You've found a building that fits your business. The location works. The layout works. The price looks reasonable. Then the financing questions start, and many first-time buyers often get stuck at this point.

Commercial real estate loan requirements aren't just a bigger version of residential mortgage rules. Lenders underwrite the borrower, the business, the property, and the deal structure at the same time. If you're using SBA financing, the rules get more specific. That's good news if you understand them early, and expensive news if you don't.

The SBA SOP is the main source of truth for owner-occupied commercial real estate financing. It tells you what underwriters need to see, why some deals sail through, and why others stall over issues that buyers never saw coming. One example is loan assumptions and transfer restrictions after closing. If you're buying a property from a seller with existing debt, or you're planning future ownership changes, it helps to spend a few minutes understanding alienation clauses before you commit.

A good loan file tells a simple story. The business is stable, the cash flow is credible, the property fits program rules, and the borrower has enough equity and experience to operate the asset responsibly. That's what lenders are trying to prove.

Table of Contents

- Navigating Your Commercial Real Estate Loan

- Borrower and Business Qualifications

- Evaluating the Asset Property Eligibility Rules

- Decoding the Numbers Key Underwriting Metrics

- Comparing Loan Programs Bank vs SBA vs CMBS

- Your Commercial Loan Application Checklist

- How to Strengthen Your Loan Application

Navigating Your Commercial Real Estate Loan

The first-time buyer usually assumes the bank is mostly lending against the building. That's only part of the story. In commercial lending, the property matters, but the lender also wants proof that the operating business can support the debt and that the ownership group can execute the plan.

That's why the process feels more layered than people expect. You're not just applying for a loan. You're presenting a full operating case that includes business history, current financials, ownership structure, property use, third-party reports, and a repayment narrative that has to hold up under scrutiny.

A clean deal doesn't mean a simple deal. It means the borrower answered the underwriter's questions before the underwriter had to ask them.

For owner-users, SBA financing often becomes the most practical path because it was built for businesses buying space for their own operations. But SBA loans aren't casual money. The SOP drives eligibility, occupancy, guaranty, appraisal, and underwriting standards, and lenders follow those rules closely.

What lenders care about before they issue a term sheet

Most credit decisions come down to four questions:

- Can the business repay the loan: Lenders want stable operating income, not optimistic assumptions.

- Does the property fit the loan program: A good building can still be the wrong SBA asset.

- Is the borrower organized: Missing entity documents, stale tax returns, and vague ownership charts create avoidable delays.

- Does the deal structure make sense: Seller notes, lease rollovers, and planned tenant changes all affect approval.

Why first-time buyers get tripped up

A buyer often focuses on rate and down payment too early. Underwriters focus on fit. If the business has weak documentation, if the property fails occupancy rules, or if the value doesn't support the structure, the loan won't get better because the quoted rate looked attractive.

The practical way through is to build the file in the same order a lender will review it. Start with borrower eligibility. Then test the property. Then run the core ratios. Then choose the program.

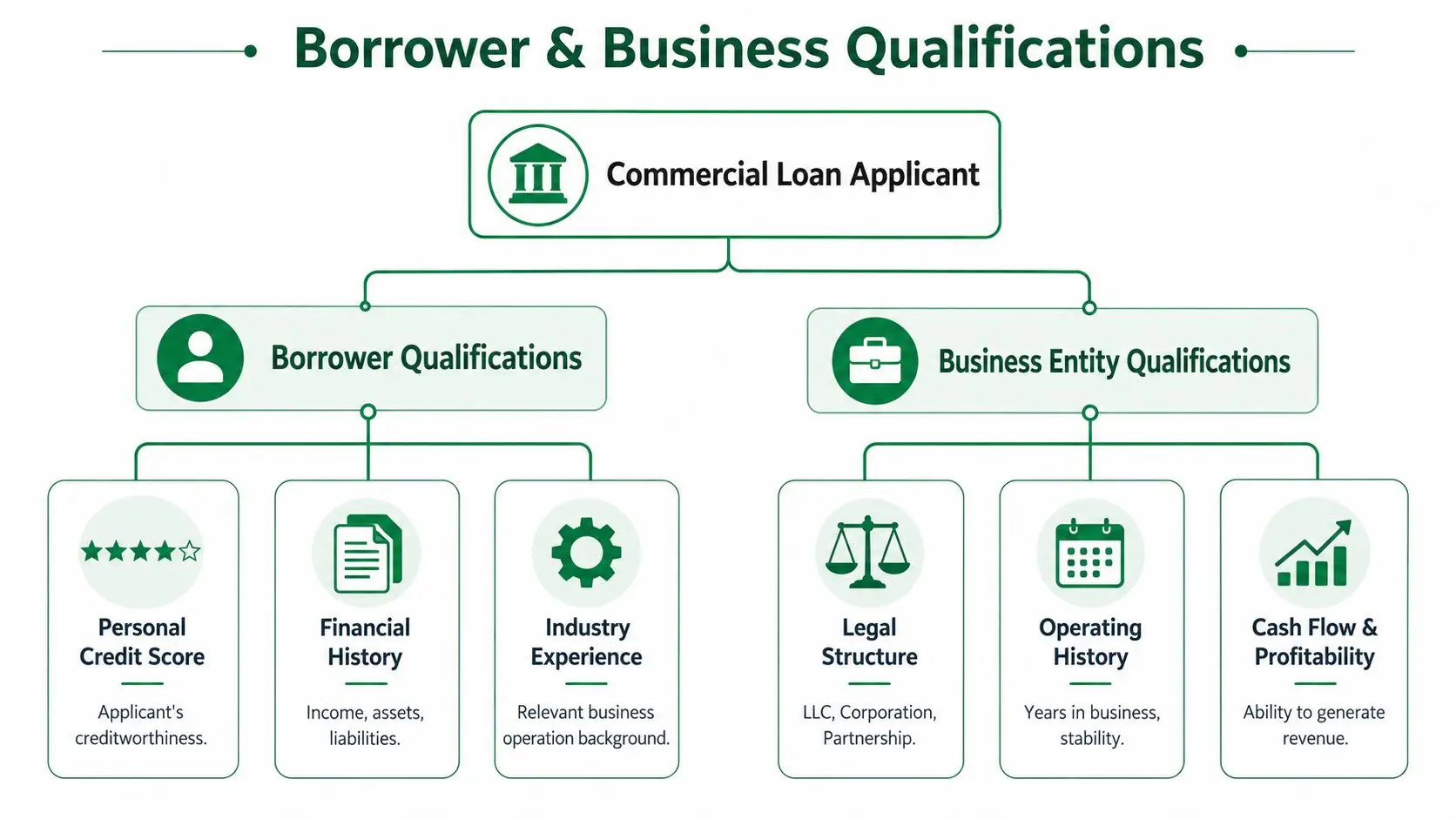

Borrower and Business Qualifications

Before a lender gets comfortable with the property, it underwrites the people and business behind the request, which makes commercial real estate loan requirements more personal than many buyers expect.

What lenders review first

The fastest way to understand borrower qualification is to think in three buckets: credit, cash flow, and experience.

Credit isn't just a score. Underwriters look at repayment history, existing obligations, liquidity, bankruptcies if any, and whether the ownership group behaves like people who can handle long-term debt. Business credit matters too, especially when the operating company already has borrowing history.

Cash flow is usually the heavier factor. According to Bank of America's commercial real estate loan guidance, most institutional lenders require a minimum of two years of business operation under existing ownership and a minimum annual revenue of $250,000. That same guidance notes lenders prefer net income that exceeds the debt carried by at least 20%.

Experience matters more than many borrowers think. A dentist buying a dental office, a contractor buying a yard and warehouse, and a physician buying a medical condo all make intuitive sense to lenders. A borrower entering an unfamiliar property or operating model has a steeper hill to climb.

How underwriters think about risk

Underwriters don't ask whether your business is promising. They ask whether it's predictable.

Here's what helps:

- Stable ownership: If the business has been under the same ownership long enough to show operating consistency, the file feels stronger.

- Clear legal entity structure: Lenders want the borrower entity and operating entity documented correctly. SBA files usually work better when the ownership chart is simple and the title-holding entity is clean.

- Financial statements that reconcile: If tax returns, profit and loss statements, and balance sheets tell conflicting stories, the deal slows down fast.

What hurts:

- Recent volatility: Sharp swings in revenue or margin without a clear explanation.

- Messy intercompany activity: Unexplained transfers between owners, affiliates, and the business.

- Unclear guarantor strength: If the key owners can't show personal financial support, the lender starts adding conditions.

Practical rule: If an underwriter has to guess how your business makes money, the file isn't ready.

A first-time buyer should also understand that “fundable” and “approved” are different. A borrower may meet baseline standards and still lose the deal if the lender sees weak management depth, unsupported projections, or unresolved tax or title issues. Strong files don't just satisfy minimum requirements. They remove doubt.

Evaluating the Asset Property Eligibility Rules

A property can be attractive on paper and still fail an SBA eligibility review. This happens all the time with mixed-use assets, partial occupancy plans, and buildings that generate too much third-party rent relative to the buyer's intended use.

Owner-occupied is the dividing line

For most SBA owner-user real estate financing, the central question is simple. Will the business occupy enough of the property to qualify as owner-occupied?

That sounds easy until the building has multiple suites, inherited leases, shared common areas, or a layout that doesn't line up neatly with the business's current footprint. Buyers often assume future plans are enough. Lenders usually want a credible occupancy story tied to the actual square footage and operating use.

When valuation enters the conversation, the quality of the appraisal framework matters too. If you're trying to understand how professional valuation logic is documented in another mature market, this overview of RICS property valuations in London is a useful reference point for how formal property reporting supports lending decisions.

If you're specifically exploring owner-user financing structures, this guide to owner-occupied commercial real estate loans is a practical next read.

The mixed-use problem most guides skip

The standard advice says SBA 504 requires 51% owner-occupancy. That's true, but it doesn't solve the practical problem. A lot of first-time buyers target properties with existing tenants because the rent helps support the deal. Then they discover the physical occupancy test is tighter than they expected.

A critical nuance for multi-use properties is the Income-Occupancy Trap. While SBA 504 loans require 51% owner-occupancy, lenders can struggle when a business acquires a mixed-use asset and cannot physically occupy that share of the total square footage. A 2024 OCC report noted that 30% of loan workouts stem from occupancy misalignment in mixed-use assets, which is why deal structure matters so much in these files.

What works in practice is early analysis of three issues:

- Physical occupancy: How much space the business will use at closing.

- Lease friction: Whether legacy tenant leases block compliance.

- Financial control: Whether the business controls the economics of the asset in a way that supports the requested structure.

Mixed-use deals fail less often because the building is bad and more often because the buyer noticed the occupancy issue too late.

This is one of the biggest gaps in generic articles about commercial real estate loan requirements. They treat occupancy as a checkbox. Underwriters treat it as a transaction design issue.

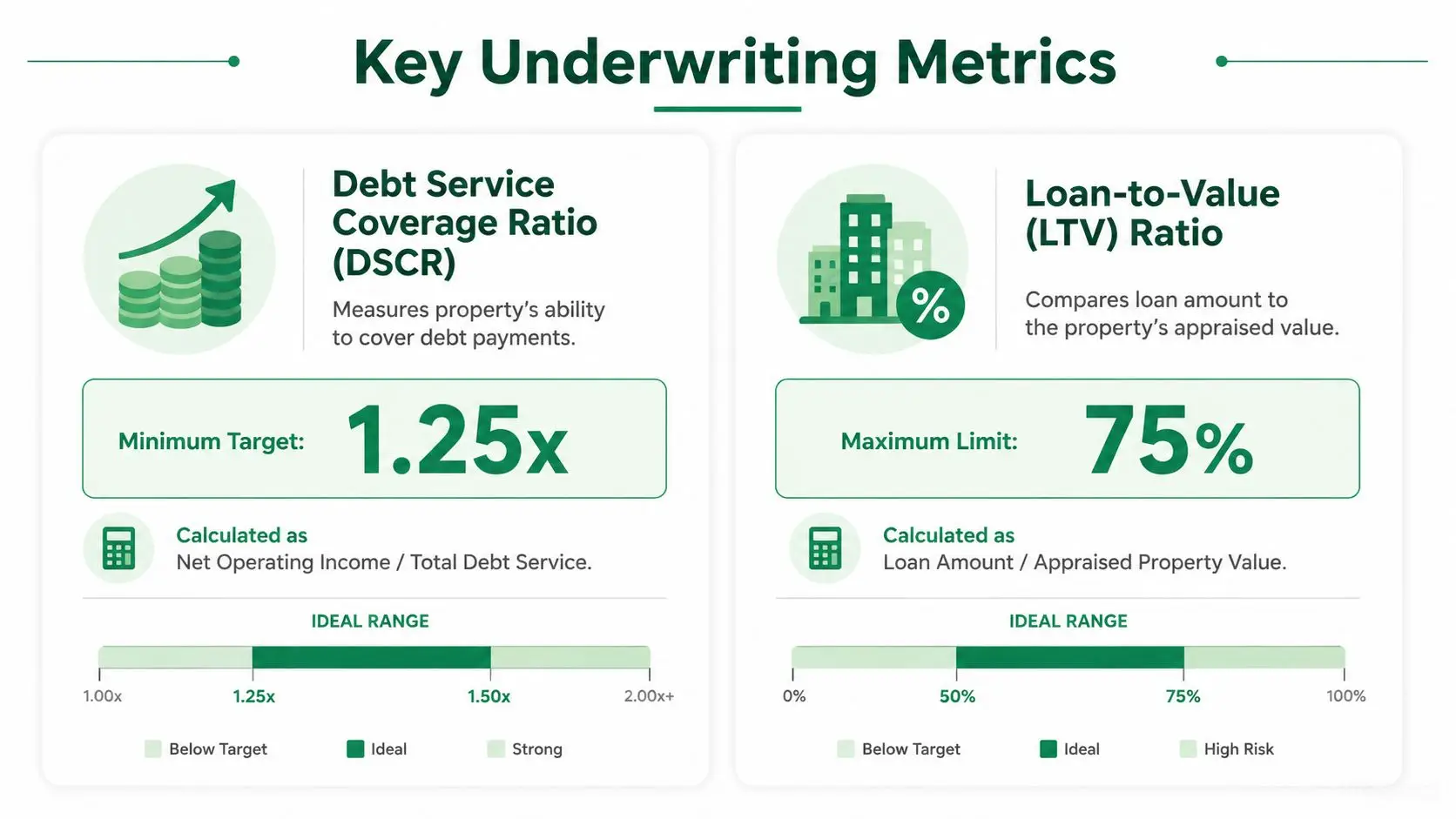

Decoding the Numbers Key Underwriting Metrics

Every commercial loan file eventually comes down to numbers. Two metrics drive most of the decision: Debt Service Coverage Ratio (DSCR) and Loan-to-Value (LTV).

Early in underwriting, I tell buyers to treat DSCR like the property's shock absorber. It shows whether the building's income can absorb debt payments without collapsing when something goes wrong. LTV answers a different question. How much of the property value is the lender willing to finance?

DSCR is the propertys shock absorber

According to the OCC's commercial real estate lending handbook, a foundational requirement is a DSCR typically between 1.1 and 1.4, which means the property's net operating income is 10% to 40% higher than annual debt service. In practice, many institutional lenders target the middle of that band or stronger.

A separate underwriting benchmark used by many institutional lenders places the minimum between 1.25x and 1.35x, meaning the property produces 25% to 35% more NOI than annual debt service. That's why a file with only a thin cushion tends to draw more scrutiny.

This is the basic formula:

| Metric | Formula | What it tells the lender |

|---|---|---|

| DSCR | NOI ÷ annual debt service | Whether property income can support the loan |

Underwriters usually calculate NOI conservatively. They want recurring income and supportable expenses, not aggressive add-backs.

A buyer trying to model this properly should understand the difference between optimistic projections and lender-grade projections. For that reason, a detailed real estate investment guide for service businesses can help frame how to build assumptions lenders will respect.

Later in the process, many buyers benefit from seeing a straightforward lending walkthrough:

LTV determines how much cash you need

The same OCC guidance says the LTV ratio is commonly capped at 80% for commercial properties and 75% for land development. Separate commercial underwriting standards often come in lower, with traditional institutional lenders typically setting maximum LTV in the 65% to 75% range for many deals.

That's the lender's equity cushion. It protects the bank if value declines and it forces the borrower to have real capital in the transaction.

| Metric | Formula | What it tells the lender |

|---|---|---|

| LTV | Loan amount ÷ appraised value | How much leverage the lender will allow |

If your appraisal comes in light, your down payment problem gets bigger immediately. That's why experienced borrowers don't just ask whether they can qualify. They ask whether the value, occupancy, and cash flow all support the same structure at once.

Comparing Loan Programs Bank vs SBA vs CMBS

The right program depends on who you are, what property you're buying, and how the business will use it. Buyers often compare rates first. Underwriters compare fit first.

Where conventional banks fit

Conventional bank loans work well when the borrower is strong, the down payment is available, and the property is easy to underwrite. Banks usually like experienced operators, clean tax returns, and straightforward owner-user assets. If your business is established and you don't need program flexibility, a bank loan can be efficient.

The trade-off is that banks can be less forgiving when the file is tight. A buyer with uneven cash flow, a more complex structure, or a mixed-use property may find that conventional credit boxes close quickly.

Why SBA often wins for owner-users

SBA loans are built for small business borrowers, especially owner-occupants. The SBA 7(a) program has clear operating and underwriting standards that matter in real transactions. Under the SBA 7(a) program, the SOP requires borrowers to demonstrate a DSCR of at least 1.15x, and the business must have been in operation for at least two years under current ownership, with limited exceptions for acquisitions of existing operating entities with proven cash flow history.

That combination makes SBA financing unusually useful for buyers who have a solid business but don't fit the strictest conventional bank profile. It also explains why buyers should review SBA-specific guidance instead of relying on generic CRE articles. This overview of SBA real estate loans using 7(a) and 504 financing helps frame where each SBA option fits.

Here's the practical comparison:

| Requirement | Conventional Bank Loan | SBA 7(a) Loan | SBA 504 Loan | CMBS Loan |

|---|---|---|---|---|

| Best fit | Strong borrower, straightforward owner-user or investment deal | Small business owner buying owner-occupied property | Owner-user buying fixed assets with long-term occupancy intent | Larger stabilized income property |

| Cash flow standard | Lender-specific, often conservative | SBA SOP minimum applies | Program-specific with lender and CDC review | Property cash flow drives the structure |

| Down payment pressure | Often higher equity expectation | Can be more flexible for qualified borrowers | Often attractive for owner-users seeking lower cash injection | Depends heavily on asset strength |

| Documentation burden | Moderate to high | High, because SBA compliance matters | High, with additional program layers | High, with property and servicing complexity |

| Ideal borrower | Established business with strong balance sheet | Small business needing structure flexibility | Business planning to occupy and hold long term | Borrower focused on stabilized cash flow and execution |

When CMBS belongs in the conversation

CMBS is usually not the first stop for a first-time owner-user. It's more common for stabilized income-producing assets where property cash flow, servicing structure, and securitized loan terms are a fit. Borrowers should go in knowing that CMBS can be less flexible after closing. If your business needs adaptability, local bank or SBA execution is often a better match.

The best loan program isn't the one with the flashiest headline term. It's the one your deal can actually close under.

Your Commercial Loan Application Checklist

A strong application package reduces friction. It shows the lender that the borrower is serious, organized, and capable of getting through closing without surprises.

Personal and ownership documents

Start with the ownership side of the file. Under the SBA SOP, borrowers must provide personal guarantees from all owners with 20% or more equity interest in the business, and the property must be appraised by an SBA-approved third-party appraiser whose valuation supports the loan amount, as outlined in this summary of commercial loan requirements tied to the SBA SOP.

That requirement shapes the checklist.

- Personal financial statements: Lenders use these to assess liquidity, debt levels, and contingent support.

- Personal tax returns: These help verify income patterns and expose undisclosed liabilities or side ventures.

- Ownership breakdown: The lender needs a clean list of who owns what, both in the operating company and any real estate holding entity.

Business and property file items

The business file has to reconcile with the ownership file and the property file. If one doesn't match the others, underwriting slows down.

Gather these early:

- Business tax returns and financial statements: Include historical P&Ls and balance sheets that tie out to tax filings.

- Entity documents: Formation documents, operating agreements, bylaws, and certificates of good standing if applicable.

- Purchase contract or LOI: The lender needs the economic terms of the transaction.

- Property operating information: Rent roll, leases, and income or expense detail where relevant.

- Third-party reports: Appraisal, environmental reports, and any inspection materials required by the lender.

A first-time buyer should also budget attention for closing mechanics, not just approval. The fee side often catches borrowers off guard, so reviewing SBA loan closing costs and fee breakdowns before commitment helps avoid last-minute confusion.

Underwriting advice: Turn in complete document sets, not fragments. Partial submissions make a lender re-underwrite the file multiple times.

The checklist itself isn't complicated. The challenge is consistency. Dates, ownership percentages, legal names, lease terms, and financial figures all need to line up across every document in the package.

How to Strengthen Your Loan Application

A file that barely qualifies is not the same as a file that gets approved cleanly. Underwriters respond best when the story is simple, documented, and resilient under stress.

What actually moves an underwriter

Three upgrades make a noticeable difference.

First, tighten your projections. If you're presenting future performance, tie it to current operations, signed leases, or obvious capacity changes. Unsupported growth stories don't help.

Second, clean up ownership and entity structure before application. If title will sit in one LLC and operations will sit in another, document that relationship clearly from the start.

Third, show operating discipline. Clear financial statements, stable deposits, documented rent or occupancy assumptions, and an organized explanation of the use of proceeds all reduce perceived risk.

The DSCR and credit score trade-off

This is the nuance many generic guides miss. For SBA 7(a) loans on owner-occupied commercial real estate, a weighted model is often used where strong DSCR above 1.3x can partially offset lower personal credit scores down to 620, provided the business shows consistent NOI growth. A 2025 NerdWallet analysis of 1,200 SBA CRE loans found that 22% of approved deals had personal credit scores below 670, and all of those approvals were tied to DSCR above 1.35 and 3-year NOI growth above 15%.

That doesn't mean credit stops mattering. It means a borrower with borderline personal credit shouldn't automatically disqualify themselves if the business cash flow is strong and well documented.

If you're in that category, the practical move is to lead with the business case. Show durable NOI, explain property logic, and document the operating trend cleanly. Many borrowers lose before underwriting starts because they assume one weak point kills the deal. Often it doesn't. A weak file gets declined. A balanced file gets reviewed.

If you're buying a building for your business and want expert help sorting through lender fit, SBA eligibility, deal structure, and closing execution, GoSBA Loans is a practical place to start. They help entrepreneurs compare SBA options, organize fundable loan packages, and facilitate the process from term sheet through closing without charging the borrower a fee.