You found a business that looks right. The seller seems reasonable, the numbers look promising, and the broker is pressing for a signed LOI. Then the financing questions hit all at once. Which SBA program fits the deal? How much cash do you really need? Will a seller note help, or make the file harder? Why does one lender like the deal while another drags its feet?

That's where most first-time buyers get stuck. Not because the business is bad, but because acquisition lending is less about filling out forms and more about building a deal that a lender can defend in credit committee. A workable SBA loan for business acquisition depends on the target's cash flow, your file quality, the capital stack, and the lender you choose. Miss one of those, and a promising deal can stall late.

Table of Contents

- So You Found a Business to Buy What Now

- Not All SBA Loans Are Created Equal

- The Underwriting Gauntlet Your Document Checklist

- Structuring a Bankable Acquisition Deal

- From Term Sheet to Closing Navigating the Timeline

- Your Next Steps to a Successful Acquisition

So You Found a Business to Buy What Now

Most buyers start in the same place. You've identified a company with a believable story, recurring customers, and earnings that seem to support the price. Maybe you already signed an LOI. At that point, the transaction stops feeling theoretical. Every next step has a cost, a deadline, or both.

The mistake is treating financing like a box to check after the deal is negotiated. In practice, financing shapes the deal from the start. Purchase price, seller note terms, working capital, and your own liquidity all affect whether the file feels safe to a lender. A business can be attractive in the market and still be hard to finance if the structure is stretched.

Most acquisition denials don't happen because the buyer forgot one form. They happen because the deal was never bankable in the first place.

A first-time buyer usually needs to focus on four questions early:

- Can the business carry the debt: Lenders look for enough cash flow to support the proposed structure.

- Is the capital stack realistic: Purchase price alone isn't the full funding need.

- Does the seller understand SBA norms: Some sellers resist standby language or post-close liquidity requirements without realizing those are common pressure points.

- Are you talking to the right lender: General SBA lenders and acquisition-focused lenders are not the same thing.

That's why an LOI should never be the finish line. It's the point where the significant work starts. The buyers who close smoothly tend to do two things well. They package the file cleanly, and they shape the transaction around what an actual SBA lender will fund.

Not All SBA Loans Are Created Equal

A buyer can bring the same deal to three SBA lenders and get three different reactions. One sees a financeable acquisition. One wants more cash down. One declines because the structure is too tight for its credit box.

That difference usually starts with loan type, but it does not end there.

For an acquisition, the SBA program you choose affects more than rate or paperwork. It affects how much of the purchase can be financed, whether working capital fits inside the structure, how a seller note is treated, and which lenders will even take the file seriously. Buyers who understand that early make better LOI decisions and waste less time with lenders that were never a fit.

Why 7(a) usually leads the conversation

For most operating company purchases, SBA 7(a) is the starting point. It is the program lenders use most often for business acquisitions because it is flexible enough to cover the full scope of a deal. Purchase price is only one piece. Many files also need closing costs, a post-close cash cushion, or a seller note that stays on full standby for part of the term. A plain asset-heavy loan does not solve those issues well.

The practical advantage of 7(a) is that it gives more room to build a bankable capital stack. That matters if the seller wants a strong headline price, but the buyer needs enough liquidity left after closing to satisfy credit. It also matters if the business has seasonal swings or customer concentration, because the lender may want extra conservatism somewhere else in the structure.

If you want a plain-English primer before you talk to lenders, this guide to SBA 7(a) loans in 2026 is a solid place to start.

7(a) vs 504 for acquisition buyers

SBA 504 comes up often when a target business includes owner-occupied real estate. That can work, but buyers get in trouble when they assume 504 is just another version of 7(a). It is not. A 504 loan is built around fixed assets. An acquisition loan is built around the earnings of an operating company and the full deal structure around it.

If real estate serves as the main collateral story and the operating business is stable, 504 may deserve a look. If the transaction needs flexibility around goodwill, working capital, or mixed uses of proceeds, 7(a) is usually the cleaner fit.

| Feature | SBA 7(a) Loan | SBA 504 Loan |

|---|---|---|

| Best fit | Buying an operating business | Deals centered on major fixed assets, especially real estate |

| Flexibility | Broad, commonly used for acquisition structures | More specialized |

| Working capital fit | Better suited for mixed acquisition needs | Less natural fit for broad acquisition structures |

| Typical buyer use case | Stock or asset purchase with operating-company financing | Real-estate-heavy project with business occupancy considerations |

Here is what buyers often miss. A technically eligible deal can still be weak if the wrong program forces a bad structure. I have seen buyers chase 504 because the property looked attractive, then lose momentum because the actual credit concern was business cash flow and post-close liquidity, not the building.

Where Express fits

Then there's SBA Express. It can work for smaller, cleaner transactions, but it is often oversold in acquisition conversations. Many lenders reserve their best acquisition appetite for standard 7(a) files because the deal size, debt structure, and transition risk call for a fuller credit process.

That does not make Express bad. It makes it narrower.

If the acquisition is straightforward and the lender already likes the industry, Express may be worth discussing. If the deal has add-backs that need scrutiny, a meaningful seller carry, customer concentration, or a thin liquidity profile after closing, standard 7(a) is usually the better lane.

Practical rule: Pick the program that supports the full deal structure, not the one that sounds fastest.

Lender choice matters just as much. Some banks like professional services roll-ups. Others are more comfortable with blue-collar service businesses, franchise resales, or companies with hard assets. The same deal can look strong or weak depending on where it lands. That is one reason buyers should pressure-test staffing, payroll, and HR exposure early, especially if the target relies on outsourced employment support. A due diligence tool like this comparing PEOs checklist can help surface operational issues that later affect lender comfort.

The right question is not which SBA product exists. The right question is which loan program, and which lender, give this transaction the best chance of closing on terms the buyer can actually live with.

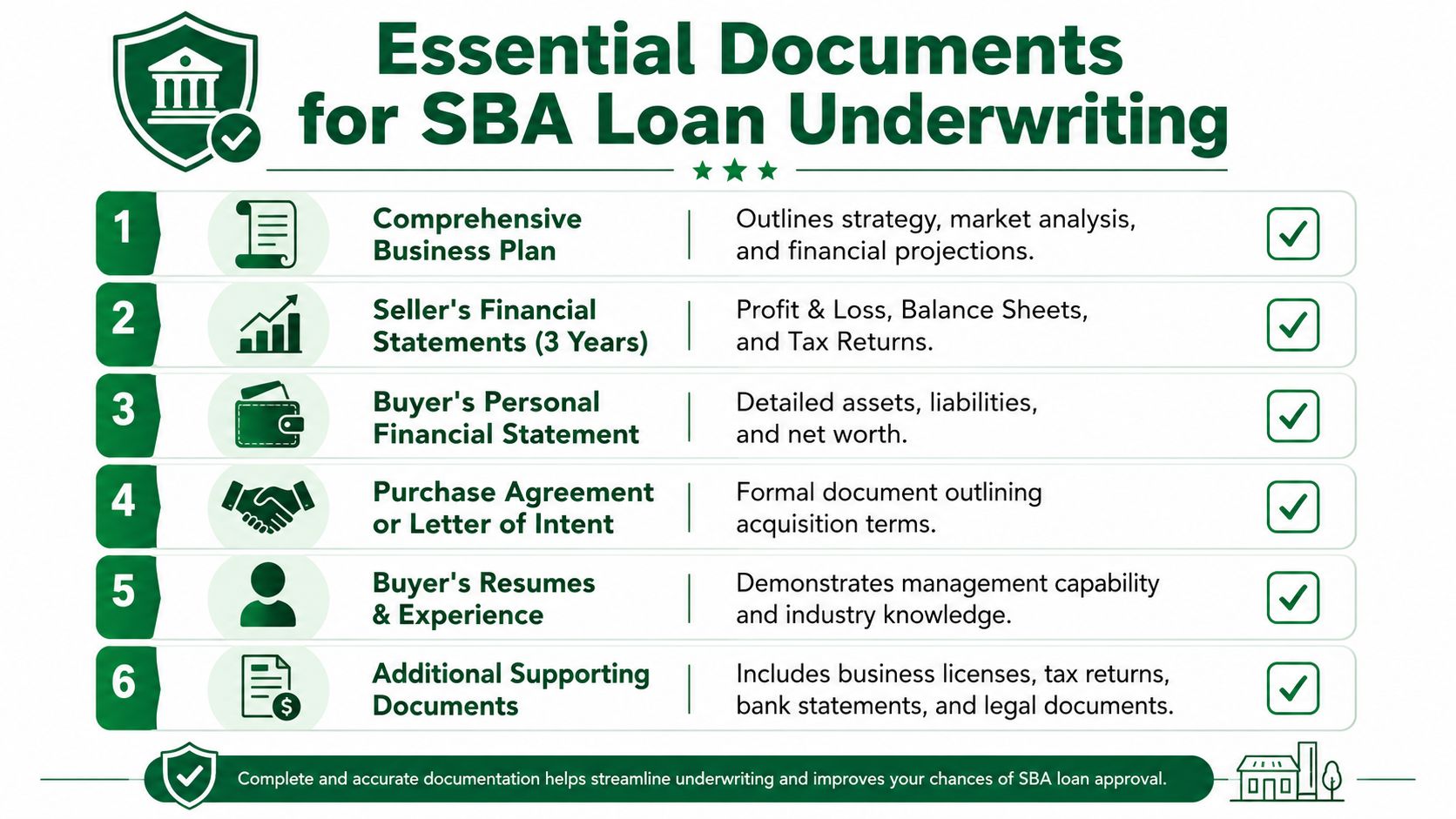

The Underwriting Gauntlet Your Document Checklist

A buyer gets an LOI signed on Friday, calls lenders on Monday, and expects quick feedback. By Wednesday, the file is stalled because the interim financials do not tie to the tax returns, the sources and uses is missing closing costs, and nobody can explain how much cash the business needs on day one. That is how decent deals lose momentum.

Underwriting starts before formal underwriting. The bank is deciding, early, whether your package looks financeable, whether the numbers hold together, and whether the buyer understands the transaction well enough to run it after closing. A complete file speeds that first read. A sloppy one creates doubt that is hard to reverse.

What lenders want before they take you seriously

For an acquisition, lenders usually want the same core set of documents up front:

- Seller financial history: The last three years of business tax returns, plus current year-to-date profit and loss and balance sheet

- Signed LOI: Enough detail to show price, structure, seller support, working capital expectations, and any post-close transition terms

- Sources and uses schedule: Purchase price, closing costs, fees, working capital, equity injection, seller note, and loan proceeds in one place

- Buyer financials: Personal tax returns and personal financial statements for each 20%+ owner

- Ownership and background details: Resumes, ownership chart, government-issued ID, and any information tied to affiliates or outside investors

If the target uses outsourced HR or payroll support, add that review early. The comparing PEOs checklist can help surface co-employment, benefits, and admin issues that later become lender questions.

Why each document matters

Each document answers a different credit question, and lenders read them together, not one at a time.

Tax returns and interim financials show earnings quality. The lender is looking for consistency, margin trends, seasonality, owner add-backs that can be defended, and whether the current year supports the story in the trailing returns.

The LOI shows whether the deal terms are underwritable. Purchase price matters, but lenders also focus on seller training, inventory treatment, assumed liabilities, working capital targets, and whether the seller note terms help or hurt the file.

The sources and uses schedule is where buyers often lose credibility. If that schedule does not include lender fees, legal, quality of earnings, broker fees, post-close cash, and any required injection, the deal looks underplanned. That is not a small issue. It suggests the buyer may be short on cash before the business even changes hands.

Buyer financials answer a simple question. Can this borrower absorb surprises? A lender wants to see post-close liquidity, outside income if relevant, contingent liabilities, and whether the guarantors have enough financial room to carry the business through a rough first quarter.

The practical point is simple. Underwriters test repayment early. They do not wait until the end of the process to see whether debt service works.

What slows files down

Credit teams can handle imperfect businesses. They have less patience for avoidable confusion.

If the banker has to rebuild your transaction from scattered documents and conflicting numbers, the file feels less credible and approval odds fall.

The delays I see most often are predictable:

- Current financials are missing or stale: Last year's tax return does not explain what the business is doing now

- The LOI leaves open major points: Vague language around working capital, seller carry, consulting period, or inventory creates immediate follow-up

- The sources and uses does not balance: Fees, holdbacks, and post-close operating cash are left out

- Add-backs are aggressive: Personal expenses, one-time costs, and owner perks are presented without backup

- Buyer finances change midstream: New debt, reduced liquidity, or ownership changes force the lender to rework the file

A strong package also shortens the back-and-forth with closing counsel, because the core economics are already documented clearly.

This walkthrough can help you organize the diligence side before the file gets deep into underwriting: business acquisition due diligence checklist for SBA loan buyers.

A quick overview is useful here:

One more point that matters in real deals. Underwriting is not only a document exercise. It is a structure test. The way your LOI, seller note, and cash injection are documented in this package will shape how the lender views risk long before a formal approval memo is issued. Buyers who understand that usually get cleaner feedback, fewer surprises, and a better chance of reaching closing on terms that still make sense.

Structuring a Bankable Acquisition Deal

You agree on a purchase price, the seller likes your offer, and the business looks solid. Then the lender starts pulling on the structure. The first question is rarely whether the company has potential. The key question is whether the deal gives the bank a clear path to repayment if the first year is tighter than expected.

That is the difference between a good target and a bankable acquisition.

The SBA 7(a) program can be used for business acquisitions, partner buyouts, and related business purposes up to $5 million, as outlined on the SBA's 7(a) loan program page. But SBA eligibility does not equal lender comfort. Banks approve transactions they can explain cleanly in credit committee, defend on cash flow, and close without structural loose ends.

What makes a deal bankable

Three variables drive approval odds more than first-time buyers expect: the seller note, the buyer's cash injection, and the lender you choose.

A seller note can help in two different ways. It can reduce the amount of bank debt, which improves debt service coverage. In some cases, if it is structured with full standby and documented correctly, it can also strengthen the equity story. But a seller note with early payments, vague subordination, or side terms that read like disguised senior debt usually creates trouble. I see buyers treat seller carry as a simple gap-filler. Lenders treat it as a risk item that has to fit the rest of the stack.

The buyer injection works the same way. The minimum contribution is only part of the conversation. If the business needs fresh working capital, equipment repairs, seasonal cash, or a cushion for customer concentration, putting in more cash can make a weak file lendable. That is not pleasant advice to give a buyer who wants to minimize their cash injection, but it is often the difference between a shaky approval and a structure that survives diligence.

Lender choice matters too. Some banks are comfortable with service businesses, some like recurring revenue, and some get nervous around customer concentration, heavy inventory, or turnaround stories. A deal can be acceptable to one lender and dead on arrival at another.

Where first-time buyers misprice the structure

The purchase price gets all the attention. The full uses of funds decide whether the deal works.

A bankable sources-and-uses schedule usually includes more than the acquisition itself:

- Purchase price

- Working capital at closing

- Loan fees and closing costs

- Inventory true-ups or AR adjustments, if the deal requires them

- Post-close liquidity the buyer needs to keep personally

- Any holdback, consulting arrangement, or transition expense tied to the sale

Many files start to wobble when the buyer has enough cash for the down payment, but not enough for the total transaction. Then the structure has to be rebuilt late in the process, usually with a lower price, a larger seller note, or more buyer equity.

Seller notes are not all equal

From a lender's point of view, seller financing only helps if it reduces pressure on the business after closing.

A useful seller note usually has clear subordination, no side agreements that conflict with loan documents, and payment terms that fit the company's projected cash flow. If the business is already tight on coverage, the lender may want standby for a period of time. If the note starts amortizing immediately, the same note that looked helpful in the LOI can weaken the file in underwriting.

That is the deal-making angle generic guides miss. Seller paper is not automatically favorable. Its value depends on how it changes the bank's risk.

Equity injection is a strategy decision

Buyers often ask how little cash they can put in. A better question is how much cash gives the deal the best chance to close on terms that still make sense.

If the business has stable margins, low customer concentration, and a clean transition plan, the standard structure may work. If the company has inconsistent earnings, deferred maintenance, customer concentration, or a learning curve for the buyer, adding equity can solve several problems at once. It lowers debt service, protects post-close liquidity, and gives the lender more confidence that the buyer can absorb an early surprise.

That trade-off needs to be measured, not guessed.

Control and rollover equity need clean rules

Rollover equity can help bridge valuation disputes and keep the seller invested in a smooth handoff. It can also create confusion if control rights, buyout terms, distributions, and guarantees are not clear.

Banks want a straightforward answer to a simple question: who controls the company after closing? If that answer is muddy, the lender starts worrying about management disputes, blocked decisions, and pressure on cash flow. The same issue comes up with outside investors. Extra capital can help, but only if the ownership structure stays simple enough for the bank to underwrite.

The practical test

Before a deal goes to credit, pressure-test it like this:

- If revenue dips after closing, can the business still cover senior debt comfortably?

- Does the seller note help cash flow, or does it just postpone an argument until underwriting?

- Is the buyer contributing enough cash to cover the full transaction, not just the headline down payment?

- Will the post-close balance sheet still leave room for payroll, repairs, and normal surprises?

- Is the ownership structure simple enough that the lender can approve it without extra legal complexity?

If too many of those answers are weak, the deal is not ready.

Insurance planning belongs in this budget as well, especially if the lender, landlord, or industry requires specific coverage. PIA's guide to business insurance costs is a useful reference for estimating one of the expenses buyers often understate.

One more practical point. The best acquisition structures are usually built before the term sheet, not after it. If you want a realistic view of how structure choices affect timing from offer to funding, review this SBA acquisition timeline from LOI to closing.

The strongest deal is not the one with the least cash in or the greatest debt financing on paper. It is the one a lender can approve, document, and fund without having to explain away obvious weaknesses.

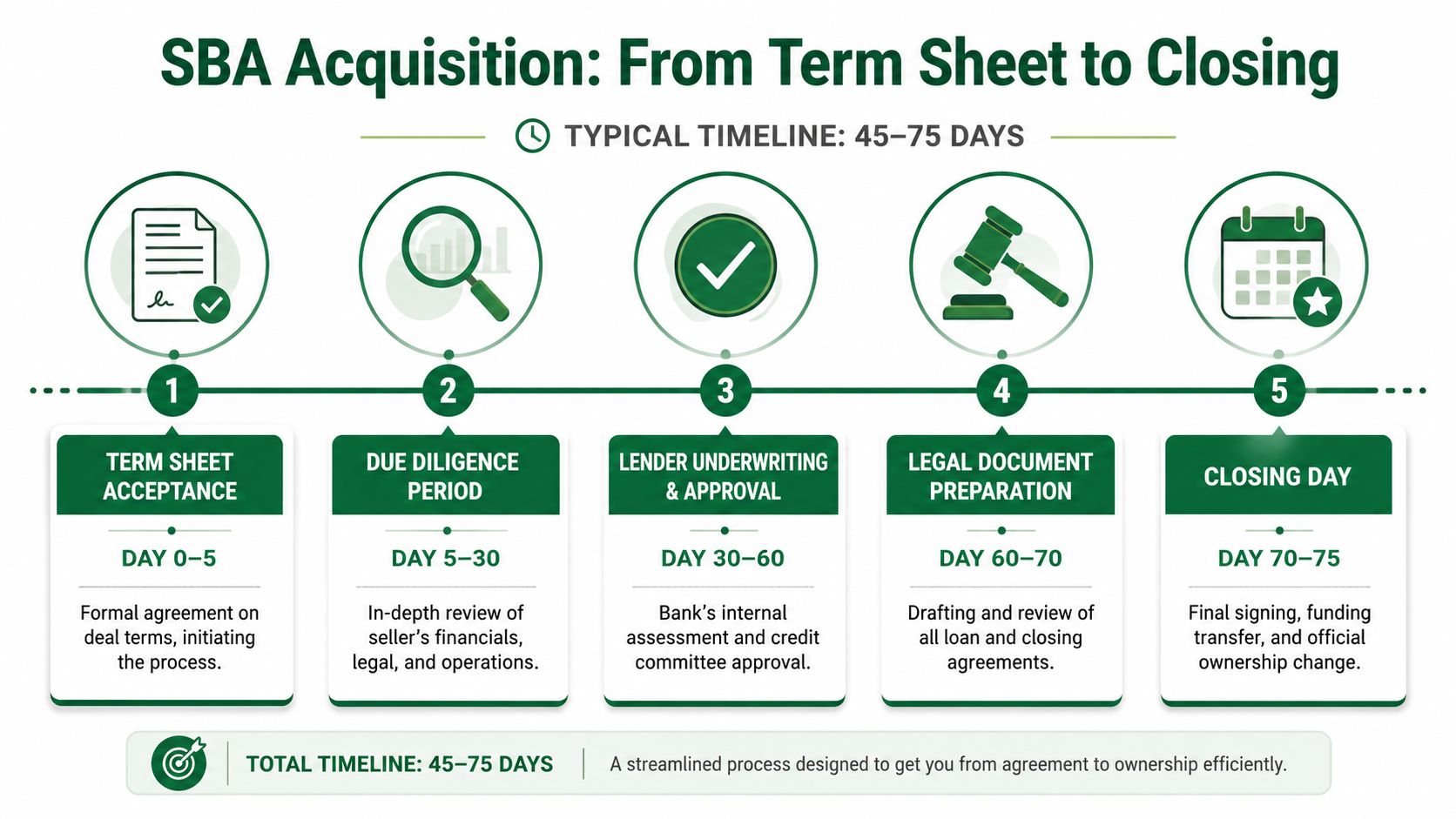

From Term Sheet to Closing Navigating the Timeline

A signed term sheet usually calms buyers down too early. The actual test starts after that, when the lender, seller, lawyers, and third-party vendors all begin pulling on the same file from different directions.

I tell buyers to treat this period as deal management, not paperwork. A transaction closes because the structure still works after appraisal, underwriting follow-up, legal edits, and updated cash needs. If one of those items changes the economics, the buyer has to solve it fast.

What happens after you say yes to a term sheet

The usual path from accepted term sheet to funding runs through the same checkpoints, even if the pace changes by lender and by deal. This LOI to closing SBA acquisition timeline shows how the sequence typically unfolds in a live acquisition.

Here is what happens:

- Term sheet acceptance starts the lender's formal file and confirms the basic loan structure.

- Lender diligence goes deeper on financial statements, tax returns, customer mix, lease terms, and background items.

- Valuation and third-party reports test whether the purchase price and projections hold up.

- Credit approval updates and legal drafting convert a conditional approval into closing documents.

- Final conditions and funding happen only after every open item is cleared, signed, and sourced.

The handoff points matter. Deals often slow down when one party assumes someone else is handling an item, especially lease consents, life insurance, entity documents, or seller-note revisions.

Where good deals start to slip

Late-stage problems usually look small on their own. Together, they kill timing.

An appraisal can come in light. The lender can require more post-close liquidity than the buyer expected. The seller note may need standby language that changes the seller's comfort level. Legal fees, transfer costs, and prorations can rise enough to force a last-minute injection increase.

That is why deal structure still matters after approval. A seller note that looked helpful in the LOI can become dead weight if the wording does not fit SBA rules or the bank's credit view. A thin cash injection can also become a closing problem if diligence uncovers working-capital pressure, deferred maintenance, or customer concentration that the lender wants buffered with more cash.

How buyers keep the file moving

The cleanest closings usually come from buyers who manage four pressure points well.

- They compare lenders on execution, not just rate. One bank may issue an attractive term sheet and then move slowly through diligence. Another may ask tougher questions early and close faster because the file is cleaner.

- They answer requests in full the first time. Partial responses create extra credit questions and reset the review clock.

- They resolve seller issues early. Training period, transition help, note terms, and working-capital targets should be settled before documents are being drafted.

- They keep legal and lending aligned. If the purchase agreement says one thing and the loan approval says another, closing counsel has to stop and fix it.

I also like buyers to have counsel who understands the transaction side, not just entity formation. If you need a practical legal overview, this guide on buying or selling a business is a useful reference alongside the financing work.

A term sheet gives you a path. Closing requires a bankable deal that still holds together after every assumption gets tested.

Your Next Steps to a Successful Acquisition

At this point, the path is straightforward, even if the work isn't easy. A successful SBA loan for business acquisition usually comes down to preparation, structure, and execution. If one of those breaks, the deal gets expensive, slow, or both.

Preparation means building a file that can stand up to scrutiny early. Structure means shaping the transaction around what lenders approve, not what looks good in a headline purchase price. Execution means managing diligence, third-party reports, legal work, and seller expectations without letting the process drift.

That's why experienced guidance matters. SBA acquisition lending isn't just lending. It sits at the intersection of credit, deal design, negotiation, and timing. Buyers who try to learn all of that in one live transaction often find out too late where the weak spots were.

If you're still evaluating the legal side of the transaction, this overview of buying or selling a business from Lein Law Offices is a useful complement to the financing work. A clean legal process and a clean lending process tend to reinforce each other.

The smartest next move usually isn't becoming your own lender, underwriter, and closing coordinator. It's working with someone who already knows how acquisition lenders think, how to package the file, and how to shape the capital stack before the deal starts slipping. The right guidance can save time, retain your advantage in negotiations, and keep you from solving the wrong problem.

If you're buying a business and want help structuring the financing, GoSBA Loans can help you compare lenders, shape a bankable capital stack, and move from LOI to closing with less friction.