You found a business that looks right. The seller's numbers are believable, the industry makes sense, and you can see yourself running it. Then the financing question hits, and that's where many first-time buyers realize a good deal on paper isn't the same as a financeable deal.

For most lower middle market and main street acquisitions, the center of gravity is the SBA 7(a) loan. The SBA reported 103,000 financings to small businesses in FY 2024 with $56 billion in annual capital impact, up 7% from FY 2023, and noted that growth was partly driven by smaller 7(a) loans, which is one reason ownership transfers and business purchases continue to fit naturally inside the program's lane, according to the SBA 2024 Capital Impact Report.

That matters because a seller usually isn't offering a company with perfect hard collateral. Many acquisitions are built on cash flow, customer relationships, location, licensing, staff continuity, and goodwill. Conventional lenders often get tight around that mix. SBA lending exists partly to bridge that gap.

Table of Contents

- Your Starting Point for an SBA Loan Business Acquisition

- SBA 7(a) vs 504 Loans for Buying a Business

- Qualifying for an SBA Acquisition Loan

- Creative Deal Structures That Get Funded

- Inside the SBA Underwriting and Approval Process

- The Acquisition Timeline from LOI to Closing

- Your SBA Loan Application Checklist

- Avoiding Common SBA Deal Killer Pitfalls

Your Starting Point for an SBA Loan Business Acquisition

An SBA loan business acquisition starts well before the loan application. It starts when you decide whether the business is merely attractive or actually financeable.

The practical difference is huge. A business can have clean branding, a persuasive broker package, and a seller who says all the right things. None of that matters if the cash flow won't support new debt, the purchase price isn't defensible, or the structure conflicts with SBA rules. Buyers who understand that early save time, legal spend, and emotional energy.

What makes SBA financing so useful is flexibility. In acquisition work, the 7(a) program can handle a full or partial change of ownership, and it can often package the purchase itself with working capital and, in some deals, real estate. That makes it a far better fit than trying to patch together separate facilities with mismatched terms.

Practical rule: The lender isn't financing your excitement. The lender is financing a transfer of a business that has to keep performing after the seller is gone.

A good acquisition loan package answers three questions at once:

- Can you run it? Lenders want a buyer whose background fits the target.

- Can the business carry it? Historical performance matters more than optimistic stories.

- Can the deal close cleanly? The purchase agreement, seller terms, lease, and ownership structure all have to line up.

That's why experienced SBA borrowers don't ask only, “Can I get approved?” They ask, “How should this deal be built so approval is realistic?”

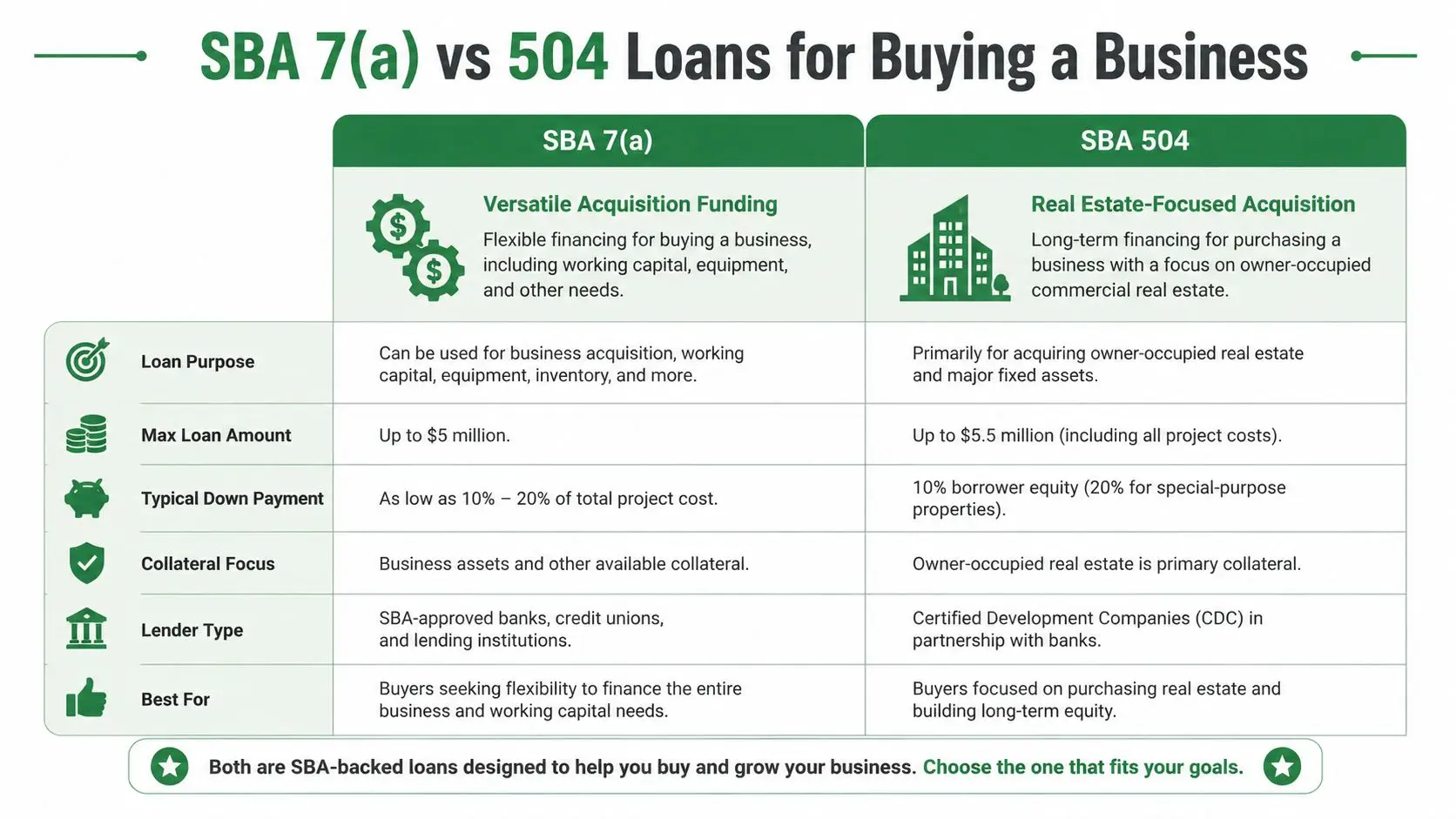

SBA 7(a) vs 504 Loans for Buying a Business

Why 7(a) usually wins for acquisitions

For most business purchases, SBA 7(a) is the main tool. The SBA states that 7(a) can be used for a complete or partial change of ownership, with most loans capped at $5 million, guarantees of up to 85% for loans of $150,000 or less and 75% above that, and standard maturities of up to 10 years for acquisitions and up to 25 years when real estate is included, according to the official SBA 7(a) program page.

That flexibility is the reason acquisition brokers, lenders, and M&A advisors usually start with 7(a). If the transaction includes purchase price, working capital, inventory, equipment, and possibly owner-occupied real estate, 7(a) can often hold all of that in one structure.

By contrast, 504 is narrower. It's a strong tool when fixed assets, especially owner-occupied commercial real estate, drive the project. It is not usually the first answer when you're buying an operating company based mainly on cash flow and goodwill.

| Feature | SBA 7(a) Loan | SBA 504 Loan |

|---|---|---|

| Primary use in acquisitions | Broad acquisition financing | Fixed-asset-heavy projects |

| Best fit | Business purchase plus operating needs | Real-estate-centered transactions |

| Can include goodwill | Yes, commonly | Not the natural fit |

| Can include working capital | Yes | Generally not the core use |

| Structure style | One facility can cover several uses | Usually part of a larger capital plan |

A strong overview of the 7(a) structure is in this SBA 7(a) loan guide.

When 504 belongs in the conversation

If the business purchase is tied closely to owner-occupied property, 504 may still matter. In practice, this comes up when real estate is central to value and long-term strategy. Think manufacturing, certain industrial users, some medical practices, and businesses where control of the premises is part of the acquisition thesis.

Here's a clear way to understand:

- Use 7(a) when the operating business is the deal and the loan needs to finance goodwill, transition, and working capital.

- Use 504 when the fixed asset component is large enough that a real-estate-focused structure deserves separate analysis.

- Use both concepts carefully when the transaction has mixed priorities and the property strategy affects the business value.

The wrong loan choice usually shows up as friction in underwriting. The right one feels coherent from the LOI forward.

Buyers get in trouble when they choose 504 because they heard it has attractive real estate economics, then try to force an acquisition structure around it. If the transaction is mostly a business purchase, not a property project, 7(a) is usually the cleaner answer.

Qualifying for an SBA Acquisition Loan

A lender underwrites three things at once in an acquisition. The buyer, the business, and the deal structure. Weakness in one area can be overcome, but weakness in all three usually kills the file.

The buyer must make sense on paper and in person

Relevant experience matters. It doesn't have to be a carbon copy of the target industry, but the lender needs a credible operating story. If you're buying a company with field staff, dispatch, customer retention pressure, and vendor management complexity, your resume should show that you've handled something operationally similar.

Lenders also review personal history closely. That includes your credit profile, liquidity, outside obligations, and how you explain rough spots if they exist. First-time buyers often assume a decent credit score is enough. It isn't. Underwriters want to know whether you've made hard decisions, led people, and managed through uncertainty.

A useful self-test is simple:

- Resume fit: Can your background explain why you can lead this company on day one?

- Financial fit: Do your personal finances show stability and reasonable capacity to contribute?

- Character fit: Are there unresolved issues that create avoidable lender concern?

The business must support the debt

The target business has to produce reliable cash flow, not just interesting topline revenue. Underwriters care about earnings quality, customer concentration, seasonality, margins, and whether the seller has been running expenses through the business that need to be normalized correctly.

They also care about transfer risk. Some businesses depend too heavily on the owner's personal relationships, licenses, or presence. If revenue walks out when the seller leaves, the lender will see it.

A business isn't financeable because it did well under the seller. It's financeable because the lender believes it can keep doing well after the handoff.

The deal itself must be SBA-compliant

Eligibility problems often hide in the structure, not the business. The entity has to be for-profit, operating in the United States, and small enough to fit SBA standards. Ownership, guaranties, seller involvement, lease rights, and use of proceeds all have to align with SBA rules and lender policy.

That's why LOI language matters earlier than many buyers think. If the LOI promises a structure that later conflicts with the lender's required documentation, you create re-trade risk before underwriting is even finished.

A fundable acquisition usually has these traits:

| Area | What lenders like to see |

|---|---|

| Buyer | Relevant management background and a clean narrative |

| Business | Stable historical performance and understandable cash flow |

| Structure | Clear ownership transfer and clean documentation |

| Seller | Responsive, organized, and realistic about post-close involvement |

Creative Deal Structures That Get Funded

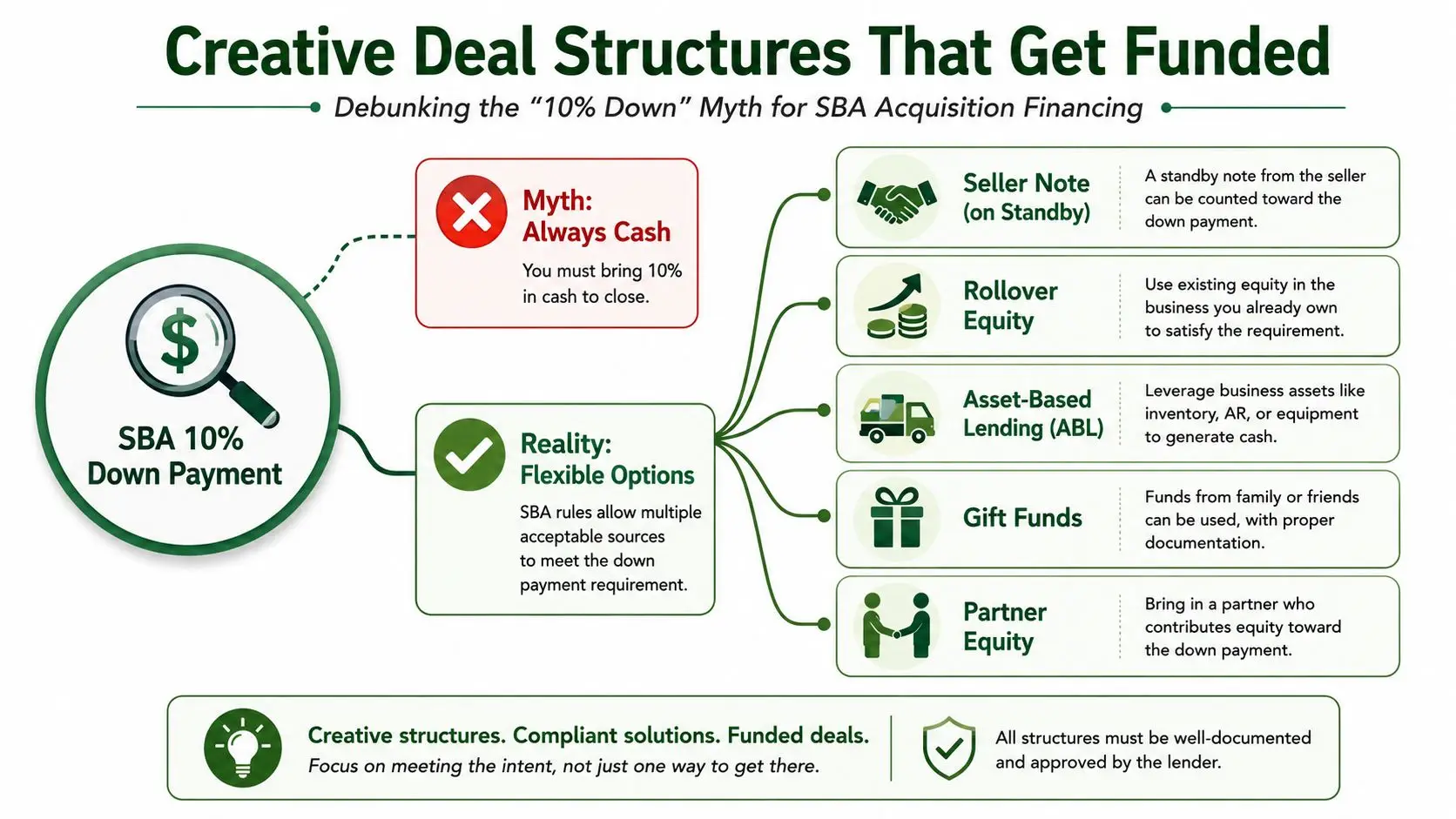

What the down payment really means

Most buyers hear some version of “SBA lets you buy a business with 10% down,” then assume that means one simple cashier's check at closing. Real deals are rarely that neat.

The better way to think about the equity injection is this: the lender wants a credible capital base beneath the senior debt. Sometimes that comes mostly from buyer cash. Sometimes it includes a compliant seller note, outside equity, or another approved source. What matters is whether the structure fits SBA rules and still leaves the business healthy after closing.

The key nuance is in the seller paper. Buyers can often finance up to 90% of the purchase price, but a seller note only counts toward the required injection under specific conditions. It generally cannot exceed 5% of the purchase price and must be on full standby for the entire term of the SBA loan, as explained in this SBA acquisition financing breakdown.

That rule changes the conversation. A seller note is not a magic workaround. It is a tightly structured tool.

Seller notes, investors, and stack design

The most common workable structures look like this:

Buyer cash plus standby seller note

This is the classic lower-cash structure. It can work well when the seller believes in the business and is willing to defer payments for the full SBA loan term.Buyer cash plus investor equity

This works when the ownership and guaranty structure are set up correctly and the investor group is documented clearly. It often helps buyers with strong operating ability but limited personal liquidity.Buyer cash plus separate seller paper that does not count toward injection

This can help bridge valuation gaps, but it must be distinguished from any note used to satisfy the required equity contribution.Pari passu or side-by-side structures in specialized deals

These are more advanced and lender-specific. They can be useful when a transaction includes asset-backed support or additional capital needs outside the core SBA facility.

For a deeper look at standby seller paper, see this guide to seller financing for business acquisition.

The smartest structures don't minimize cash at all costs. They preserve enough liquidity so the buyer can survive the first ugly quarter after closing.

A strong capital stack also respects post-close reality. If the business needs working capital, deferred maintenance, key employee retention, or a short seller transition, then stretching the debt financing to its limit can backfire even if the deal technically qualifies.

What usually does not work

First-time buyers often lose momentum. They rely on internet shorthand instead of lender logic.

Common mistakes include:

Treating any seller note as injection

If the note terms don't satisfy standby requirements, the lender won't give it equity credit.Using investor money without clear ownership documentation

If capital is coming from partners, the lender needs to understand exactly who owns what and who controls operations.Ignoring goodwill concentration

Goodwill-heavy deals can still get funded, but they require a stronger narrative around cash flow durability and transition.Draining personal liquidity to make the down payment

A buyer who closes with no cushion may look weaker, not stronger.

The best structures balance compliance, lender comfort, and operating reality. If one of those is missing, the deal may still get approved, but it becomes much harder to keep together.

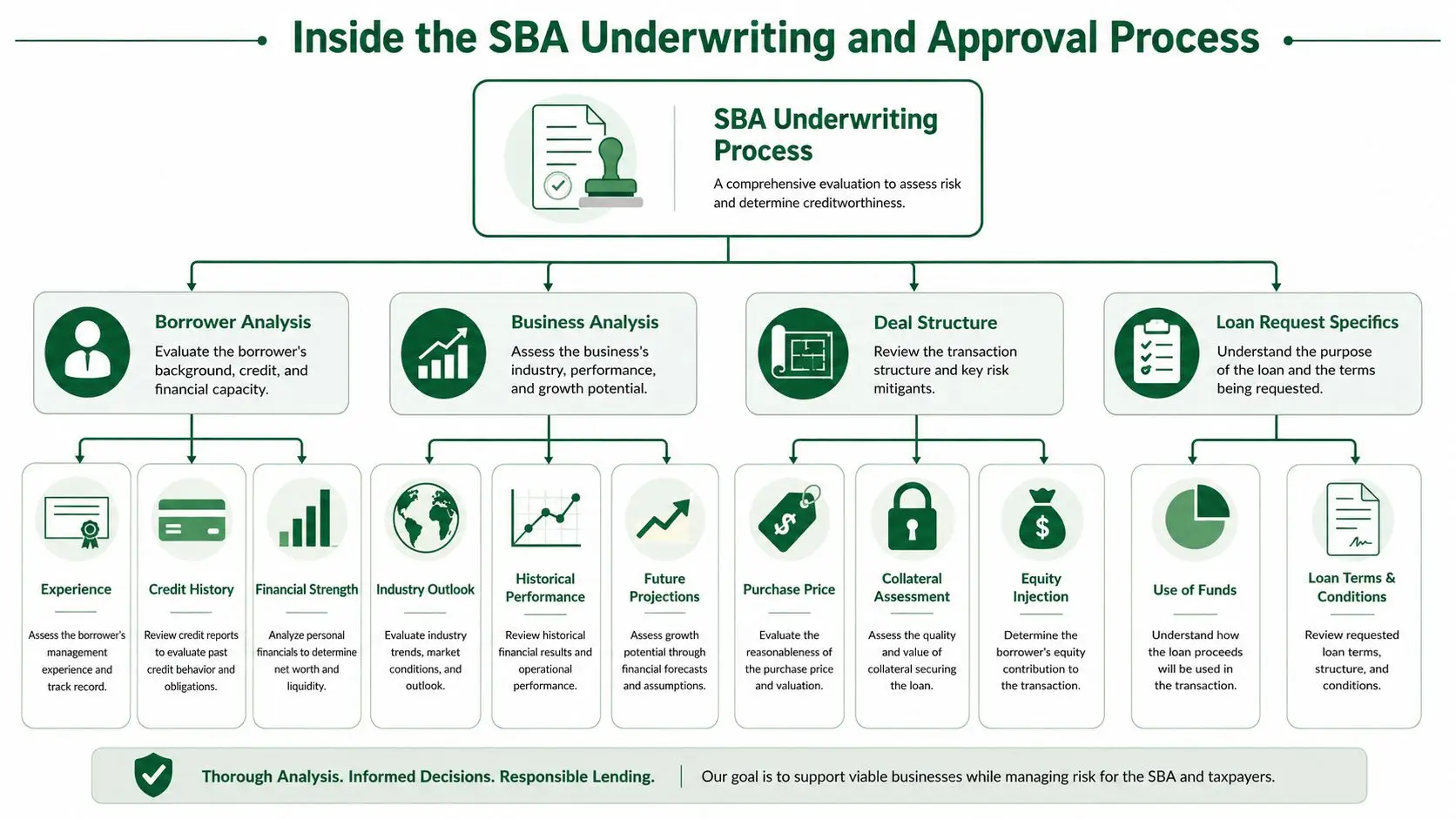

Inside the SBA Underwriting and Approval Process

Once the lender has a live file, underwriting stops being theoretical. Every weak assumption gets tested. Every missing document becomes visible. Every inconsistency between the LOI, financials, and buyer narrative turns into a question.

How lenders apply the five Cs in acquisitions

The old Five Cs of Credit still frame the process, but acquisitions have their own version of each one.

| Credit factor | How it shows up in an acquisition |

|---|---|

| Character | Your background, explanation of the deal, and how you handle scrutiny |

| Capacity | Whether business cash flow can support the new debt burden |

| Capital | Your injection, liquidity, and financial resilience after closing |

| Collateral | Available business and personal collateral, even in goodwill-heavy deals |

| Conditions | Industry risk, transition risk, lease terms, and deal-specific issues |

Character is bigger than credit history. Underwriters look at how realistic you are. If your projections assume smooth growth, no customer loss, no hiring issues, and instant owner transition, the file feels weak even if the spreadsheet looks polished.

Capacity is the center of the file. Historical earnings usually carry more weight than projections. Projections still matter, but mainly as a test of your judgment. If they're too aggressive, they hurt you.

Capital is where many buyers make a strategic error. They focus on getting to minimum injection and forget that lenders also care what remains after funding. A buyer with reserves often looks safer than one who empties personal accounts to win approval.

What approval actually depends on

Underwriting is partly analysis and partly risk narrative. The file gets stronger when the lender can explain, in plain language, why this borrower should succeed with this business under this structure.

What helps most:

- Clean recast financials that explain owner add-backs clearly

- A buyer resume that matches the operating demands of the target

- A sensible transition plan for customers, staff, and vendors

- A coherent use-of-funds schedule that ties exactly to the purchase and closing structure

- Fast response time when the lender asks follow-up questions

Underwriters don't expect perfection. They expect consistency.

There is also a practical difference between lenders. Some have stronger acquisition teams, faster internal process, and more comfort with nuanced structures. Preferred lenders can often move more efficiently because they handle much of the approval process internally, but speed still depends on file quality.

The files that stall are usually not the most complex. They're the most inconsistent.

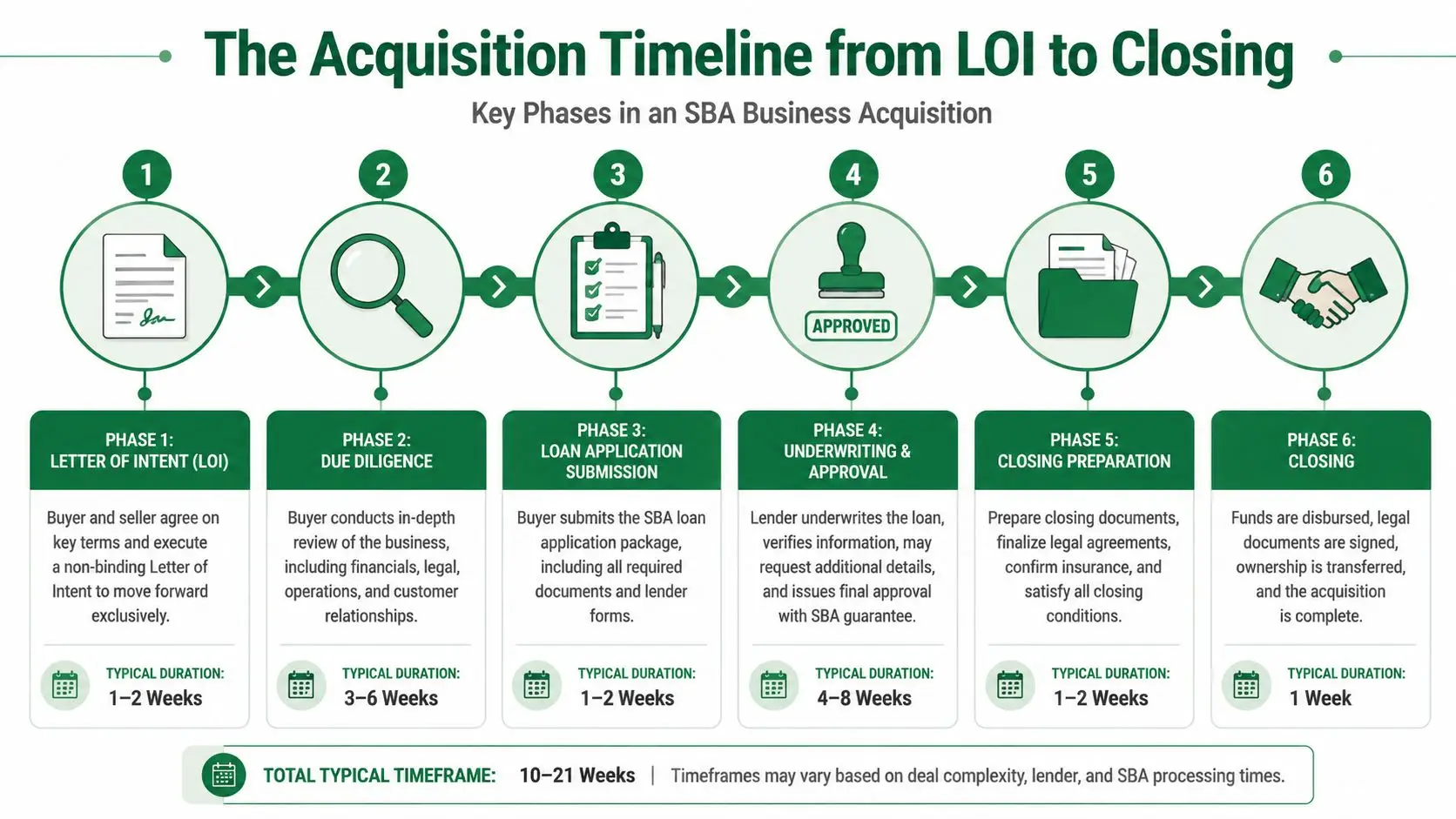

The Acquisition Timeline from LOI to Closing

The clock starts when the LOI is signed, not when the lender issues a term sheet. That's why experienced buyers treat the acquisition like a project plan from day one.

A useful companion is this step-by-step SBA acquisition timeline guide.

Phase-by-phase from signed LOI to funding

In a well-managed process, the first phase is document collection and diligence setup. The buyer requests tax returns, interim financials, debt details, payroll reports, lease documents, organizational records, and anything else needed to build the file. At the same time, the lender begins sizing the request and pressure-testing the structure.

Then lender diligence and underwriting begin to run in parallel with business diligence. That parallel motion matters. If you wait to finish one before starting the other, you lose precious time and often your seller's patience.

A typical flow looks like this:

LOI signed

The basic economics, exclusivity, and financing path are set.Packaging begins

Buyer and seller documents are collected and organized for lender review.Term sheet and underwriting entry

The lender confirms structure, then starts formal review.Third-party reports ordered

Valuation, appraisal if needed, and other required reports move onto the critical path.Closing prep

Final conditions, legal documents, insurance, lease assignments, and entity paperwork get tied down.Funding day

Loan documents are signed and proceeds are disbursed through the closing process.

Here's a useful walk-through of the process in video form:

Where timelines usually slip

The biggest delays usually come from third parties, not the lender's first review. Sellers sit on document requests. Landlords delay lease consent. Valuation providers ask for missing materials. Attorneys revise purchase agreement language after underwriting has already approved a different structure.

That's why good buyers push these items early:

- Lease review early if the location matters to the business

- Seller responsiveness early because document delays tend to compound

- Valuation coordination early so nobody discovers missing records late

- Entity and ownership planning early if investors or partners are involved

If the seller says, “We can get that later,” assume it belongs on the critical path now.

Deals close fastest when diligence, underwriting, and legal drafting move together, not in sequence.

Your SBA Loan Application Checklist

A complete file tells the lender you're organized and serious. A sloppy file tells the lender your post-close management may be sloppy too. That isn't fair, but it's real.

Buyer documents

Start with the documents that establish who you are financially and operationally.

Personal financial statement

This shows liquidity, liabilities, and where your injection is coming from.Resume or executive bio

This is not a formality. It is your operating case for why you can run the company.Personal tax returns

Lenders use these to verify income patterns and identify outside obligations.Government ID and background forms

These support eligibility and compliance review.

If you have partners, collect the same package for each required principal early. Multi-owner delays are common because one person is always slower than the rest.

Seller and business documents

This set is usually the heaviest and the most likely to arrive incomplete.

- Business tax returns

- Year-to-date profit and loss statements

- Balance sheets

- Debt schedule

- Payroll summary

- Customer concentration information

- Equipment or asset lists

- Lease documents

- Organizational and licensing records

Ask for native files where possible, not just PDFs. Underwriters and valuation providers often need to trace details, and that goes faster when financials are easier to work with.

Deal documents

The structure lives here. If these documents drift out of sync with lender expectations, the deal gets messy fast.

| Document | Why it matters |

|---|---|

| Signed LOI | Establishes headline terms and exclusivity |

| Purchase agreement draft | Must align with lender-required structure |

| Use of funds | Shows exactly where proceeds go |

| Lease assignment or real estate contract | Critical when location is tied to business continuity |

| Seller note terms | Must match the intended underwriting treatment |

| Entity documents for buyer | Confirm ownership and signing authority |

A good checklist doesn't just gather paperwork. It prevents contradictions.

Avoiding Common SBA Deal Killer Pitfalls

Most failed SBA acquisition deals don't die because the buyer was unqualified. They die because one issue sat ignored until it became impossible to solve quickly.

Problems that show up late and kill momentum

One common problem is the seller who is friendly but slow. They agree to the sale, then drag their feet on tax returns, payroll records, debt payoffs, or lease details. Underwriting can't move cleanly without that information. Delay creates doubt, and doubt changes how lenders view the file.

Another problem is the valuation that doesn't support the agreed price. If the number comes in light, the capital stack may have to change. That can mean more buyer cash, more seller concession, or a renegotiation nobody wants to have late in the process.

You also see deals wobble when the landlord won't cooperate, or when diligence uncovers liabilities the buyer didn't model. Sometimes the issue is subtler. The purchase agreement says one thing, the lender approved another, and the attorneys have to reopen economics just to match the structure.

How experienced buyers protect the deal early

The best defense is front-loaded discipline.

Build financing contingencies into the purchase process

Don't assume the lender will solve structural problems after the fact.Engage the landlord and key counterparties early

If the lease, franchise approval, or license transfer matters, start those conversations before underwriting is deep.Get specific on seller transition

If the business depends on the owner's relationships, document how the handoff works.Pressure-test the price before you fall in love with it

A high asking price isn't a problem. An unsupported one is.Keep the structure simple unless complexity has a purpose

Every extra note, investor, reimbursement, or side agreement creates another chance for conflict.

Buyers often focus on whether the bank will say yes. The sharper question is whether the entire transaction can stay coherent under pressure.

The safest mindset is to assume the file will be examined by someone who knows nothing about the deal and trusts none of the assumptions. If your documents still make sense under that standard, you're in good shape.

If you're buying a business and want expert help structuring the financing before underwriting gets messy, GoSBA Loans can help you compare lenders, shape a compliant capital stack, and move from LOI to closing with fewer surprises.