You're probably in one of two spots right now. Your lease is getting expensive, or your business has outgrown the space and you're tired of building someone else's equity. Buying the building feels like the smart move, but commercial lending language gets murky fast, especially once people start throwing around “owner-occupied,” “SBA,” “DSCR,” and “down payment” as if they all mean the same thing.

They don't.

The biggest mistake I see is simple. A business owner finds a property, confirms they'll use most of it, and assumes that means they qualify for owner occupied commercial real estate loans. Sometimes they do. Sometimes they don't. The reason is that lenders don't only care about how much of the building you physically use. They also care about what repays the debt.

That distinction changes everything. It affects which loan program fits, how the file is underwritten, what terms you can realistically expect, and whether your deal gets approved or dies late in the process.

Table of Contents

- Understanding Owner Occupied Commercial Real Estate Loans

- Conventional vs SBA 7(a) vs SBA 504 Loan Comparison

- The Underwriting Gauntlet What Lenders Really Look For

- Your Loan Application Timeline and Required Documents

- Critical Mistakes That Get OOCRE Loans Denied

- Secure Better Terms with GoSBA Loans

- Frequently Asked Questions About OOCRE Loans

Understanding Owner Occupied Commercial Real Estate Loans

An owner occupied commercial real estate loan is the business version of buying your own home instead of buying a rental property for someone else. The core idea is straightforward. Your company is buying the property to operate from it, not mainly to collect rent from outside tenants.

That distinction matters because lenders usually treat an owner-user deal differently from an investment-property deal. In an owner-occupied transaction, they're primarily lending against the strength of the business. In an investment-property deal, they focus much more heavily on rent rolls, tenant quality, and property income.

The basic occupancy rule

A foundational rule in U.S. commercial lending is that a property is typically treated as owner-occupied when the business uses at least 51% of the space. A practical example from Sunwest Bank's owner-occupied real estate explanation makes this easy to visualize. If you buy a 5,000-square-foot building, your business would need to occupy at least 2,550 square feet to meet that test.

That's why these properties can work well for companies that need room now but also want flexibility. You can occupy the majority of the building and still lease some excess space, as long as the deal still fits the owner-user framework.

Why borrowers like these loans

The appeal is practical, not theoretical:

- Control over space: You're no longer asking a landlord for permission to improve the property.

- Long-term stability: You reduce lease-renewal risk and the disruption that comes with forced moves.

- Potential financing advantages: Owner-user lending is often more accommodating than investment-property lending because the business itself supports the loan.

Practical rule: Don't evaluate the building first and the loan second. Evaluate whether the property fits owner-user rules before you get emotionally attached to it.

A lot of borrowers reverse that order. They negotiate hard on price, line up contractors, and sketch out renovation plans before confirming whether the property qualifies under the program they want.

What lenders are really trying to determine

Lenders want to know whether the property is part of your operating business or mainly a real estate investment. That's the dividing line. If the building is the place your company earns revenue, owner occupied commercial real estate loans can be one of the strongest financing tools available. If the property is really a rental play with your business as a partial occupant, the lender will likely underwrite it very differently.

That's where many applications go off course. The physical occupancy rule is only the starting point. The financial side of the deal matters just as much, and in many files it matters more.

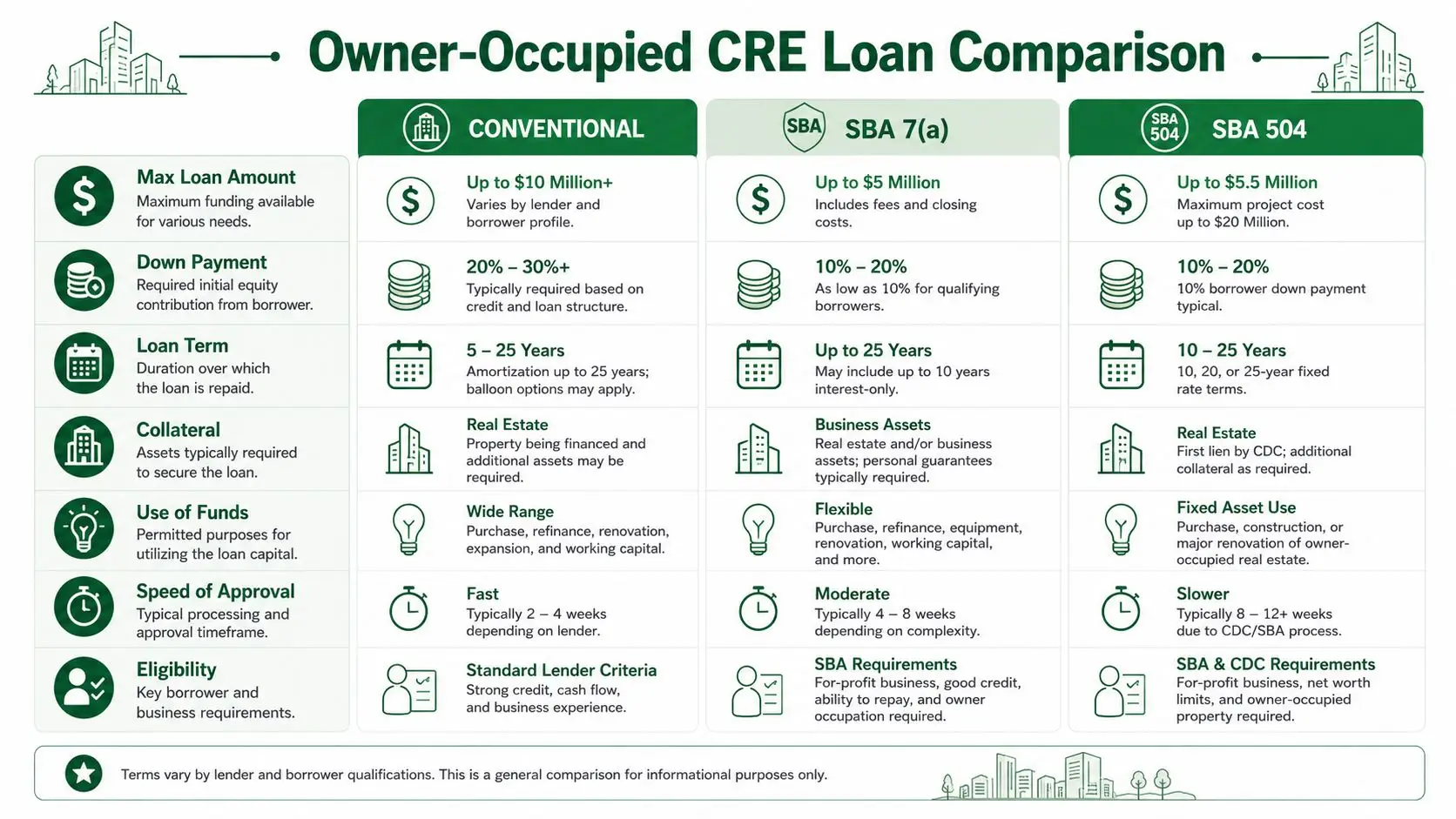

Conventional vs SBA 7(a) vs SBA 504 Loan Comparison

A borrower finds a building that fits the operation, agrees on price, and assumes the loan choice is just about rate and down payment. That assumption causes problems. The right program depends on two separate tests. How much of the property the business will occupy, and what source of cash flow will repay the debt. A file can satisfy the occupancy rule and still fail because the repayment story does not fit the loan structure.

A quick comparison

| Loan type | Best fit | Down payment profile | Term profile | Main strength | Main limitation |

|---|---|---|---|---|---|

| Conventional | Established businesses with strong global cash flow, liquidity, and a clean credit story | Usually higher borrower equity than SBA structures, with bank policy driving the exact requirement | Often shorter fixed periods or balloons, with amortization and reset risk depending on the lender | Faster, simpler bank execution for strong files | Less tolerance for weaker DSCR, limited liquidity, or unusual occupancy and use-of-proceeds issues |

| SBA 7(a) | Deals that combine real estate with other business needs, or borrowers who need more structural flexibility | Often lower equity than conventional, but borrower injection still matters and can rise with risk factors | Long repayment terms are available for owner-occupied real estate | Flexible use of proceeds and broader problem-solving ability | More documentation, guaranty fees, and tighter scrutiny around affiliate debt and repayment sources |

| SBA 504 | Businesses buying or improving a property they will occupy long term | Lower equity is possible for eligible projects, especially compared with many conventional loans | Long-term financing designed for fixed assets | Strong fit for real estate and equipment projects where payment control matters | Narrower use of proceeds than 7(a), and the structure is less helpful if the deal includes working capital or business acquisition needs |

For a more detailed look at program structure, eligible uses, and how each option is typically set up, review this guide to SBA real estate loans for commercial property financing with SBA 7(a) and 504.

Conventional loans fit the cleanest files

Conventional financing works well when the borrower already looks strong on paper and does not need SBA help to make the deal work. Banks like these loans when the business has stable earnings, good post-closing liquidity, and a property that clearly supports the operating company.

The trade-off is flexibility. A conventional lender may like a borrower who occupies the right amount of space, then still decline the deal because too much repayment strength depends on tenant rent, a recent dip in margins, or a balloon structure that creates refinance risk later. The occupancy test gets the file in the door. The repayment test gets it approved.

SBA 7(a) solves mixed-purpose deals

SBA 7(a) is often the right tool when the transaction is not just a real estate purchase. It can cover a building, closing costs, limited improvements, equipment, and in some cases business acquisition components, depending on how the deal is structured.

That flexibility helps borrowers who do not fit a bank's standard credit box. It also creates more room for mistakes. I see 7(a) files stall when the borrower focuses on the fact that the company will physically occupy the property but does not clearly show that business cash flow, not projected rent or optimistic growth assumptions, will carry the payment.

SBA 504 is built for long-term owner-users

SBA 504 is usually the strongest fit when the goal is simple. Buy, build, or improve the building the business will operate from and keep more cash in the company.

It is less flexible than 7(a), but better targeted. The program is designed around fixed assets, which is why it can produce a payment profile many owner-users prefer. That matters for manufacturers, medical practices, auto service operators, and other businesses where facility control is part of the operating model, not a side investment.

Property insurance also needs attention early, especially on larger or special-use buildings. Premium changes can affect projected payment comfort more than borrowers expect, so it helps to get insurance input before final term negotiations. Select Insurance Group, Inc. is one example of the kind of specialist borrowers use to evaluate business property coverage during the financing process.

The practical rule for choosing

Choose the program based on the weakness in the deal.

- Choose conventional if the file is strong enough to stand on bank credit standards without SBA support.

- Choose SBA 7(a) if the transaction includes real estate plus other business needs, and the repayment case still comes primarily from operating cash flow.

- Choose SBA 504 if the project is centered on owner-occupied real estate or equipment, and the business wants to preserve cash while spreading repayment over a longer horizon.

The mistake is treating these programs as interchangeable. They are not. One asks whether the bank likes the credit. Another asks whether the SBA structure can support the purpose. All three still come back to the same issue. The business must occupy enough of the property, and the business itself must be the clear source of repayment.

The Underwriting Gauntlet What Lenders Really Look For

A business can meet the occupancy rule and still get declined.

That surprises owners all the time. They hear “owner occupied” and assume the main hurdle is using enough of the building. Underwriting looks at a different question after that. Can the operating company repay the debt from business cash flow, with enough margin to survive a soft quarter, a delayed receivable cycle, or a jump in expenses?

Cash flow decides the file

For most lenders, the center of the credit decision is DSCR, the debt service coverage ratio. In plain terms, they compare the business's available cash flow to the proposed annual loan payments and ask whether there is enough room for error.

That distinction matters because many weak applications mix up occupancy with repayment. A company may plan to use most of the building and still have a thin file if cash flow is inconsistent, adjusted income is hard to support, or the new payment strains the business after payroll, taxes, and existing debt. Owners who want a clearer breakdown should read this guide on what DSCR means for SBA loan approval.

Lenders also look at how the cash flow is built. Stable customer concentration, recurring revenue, and reasonable owner add-backs help. One-time spikes, aggressive adjustments, and messy intercompany transfers do not.

Durability matters more than growth

A fast-growing business is not always an easy approval. Underwriters prefer a company they can understand.

They review tax returns, year-to-date financials, debt schedules, and bank statements to see whether earnings hold up under scrutiny. They want to know whether the move into the property fits the business model, whether occupancy costs stay sensible after closing, and whether the company still has working capital left once the down payment, closing costs, and any buildout are done.

This is also where many borrowers miss the insurance issue. If coverage comes in late, premiums are higher than expected, or the carrier adds conditions on an older or special-use building, the monthly payment picture changes. A practical starting point is this overview from Select Insurance Group, Inc., especially for owners evaluating commercial property coverage before closing.

The guarantor still gets underwritten

Even when the property is clearly owner occupied and the business is the repayment source, the personal guarantor still matters. Lenders look at credit history, liquidity, tax payment history, and whether the owner can explain prior problems clearly.

Three things usually help:

- A clean credit story: Prior issues do not always kill a deal, but unexplained issues create doubt fast.

- Relevant operating experience: Owners with a track record in the same line of business present less execution risk.

- Organized financials: Accurate statements and a consistent narrative make an underwriter's job easier.

I see the same mistake repeatedly. Borrowers spend all their energy proving they will occupy the building, then submit a file that does not clearly prove how the loan gets repaid.

Good files answer both questions. Who uses the property, and what cash flow pays the note. When those two answers line up cleanly, approvals get much easier.

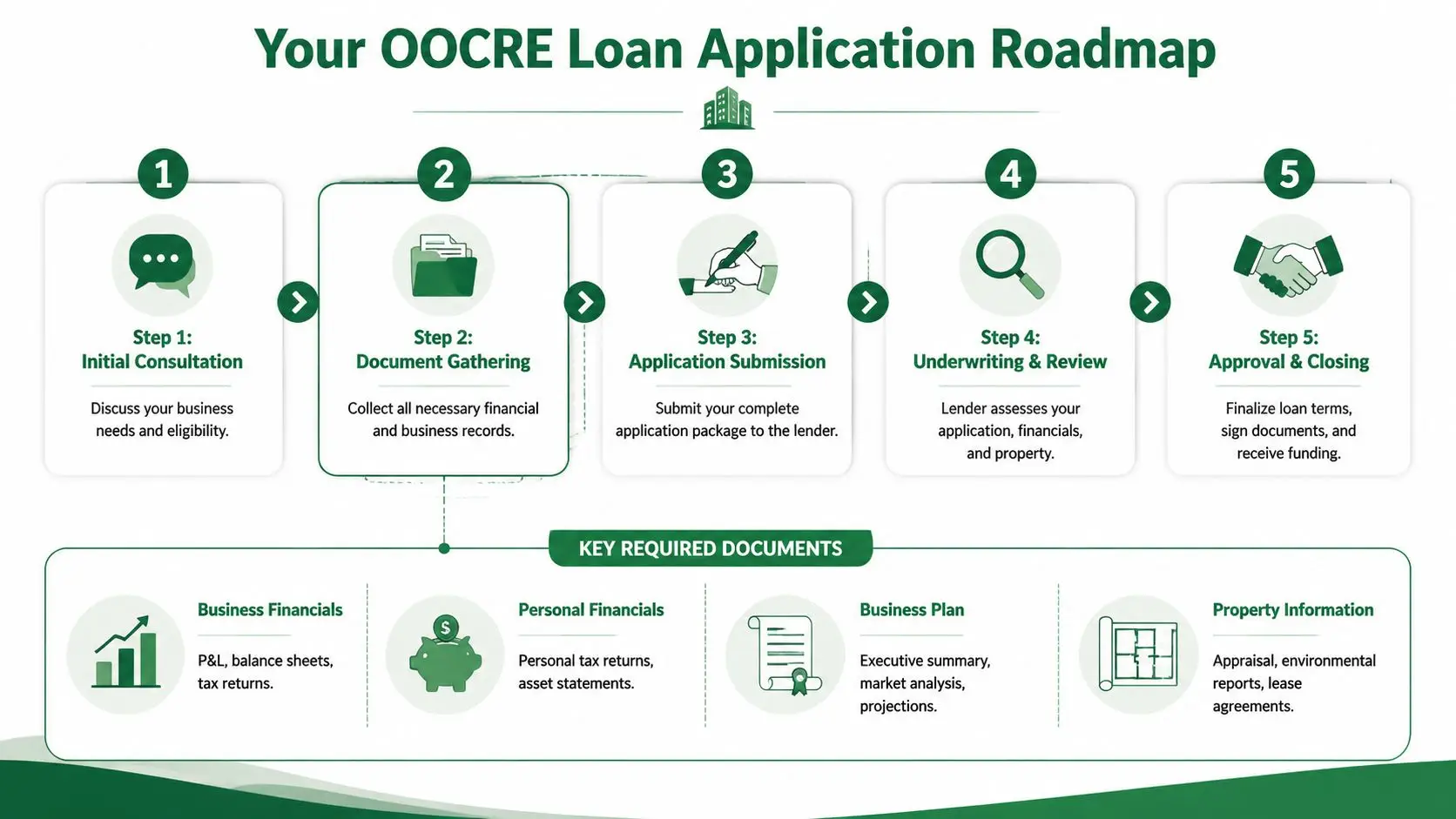

Your Loan Application Timeline and Required Documents

Most owner occupied commercial real estate loans don't fail because the business is unfinanceable. They fail because the borrower submits the wrong file, to the wrong lender, in the wrong order.

This process moves better when you treat it like a transaction checklist instead of a paperwork scramble.

Phase one lender fit and early screening

Start with lender matching, not full submission. Different lenders have different tolerances for industry type, mixed-use properties, partial tenant income, and deal complexity.

Before you apply, gather:

- Business financial statements: Current profit and loss statements and balance sheets

- Tax returns: Business and personal returns for the most recent available years

- Basic property details: Flyer, rent roll if applicable, and purchase contract or letter of intent

- Borrower narrative: A concise explanation of the business, ownership, and why this property fits

If you're still evaluating locations or submarkets, a solid real estate market analysis guide can help sharpen the location logic behind your file.

Phase two underwriting and third party work

Once the application is in, underwriting starts testing the file from multiple angles, with lenders requesting additional documents and ordering third-party reports tied to the property and borrower.

Expect requests for:

- Personal financial statements: A current snapshot of assets, liabilities, and liquidity

- Organizational documents: Articles, operating agreement, ownership breakdown

- Business plan or expansion memo: Especially helpful when the move supports growth or operational change

- Property due diligence: Appraisal, environmental work, leases, and insurance information when required

Phase three approval to closing

Approval doesn't mean you're done. It means the lender is willing to proceed if the closing conditions are satisfied.

Typical closing-stage items include:

- Entity verification: Borrowing entity and ownership must match the approval.

- Final insurance and title work: These often create last-minute delays.

- Cash to close confirmation: The lender wants the source and timing documented.

- Execution package review: Notes, guarantees, and closing statements need to align.

Go into closing with a checklist, not assumptions. This SBA loan closing checklist is a practical resource for that final stretch.

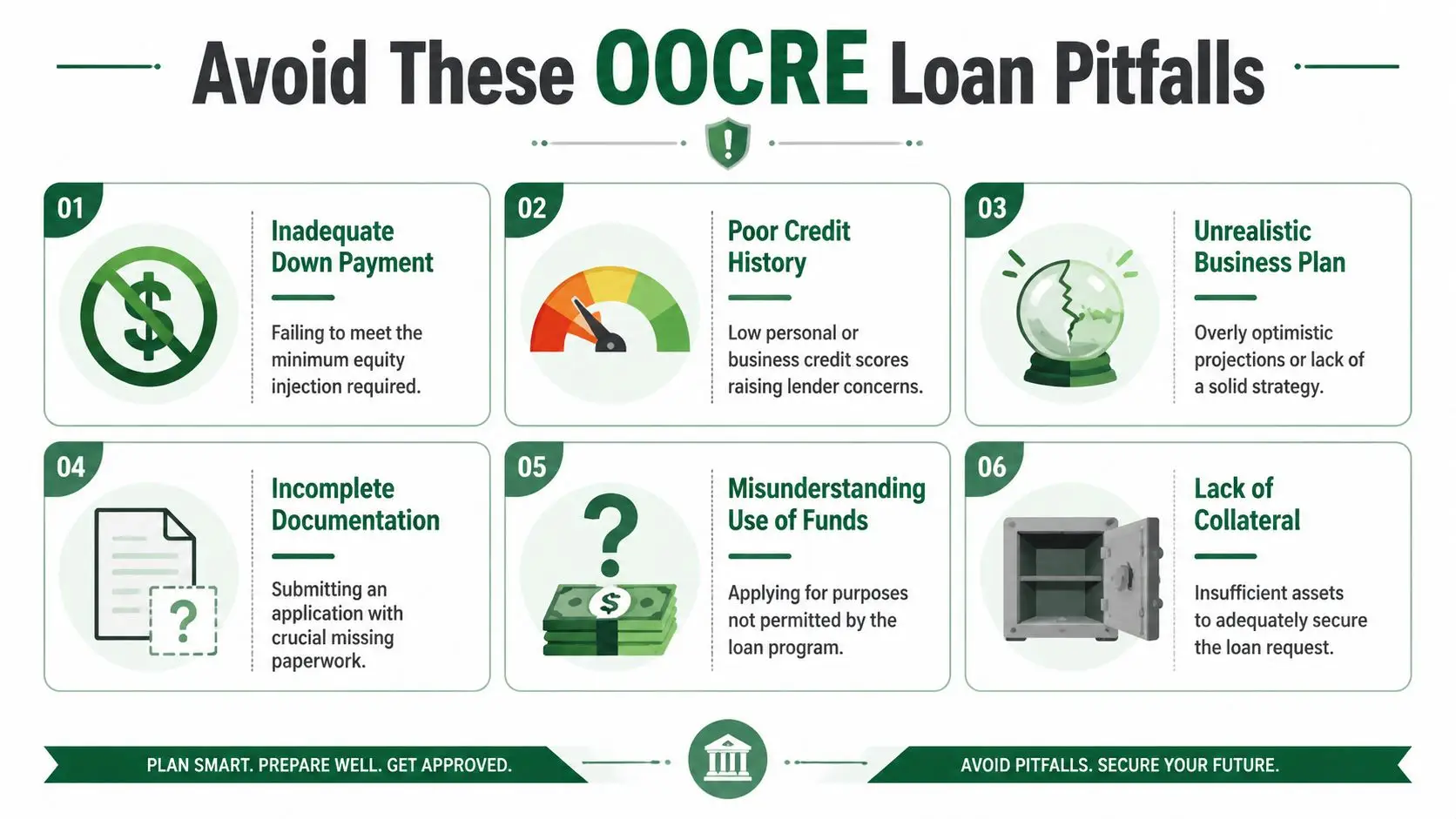

Critical Mistakes That Get OOCRE Loans Denied

Most borrowers often get blindsided. They think they have an owner-occupied deal because they meet the space test, but the lender declines the file because the money coming in tells a different story.

The hardest denials are the preventable ones.

The occupancy trap that catches borrowers

The most misunderstood issue in owner occupied commercial real estate loans is the difference between physical occupancy and repayment source.

A borrower may use enough of the building to satisfy the physical occupancy expectation. That still doesn't guarantee the deal will be treated as owner-occupied for underwriting purposes. As explained by Woodsboro Bank's discussion of owner-occupied commercial real estate, if 50% or more of the repayment source comes from third-party rental income, the OCC's framework classifies the property as non-owner-occupied regardless of physical occupancy percentage.

That rule changes outcomes on mixed-use properties all the time.

If tenant rent is doing too much of the repayment work, the lender may treat the deal like an investment property even when your business occupies most of the building.

Borrowers often run into trouble with office and retail combinations, medical buildings with subtenants, and properties that look owner-user on a floor plan but underwrite like rental real estate on cash flow.

Other mistakes that wreck good deals

Some denials have nothing to do with the property itself. They come from poor preparation.

- Bringing too little cash: Borrowers often focus on the minimum down payment they heard about and ignore the rest of the capital stack. Equity injection, reports, reserves, legal costs, and closing friction all matter.

- Submitting inconsistent financials: If tax returns, internal statements, and bank narratives don't line up, the lender assumes there's more they haven't found.

- Using the wrong loan product: A borrower who needs flexibility may waste time chasing a conventional structure that was never a fit.

- Treating projections like proof: Forecasts can support a deal, but they don't replace demonstrated repayment ability.

- Ignoring tenant impact: Existing leases, rollover risk, and related-party rent need to be framed correctly.

Here's the practical fix. Before you apply, calculate who really pays the debt, organize every financial statement so it tells one coherent story, and choose the program that fits the transaction instead of forcing the transaction into the wrong program.

The video below adds a useful overview of SBA real estate loan pitfalls and planning considerations.

The 100 percent financing question

Business owners ask about full financing all the time. The honest answer is that it's not the standard path, but it can be possible in some SBA 7(a) structures when the equity requirement is satisfied through permitted means such as seller notes on standby or other approved structuring approaches, as discussed in this video covering SBA 7(a) equity substitution concepts.

What doesn't work is building your entire acquisition strategy around a casual promise that “someone can probably get it done.” Heavily financed structures require careful packaging, lender buy-in, and a file that stays clean under scrutiny.

Secure Better Terms with GoSBA Loans

Getting an owner-occupied real estate loan approved is only half the job. The other half is getting the right structure, with the right lender, before a preventable issue costs you time or advantage.

GoSBA Loans is a full-service, no-cost SBA loan brokerage focused on transactions like acquisitions, partner buyouts, working capital, and owner-occupied commercial real estate. Instead of relying on a single bank's credit box, borrowers get access to a network of 50+ SBA lenders and support across packaging, underwriting, third-party reports, and closing coordination.

That matters because many OOCRE deals don't fail for lack of demand. They fail because the file lands with the wrong lender, the occupancy story isn't framed correctly, or the business doesn't present its cash flow the way credit teams need to see it.

GoSBA Loans also brings real execution history. The firm has $320M+ funded and 126+ deals closed, with support for SBA 7(a), 504, Express, small loans up to $350K, refinancing, pari passu structures, seller notes on standby, and investor-heavy capital stacks. Typical timelines average seven days to term sheet and 45–75 days to close.

If you want broader lender reach, stronger packaging, and a cleaner path through underwriting, that's where a specialized SBA brokerage can materially improve the outcome.

Frequently Asked Questions About OOCRE Loans

Can I use an OOCRE loan for new construction

Yes. New construction is financeable under the right program, and SBA 504 is often the first place to look if the building will house your own operations.

The part borrowers miss is that construction adds two approval tests at once. The lender has to get comfortable with the property project, and it also has to get comfortable with the operating business that will repay the debt. A lot of applications get into trouble because the borrower focuses only on future occupancy. The lender also wants a clear repayment source, a realistic budget, and confidence that the business can carry the payment once the project is complete.

Expect more documentation, more third-party reports, and more scrutiny around plans, permits, contractor qualifications, and contingency reserves.

What closing costs and fees should I expect

More than the down payment.

Cash to close usually includes third-party reports, lender and closing charges, insurance, and recording costs. On some deals, borrowers also need to cover interest reserve requirements, interim construction-related costs, or repairs required before funding.

Common expenses include:

- Appraisal and environmental reports: Frequently required before final credit approval.

- Legal, title, and escrow charges: Entity review, title work, settlement services, and loan documents add up fast.

- Insurance: Hazard coverage and, where applicable, flood insurance must usually be active before closing.

- Government filing and recording fees: Smaller line items, but still part of the total cash requirement.

Get a full funds-needed estimate early. Borrowers who budget only for the equity injection are often short at the closing table.

Can I refinance an existing commercial mortgage

Often, yes, but the file has to make sense under current occupancy and cash flow rules.

Refinances work best when they solve a specific problem: lowering a monthly payment, replacing a short-term balloon, pulling debt out of an unsuitable structure, or pairing real estate financing with business needs. The property still needs to qualify as owner-occupied under the applicable program. Just as important, the operating company usually needs to show it can repay the new loan. That distinction matters. Physical occupancy gets the deal into the right loan category. Business cash flow is what usually gets the deal approved or declined.

Refinance requests become harder when the business has changed, the property is no longer used the way it was originally represented, or the debt sits in an entity structure the new lender does not like. I see this often with borrowers who assume, "we use the building, so it should qualify." Lenders go further than that. They want occupancy documented correctly and repayment supported cleanly by business financials.

Borrowers also tend to get better equity requirements on owner-occupied transactions than on pure investment-property loans. That pricing and structure advantage is one reason many business owners try to keep the deal inside owner-user guidelines, but the occupancy story has to be accurate and defensible.

If you're planning to buy, build, or refinance the property your business operates from, GoSBA Loans can help you compare lenders, structure the deal correctly, and avoid the underwriting mistakes that delay or kill otherwise financeable transactions.