Some SBA loans can be approved in days, but the full process from application to funding typically takes 60 to 90 days. The reason this answer confuses so many borrowers is simple: the timeline changes a lot based on the loan program you choose, the complexity of the deal, and how prepared you are before underwriting even starts.

That last factor matters more than most first-time borrowers realize. A standard SBA 7(a) or 504 file doesn't move slowly just because lenders drag their feet. It slows down when documents arrive in pieces, when real estate diligence starts late, or when a borrower mistakes “approval” for “money in the account.” The SBA SOP is the right baseline for understanding the rules, but in practice, speed comes from execution. Clean package in, clean process out.

If you're asking how long does an SBA loan take, the useful answer isn't one generic number. It's a timeline by loan type, then by stage, then by the avoidable mistakes that add weeks.

Table of Contents

- The Real Answer to Your SBA Loan Timeline Question

- SBA Loan Timelines by Program Type

- The SBA Loan Process from Application to Closing

- Common Bottlenecks That Can Delay Your Funding

- Your Document Checklist for a Faster Approval

- How to Accelerate Your SBA Loan Timeline

- Frequently Asked Questions About SBA Timelines

The Real Answer to Your SBA Loan Timeline Question

For a standard SBA loan, a typical timeframe is 60 to 90 days from application to funding, especially for common 7(a) transactions, as noted by SmartBiz on the SBA loan timeline and application process. That's the number most borrowers hear, and it's directionally right.

But it hides the issue. SBA lending is not one product with one timeline. An Express loan can move far faster. A 504 project with real estate and third-party reports can take much longer. A clean working capital file and a layered acquisition with multiple owners should never be expected to move at the same pace.

What determines the timeline

Three variables drive almost every SBA closing calendar:

- Loan program: Express, standard 7(a), and 504 work differently. Delegated authority, CDC involvement, and collateral requirements all change speed.

- Deal complexity: Working capital is usually simpler than owner-occupied real estate. Acquisitions can also slow down when the seller's records are incomplete.

- Borrower readiness: A lender can only underwrite what it has. Missing returns, unsigned forms, stale financials, and unclear use of proceeds force rework.

Practical rule: The fastest SBA files aren't the ones with the most aggressive closing target. They're the ones where the borrower delivers a complete, lender-ready package the first time.

Borrowers often assume lender speed is the main lever. It isn't. Lender choice matters, but preparedness matters more. When a lender asks for clarification and gets it the same day, the file keeps moving. When requests sit for days and come back partially answered, underwriting resets its review.

The right mindset is to treat SBA financing like a transaction process, not a simple online loan application. If you approach it that way, the timeline starts to make sense. What's more, it becomes manageable.

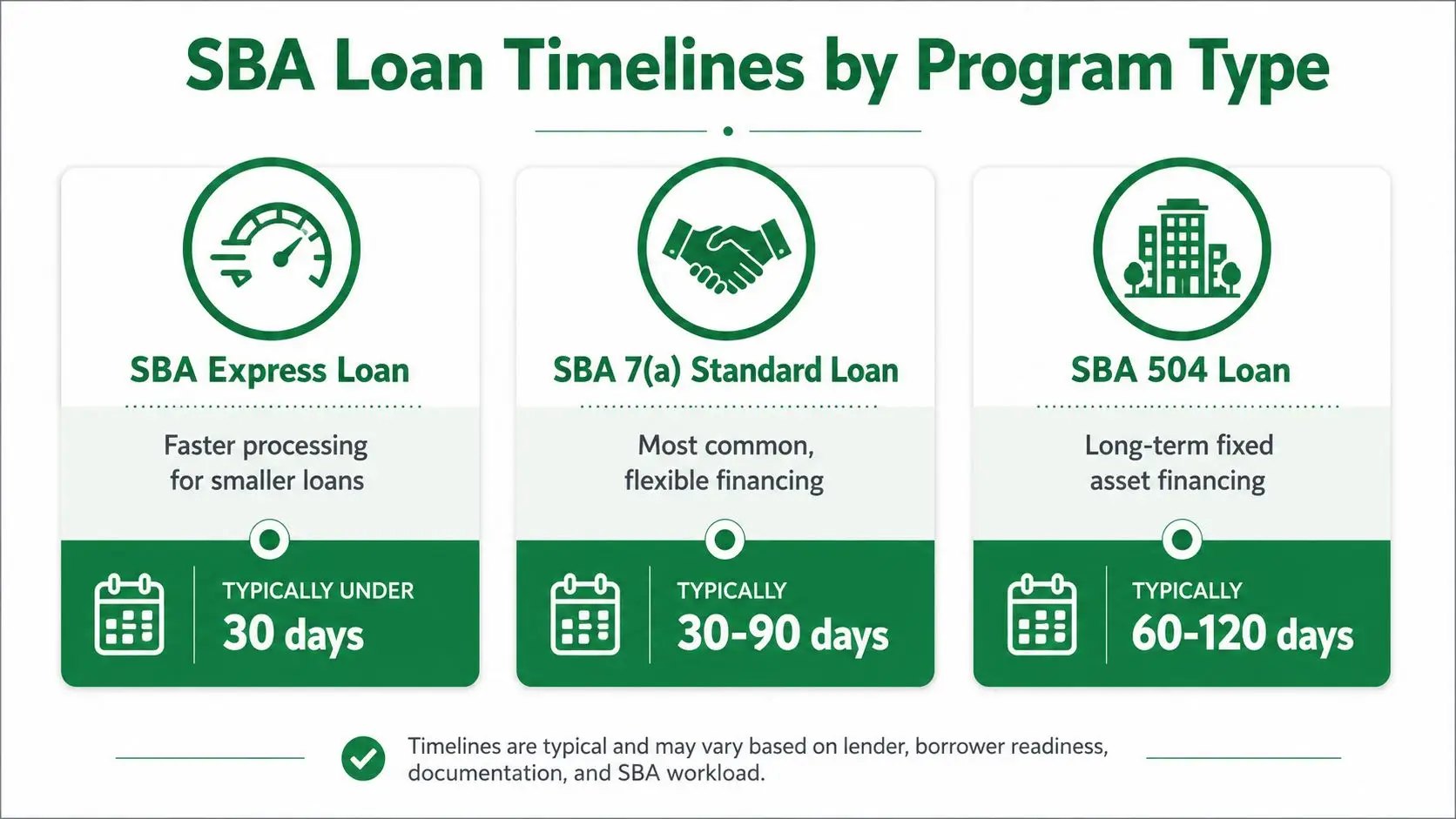

SBA Loan Timelines by Program Type

A borrower asking how long does an SBA loan take is really asking two questions. Which SBA product fits the need, and what trade-off comes with that choice?

Why program choice changes the clock

SBA Express is built for speed. The SBA decision can come in as little as 36 hours, which is a major break from the normal pace of traditional SBA processing, according to Crestmont Capital's summary of SBA Express approval timing. That speed exists because Express lenders use delegated authority and avoid the slower standard review path.

That doesn't mean every Express borrower has cash in hand immediately. Even fast products still require lender underwriting, documentation, and closing steps. But if urgency matters, Express is the first program worth examining. For a deeper side-by-side breakdown, compare SBA Express vs. standard 7(a) loan options.

Standard SBA 7(a) is the workhorse program. It's flexible and widely used for acquisitions, partner buyouts, refinancing, and working capital. The trade-off is that it usually moves slower than Express, especially when the lender doesn't have the authority or internal process to compress review.

SBA 504 is excellent for owner-occupied commercial real estate and fixed assets, but it is not the program to choose when speed is the top priority. The structure itself adds friction. You have a bank, a CDC, the SBA component, and property-level diligence.

SBA loan program timelines compared

| Loan Program | Typical Time to Fund | Key Factors |

|---|---|---|

| SBA Express | Typically under 30 days | Fast SBA decision, delegated authority, smaller and time-sensitive uses |

| SBA 7(a) Standard | Typically 30 to 90 days | Flexible use of proceeds, lender process, underwriting depth |

| SBA 504 | Typically 60 to 120 days | Real estate diligence, CDC coordination, appraisal and collateral review |

A few practical takeaways matter here.

- Choose Express when speed matters most: It's designed for urgent capital needs and can be the best fit when timing outranks flexibility.

- Choose 7(a) when the structure matters more than raw speed: This is often the best option for business acquisitions and broader financing needs.

- Choose 504 when you're financing fixed assets and can tolerate a longer path: The long-term structure is strong, but the closing process isn't the fastest lane.

The words "SBA loan" make these products sound interchangeable. They aren't. The structure you pick can change the funding calendar by weeks or longer.

This is why first-time borrowers get frustrated. They hear that SBA approval is fast in one article and that SBA lending takes months in another. Both can be true, depending on the product and what stage the writer is discussing.

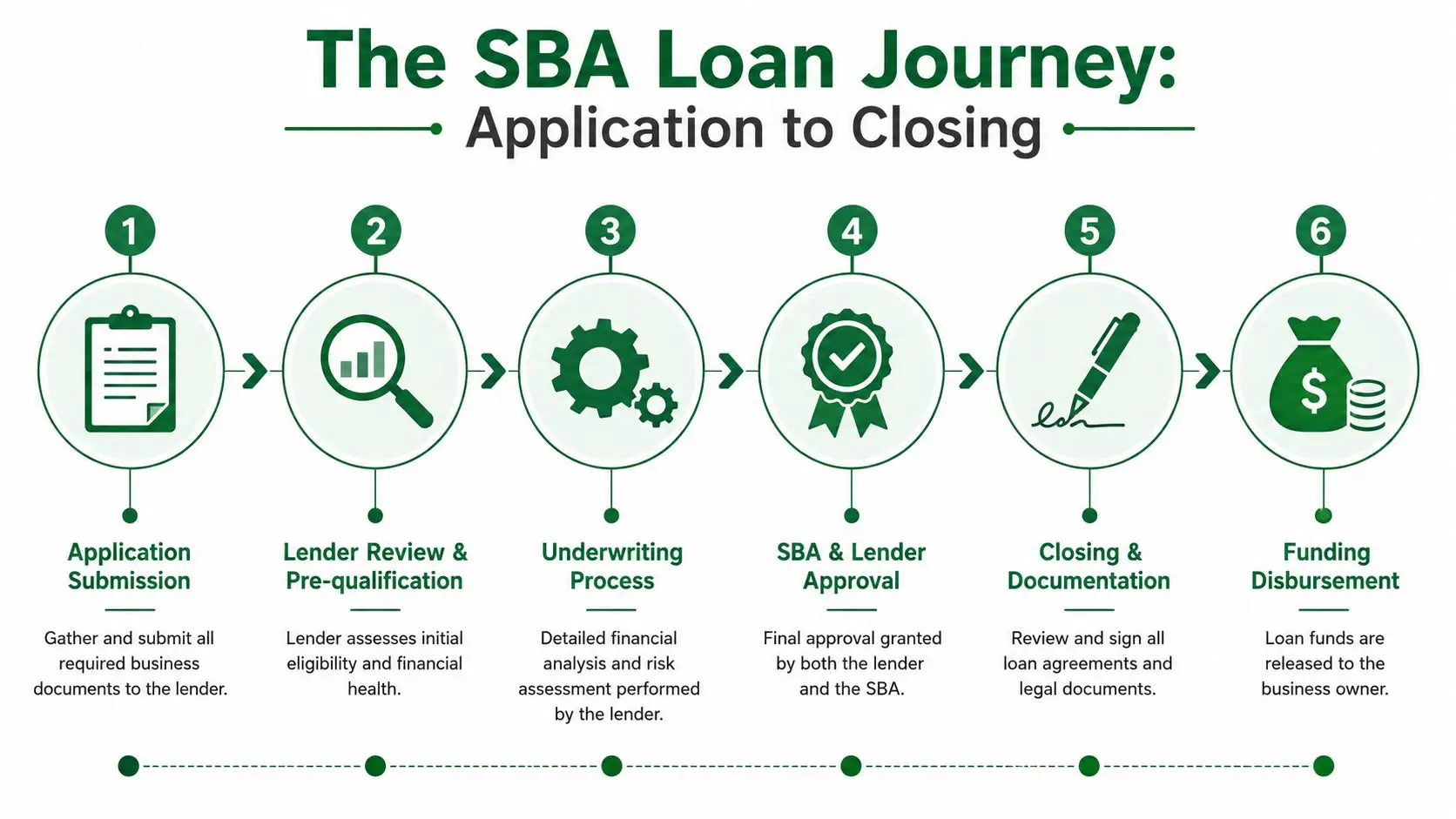

The SBA Loan Process from Application to Closing

Roughly two-thirds of the SBA timeline is usually spent before money hits your account. Borrowers who only track the approval date miss the stages that consume the most time.

Where the time goes

The better way to judge an SBA timeline is by stage, not by one headline estimate. In practice, the process usually breaks into four parts: application packaging, underwriting, approval with conditions, and closing. A fast file moves through each handoff cleanly. A slow file stalls because one stage was incomplete and the problems surface later.

Application packaging

This stage includes tax returns, interim financials, ownership details, debt schedules, resumes, and any transaction-specific items. For an acquisition, that can include the purchase agreement, seller financials, and lease details. For real estate, it often expands to property information and occupancy questions. If the package is thin or inconsistent, the file enters underwriting with built-in delays.Underwriting

The lender reviews cash flow, global debt coverage, credit, collateral, management experience, and SBA eligibility. At this stage, underwriters test whether the story holds together on paper. If revenue trends, add-backs, ownership structure, or use of proceeds are unclear, the lender starts issuing follow-up requests. Every round of questions adds days.Approval and commitment

Credit approval is a milestone, not the finish line. The lender issues a commitment or approval letter with conditions that still must be cleared. Those conditions often include updated financials, proof of equity injection, entity documents, insurance, franchise or lease review, and third-party reports.Closing and funding

Closing turns an approved file into funded dollars. Attorneys, title companies, landlords, insurance agents, and sellers may all have open items at this point. That is why a borrower can be fully approved and still be weeks away from funding.

The files that close fastest are usually not the ones with the easiest businesses. They are the ones with a clean package, quick borrower responses, and a lender or broker who catches problems before underwriting sees them.

If you're buying a business, this step-by-step guide to from LOI to closing in an SBA business acquisition shows how the timeline expands once a transaction has a seller, lease, and diligence workstream attached to it.

A short visual can help if you prefer to see the sequence laid out step by step.

Approval is not funding

First-time borrowers confuse these terms all the time. Approval means the lender is willing to make the loan if the remaining conditions are satisfied. Funding happens after those conditions are cleared and the closing documents are signed.

That distinction matters in real deals. I regularly see borrowers tell a seller or landlord, "We're approved," when what they mean is, "Credit signed off, but closing still needs title, insurance, entity documents, and final source-of-injection proof." Those are very different positions.

If you're trying to time payroll, inventory, or a closing with a seller, the funded date is the date that matters.

This gap between approval and funding gets wider in loans tied to real estate, lease assignments, landlord consents, life insurance, environmental reports, or business acquisitions with multiple parties involved. None of that means the loan is off track. It means the process has shifted from credit risk review to condition clearing and document control.

The practical takeaway is simple. Preparation gets the file into underwriting. Underwriting gets the file approved. Closing gets the loan funded. Borrowers who understand those handoffs make better decisions, respond faster, and avoid promising a closing date before the file is ready.

Common Bottlenecks That Can Delay Your Funding

Most SBA delays are not mysterious. They usually fall into two buckets: borrower-side delays and transaction-side delays.

The delays borrowers can control

The first and most common problem is incomplete documentation. A lender asks for tax returns and gets one year instead of the full package. It asks for current financials and receives statements that are out of date. It asks one ownership question and gets a partial answer. Each gap creates another turn in the cycle.

Slow communication is the second problem. SBA files move best when the borrower treats lender requests like closing items, not casual admin tasks. Same-day responses keep the file live. Delayed responses push it behind newer files in active underwriting queues.

A third issue is changing the story midstream. Borrowers revise use of proceeds, restructure ownership, add guarantors, or change the target property after review has started. Sometimes those changes are necessary. But every major change creates new review work.

Borrowers don't usually lose time because one document is hard to find. They lose time because the file keeps changing while the lender is trying to finalize it.

The delays tied to the deal itself

Some delays come with the transaction, not the borrower. Real estate is the clearest example. Complex real estate transactions often take 60 to 120 days from application to funding because appraisal reviews and collateral evaluations add time, according to AOFund's explanation of SBA real estate loan timing.

That matters because many borrowers compare a working capital loan timeline to a property-backed transaction and assume they should move the same way. They won't.

Other common friction points include:

- Third-party reports: Appraisals, business valuations, environmental reviews, and title work don't move on your desired closing date. They move when vendors complete them.

- Seller cooperation: In acquisition deals, lender questions often require seller financials, lease details, or operational clarifications.

- Legal and landlord items: Lease assignments, estoppels, and entity clean-up can drag out the final stretch.

These problems are frustrating, but they're not random. Once you know where delays happen, you can start managing them early instead of reacting late.

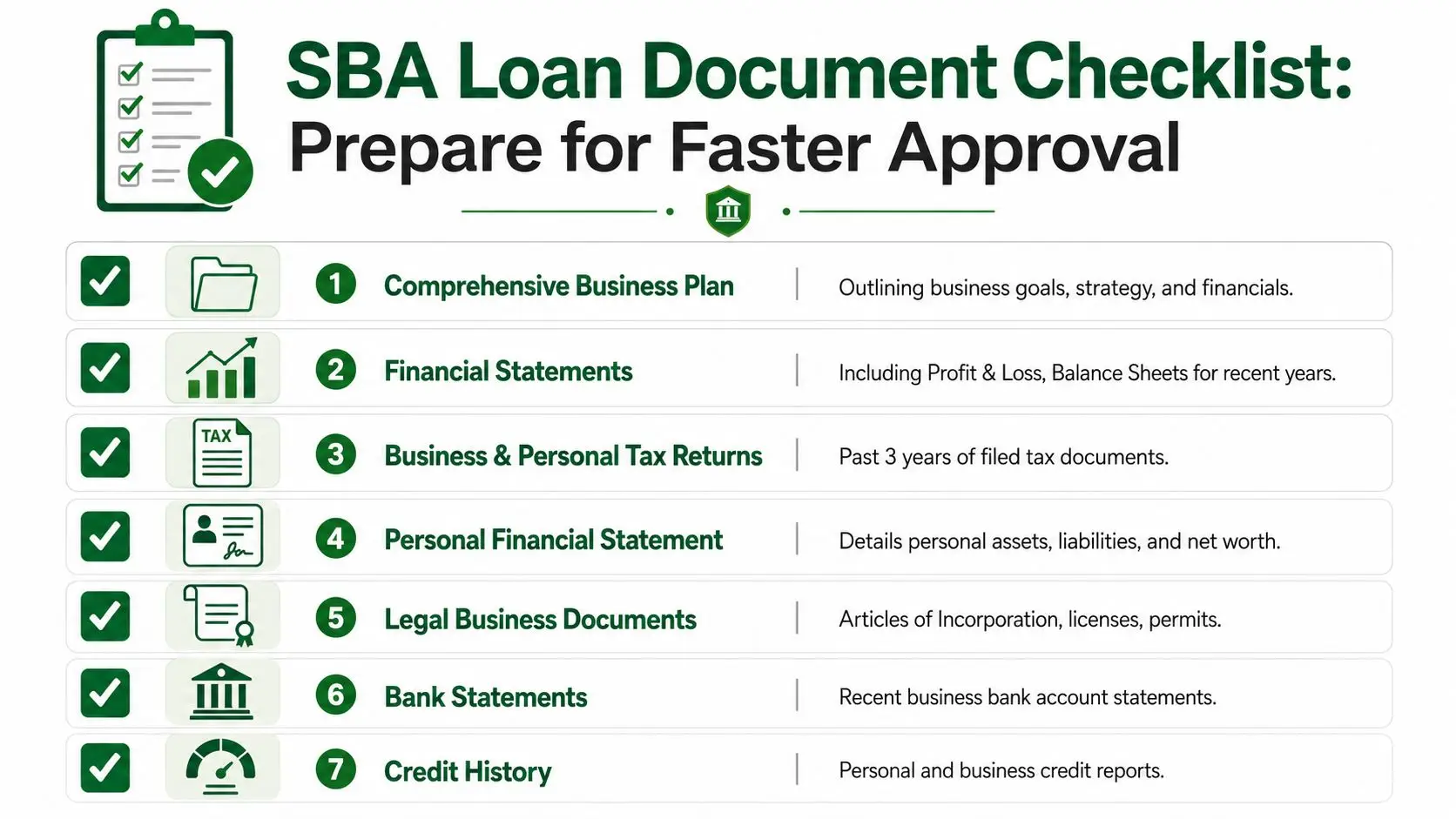

Your Document Checklist for a Faster Approval

The fastest way to shorten an SBA timeline is simple. Show up organized.

What to gather before you apply

A lot of content says SBA loans take 60 to 90 days, but misses the biggest driver: the preparation phase often takes 30+ days while borrowers collect 3 years of tax returns, interim financials, and organizational documents, making readiness the dominant variable, as explained by Capital Bank's overview of the SBA loan process.

That means your checklist isn't busywork. It's your speed strategy.

Start with the core file:

- Business and personal tax returns: Lenders want a complete picture, not selected pages.

- Current interim financials: Profit and loss statement, balance sheet, and sometimes receivables or payables support.

- Personal financial statement: This needs to be current and internally consistent.

- Business debt schedule: Include lender names, balances, payment amounts, and maturity structure.

- Entity documents: Articles, operating agreement, stock ledger if applicable, licenses, and formation records.

- Bank statements: Recent business account statements help confirm operating activity.

- Deal documents: Purchase agreement, LOI, lease, franchise papers, or property details when relevant.

If you want a lender-ready worksheet to organize this file, use an SBA loan application checklist built for borrowers.

How organized documents speed up underwriting

Good packaging doesn't just help the lender. It reduces preventable back-and-forth. If one signer is constantly traveling or slow to return forms, even basic paperwork can become a bottleneck. For forms that require signatures, it helps to learn to sign W9s with SignWith so tax paperwork doesn't become an unnecessary delay.

A few practical habits make a real difference:

- Use one shared folder: Keep labeled PDFs in a single place instead of emailing attachments in batches.

- Name files clearly: "2024 business tax return signed" is better than "scan_04."

- Check date consistency: Mismatched dates across returns, P&Ls, and debt schedules trigger extra questions.

- Submit complete answers: When a lender asks one question, check whether two related documents should be updated too.

A clean package signals that the borrower is serious, organized, and less likely to create surprises in closing.

Experienced borrowers distinguish themselves from first-timers. They don't wait for the lender to build the file for them. They deliver a file that's already close to underwriteable.

How to Accelerate Your SBA Loan Timeline

Borrowers usually focus on lender speed. In practice, the faster files are the ones that enter underwriting clean, stay consistent, and get placed with the right lender the first time.

What works

Pick the right loan lane early. The biggest time savings often happen before you submit anything. A straightforward working capital request, an equipment purchase, and an owner-occupied real estate deal do not belong in the same process lane. Match the transaction to a lender that handles that exact deal type often and has delegated authority when available. That cuts avoidable review time and lowers the odds of a late-stage handoff.

Respond the same business day. Underwriting delays usually come from small missing items, not one dramatic problem. A stale bank statement, an unsigned form, or an unexplained deposit can stall a file for days if nobody answers quickly. Fast replies keep your file active in the underwriter's queue.

Start third-party work as soon as the lender gives the green light. Appraisals, title, insurance, lease review, and franchise approval can move on their own timeline. If your deal includes real estate or a business acquisition, those items should not wait until credit approval is fully wrapped up unless the lender specifically tells you to hold.

Keep the structure stable. Midstream changes slow everything down. If ownership percentages change, the seller note gets revised, or the use of proceeds shifts, underwriting usually has to revisit the file. Sometimes legal documents have to be redrafted too.

Use a broker who packages SBA loans every week. This is one of the few real shortcuts. A good broker does more than introduce you to lenders. They pressure-test the deal, flag weak spots before submission, place it with a lender that suits the file, and keep underwriting and closing from drifting. That saves time because fewer avoidable issues make it into the process.

What slows files down

Submitting partial packages to multiple lenders is a common mistake. Borrowers think they are creating competition. What they usually create is duplicate work, inconsistent explanations, and conflicting document requests. Then they spend a week answering the same question three different ways.

Another delay starts with an unrealistic purchase contract deadline. Closing dates do not speed up appraisals, title work, insurance changes, or SBA eligibility review. A serious deadline only helps when the borrower, lender, broker, seller, and closing parties are already aligned on documents and next steps.

I see one pattern repeatedly. First-time borrowers assume approval speed is mostly about the lender. It is not. Prepared borrowers and experienced SBA packaging teams are usually the biggest drivers of a short timeline.

If you want the shortest realistic path, improve the file quality, choose the right lending channel, and treat every lender request like it affects the closing date. It usually does.

Frequently Asked Questions About SBA Timelines

Can an SBA loan close in under 30 days

Yes, but only in the right circumstances. Express loans can move very fast, and some simple transactions close quickly when the borrower is fully prepared and the lender has authority to move without unnecessary delay. It is possible. It is not the default expectation for a standard SBA file.

Is SBA approval the same as funding

No. This is one of the most misunderstood parts of the process. SBA approval can take 5 to 7 days for 504 loans and 2 to 10 days for 7(a), but the total funding timeline adds 30 to 60 extra days after approval for closing, appraisal, and debenture-related steps, as explained by TMC Financing's SBA 504 timeline guide.

Do business acquisitions and real estate deals move at the same speed

No. Real estate adds appraisal, collateral review, title, insurance, and often more legal coordination. Business acquisitions can also get delayed, but the drag often comes from seller documents, lease issues, or transaction structure rather than property diligence.

Does personal credit affect timeline speed

Yes, indirectly. Weak or complicated credit usually creates more underwriting questions, more documentation requests, and more conditional review. Strong, clean files tend to move with less friction. Credit doesn't determine speed by itself, but it does affect how much work the lender has to do before saying yes.

If you want help turning a messy SBA timeline into a clear funding plan, GoSBA Loans can help you compare lenders, package the file correctly, and move from application to closing with fewer delays. For borrowers buying a business, refinancing debt, or financing owner-occupied real estate, having the right lender match and a complete package upfront can make the process faster and a lot less painful.