You've got a deal in motion. Maybe you signed an LOI on a business acquisition. Maybe you need working capital to stabilize growth. Maybe you found an owner-occupied building and want to stop renting. Then the financing process starts, and the simple question becomes hard fast: what are the actual SBA minimum requirements, and which of them matter in practice?

That confusion is normal. The SBA publishes baseline rules, lenders apply their own credit judgment, and many online guides blend the two together. The result is that borrowers often think they qualify because they meet one threshold, only to learn later that their structure, cash flow, ownership, or down payment doesn't fit how lenders underwrite.

The main source of truth should always be the SBA SOP. It's the rulebook lenders work from. But borrowers also need practical interpretation. Policy discussions around Reforming SBA to help businesses matter because they highlight a reality every serious borrower feels: access to capital depends not just on program design, but on how rules get applied.

Table of Contents

- Navigating the Maze of SBA Loan Eligibility

- The Foundation SBA's Core Eligibility Rules

- Key Underwriting Metrics You Must Meet

- SBA Loan Programs A Head-to-Head Comparison

- Understanding Equity Injection and Collateral

- The Lender Overlay Why SBA Minimums Are Just the Start

- Common Questions About SBA Minimum Requirements

Navigating the Maze of SBA Loan Eligibility

Most borrowers don't lose time because the SBA is impossible. They lose time because they apply with the wrong expectations.

A buyer sees a business with solid historical earnings and assumes that should be enough. An owner with strong revenue assumes a bank will overlook weak global cash flow. A startup founder hears “SBA-backed” and thinks that means flexible. Then underwriting starts, and the deal gets picked apart from every angle: ownership, experience, guarantors, repayment ability, equity injection, and documentation quality.

That's where the gap opens between published SBA minimum requirements and lender reality.

Meeting the floor gets you into the conversation. It doesn't get you approved.

The practical way to think about SBA eligibility is this: first, determine whether the business and ownership structure fit the program at all. Second, test whether the financial profile clears underwriting. Third, ask whether the deal is strong enough for a lender to compete for it.

Serious borrowers do better when they stop asking, “Can this deal qualify?” and start asking, “Will a lender want this deal in its credit box?” That second question is what saves months.

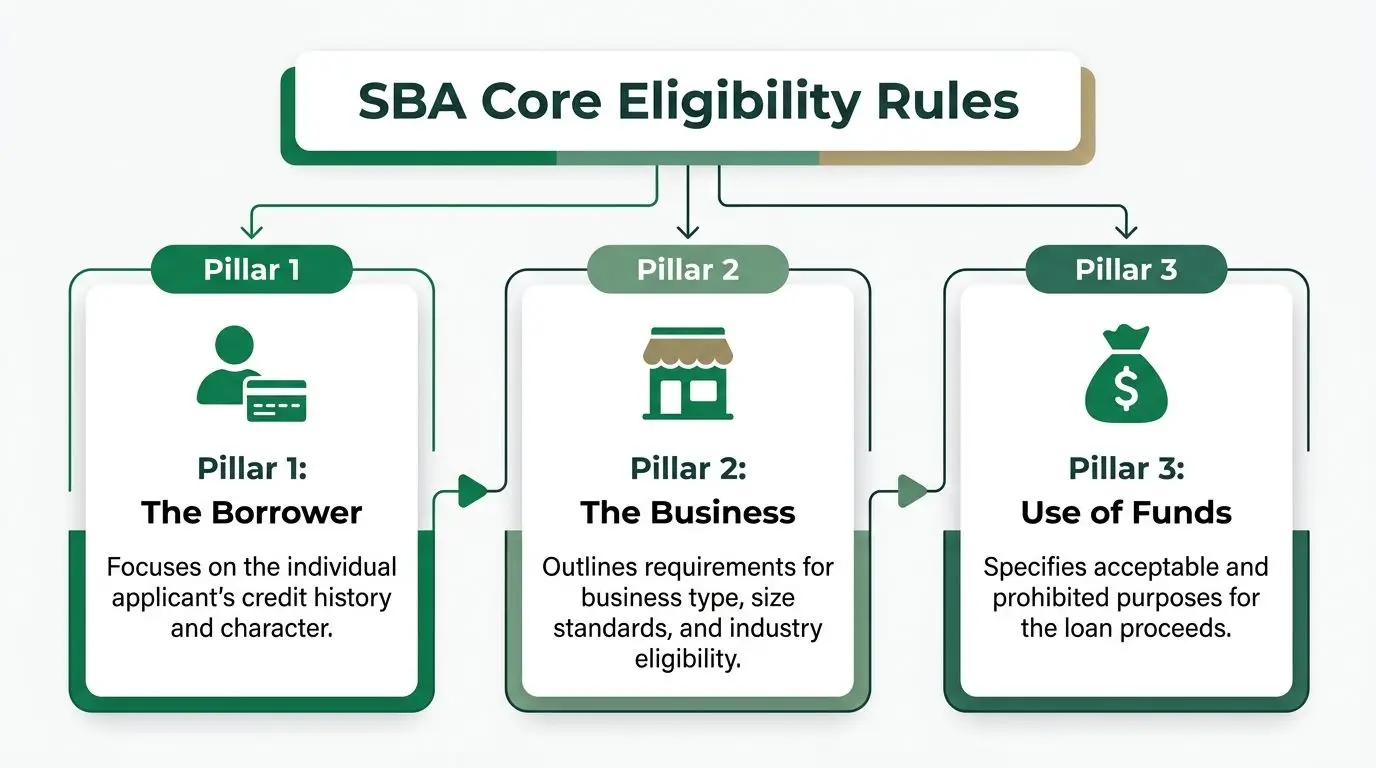

The Foundation SBA's Core Eligibility Rules

The cleanest way to understand SBA minimum requirements is to group them into three pillars: the borrower, the business, and the project.

The Borrower

At the borrower level, the SBA and lenders are asking a simple question: who is standing behind this obligation?

The clearest rule is that any owner with 20% or more equity must provide an unconditional personal guaranty under SBA 7(a), and lenders must also verify that the business is for-profit, legally registered, operating in compliance with applicable laws, and primarily located in the United States, as summarized by Lendio's overview of SBA loan requirements. If you want a deeper practical breakdown of how guaranties affect ownership groups, this guide on SBA personal guarantee requirements is useful.

That rule matters because many borrowers treat ownership percentages as paperwork. Lenders don't. They treat ownership as risk allocation.

The Business

The business itself has to fit SBA eligibility. That means a real operating company, organized legally, run for profit, and based primarily in the United States.

There's also a size test. If industry-specific size standards don't apply, the SBA's alternative size standard says the applicant's tangible net worth must not exceed $15 million and average net income after federal income taxes for the two full fiscal years before application must not exceed $5.0 million, according to the SBA SOP 50 10 7.1.

A lot of otherwise strong companies miss this point. A business can be profitable and still fail SBA eligibility if its balance sheet or earnings place it outside the program.

The Project

Then comes the project itself. What are you financing, and does that use of proceeds make sense under SBA rules and lender logic?

Common SBA uses include acquisitions, working capital, partner buyouts, equipment, and owner-occupied real estate. But even an allowed use of proceeds can fail if the structure doesn't hold together. A lender wants a clean story: sensible purchase price, credible borrower contribution, realistic repayment, and no hidden issues inside the transaction.

Practical rule: Strong SBA deals are coherent. The borrower fits, the business fits, and the use of funds fits. If one pillar is weak, the rest of the file has to work harder.

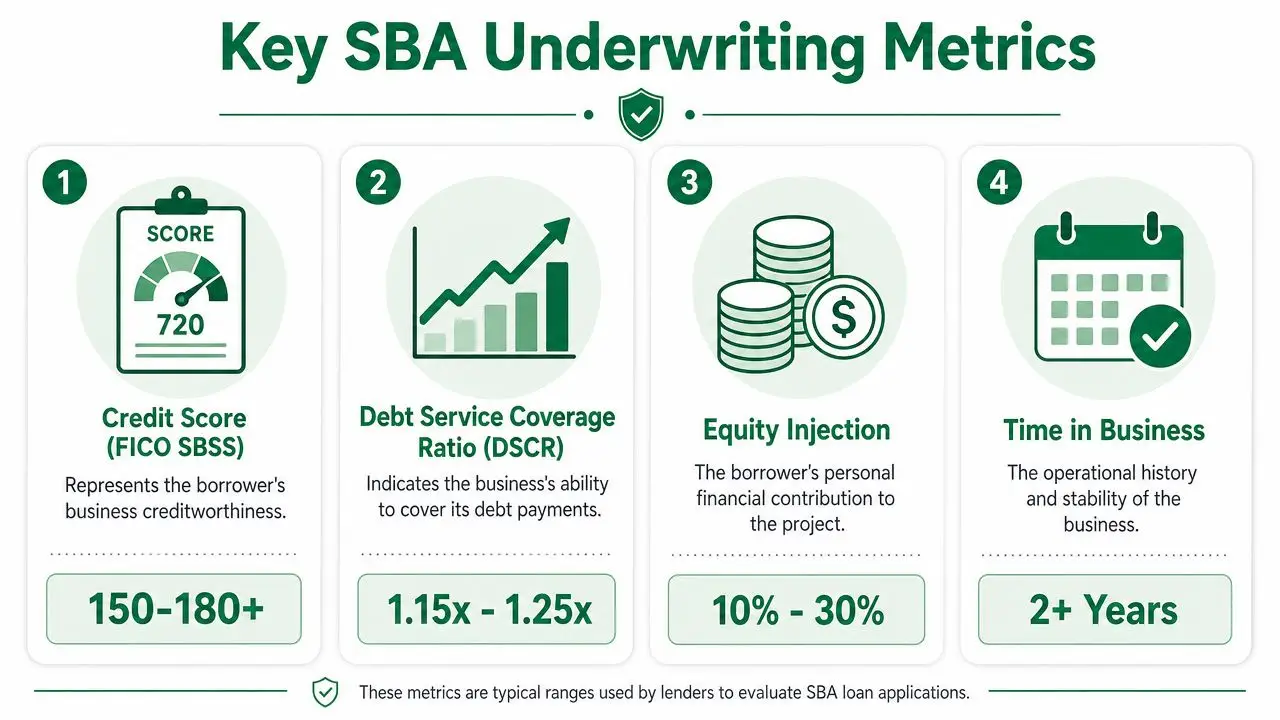

Key Underwriting Metrics You Must Meet

Rules decide whether your deal is eligible. Metrics decide whether it's financeable.

The numbers lenders look at first

On the front end, lenders usually zero in on credit, time in business, revenue, and cash flow.

According to Newity Market's summary of 7(a) minimum requirements, the baseline framework includes $100,000 in average annual gross revenue, a minimum FICO score of 600 for majority owners, and operational history of two years for loans up to $350,000 and three years for loans over $350,001. The same source notes that for loans under $350,000, the SBA uses the FICO Small Business Scoring Service with a score of 165 or higher out of 300 for prescreening.

Those are minimums. In practice, lenders often want a cleaner file than the published floor suggests. The same source notes many lenders prefer FICO scores between 680 and 700, though some will consider 640+ when the financials are strong.

That distinction matters. A borrower at the minimum may still be technically eligible, but that profile usually needs compensating strengths elsewhere, such as stronger cash flow, more liquidity, more experience, or a simpler transaction.

What DSCR really means in underwriting

The most important underwriting metric is usually Debt Service Coverage Ratio, or DSCR.

Per NerdWallet's SBA loan requirements guide, for 7(a) loans greater than $500,000, borrowers must show a DSCR of at least 1.15x, which means available operating income must be 15% higher than current debt obligations. That same source explains that the SBA has replaced the legacy SBSS score with DSCR as the primary cash flow metric for many loans. Newity Market adds practical lender context: most lenders want 1.15x to 1.25x, meaning the business generates $115 to $125 in cash flow for every $100 in annual debt payments.

A simple way to grasp this is:

- If cash flow is tight: lenders assume the first disruption will create a repayment problem.

- If DSCR is barely above minimum: the deal may still work, but the lender will scrutinize add-backs, existing debt, and post-close working capital.

- If DSCR is healthy: the rest of the file gets easier.

If you want a borrower-friendly explanation of how lenders calculate this metric, review what DSCR means for SBA approval.

Cash flow repays loans. Collateral only reduces damage if cash flow fails.

SBA Loan Programs A Head-to-Head Comparison

Borrowers often ask for “an SBA loan” as if there's one product. There isn't. The right program depends on what you're buying, how fast you need to move, and how the deal pencils out.

Program comparison table

| Program | Typical use | Max loan size | Guarantee detail | Minimums and practical notes |

|---|---|---|---|---|

| SBA 7(a) | Acquisitions, working capital, refinance, partner buyouts, real estate, equipment | $5 million under the standard program, per CapBench's 7(a) guide | 85% on loans up to $150,000 and 75% on loans above $150,000, per the same source | Broadest use-case program. Best when flexibility matters more than fixed-rate real estate structure. |

| SBA 504 | Owner-occupied commercial real estate and major equipment | Not detailed here with a verified figure | Not detailed here with a verified figure | Best fit when the core asset is real estate or major equipment and the project supports the 504 structure. |

| SBA Express | Faster-turn working capital and smaller needs | Not detailed here with a verified figure | Not detailed here with a verified figure | Useful when speed matters, but lenders still underwrite risk carefully. |

| SBA Microloan | Smaller business needs and early-stage uses | Not detailed here with a verified figure | Not detailed here with a verified figure | More limited in size and scope. Often not the right fit for acquisition transactions. |

The key point is that 7(a) is the most flexible platform. It's the program most borrowers use for acquisitions, recapitalizations, and situations where the financing package needs to cover multiple purposes at once.

Which program fits which deal

If you're buying a business, 7(a) is usually the first place to look because it can handle intangible-heavy transactions. That's why it dominates acquisition financing.

If you're buying a building that your business will occupy, 504 often deserves serious consideration. The structure is geared toward long-term fixed-asset financing rather than general-purpose flexibility. Borrowers evaluating that route should understand how SBA 504 financing works for real estate and equipment.

Express is a conversation about speed and convenience. It can be attractive when the need is straightforward and the borrower values faster processing. But borrowers shouldn't confuse a simplified product with reduced scrutiny. Lenders still want to see a file they can defend.

Microloans serve a different borrower profile altogether. They can help when the capital need is smaller and the business is earlier-stage, but they're often not the ideal answer for someone trying to close an acquisition or structure a complex expansion.

A practical way to choose:

- Buying a business: Start with 7(a).

- Buying owner-occupied property: Compare 7(a) against 504.

- Need faster access for a smaller request: See whether Express is realistic.

- Need modest capital and your deal is simple: A microloan may be worth exploring.

The mistake is picking the program by brand name instead of deal logic. Good borrowers start with the use of proceeds, repayment source, and closing timeline, then back into the product.

Understanding Equity Injection and Collateral

For many borrowers, the hardest part of SBA minimum requirements isn't credit. It's cash to close.

How equity injection gets structured

For 7(a) business acquisitions and startup financing, a foundational rule is a 10% equity injection of total project costs, and for acquisitions that often means at least 5% must be the borrower's own cash while the remainder can come from other sources, such as a seller note, according to Funding Fred's SBA 7(a) eligibility breakdown.

That one rule changes how deals get assembled.

In plain terms, lenders want to see that the buyer is financially committed. A borrower who brings cash to closing has real skin in the game. For acquisitions, that contribution can sometimes be structured more efficiently than borrowers expect. A seller note on acceptable standby terms can help fill part of the required injection, which is why deal structure matters as much as the raw down payment amount.

If you're working through that math, this guide on SBA equity injection for acquisitions is a practical reference.

A weak equity story makes lenders question the whole deal. A clean equity story makes the file feel safer before they even finish the cash flow analysis.

What collateral does and does not do

Borrowers often overestimate collateral and underestimate liquidity.

Collateral helps. It gives a lender additional support. But collateral usually does not rescue a business that can't demonstrate credible repayment ability. A strong cash flowing business with a sensible structure is more financeable than a deal with excessive debt backed by assets the lender may never want to liquidate.

That's why experienced lenders ask different questions than borrowers do. Borrowers ask, “Do I have enough collateral?” Lenders ask, “If this business hits a rough patch, is there enough earnings cushion, owner commitment, and structure discipline to get through it?”

When collateral is tight, the conversation shifts to the overall package: guarantor strength, liquidity after close, industry stability, and whether the buyer is stretching to get the deal done. What works is balance. What doesn't work is trying to cover a thin file with asset value alone.

The Lender Overlay Why SBA Minimums Are Just the Start

The SBA sets the floor. Every lender builds its own ceiling.

Why eligible deals still get declined

A borrower can satisfy core SBA minimum requirements and still get turned down repeatedly. That isn't a contradiction. It's underwriting.

Banks apply overlays. They may avoid certain industries, dislike thin post-close liquidity, prefer larger or smaller deal sizes, or get uncomfortable with first-time operators buying businesses that need immediate operational cleanup. None of those judgments necessarily means the deal is impossible. It means the deal doesn't fit that lender.

Borrowers frequently waste the most time. They assume one decline means the transaction is dead, or they assume every SBA lender looks at risk the same way. Neither is true.

A lender's “credit box” is a mix of policy and appetite. Two banks can read the same file and reach different conclusions because they emphasize different risks.

What competitive lenders usually want

Competitive lenders generally want a file that is not just eligible, but easy to defend. That usually means:

- Clear borrower fit: relevant management or industry experience, clean ownership, and straightforward guarantor support.

- Convincing repayment story: earnings that hold up under scrutiny, with realistic assumptions and no aggressive adjustments.

- Orderly deal structure: clean injection, credible purchase logic, and enough room after closing for the business to operate normally.

- Full documentation early: missing tax returns, stale financials, and vague explanations slow the process and raise doubt.

One option borrowers use when they need lender matching and underwriting guidance is GoSBA Loans, which provides educational material on how SBA lenders underwrite deals. The broader lesson is more important than the tool: lender selection is a credit strategy, not an administrative step.

The right lender asks, “How do we structure this correctly?” The wrong lender says no after six weeks of document requests.

The unwritten rules are simple. Lenders like clarity. They like conservative assumptions. They like borrowers who know their numbers, know their role after closing, and aren't trying to force a structure that doesn't belong in the program.

Common Questions About SBA Minimum Requirements

Can I qualify with credit issues or a past bankruptcy

Sometimes. But the answer depends on the full file, not the blemish alone.

A low score, prior credit event, or messy background doesn't automatically end the conversation if the rest of the package is strong. Lenders look at recency, explanation, current repayment behavior, liquidity, and whether the business cash flow is solid enough to offset concern. What doesn't work is pretending the issue won't come up. Underwriters want a direct explanation and supporting context.

If your file has a weakness, the practical move is to strengthen the parts you can control: clean financial statements, documented cash flow, realistic projections when needed, and a clear explanation letter.

What if my business is new or my ownership is complicated

New businesses face a tougher path because lenders have less operating history to underwrite. That doesn't mean every newer deal is impossible. It means the burden shifts to experience, capitalization, and structure quality.

Ownership complexity creates a separate issue. The biggest recent change is citizenship and ownership compliance. According to Fundera's SBA loan requirements guide, the 2025 SBA rule change mandates 100% U.S. ownership for businesses receiving SBA loans, invalidating prior guidance that allowed up to 49% non-citizen ownership.

That rule has real consequences for investor-heavy deals. Entrepreneurs with foreign investors often assume they're automatically excluded from any path forward. The fact is that the ownership and deal structure have to be reviewed carefully before an application ever goes in. If the equity stack is wrong, the deal can fail before underwriting gets started.

Do I need a business plan

Not every lender treats the business plan the same way, but strong narrative documents help more than most borrowers think.

A business plan matters most when the file needs interpretation. That includes acquisitions with a first-time buyer, expansion loans where growth assumptions need support, or any deal where the lender must understand why the business will perform well after closing. A good plan is not marketing copy. It's an underwriting document. It explains the model, management, customers, transition plan, and repayment logic in a way credit teams can follow.

Borrowers get better results when the documents all tell the same story. Tax returns, interim statements, projections, LOI terms, and the written narrative should reinforce each other rather than introduce new questions.

If you're evaluating a deal and want a practical read on whether it fits SBA guidelines and lender expectations, GoSBA Loans can help you pressure-test the structure, compare lender fit, and identify issues before they slow down underwriting.