You've likely run into this already. You found a business that fits your experience, the cash flow looks workable, and the seller's asking price isn't outrageous. Then the financing quotes come in, and there's a gap between what the lender will support, what you can put down, and what the seller wants to net at closing.

That gap kills a lot of otherwise good deals.

Seller financing for business acquisition is often what keeps the transaction alive. In plain English, the seller agrees to get paid for part of the purchase price over time instead of demanding all cash at close. In an SBA deal, that can be useful. In the right structure, it can also be decisive.

Most articles stop at the definition. The main point is whether the note helps the deal get approved, how the lender will treat it, and what terms are effective in underwriting. That's where buyers get tripped up.

Table of Contents

- Why Seller Financing Can Make Your Deal Possible

- The Four Main Types of Seller Financing Explained

- How Seller Financing Works with an SBA Loan

- Structuring and Negotiating Your Seller Note

- Key Advantages and Risks for Buyers and Sellers

- Essential Legal Documents and Due Diligence

- Common Pitfalls and How to Avoid Them

Why Seller Financing Can Make Your Deal Possible

You find a good business. Cash flow is there. The lender likes the industry, likes the historical numbers, and still stops short of the total amount needed to close. That is a normal acquisition problem, especially in SBA deals where the bank is watching debt service, buyer liquidity, and post-close working capital all at once.

Seller financing often solves that problem better than forcing more buyer cash into the deal.

The practical reason is simple. A seller note can fill the gap between what the lender will support and the price the seller expects, without stripping the business of the cash the buyer needs after closing. In many lower middle market and main street transactions, seller paper is part of the structure because it keeps the deal financeable.

It also changes the lender's view of the file. When a seller is willing to carry a note, the bank sees a seller who still has money at risk after closing. That does not replace due diligence, and it does not fix weak earnings, customer concentration, or a bad valuation. It does help when the business is sound but the structure needs one more layer to work.

In SBA acquisitions, that point matters more than many buyers realize. Seller financing is not just a convenience. Used correctly, it can help satisfy equity injection requirements, reduce the buyer's cash burden, and improve the odds of approval. Used incorrectly, it can do the opposite. If the note is not on full standby when the lender requires it, or if the repayment terms create too much pressure on post-close cash flow, the same note that was supposed to help can kill the deal.

That is why experienced buyers do not ask only, "Will the seller carry paper?" They ask, "Will the seller carry it in a way the SBA lender will approve?"

For buyers trying to find acquisition financing solutions, seller paper is usually one layer in the capital stack, not the whole answer. It works alongside buyer equity, senior debt, and sometimes rollover or earnout mechanics. If you are comparing options, this guide on how to finance a business acquisition gives the broader funding picture.

A good seller note does three jobs at once. It helps bridge valuation and lending gaps, shows lender-friendly seller confidence, and preserves buyer liquidity for the first year of ownership, which is where many otherwise good acquisitions get into trouble.

Seller financing structures at a glance

The Four Main Types of Seller Financing Explained

A seller can say, “I'll carry paper,” and still mean four very different things. That distinction matters because lenders underwrite each structure differently, and some forms of seller financing help an SBA deal while others create more review, more documents, and more post-close risk.

| Financing Type | How It Works | Best For | SBA Treatment |

|---|---|---|---|

| Seller note | Seller finances part of the purchase price through a promissory note with scheduled repayment | Straightforward price gap between available cash and total deal value | Usually acceptable if documented properly and coordinated with the senior lender |

| Earnout | Part of the seller's payment depends on post-close performance | Deals with uncertainty around future revenue, margin, or customer retention | Needs close review because contingent payments can complicate underwriting and post-close monitoring |

| Standby note | Seller note is subordinated and repayment is delayed under lender-required terms | SBA acquisitions where the note is being used to support approval or reduce buyer cash burden | Critical in SBA structures when the lender requires standby treatment |

| Consulting or employment agreement | Seller receives compensation post-close for transition help or ongoing services | Transactions where the seller's know-how or relationships are central to continuity | May be permitted, but it must reflect real services and cannot be used carelessly as disguised purchase price |

How these structures behave in a real deal

The plain seller note is the simplest form. The seller finances part of the purchase price, and the buyer repays that amount under a note with defined payment terms. In practice, this structure is often used to close a valuation gap or preserve buyer cash at closing. It is also the version buyers misunderstand most often, because a standard amortizing note and an SBA-friendly standby note are not the same thing.

The earnout shifts part of the price into the future and ties it to performance after closing. That can solve a real pricing dispute. It can also create one. If the earnout formula depends on EBITDA adjustments, customer retention, or gross margin definitions that are not precise, the parties are setting up a disagreement before the deal even closes.

The standby note is the most important version for SBA buyers. It is still seller debt, but the lender may give it much better treatment if the terms fit SBA requirements and the bank's credit standards. Buyers who want to minimize cash in need to understand this structure early. Our guide to SBA seller note rules and 5 percent down deal structures explains where standby treatment can help and where it will not.

The consulting or employment agreement sits in a different category. Sometimes it is legitimate compensation for transition support, customer handoff, licensing help, or training. Sometimes parties try to use it to move purchase price into a form that looks operational instead of financed. Lenders usually spot that quickly. If the seller is being paid for “advisory help,” the file needs to show real duties, a market-based payment level, and a business reason for keeping the seller involved.

One more distinction matters. Subordinated debt gets paid after the senior lender. Pari passu debt shares priority with the senior lender. In SBA acquisition loans, seller paper generally needs to sit behind the bank, because the lender wants free cash flow protecting the SBA note first, not splitting repayment priority with the seller.

A good structure does more than explain how the seller gets paid. It shows the lender why the business can handle the debt stack if year one comes in tight.

How Seller Financing Works with an SBA Loan

In an SBA 7(a) acquisition, seller financing is not just a convenience. It's part of the lender's risk analysis. The note can help the file, but only if it fits SBA rules and the bank's credit box.

Here's the key point. In SBA 7(a) acquisitions, a seller note only counts toward the buyer's equity injection if it is fully subordinated and on full standby for the entire SBA loan term, meaning no principal or interest payments are made during that period.

That rule changes how you negotiate the note from day one.

A simple visual helps show where the note belongs in the stack:

What full standby actually means

Buyers often hear “standby” and assume it means reduced payments or interest-only payments. That's not what full standby means in this context. It means no payments on the seller note while the SBA-required standby period is in effect.

From the lender's standpoint, that changes the nature of the obligation. If the business doesn't have to service the seller note during the SBA term, the cash flow is available to support the senior loan. That's why lenders may treat the seller paper more like support capital than active debt.

Many deal drafts go sideways at this point. The LOI says the seller will “carry part of the note,” but nobody has confirmed whether the seller will accept full standby. Later, the lender says the structure only works if the note is fully subordinated and receives no payments. Then the seller pushes back because they expected monthly income right after closing.

Why lenders care so much about the note

Lenders are not trying to make the note inconvenient. They're trying to make sure the business can survive the first years after transfer. SBA acquisitions already carry transition risk. Adding immediate seller payments can tighten debt service too far, especially when the buyer also needs working capital and a buffer for surprises.

That's why the seller note often operates as a credit signal. If the seller is willing to subordinate and wait, the lender sees confidence in the business and alignment with the deal.

A more detailed look at SBA seller note rules and how to buy a business with lower cash down is useful if you're trying to determine whether your planned note helps approval or just adds complexity.

Later in the process, it can help to hear this explained verbally before you negotiate final terms:

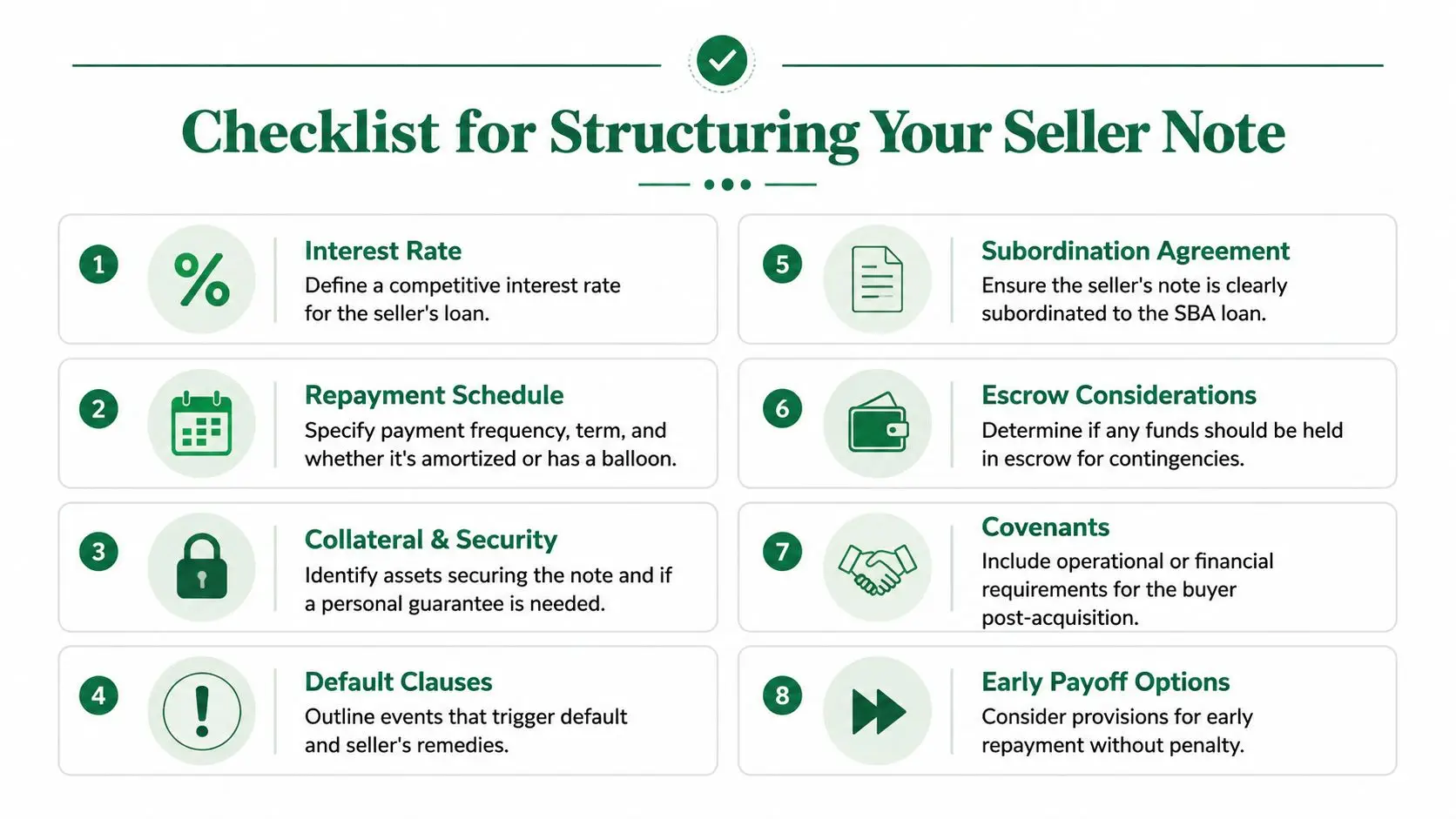

Structuring and Negotiating Your Seller Note

A seller note gets negotiated twice. First by the buyer and seller in the LOI and purchase agreement, then again by the SBA lender when the file hits underwriting. The second negotiation is the one that decides whether the deal closes.

That is why smart buyers do not start with rate or term. Start with lender treatment. If the note is supposed to help with SBA equity injection, the lender may require full standby for a defined period and no payments of principal or interest during that time. If the note is just additional subordinated debt, the lender may allow payments, but only if cash flow supports them and the intercreditor terms are clean.

What to negotiate first

The first question is simple. Is this note being used to reduce buyer cash into the deal, or is it only part of the purchase price stack?

If it is being used to satisfy part of the equity injection, structure drives approval. SBA lenders usually want the seller note on full standby. No scheduled payments. Clear subordination. Documents that match the lender's closing requirements. A seller who expects monthly income right after closing is negotiating against the capital stack.

Once that point is settled, the rest of the note can be shaped around actual risk:

- Payment status: Full standby, interest-only after a hold period, or amortizing payments. This affects debt service coverage from day one.

- Term and balloon: Longer maturities reduce pressure on the business. Short balloons can create a refinancing problem before the new owner has stabilized operations.

- Interest accrual: Some sellers accept accrued interest during standby if it improves headline economics without hurting early cash flow.

- Subordination language: The senior lender will want this drafted tightly. Loose language causes closing delays.

- Default provisions: Cross-default terms need to be coordinated with the SBA loan so one technical issue does not trigger multiple problems at once.

- Security: Many sellers ask for a junior lien or pledge rights, but those rights always sit behind the senior lender.

A good seller note solves a deal problem. A bad one creates a new underwriting problem.

Where negotiations usually break down

The friction usually comes from mismatched expectations, not bad intent. Sellers hear "note" and think income stream. Lenders hear "seller note" and ask whether it is subordinated, on standby, and documented in a way that protects cash flow.

I have seen buyers lose months because they negotiated seller-friendly economics before asking the bank one direct question: "Will this note count the way we think it will count?" That answer changes the structure, and sometimes the valuation discussion with it.

A disciplined buyer should handle the note in this order:

- Get lender guidance before finalizing economics. Confirm whether the note will be standby, partially deferred, or currently paying.

- Match payments to the business cycle. Seasonal cash flow, customer concentration, and working capital swings matter more than abstract note terms.

- Preserve cash after closing. The first year often includes inventory timing issues, employee turnover, and customer handoff risk.

- Tie the documents together. The LOI, purchase agreement, promissory note, and subordination agreement should say the same thing in practical terms.

- Use the note to bridge a gap you can explain. It works well when the seller wants a higher price than the lender will finance in senior debt, but the business can still support the structure.

If the seller wants premium pricing, seller paper is often how that premium gets financed without forcing the buyer to bring in more cash.

Vague drafting is where good deals start to slip. "Seller to carry a note on reasonable terms" is not enough. The note terms should be clear before the file goes deep into underwriting, especially if the SBA structure depends on standby treatment or a specific equity injection calculation.

Key Advantages and Risks for Buyers and Sellers

Seller financing works because it aligns interests, but it also leaves both sides exposed in ways an all-cash deal doesn't. The value is real. So is the risk.

Where buyers benefit and where they get hurt

For buyers, the biggest advantage is flexibility. A seller note can reduce the cash you need to bring in, preserve liquidity for operations, and help bridge a valuation gap that a bank won't finance on its own.

It can also improve the human side of the transition. When the seller still has money tied to the company, they're often more invested in training, handoff quality, and customer continuity.

The risk is that buyers sometimes treat seller financing as cheap capital when it's expensive complexity. If the business already has tight coverage, another layer of obligations can crowd out working capital. The other risk is relational. A seller who stays economically involved after closing may also stay emotionally involved.

Why sellers agree and why they hesitate

Sellers agree to finance part of the purchase price for a few practical reasons. It can widen the buyer pool, support the asking price, and create interest income over time. In some structures, deferred payment may also affect the timing of taxable gain, which is why sellers almost always need tax advice before agreeing to installment-style proceeds.

But the seller is taking real repayment risk. If the buyer underperforms, the seller becomes a creditor behind the senior lender. Recovering value after default is rarely simple, especially when customers, employees, and goodwill have already shifted under new ownership.

A fair negotiation usually recognizes both truths:

- Buyer upside: Lower upfront cash and a better chance of getting the deal done

- Buyer risk: Increased financial commitment and possible post-close friction

- Seller upside: Better closeability and often stronger pricing support

- Seller risk: Delayed proceeds and exposure to buyer execution risk

That's why the best seller-financed deals are not the most aggressive ones. They're the ones where repayment terms match actual business performance and both sides understand what happens if the transition goes badly.

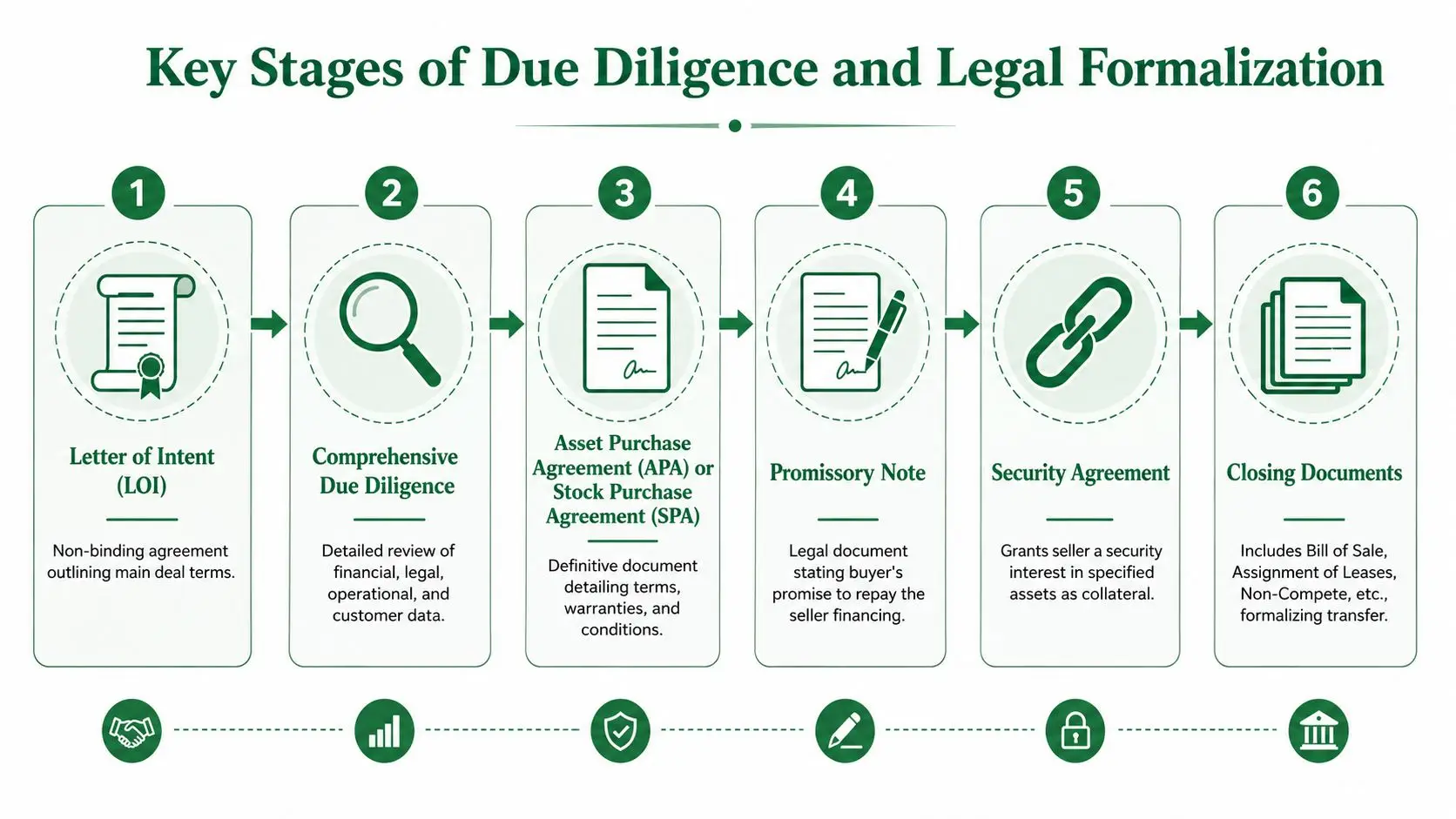

Essential Legal Documents and Due Diligence

A seller note can help get an SBA acquisition approved, but sloppy documentation can kill the deal late. I see this happen when the buyer and seller agree on economics, then discover the lender needs different standby language, tighter subordination terms, or clearer collateral provisions before credit will sign off.

At closing, the paper has to match the structure the lender underwrote. If the note, purchase agreement, and SBA requirements point in different directions, counsel ends up rewriting documents under deadline and both sides start losing confidence.

The documents that matter most

The asset purchase agreement sets the legal and economic foundation. It should line up with the LOI on price, allocation, working capital treatment, assumed liabilities, transition support, and any seller holdbacks or contingent payments. In an SBA deal, this agreement also needs to fit the lender's approval exactly, especially if part of the buyer injection is coming from a seller note on full standby.

The promissory note controls repayment. It should state principal, interest rate, amortization, maturity, payment dates, default triggers, cure periods, and remedies. If the note is intended to count toward equity injection under SBA rules, the standby language cannot be vague. Lenders look closely at whether principal and interest are deferred for the required period and whether the note terms conflict with cash flow assumptions.

The subordination agreement is often the document that makes the structure workable. The senior lender wants its lien priority and payment rights protected. The seller needs to understand what rights are being postponed, when payments can resume, and what happens after a default.

The security agreement and related UCC filings matter if the seller is taking a junior secured position. Some sellers ask for collateral without appreciating how little control that gives them behind a senior SBA lender. A junior lien may still be worth having, but it is not the same as practical recovery power.

The personal guarantee deserves real attention. Sellers often want one. Buyers often treat it as boilerplate until they understand they may still owe the note even after the business underperforms or shuts down.

Due diligence has to support the note

A seller note is only as good as the company's post-close cash flow. That makes diligence more than a checklist exercise. Buyers need to verify earnings quality, customer concentration, payroll burden, seasonality, deferred maintenance, tax exposure, and any working-capital pressure that could leave the business short right after closing.

For a practical framework, use this SBA acquisition due diligence checklist alongside broader guidance on understanding M&A due diligence.

Tax treatment also needs to be documented cleanly. Deferred payments, consulting agreements, and earn-outs can be taxed differently depending on how they are drafted and how the parties operate after closing. Agile Legal discusses this well in its analysis of seller financing options in M&A transactions. If compensation, purchase price, and contingent consideration are blurred together, expect disputes with the other party, the lender, or the CPA.

One more point matters in SBA transactions. If the seller note includes standby, partial standby, or payment restrictions tied to debt service coverage, those terms should appear consistently across the note, the lender's agreements, and the closing instructions. Lenders do not like side understandings.

Separate counsel matters here. Buyer's counsel should protect the buyer. Seller's counsel should protect the seller. One lawyer trying to keep it simple usually leaves important terms unclear.

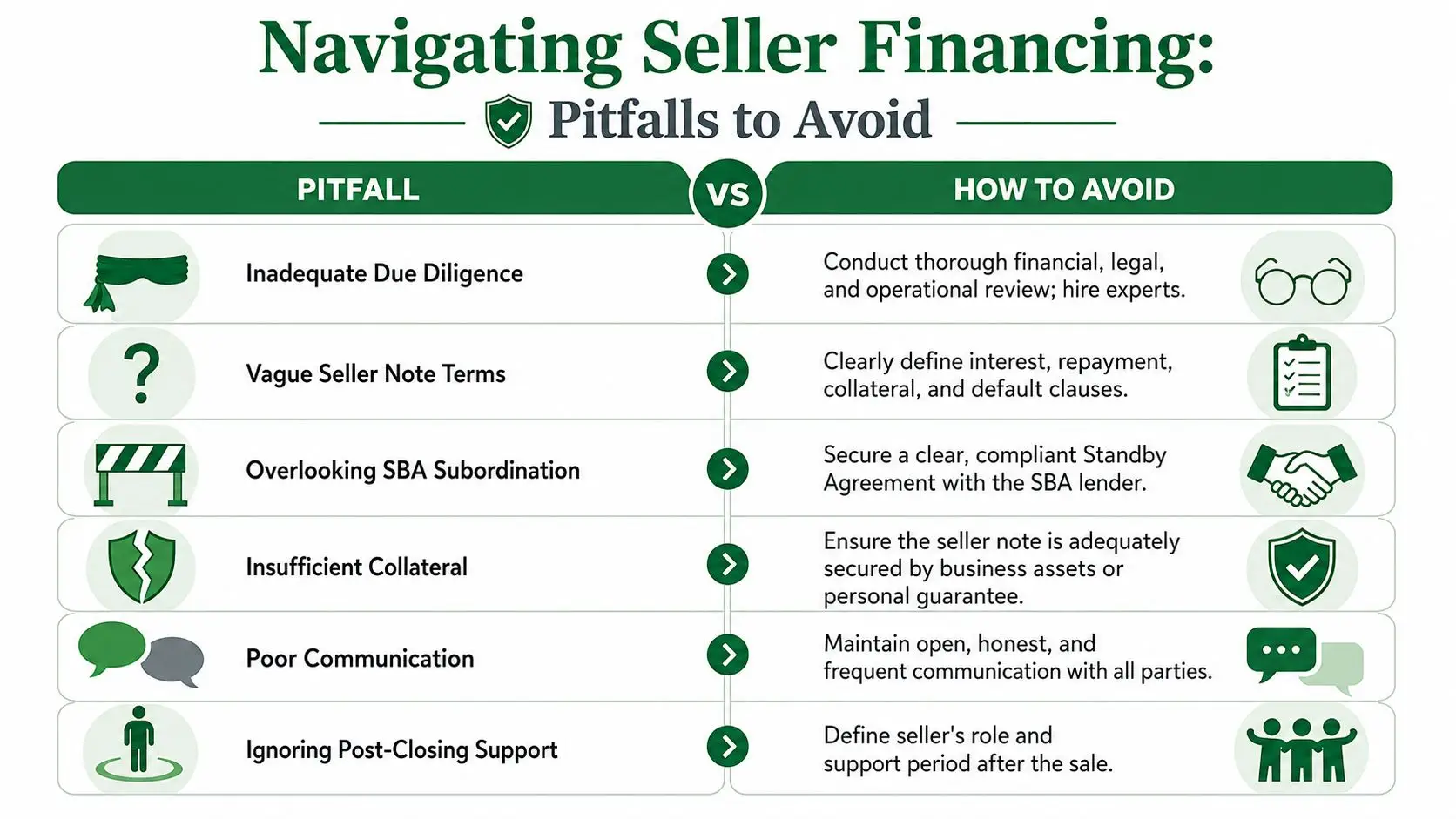

Common Pitfalls and How to Avoid Them

Most seller-financed deals don't fail because the concept is flawed. They fail because the structure was never made lender-ready, or because the parties used vague language where precision was required.

A point many buyers miss is that seller financing terms, especially standby requirements, can directly affect SBA lender approval. Some guidance explains typical note terms but doesn't explain that in an SBA deal the seller note isn't just flexible capital. It's also a quality signal that has to fit underwriting standards, as discussed in MidStreet's buyer financing guidance.

The mistakes that derail approvals

A frequent problem is negotiating with the seller before confirming lender parameters. The buyer gets an LOI signed, the seller expects immediate note payments, and the lender later requires standby or a different subordination package.

Another problem is overleveraging the business. Buyers focus on getting to closing and underestimate how much cash the company needs after the handoff. If the debt stack only works on a best-case model, it isn't durable.

Poorly drafted contingent payments are another trap. Earn-outs, offsets, and transition compensation can all be legitimate, but if the measurement method is fuzzy, the dispute starts the month the first report is due.

What disciplined buyers do differently

Buyers who get these deals done usually keep to a few habits:

- Get lender feedback early: Don't assume the note you and the seller like will be bankable.

- Model downside cash flow: Test the business with conservative assumptions before adding another payment layer.

- Define post-close roles clearly: If the seller is consulting, specify duties, duration, and compensation.

- Document default mechanics carefully: Everyone should know what happens after a missed payment, covenant breach, or lender default.

The strongest seller-financed deals are boring on paper. That's a compliment. Clean terms, realistic repayment expectations, lender-compliant subordination, and precise documents beat “creative” structures almost every time.

If you're buying a business and want to minimize cash outlay without building a structure that an SBA lender will reject, GoSBA Loans can help you evaluate the deal, shape the capital stack, and match the transaction with lenders that understand standby seller notes, acquisition underwriting, and what gets funded.

Produced via Outrank app