You're usually not worried about licensing when you start an SBA loan file. You're worried about approval odds, down payment, debt service, and how fast you can close. Then underwriting starts asking sharper questions. Who holds the professional license? Is that license transferable? Does the ownership chart include any indirect foreign owner? Is the seller keeping a sliver of equity?

That's where deals get stuck in 2026. Not because the business lacks revenue, but because the legal right to operate the business after closing doesn't line up with SBA rules. The SBA SOP is the main source of truth here, and lenders treat licensing as an operating-risk issue, not a paperwork issue.

Most generic articles stop at “make sure you have the right permits.” That's too shallow for today's market. The hardest parts now are the non-transferable license trap in regulated service businesses and the strict 100% citizenship and residency rule under SBA Policy Notice 5000-876441, which reaches indirect ownership too. If you miss either one, a strong loan package can still fail.

Table of Contents

- Why Licenses Are a Core Requirement for SBA Lenders

- The Universal SBA Loan Licensing Checklist

- Navigating Industry-Specific License Requirements

- Uncovering State and Local Permit Nuances

- Critical Pitfalls The License Traps That Kill Deals

- Your Action Plan for Missing or Pending Licenses

- Frequently Asked Questions About SBA Licensing

- Can I close if my license is still pending

- Do home-based businesses face different licensing issues

- If I hire a licensed employee, is that enough

- Can a seller's license carry me through a transition

- Do franchise buyers have extra licensing concerns

- What's the difference between an operating business license and an SBLC license

- Will a strong credit profile overcome a licensing issue

Why Licenses Are a Core Requirement for SBA Lenders

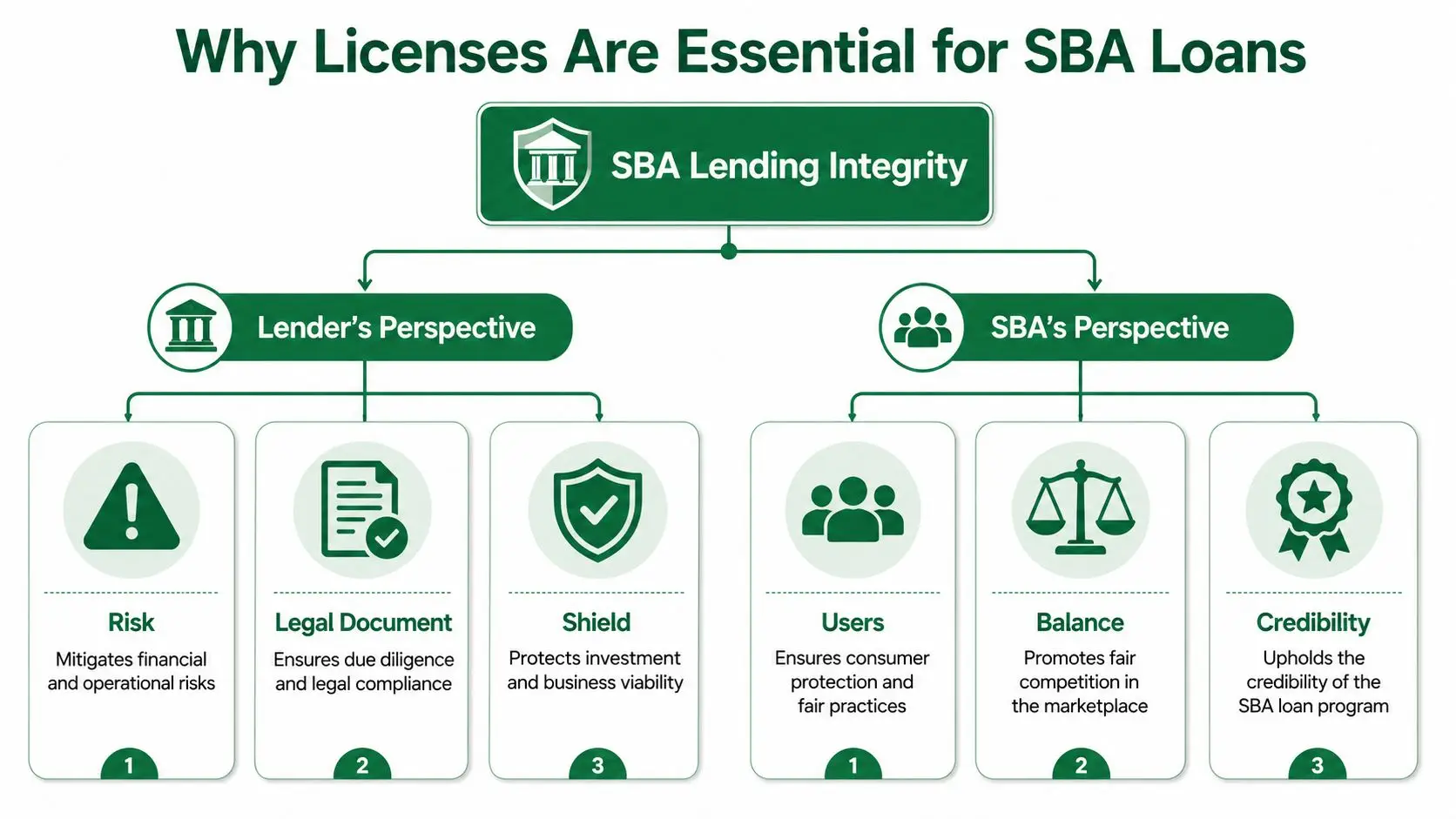

A borrower can have strong tax returns, a solid down payment, and a clean credit profile, then lose the deal because the business cannot legally operate the day after closing. I see this in acquisitions all the time. The buyer focuses on cash flow, while the lender focuses on legal operability, control, and whether the license structure survives the ownership change.

What the lender is really testing

Under SBA SOP underwriting, licensing is not a side issue. It sits inside eligibility, repayment ability, and collateral risk. The lender is asking whether the borrower has the legal right to generate the revenue used to repay the loan, and whether that right stays in place after the transaction closes.

That review usually comes down to three questions.

- Can the business legally operate at closing and immediately after funding?

- Does the ownership and control structure match the licensing rules for that industry and state?

- If the loan goes bad, is there still an operating business the lender can enforce against or sell?

Those questions get harder in 2026, not easier. Two issues are killing otherwise bankable files. First, some licenses do not transfer cleanly in an asset sale, especially in service businesses where the actual value depends on a specific professional, entity, or management structure. Second, the new SBA citizenship rule under Policy Notice 5000-876441 is strict enough to knock out borrowers with indirect foreign ownership, even where the operating company itself looks domestic on first review.

This is why lenders ask for more than a license certificate. They compare entity documents, ownership schedules, leases, management agreements, and professional credentials to make sure the full structure works. In practical terms, licensing review is also a compliance review. If you want a plain-English legal framing of that concept, Kons Law explains compliance in a way that tracks closely with how credit teams assess risk.

Practical rule: If the licensed activity, the legal entity, and the control rights do not line up, the lender will treat the file as unstable.

Cash flow analysis follows the same logic. A lender still has to size debt against credible operating income, often using debt service coverage as a core screen. But projected cash flow only matters if the business can legally keep producing it after closing. If the license sits with the seller, depends on a barred ownership structure, or cannot be reissued on time, underwriting income loses credibility fast.

Licensing affects cash flow, collateral, and closeability

The risk is immediate. A contractor that loses its qualifying party, a restaurant missing local approvals, or a med spa built on a weak CPOM structure can see revenue interrupted overnight. That is not a technical defect. It is a repayment problem.

Collateral gets weaker too. SBA lenders do not underwrite liquidation alone, but they care whether the assets support an operating business. If the license cannot be transferred or reissued, furniture, equipment, and goodwill may have much less value than the purchase price suggests. I have seen buyers discover this after signing the LOI, when they assumed the seller's license or medical director arrangement would automatically carry over. In many states, it does not.

That is why experienced lenders review licensed-business structure before they get comfortable with the rest of the credit file. The team at GoSBA Loans covers licensed-business lending issues with the same practical focus used in real SBA underwriting. Legal operability comes first. Financial strength only counts if the business is allowed to earn the revenue.

The Universal SBA Loan Licensing Checklist

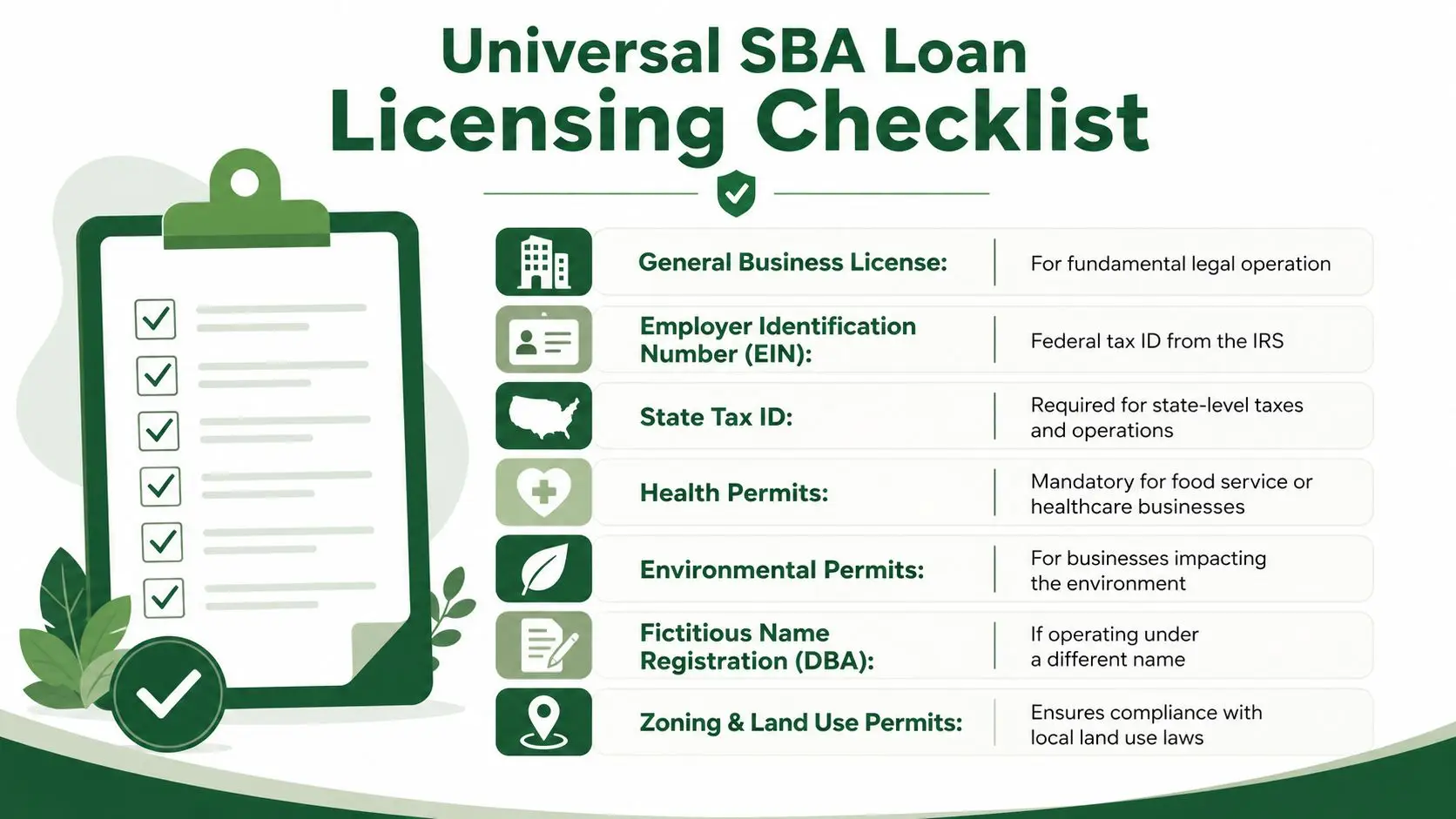

Most borrowers need a simpler starting point than the SBA SOP itself. Before you tackle industry-specific problems, assemble the base file that every lender will expect to see. This doesn't solve every underwriting issue, but it surfaces missing pieces early enough to fix them.

Core documents every borrower should assemble

Use this as your baseline checklist.

- Entity formation documents: Articles of Incorporation, Articles of Organization, partnership filings, and any amendments. Lenders compare these against the ownership schedule and guarantor list.

- Governing documents: Operating agreement, bylaws, shareholder agreement, or partnership agreement. These matter because control rights often determine whether the licensing structure works.

- Federal tax ID: Your EIN confirmation. The lender uses it to tie tax returns, transcripts, and entity identity together.

- State registration status: Certificate of good standing or equivalent proof that the entity is active where it was formed and where it does business.

- DBA or fictitious name registrations: If the business operates under a trade name, the lender will want the filing to match bank statements, leases, and customer-facing documents.

- Local business license: Many cities and counties require a general business operating license even when the industry itself isn't heavily regulated.

- Sales tax or state tax registrations: If the business collects sales tax or has state payroll obligations, expect the lender to check that the registration trail is clean.

- Facility-specific permits: Health, fire, occupancy, zoning, signage, or environmental permits when the location and use require them.

A useful mindset is to run your loan package like a compliance audit. If you work with security, legal, or compliance teams in other contexts, the structure in this compliance guide for CISOs mirrors the same discipline lenders want to see: identify obligations, verify documents, and match ownership to responsibility.

How to use the checklist in underwriting

Don't just gather documents. Match each one to four questions:

| Document type | What the lender checks |

|---|---|

| Formation records | Is the borrower entity valid and current? |

| Governing documents | Who controls the company and can sign? |

| Operating licenses | Can the business legally generate revenue? |

| Permit file | Can the location legally be used as intended? |

A complete checklist doesn't guarantee approval. It does prevent avoidable delays caused by obvious gaps.

Borrowers who want a practical file-prep template can use an SBA loan application checklist before they submit to a lender. It helps keep the licensing package aligned with the broader underwriting package instead of treating permits as a last-minute add-on.

Navigating Industry-Specific License Requirements

A file can look financeable until the lender asks a simple question: who holds the license that lets this business earn revenue on day one after closing?

That question drives many of the hardest SBA deals in regulated industries. Under SBA SOP 50 10 and standard lender closing practice, the borrower must be able to operate legally at closing. In practice, lenders test more than whether a license exists. They look at whether the right entity holds it, whether the required person will remain in place, and whether the license structure matches the ownership and control shown in the loan file.

The recurring problem is misalignment. The buyer wants to acquire the economics of the business, but state law may give operating authority to a licensed individual, a professional entity, or a designated qualifying party. If those pieces do not line up, the credit story falls apart even when cash flow looks strong.

The pressure points show up in the same industries again and again: healthcare, dental, veterinary, pharmacy, HVAC, plumbing, electrical, childcare, transportation, and many construction trades.

Where deals get stuck

Lenders usually slow down or decline when the business depends on one of these arrangements:

- A license that stays with the seller: If the seller leaves and the license cannot transfer, post-closing operations may stop immediately.

- A qualifying individual with weak legal authority: A leased employee or contractor may satisfy day-to-day operations, but lenders still ask who controls the business if that person resigns.

- An ownership chart that conflicts with state law: If a state requires licensed ownership or licensed control, side agreements and nominee structures usually create more problems than they solve.

- An MSA layered over a regulated business: A management services agreement can separate economics from clinical or professional services, but it does not cure a borrower structure that violates licensing rules.

The med spa and CPOM trap

Med spas deserve special attention because they combine two issues that kill SBA deals fast. First, many states restrict who can own or control the medical side of the practice under corporate practice of medicine, or CPOM, rules. Second, the operating license or clinical authority is often tied to a physician, nurse practitioner, physician assistant, or professional entity that is not the actual SBA borrower.

That does not mean med spas are unfundable. It means the structure has to be legally clean before the file reaches underwriting. I have seen borrowers spend weeks polishing projections while ignoring the core problem: the proposed buyer can buy the cash flow, but not the legal right to deliver the licensed service in the same form after closing.

This is also where the non-transferable license trap becomes expensive. If the med spa's model depends on a seller-owned professional entity, a medical director arrangement that is too thin, or a state-specific CPOM workaround that counsel has not fully documented, the lender will usually pause the file until healthcare counsel confirms operability. Some lenders will choose to pass.

Before you underwrite earnings in a regulated business, confirm the buyer will have lawful operating authority on the first day after closing.

The same analysis applies outside healthcare. A construction company may rely on a qualifier's license. A dental practice may require licensed ownership or reserved governance rights. A veterinary clinic can raise the same control issues. Childcare and transportation businesses often have agency approvals tied to a location, a named operator, or both. The common thread is simple: the income stream only counts if the borrower can legally continue it.

Franchise transactions raise a different version of the same issue. Brand approval does not replace state licensing, and state licensing does not replace franchise system approval. Buyers comparing those layers should review this guide to buying a franchise with an SBA loan because franchise files often expand into the same control, entity, and operability questions that appear in licensed industries.

Uncovering State and Local Permit Nuances

Many SBA files don't fail because the borrower missed a federal rule. They fail because the borrower assumed a state board, city department, or county office would “figure it out later.” Local permitting doesn't work that way.

Start with the entity then move to the location

Check the business in layers.

First, confirm the entity is registered and active in the right state. Then confirm the business activity itself is permitted under state law. After that, check the physical location. A business can be validly formed and still be unable to operate at a specific site because of zoning, health, occupancy, signage, or use restrictions.

This is especially important in owner-occupied real estate files. Buying the building doesn't solve permit issues. It can create new ones if the planned use triggers environmental review, occupancy changes, or municipal approvals. Borrowers working through that part of diligence should review how SBA environmental requirements for commercial real estate fit into site-level underwriting.

A practical research path

Use a simple order of operations:

- Secretary of State: Verify entity status, legal name, and foreign registration if applicable.

- State licensing board: Confirm whether the activity requires an individual license, entity license, or both.

- City hall or county clerk: Ask about local business licenses, zoning clearance, occupancy permits, and use-specific approvals.

- Landlord or seller file: Review existing permits, prior violations, and renewal history.

- Your attorney and lender: Match the legal requirements to the ownership and closing structure.

A borrower who calls only one office usually gets an incomplete answer. Licensing is fragmented. One agency may approve the entity while another controls the premises and a third controls the profession.

Bring the exact post-closing ownership structure when you ask questions. Agencies often answer differently once they know who will own and control the business.

Critical Pitfalls The License Traps That Kill Deals

A buyer gets through credit, cash flow, and valuation. Then lender counsel reviews the ownership chart and licensing file, and the transaction stalls. In 2026, that is the pattern I see most often. The problem is usually not an expired permit. It is a structural issue that cannot be patched a week before closing.

The 100% citizenship rule is now an eligibility screen

Under SBA Policy Notice 5000-876441, effective March 1, 2026, the applicant's ownership chain must be entirely U.S. citizen or U.S. national ownership, including direct and indirect owners. SBA lenders are treating this as a threshold eligibility issue, not a document cleanup item. A borrower can have strong debt service coverage, good collateral, and years of operating history, and still fail here.

Review the cap table before the term sheet goes out. That review needs to include holding companies, trusts, spouses with ownership interests, and any parent entity above the borrower. If an ineligible owner appears anywhere in the chain, the lender may stop the file before underwriting gets very far. The relevant SBA notice is available directly through the SBA policy notice archive.

The errors are predictable:

- Borrowers disclose only the operating company. Lender counsel asks for the upstream entity chart and finds a problem later.

- Trust ownership is treated as invisible. It is not.

- Operating agreements were amended informally but not legally updated. The stale version is what the lender underwrites.

- Minor indirect interests are dismissed as irrelevant. Under the current rule, the question is whether the interest exists, not whether that owner controls the business.

I tell clients to solve this before they spend money on appraisals, legal, or franchise review. If the ownership chain is not clean, fix the structure first or choose a non-SBA path.

A document review tool can help organize the file, but it does not replace counsel. If your team wants a structured way to review financing documents and compliance language before lender legal does, PDF AI's finance advisor can help with internal review.

Non-transferable licenses create a second trap

The other deal-killer is common in service businesses where the revenue depends on a person-specific or entity-specific license. Med spas are a good example. If the current model depends on a physician relationship, management structure, or ownership arrangement that raises corporate practice of medicine concerns, the lender is not looking at a routine license handoff. The lender is asking whether the post-closing business can legally operate at all.

Buyers often get hurt by bad assumptions. The seller says, "We have always done it this way." The agency says the license does not transfer, the professional must stay in control, or the management agreement needs to be rewritten. By that point, the purchase agreement is signed and the financing clock is running.

The pattern shows up in several forms:

| Trap | What it does to the deal |

|---|---|

| License is issued to the seller personally | Buyer cannot rely on it after closing |

| License is issued to the wrong entity | New application may be required under the borrower |

| Professional owner must retain control under state law | SBA ownership and guaranty structure may conflict with the operating model |

| CPOM-sensitive management model is undocumented or weak | Lender legal questions whether the business can lawfully operate post-close |

This is why regulated acquisitions need legal diligence early, not after commitment. A focused M&A due diligence checklist for SBA-backed deals helps surface whether the license follows the assets, the entity, or the individual.

Seller rollover equity can also block closing

Buyers often propose a small seller rollover to keep the transition stable. In ordinary business terms, that can make sense. In SBA lending, it can create two separate problems at once. First, the seller may need to remain liable on the loan if they keep equity, depending on the final structure and the lender's reading of the current SOP. Second, a retained seller interest does nothing to fix a non-transferable license if the underlying issue is who must legally own or control the practice.

That trade-off is often misunderstood. Keeping the seller involved may help operations, but it can complicate guarantees, ownership compliance, and licensing. For a more durable discussion of SBA transaction structuring and post-closing obligations, a law firm analysis such as this summary of SBA acquisition structuring issues from Greenberg Glusker is a better reference point than informal commentary.

The practical rule is simple. Do not approve seller rollover, consulting, or transition equity until three things line up on paper: SBA eligibility, state licensing law, and the lender's guaranty requirements. If one of those three breaks, the deal can still die after approval.

Your Action Plan for Missing or Pending Licenses

The problem usually surfaces at the worst point in the deal. The buyer has cleared underwriting questions, the seller is counting days to close, and then someone asks for proof that the business can legally operate on day one under the post-closing structure.

Treat that moment like triage, not cleanup. The first question is not whether a license exists. The question is whether the right person or entity will hold the right authority at closing. In 2026, that matters even more for two recurring problem files: service businesses with non-transferable professional licenses, and ownership structures that raise citizenship issues under SBA Policy Notice 5000-876441.

Start by sorting the issue into one of these categories:

- Missing but obtainable before closing

- Pending with the agency

- Legally non-transferable or incompatible with the deal structure

Those categories lead to very different lender responses. A pending city permit can be workable. A professional license tied to the seller, or tied to a physician in a med spa structure with CPOM concerns, can force a full restructuring of ownership, management, or the asset purchase terms.

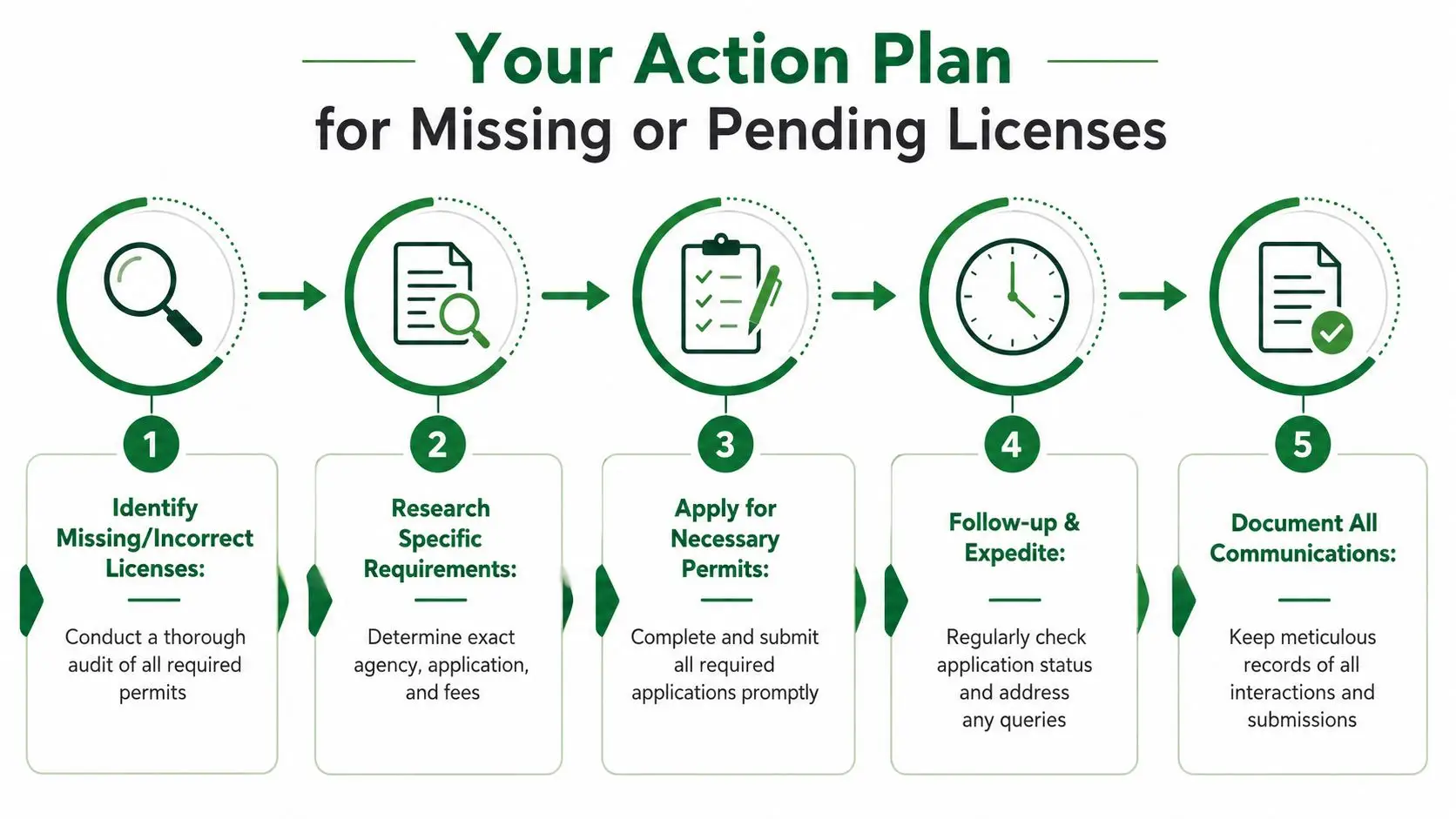

What to do immediately

Use this sequence:

- Tell the lender before underwriting finds it. Early disclosure gives the lender a chance to set conditions instead of questioning credibility.

- Confirm the rule with the licensing authority. Ask whether the license transfers, whether temporary operation is allowed, and whether the application must be filed in the buyer's post-closing entity.

- Get the answer in writing. Email confirmation, portal status, or agency instructions carry far more weight than a phone summary.

- Check the ownership chart and citizenship issues at the same time. If the file has any direct or indirect foreign ownership, fix that before you spend more money on the license path.

- Align the purchase agreement with the licensing reality. Add extensions, cooperation obligations, and clear closing conditions if approvals are still outstanding.

- Tie the license plan to the operating plan. If the business needs a qualifying individual, medical director, designated broker, or licensed manager, document who that person is, when they start, and what authority they will hold.

One bad assumption can sink the file. I see this often with buyers who file under the wrong entity, or assume the seller's license can remain in place for a transition period when state law says otherwise.

The quickest way to lose lender confidence is to call a licensing defect "administrative" before anyone has confirmed transferability, control requirements, and post-closing legal authority to operate.

How to keep the deal alive

The lender still has to approve the whole credit and eligibility package. Delays on licensing can push financial statements stale, force revised projections, extend rate locks, and reopen underwriting questions that were already settled. Even strong borrowers lose momentum when the file sits because no one defined the cure path.

Build that cure path in writing:

- Agency contact log: who you spoke with, what was confirmed, and what remains outstanding

- Exact filing status: submitted, deficient, under review, approved pending fee, or awaiting inspection

- Funding condition: what the lender must see before closing or before disbursement

- Seller cooperation list: signatures, attestations, transition services, record releases, or board approvals

- Licensed personnel plan: employment agreement, start date, supervisory role, and whether the arrangement satisfies state law

- Revised closing calendar: a date-by-date timeline shared with the lender, buyer, seller, and counsel

Be careful with workarounds. Hiring a licensed employee can solve the problem in some industries, but not where the law requires ownership or control by a licensed person. That distinction matters in regulated service businesses. It also matters in acquisitions where the seller is exiting and the license does not follow the assets.

If the license cannot be transferred, say so early and restructure the deal around that fact. Possible fixes include delaying closing until a new license issues, changing who owns the operating entity if state law allows it, carving out restricted services until approval is complete, or walking away before diligence costs climb further. A weak workaround usually costs more than a hard reset.

For borrowers who need help matching the licensing structure to lender expectations, GoSBA Loans can evaluate whether the buyer, seller, or employee-held license setup is likely to fit SBA lender requirements before the file gets too far. That screening is useful when the primary issue is not credit quality but whether the ownership, control, and licensing pieces work together on paper and in practice.

Frequently Asked Questions About SBA Licensing

Can I close if my license is still pending

Sometimes, but only when the lender believes the pending approval is real, timely, and sufficient for legal operation after closing. A receipt alone usually isn't enough. The lender will want to see what was filed, who filed it, whether it was filed under the correct entity, and whether the business can legally operate while the application is pending.

If the license is essential and no temporary authority exists, many lenders will require issuance before funding.

Do home-based businesses face different licensing issues

Yes. Home-based businesses often trigger local zoning, occupancy, HOA, signage, and use restrictions that borrowers underestimate. The state may not care, but the municipality might. A business can be legal at the entity level and still violate local rules at the property level.

The practical fix is to confirm both business registration and property-use permission before you submit the loan.

If I hire a licensed employee, is that enough

Sometimes, but it depends on the industry and the state rule. In some businesses, the licensed person must hold a particular ownership, officer, or control role. In others, a qualified employee may be enough if the entity license and supervisory structure are correct.

Lenders won't accept a generic promise to “hire someone later.” They want to know the role, authority, timing, and durability of that arrangement.

Can a seller's license carry me through a transition

You shouldn't assume that. Many licenses are personal, entity-specific, or ownership-sensitive. A change of control can force requalification or terminate the license's usefulness for the buyer. That's why regulated acquisitions need licensing review before the purchase agreement becomes binding.

Do franchise buyers have extra licensing concerns

Yes, sometimes. Franchises can add another layer of approval through the franchise agreement, the franchisor's operational standards, and site requirements. That doesn't replace ordinary licensing. It stacks on top of it. Borrowers need both the brand-side approvals and the legal authority to operate the underlying business.

What's the difference between an operating business license and an SBLC license

They're completely different. An operating business license lets your company legally conduct its business under state or local rules. An SBLC license allows a non-depository lender to make SBA 7(a) loans directly. The SBA's 2023 announcement on new Small Business Lending Company license applications noted that it opened the first application window for new SBLC licenses in over 40 years and capped new licenses at just three, which shows how tightly controlled that lender-side licensing process is.

Will a strong credit profile overcome a licensing issue

No. Good credit helps, but it doesn't override legal operability. Lenders need both. If the borrower can't legally operate the business or the ownership structure conflicts with the licensing regime, strong numbers alone won't fix it.

If you're buying a business, refinancing, or trying to solve a licensing issue before submitting to lenders, GoSBA Loans can help you pressure-test the ownership structure, licensing setup, and lender fit before you waste time on a file that won't clear SBA underwriting.