sense when owner-occupied commercial real estate or major fixed assets are the priority.

When 7(a) is the right tool

If you're buying routes, taking over an operating company, or need a structure that can support acquisition plus operational needs, 7(a) is usually the better fit. It's the workhorse product for this type of transaction because the underwriting can follow the economics of the business acquisition itself.

A good primer on the broader rules and structure is this guide to SBA 7(a) loans.

This short video gives a useful overview before you get into lender-specific questions:

When 504 belongs in the conversation

A 504 loan generally enters the picture when a larger FedEx contractor is buying or improving owner-occupied real estate, such as an operations facility, yard, or warehouse tied to the business. That's a different objective from buying routes. If your main goal is acquiring an operating route business, spending time chasing 504 options usually just slows the process.

This can be understood as follows:

- Use 7(a) when the center of the deal is the business acquisition.

- Use 504 when the center of the deal is owner-occupied commercial real estate.

- Use both only with careful structuring when the transaction has more than one major component and the lender can support that complexity.

The mistake I see most often is buyers mixing the two too early and assuming “SBA” means interchangeable. It doesn't. Program fit matters because the wrong application path creates delays before underwriting even gets serious.

Are You Eligible for a FedEx SBA Loan

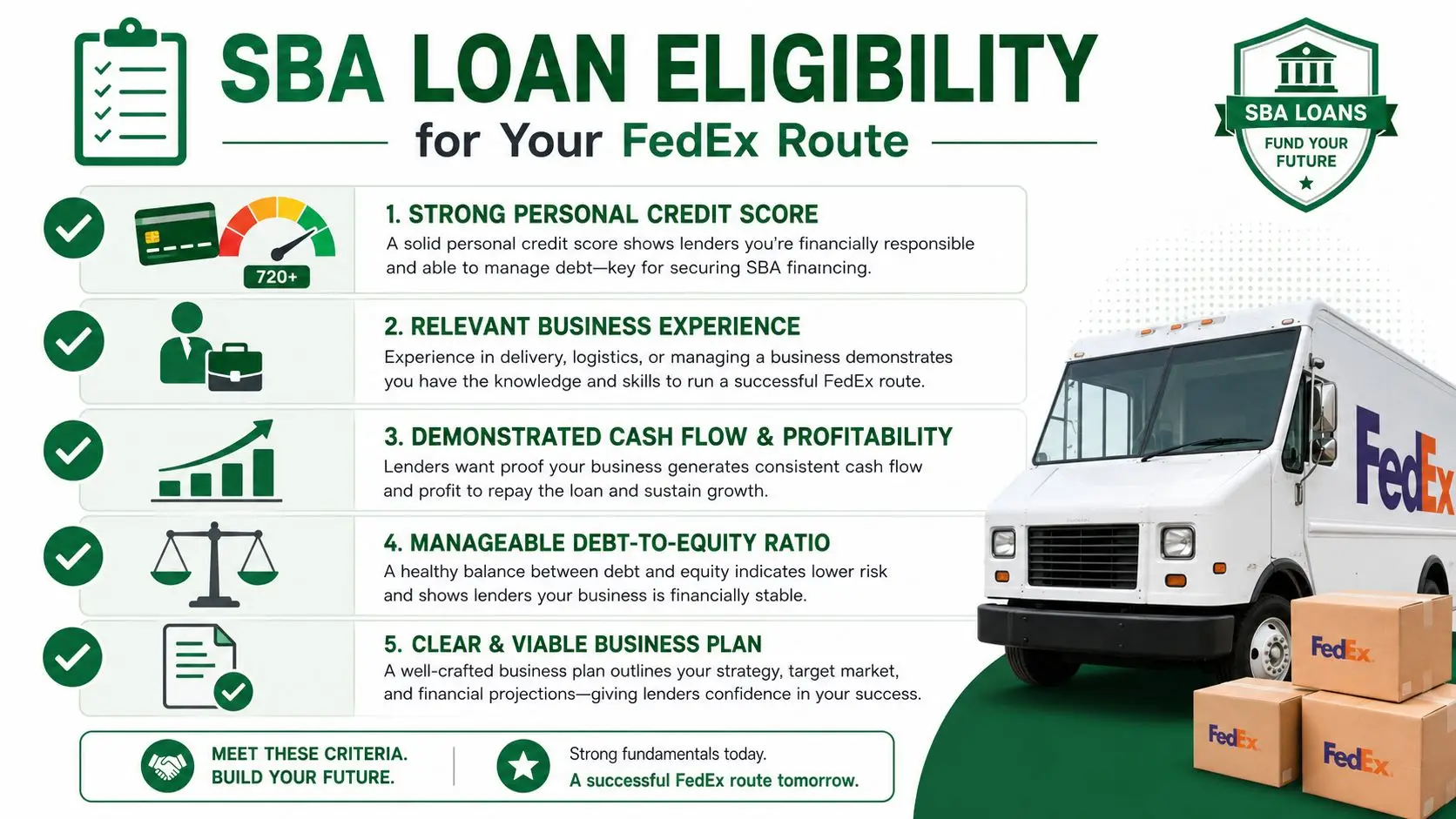

Eligibility is where most online advice gets too soft. A route may be SBA-financeable in theory, but lender approval usually turns on issues that are much more specific than the usual checklist of “good business, good credit, good opportunity.”

Liquidity is usually the first screen

Before a lender debates your projections, it looks at your cash position and your source of funds. That's where many applications weaken. According to Route Consultant's preparation guidance for SBA lending, approval often depends on a meaningful equity injection of 10% to 30% of the purchase price, and some lenders also want at least 10% liquid reserves post-closing.

That changes how you should think about qualification. The main issue often isn't whether the route counts as an SBA-eligible business. The issue is whether you can close the deal and still have enough liquidity left to operate responsibly.

Here's what lenders are really testing:

- Your equity injection. They want to know how much of your own capital is going in and whether it is documented cleanly.

- Your reserves after closing. Running too lean makes the file harder, especially in a business with fleet and labor exposure.

- Your source of funds. Unclear transfers, borrowed down payments, or poorly documented gifts create avoidable friction.

If you have just enough cash to close and nothing left to absorb normal operating surprises, many lenders will pass even if the route itself looks solid.

Experience and planning decide the harder files

The second filter is management credibility. Lenders want to see who will oversee drivers, vehicles, compliance, scheduling, and transition risk. Direct route ownership experience helps, but it isn't the only way to build a strong file. Transferable operating experience, team leadership, logistics management, and prior business ownership can all matter if they're explained properly.

A thin business plan is where many otherwise qualified buyers lose momentum. For FedEx route deals, the plan needs to answer practical questions:

- Who runs the operation daily?

- How will driver coverage be handled during the transition?

- What assumptions support revenue and expense expectations?

- What happens if maintenance or payroll timing creates early pressure?

The better files read like an operating memo, not a school assignment. They don't oversell. They show the lender that the buyer understands what can go wrong and has a sensible plan for handling it.

Required Documents for Your Loan Application

FedEx route loans don't die because the concept is wrong. They usually stall because the file is incomplete, inconsistent, or assembled too late. Documentation quality affects both lender confidence and speed.

According to Capital Bank's checklist for financing a FedEx route, lenders require three years of financial projections, with the first year broken down month by month and the next two years annualized. The same guidance notes the need for written assumptions, three prior years of business tax returns for both buyer and seller, interim business financial statements from the seller, and management experience detailed in the business plan.

What buyers need to produce

The buyer side of the file should be organized before the lender asks for it twice. A clean package shortens the back-and-forth and reduces the chance that an underwriter starts questioning your readiness.

Use this as a working checklist:

- Personal financial statement that clearly shows assets, liabilities, and outside income.

- Tax returns for the required prior years.

- Business plan that explains operating strategy, management background, and transition execution.

- Financial projections for the required three-year period, including the monthly first year and written assumptions.

- Affiliate information if you own a significant stake in other businesses and the lender asks for related records.

If you want a broader preparation guide, this SBA loan document checklist is a useful reference point.

What lenders need from the seller

Seller documentation matters just as much because the lender is underwriting the historical business you're buying. Missing seller records can slow the file even when the buyer is fully prepared.

Expect requests for:

- Historical business tax returns for the required prior period.

- Interim financial statements to show current performance.

- Purchase documents, especially if seller financing is involved.

- Supporting exhibits that clarify the transaction structure and what is included in the sale.

For buyers who haven't gone through a business acquisition before, it can help to compare the rhythm of underwriting with a structured consumer lending workflow. This overview of the mortgage loan application process is useful because it shows how documentation, verification, and condition clearing often move in stages. The paperwork is different, but the discipline is similar.

Clean documents don't guarantee approval. Messy documents can absolutely cost you one.

Real-World FedEx SBA Loan Scenarios

A FedEx SBA loan starts to make sense when you can see how the structure behaves in a real deal. The key numbers that matter here are the ceiling and the financing structure. According to Route Consultant's SBA financing overview, the SBA 7(a) loan has a strict $5 million aggregate exposure cap per borrower, most route-business loans average about $214,034, and the loan typically covers up to 90% of cost with a 10% down payment, fully amortized over 10 years with no balloon payment.

Scenario one for a first-time route buyer

A buyer targets a single route business priced at a level that fits comfortably within normal SBA lending patterns. The borrower brings the required equity injection, keeps additional cash available for operating needs, and buys a business with clean financials and a solid fleet.

The file tends to work when these pieces line up:

- The down payment is fully documented and sourced cleanly.

- The projections are conservative and tied to actual route operations, not optimistic assumptions.

- The buyer can explain management coverage from day one after closing.

This is the kind of transaction lenders usually understand best. It's simple enough to underwrite, but still demanding enough that weak liquidity or vague planning can derail it.

Scenario two for a portfolio-minded operator

A more experienced buyer may pursue multiple routes or a larger operating company. Here, the discussion changes. The borrower still needs to satisfy the basic structure of the SBA loan, but the larger issue becomes concentration and the borrower's total borrowing exposure under the program.

That's where the $5 million aggregate cap becomes more than a technical detail. It creates a hard limit for buyers trying to scale through repeated acquisitions. A lender may like the business and still need to examine whether the borrower is approaching that ceiling, how the current operation is performing, and whether additional routes increase operational risk faster than management capacity.

A larger route file also gets more sensitive to structure choices such as seller participation, transition planning, and how much working capital remains after closing.

Bigger isn't always harder because of size alone. It's harder because every weakness in management depth, cash reserves, and transition planning becomes more visible.

In practice, the strongest larger acquisitions are the ones where the borrower treats underwriting like due diligence on themselves, not just due diligence on the seller.

Your Next Steps to Secure Financing

The fastest way to waste time on a FedEx SBA loan is to start with lender shopping before your deal package is ready. In this market, route financing still gets done, but lenders are paying closer attention to the business model, the borrower's liquidity, and the downside if route cash flow gets disrupted.

Industry commentary summarized by Route Tycoon's discussion of SBA loans for FedEx routes points to a more cautious lending environment around route economics. That same guidance also highlights an issue buyers need to understand early: because route businesses may not have enough hard collateral, borrowers often need to pledge personal assets, and expert help can improve structure and reduce the chance of avoidable problems in a purchase, start-up, or refinance.

What to do before you apply

Start with your own file, not the seller's pitch deck.

- Pull together your personal financials so you know exactly what funds are available and how they'll be documented.

- Review the seller's historical records early so you can spot weak reporting, inconsistent margins, or fleet issues before underwriting does.

- Draft a route-specific business plan that addresses operations, staffing, transition, and risk management.

If any one of those pieces is weak, fix it before you circulate the deal. A rushed submission rarely saves time.

What works better than shopping blindly

Route lending is specialized enough that lender fit matters almost as much as borrower fit. Some lenders are open to these deals. Some are cautious. Some will technically review them but create enough friction that the transaction loses momentum.

A good process usually looks like this:

- Confirm that the target business is financeable in structure, not just attractive on summary.

- Build the loan package around lender questions, especially liquidity, reserves, and operating control.

- Match the deal to lenders that understand route acquisitions instead of pushing a generic business acquisition file everywhere.

- Stay responsive during underwriting because condition clearing often determines whether timing holds.

The buyers who close cleanly usually aren't the ones with the flashiest story. They're the ones who can document their cash, explain their operating plan, and stay disciplined when underwriting starts pressing on details.

If you're buying a route and want help structuring the financing the right way, GoSBA Loans can help you compare lenders, build a stronger package, and manage the process from LOI through closing at no cost to the borrower.