You're probably staring at a seller's P&L right now, trying to make the numbers work. The business looks solid operationally. Customers are there. The seller says cash flow is stronger than the tax returns suggest. But the reported net income doesn't seem high enough to support the SBA loan you need.

That gap is where most first-time buyers get stuck.

The fix usually isn't financial engineering. It's understanding SBA add backs well enough to separate real cash flow from owner-specific noise. In SBA acquisition lending, the lender isn't trying to finance a seller's tax strategy, personal perks, or unusual one-off spending. The lender is trying to determine what the business should produce for a new owner after normalizing the books. If you haven't reviewed the broader underwriting standards yet, start with these SBA loan requirements for business acquisitions.

Table of Contents

- Your Guide to SBA Loan Add Backs

- What Are Add Backs and Seller's Discretionary Earnings

- Commonly Allowed vs Disallowed SBA Add Backs

- How to Calculate SDE A Step-by-Step Example

- How Add Backs Directly Impact Your Loan Approval

- Documentation Best Practices and Avoiding Red Flags

- Frequently Asked Questions About SBA Add Backs

Your Guide to SBA Loan Add Backs

A common buyer mistake is taking reported net income at face value.

Say you're reviewing a business that looks healthy on the surface, but the tax return shows modest profit. The seller insists the business throws off much more cash than that because the company paid for owner compensation, some financing costs, and a few unusual expenses that won't continue. Sometimes the seller is right. Sometimes the seller is stretching. The lender has to sort out which is which.

That's why SBA add backs matter so much in acquisition lending. They bridge the gap between reported accounting profit and fundable cash flow. When they're legitimate and documented, they can turn a deal that appears too thin into one that underwrites cleanly. When they're sloppy or aggressive, they can sink a file fast.

A first-time buyer usually thinks the key question is, “What did the business make last year?” An SBA lender asks a different question: “What cash flow will be available to the new owner to service debt after removing expenses that were personal, non-cash, financed, or one-time?”

The goal isn't to make the business look better than it is. The goal is to show the lender what the business actually earns once seller-specific noise is stripped out.

That's the practical lens to use all the way through due diligence. If an expense would continue after closing, assume the lender will keep it in. If it won't continue, and you can prove that clearly, it may qualify as an add-back.

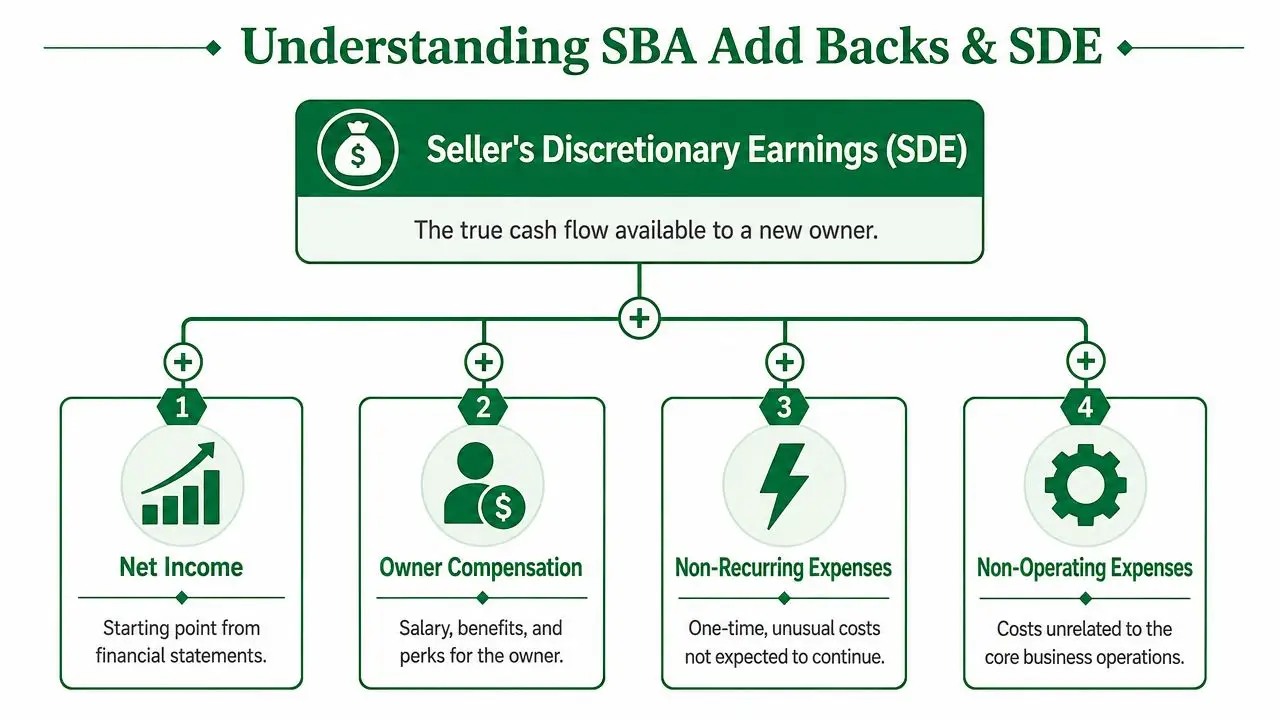

What Are Add Backs and Seller's Discretionary Earnings

A buyer reviews a company showing $120,000 of net income on the tax return. The seller says the business really produces $220,000 because the books include owner salary, interest, and a few personal expenses. That $100,000 gap can be the difference between an SBA approval and a decline. It can also be the difference between a sound deal and a file that falls apart in underwriting.

Seller's Discretionary Earnings, or SDE, is the cash flow figure SBA lenders usually use for owner-operator acquisitions. It starts with net income, then adds back expenses that are tied to the current owner, non-cash, financing-related, or genuinely non-recurring. The point is simple: determine how much cash a new owner should reasonably have available to cover debt service after the business changes hands.

Why lenders recast the numbers

Lenders do not underwrite off raw tax return profit alone because tax returns often reflect the seller's personal spending choices, tax strategy, and capital structure. A buyer inherits the business, not every accounting decision the seller made. Recasting adjusts for that.

The math matters more than the label. If a lender accepts a $40,000 add-back and applies a 1.25x DSCR requirement, that adjustment can support roughly $32,000 of additional annual debt service. Depending on rate and term, that may translate into a meaningfully larger loan. If the lender rejects that same add-back, the borrowing base drops immediately.

That is why buyers get into trouble when they treat add-backs as a wish list. More add-backs do not automatically make a file stronger. An aggressive recast may raise SDE on paper, but it also signals underwriting risk. Once a lender sees unsupported personal charges, vague one-time expenses, or costs that clearly continue after closing, credibility starts to erode.

What usually goes into SDE

In a typical owner-operator deal, SDE often includes:

- Owner compensation, such as salary, draws, payroll taxes, and owner-specific benefits

- Interest expense, because the buyer's financing structure will differ from the seller's

- Depreciation and amortization, since they are non-cash accounting charges

- True one-time expenses, if they are unusual, documented, and unlikely to recur after closing

A simple example shows why buyers focus on this metric. If net income is $100,000, owner compensation is $70,000, interest is $15,000, and depreciation is $10,000, preliminary SDE becomes $195,000. If annual debt service on the proposed SBA loan is $130,000, DSCR based on net income is too thin. DSCR based on accepted SDE is much stronger. But if a claimed $20,000 "one-time" expense gets disallowed, SDE falls back to $175,000, and the maximum safe loan amount may shrink fast.

That is the practical difference between a clean add-back and a rejected one. Every adjustment has a direct effect on DSCR, and DSCR drives approval, structure, and loan size.

For buyers comparing smaller owner-operated businesses to larger management-run companies, this guide on EBITDA vs SDE for SBA loan approval helps clarify which earnings metric lenders are likely to use.

Valuation also matters here. Buyers should not pay a higher multiple just because a seller presents a heavily adjusted SDE figure. These 2026 private company valuation insights are useful context when you are pressure-testing price against real cash flow.

Practical rule: Add back the expenses that clearly disappear after closing. Leave in the expenses the business still needs. A smaller, defensible SDE gets approved more often than an inflated one.

Commonly Allowed vs Disallowed SBA Add Backs

A buyer submits an offer based on $300,000 of SDE. Underwriting trims $40,000 of weak add-backs. At a 1.25x DSCR requirement, that cut does not just reduce a ratio on paper. It can reduce the supportable loan amount enough to force a price cut, a larger equity injection, or both.

That is why this section matters. The goal is not to pile on every possible adjustment. The goal is to use the add-backs a lender will accept and avoid the ones that make the file look stretched.

How lenders separate acceptable add-backs from weak ones

Lenders usually accept add-backs that are easy to prove and easy to explain. Owner salary in an owner-operator deal, interest expense tied to the seller's current debt, depreciation, and amortization are standard examples. These items either disappear after closing or do not reflect the buyer's ongoing cash cost in the same way.

The harder calls sit in the middle. Owner health insurance, retirement contributions, charitable giving, unusual legal bills, and project-based expenses can be accepted, but only when the facts are clean and the support is strong. A claimed add-back needs more than a note from the seller. It needs a clear story in the financials, the general ledger, and often bank or invoice support.

Then there is the category that hurts deals. Personal expenses mixed into the books, undocumented one-time charges, and costs that are plainly part of running the business usually get rejected. AcquiDex lays out this pattern well in its SBA add-back analysis from AcquiDex.

A good rule is simple. If the business still needs the expense after closing, leave it in.

For buyers who want a second layer of verification before relying on recast earnings, a quality of earnings report for an SBA loan can help test whether an add-back is real, supportable, and likely to survive underwriting.

If you want a broader framework for classifying expenses during diligence, even outside SBA lending, this UK business expense guide is a helpful reference.

SBA Add Back Cheat Sheet Accepted vs Rejected

| Expense Category | Typically Allowed? | Lender's Rationale & Notes |

|---|---|---|

| Owner salary and wages | Usually yes | Common in owner-operator acquisitions. Removing owner comp often increases SDE materially and can improve DSCR enough to support a larger loan. |

| Owner payroll taxes tied to compensation | Usually yes | Usually follows the same logic as owner compensation if those taxes disappear with that payroll expense. |

| Owner health insurance | Sometimes | Works only if the buyer will not continue the benefit as a business expense. If it stays, lenders keep it in the expense base. |

| Interest expense | Usually yes | Seller debt comes off at closing, so lenders typically recast this item and replace it with the buyer's proposed debt service in DSCR analysis. |

| Depreciation | Usually yes | Non-cash charge. Commonly added back, though lenders still care whether the business will need future capital spending. |

| Amortization | Usually yes | Same treatment as depreciation in most files. |

| One-time legal settlement | Sometimes | Can be acceptable if it was isolated, documented, and clearly unrelated to normal operations. Weak support often gets it cut. |

| Emergency repair | Sometimes | Possible if it was unusual and not part of a recurring maintenance pattern. If similar repairs show up every year, expect pushback. |

| Retirement contributions for the owner | Sometimes | Often allowed in true owner-operator deals, but lenders may question it if the buyer plans to keep a similar compensation package. |

| Charitable contributions | Sometimes | More likely to work if they are clearly discretionary and owner-specific, less likely if they look tied to ongoing marketing or community presence. |

| Meals and entertainment | Usually no | Often viewed as recurring and hard to separate cleanly between personal and business purpose. |

| Personal auto expense | Usually no | Rejected unless the books clearly isolate a personal component that disappears after closing. Mixed-use expenses create credibility issues fast. |

| Personal cell phone costs | Usually no | Same problem as auto. Small dollar amount, high skepticism, limited upside. |

| Undocumented one-time expenses | No | If the seller cannot tie the charge to tax returns, ledger detail, and backup documents, lenders will not give credit for it. |

| Failed advertising campaign | Usually no | The business chose to spend the money to generate revenue. Poor results do not make it non-operating. |

| Ongoing website maintenance | Usually no | Normal operating expense. It stays. |

| One-time website development project | Sometimes | Possible if it was a distinct project with invoices and no clear recurrence. Even then, lenders may discount it if the business regularly reinvests in digital updates. |

The math is where buyers get into trouble. A $25,000 add-back does not just add $25,000 to SDE. It can change DSCR enough to support more debt, which can tempt a buyer to justify a higher price. If that add-back gets removed late in underwriting, the structure can break quickly.

I see this mistake often in first-time acquisitions. Buyers assume more add-backs mean a better deal. In practice, aggressive recasts often create the opposite result. They invite more underwriter scrutiny, more document requests, and more last-minute cuts. A smaller SDE that survives credit review is worth far more than a larger SDE that exists only in the broker memo.

The cleanest files usually win.

How to Calculate SDE A Step-by-Step Example

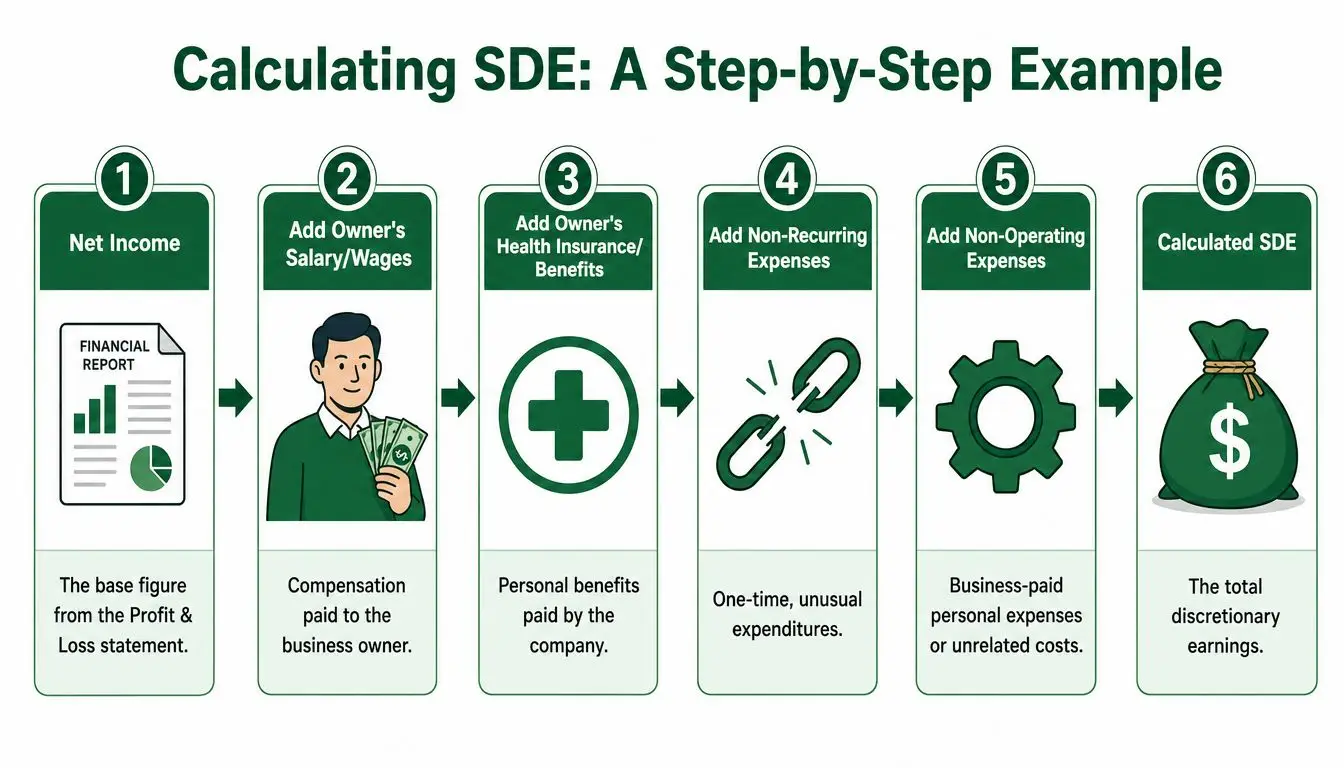

A buyer sees a business with $100,000 of net income and assumes the loan will size off that number. Then the recast adds back owner pay, interest, depreciation, and a one-time legal bill, and SDE jumps to $210,000. That difference is not academic. It can change whether the deal supports the note payment or falls short.

Start with the tax return, then prove each adjustment

Use the seller's tax return and current financials. Ignore the polished recast until every line can be tied back to returns, profit and loss statements, and general ledger detail.

Start with net income. Then test each proposed add-back against a simple question. Will this expense disappear or change under new ownership, and can the file prove it? Standard non-cash items such as depreciation, amortization, and interest usually have a clear path. Owner-specific or unusual expenses need more support.

A practical review usually works in this order:

- Pull net income from the tax return.

- Add owner compensation that a single owner-operator would not treat as a business expense in the same way.

- Add non-cash charges such as depreciation and amortization.

- Review one-time expenses individually and confirm they were isolated.

- Park gray-area items until invoices, ledger entries, and a credible explanation support them.

If the file has several adjustments or the earnings history is messy, a quality of earnings report for an SBA loan can help separate defensible add-backs from seller optimism before the lender does it for you.

A simple SDE schedule

Use a schedule like this.

| Line Item | Amount |

|---|---|

| Net income | $100,000 |

| Add owner compensation and perks | $80,000 |

| Add interest expense | $15,000 |

| Add depreciation | $10,000 |

| Add one-time legal fees | $5,000 |

| Calculated SDE | $210,000 |

The math is straightforward. The judgment is not.

That $210,000 is the number a buyer will often use to estimate debt coverage and back into a supportable loan amount. If annual debt service on the proposed SBA loan is $160,000, this example produces a DSCR of about 1.31x. Remove the $5,000 legal add-back and DSCR drops to about 1.28x. Remove another weak $15,000 adjustment and DSCR falls to about 1.19x. A deal that looked financeable can slip below a lender's comfort range fast.

That is why I tell buyers to build two versions of the recast. One version includes every add-back they think they can defend. The second includes only the adjustments that are clean, documented, and likely to survive underwriting. The second number is usually the one that matters.

List each adjustment on its own line. A single “miscellaneous add-back” entry signals weak support and gives the underwriter a reason to question the whole schedule.

The goal is not to produce the biggest SDE. The goal is to produce an SDE that survives credit review and still supports the purchase price. That is the difference between a model that looks good in diligence and a loan that closes.

How Add Backs Directly Impact Your Loan Approval

SBA add backs stop being an accounting exercise and start becoming a financing issue.

The math lenders care about

For SBA 7(a) acquisitions, lenders generally focus on whether the business produces enough normalized cash flow to cover debt. The standard framework is that SDE = Net Income + Owner Comp/Perks + Interest + Depreciation + Amortization + Valid One-Time Costs, and lenders typically require a DSCR of at least 1.25x, according to this overview of SDE, DSCR, and SBA loan approval math.

That's why each accepted add-back matters. The same source explains that a $50,000 valid add-back can move a file from 1.10x DSCR to 1.28x DSCR, which changes the outcome from rejected to approved in a borderline deal.

That's not theoretical. It's exactly how many acquisition files live or die. A lender doesn't fund based on what a seller “could have earned.” The lender funds based on the recast earnings that survive underwriting.

If you want to understand how this fits into the larger credit process, review how SBA lenders underwrite your deal. It's the clearest way to see why even one accepted or rejected adjustment can change the credit story.

Why aggressive add backs can backfire

Buyers sometimes assume more add-backs always mean more borrowing power. That's only true up to the point where the file remains credible.

Once the schedule starts looking padded, the lender often reacts by stripping items out, questioning the seller's bookkeeping, and taking a much more conservative view of the whole transaction. In practice, one weak add-back can trigger a deeper review of every other line.

A shorter, cleaner add-back schedule often gets further than a longer one packed with arguments.

The best recasts improve DSCR because they are boring. They tie cleanly to the tax return. They make sense operationally. They don't ask the lender to take leaps of faith.

Documentation Best Practices and Avoiding Red Flags

An add-back isn't real in underwriting until the file proves it.

The three-part test underwriters use

For an add-back to survive SBA underwriting, it has to meet three conditions. It must be valid, documentable, and identified on the tax return or year-to-date P&L, based on this underwriter-focused explanation of add-back validation.

That standard is stricter than many buyers expect.

Here's what that means in practice:

- Valid means the expense did not benefit the business in an ongoing way.

- Documentable means there's proof, such as invoices, payroll records, or W-2 support.

- Identified on official financials means the item can be traced to the tax return or lender-accepted interim statements.

If you need outside accounting help to clean this up before the file reaches credit, specialized expert financial services can help organize support and reconcile line items without turning the add-back schedule into guesswork.

What causes an underwriter to lose confidence

One of the biggest red flags is the use of round numbers or repeated identical amounts across years. Underwriters often treat that as estimation rather than evidence. The same source notes that lenders scrutinize multi-year tax returns to confirm the expense was absent in prior years before accepting it as one-time.

Another common problem is mixing a legitimate project cost with an ongoing operating expense. A one-time website development invoice may be defensible. A recurring maintenance charge usually isn't. If those are bundled together, the lender may reject both.

Use this checklist before submitting any recast:

- Match every line item to a source document so the lender can follow the trail.

- Separate one-time costs from recurring expenses instead of blending them under one label.

- Avoid seller-created estimates that can't be tied to actual booked entries.

- Make the tax return and recast talk to each other so there's no mystery about where the adjustment came from.

For a broader file-prep workflow, this SBA loan document checklist is worth keeping open during diligence.

Underwriters don't mind conservative math. They mind unsupported math.

Frequently Asked Questions About SBA Add Backs

What if the seller has no invoice for a one-time expense

Start with the lender's view. If the expense cannot be tied to a tax return, general ledger entry, bank statement, payroll record, or other official support, it usually does not count.

That matters because every unsupported add-back changes the math twice. It inflates cash flow on paper, then it inflates the loan amount built on that cash flow. If a buyer needs that adjustment to hit minimum DSCR, the deal can fall apart as soon as underwriting asks for backup. In practice, I would rather submit a smaller, defensible recast than a bigger one that gets stripped out late.

Can projected savings count as add backs

Usually no.

Future payroll cuts, vendor renegotiations, or software savings are part of the buyer's plan after closing. They are not historical earnings. SBA lenders underwrite the business based on what the company has already proven, not what the buyer hopes to improve in month three or month six.

You can still present the upside. Just keep it separate from the add-back schedule.

What about family members on payroll

The question is simple. Will that cost remain after the sale?

If a family member handles bookkeeping, production, sales, or another real job the business still needs, underwriters usually leave the expense in place. If the seller's spouse is drawing $45,000 a year and will not work for the buyer after closing, some or all of that amount may be added back. The closer the file gets to a personal expense dressed up as payroll, the more documentation you need.

A title alone does not decide it. The lender will look at duties, hours, pay level, and whether someone else must be hired to replace that work.

Can too many add backs hurt the deal

Yes, and at this point, first-time buyers get in trouble.

Every legitimate add-back can improve DSCR and increase proceeds. But excessive add-backs can make the lender question the whole recast. A file full of borderline adjustments tells the underwriter that reported earnings may not hold up after closing. Once that confidence drops, the lender may haircut multiple items, lower the supported loan amount, or pass on the deal entirely.

The same concern shows up in lender discussions about add-back red flags and the growing use of third-party Quality of Earnings reports, as noted in this discussion of add-back red flags and Quality of Earnings trends. The practical lesson is straightforward. More add-backs do not automatically mean a better file. They often mean more scrutiny.

Here is the trade-off buyers need to understand. A clean $60,000 add-back that the lender accepts is worth far more than a stretched $140,000 package where half the schedule gets rejected. The first version may support the DSCR you need. The second can sink it.

What's the safest mindset for a first-time buyer

Be conservative and build your case as if every number will be challenged.

A deal gets approved when the lender believes the cash flow will still be there after the ownership change. That usually means fewer add-backs, better support, and a recast that still works even if one or two adjustments are removed.

If you're buying a business and want an experienced team to pressure-test the seller's add-backs, structure the financing, and match your deal with the right SBA lenders, GoSBA Loans can help. They work as a no-cost SBA loan broker for buyers, coordinate lender options, and help turn a messy acquisition file into one that's easier to underwrite and close.