A well-structured SBA loan for business expansion can fund growth with far less cash in than many owners expect. The best example is the 0% down expansion path available in the right file. It usually depends on whether the new location or operation is a true continuation of the business you already run, not a new concept dressed up as one.

That distinction matters more than rate shopping. I see owners lose good deals because they focus on headline terms before they confirm whether the expansion matches the same NAICS code, ownership, and operating model lenders want to see. If those pieces line up, the financing conversation changes fast.

Expansion also goes beyond buying a building or adding equipment. A second location often needs hiring, reporting, scheduling, and systems that can handle more volume without adding back-office drag. Many borrowers pair financing with operational improvements such as unlocking business growth with cloud so the new capacity performs from day one.

If you are weighing locations, working capital, partner buy-in, or real estate, this guide to business expansion financing options will help you frame the deal the way lenders do.

Table of Contents

- Fueling Your Growth with an SBA Expansion Loan

- Choosing Your Path SBA 7(a) vs 504 Loans

- The 0% Down Expansion A Game Changer for Growth

- Underwriting Demystified What Lenders Really Look For

- Your SBA Expansion Loan Application Timeline

- Common Pitfalls and How a Broker Streamlines the Process

- Real World Expansion Financing Scenarios

- Frequently Asked Questions About Expansion Financing

Fueling Your Growth with an SBA Expansion Loan

Expansion financing can either protect your cash or drain it before the new location, equipment, or team has time to produce. The difference usually comes down to structure, not just approval.

I see owners focus on rate first and use of proceeds second. That is backwards. A strong SBA expansion loan gives the business enough room to execute the plan, cover the predictable overruns, and avoid starving operations right after closing. If you want a broader view of how these projects are typically structured, this guide to business expansion financing options lays out the main paths.

The practical advantage with SBA financing is flexibility. It can support growth projects that do not fit neatly into one box, especially when expansion includes a mix of buildout, equipment, working capital, and hiring. That matters because real expansion rarely shows up as a single clean invoice.

The best opportunities often come from businesses staying inside the work they already know. If the expansion keeps you in the same NAICS code, the financing conversation can change materially. That detail gets missed in generic advice, but it often determines whether a borrower has to bring a large equity injection or can qualify for a much lighter cash-in structure.

What strong expansion financing really does

Good expansion debt should do four jobs at the same time:

- Preserve operating cash: New locations and added capacity almost always cost more, and take longer, than the first projection suggests.

- Fit the actual project: Inventory, tenant improvements, equipment, and payroll should be financed with a structure that matches how the money will be used.

- Reduce avoidable strain on the owner: Excessive conditions, weak documentation, or the wrong lender can turn a workable deal into a time sink.

- Leave margin for a slow ramp: Expansion rarely hits full speed on day one.

Practical rule: If the loan covers the project cost but leaves the business tight on payroll, inventory, or launch expenses, the deal was not built correctly.

There is also an operating side to expansion that lenders notice. A second unit in the same line of business is different from trying to add an unfamiliar revenue stream. One is usually an extension of a proven model. The other often looks like a partial startup inside an existing company. That distinction affects risk, structure, and how much cash the lender expects the borrower to keep available after closing.

The same logic applies outside finance. Teams that scale well usually add systems before they add complexity, whether that means better reporting, tighter inventory controls, or unlocking business growth with cloud for multi-location operations. Growth works better when the capital plan and the operating plan match.

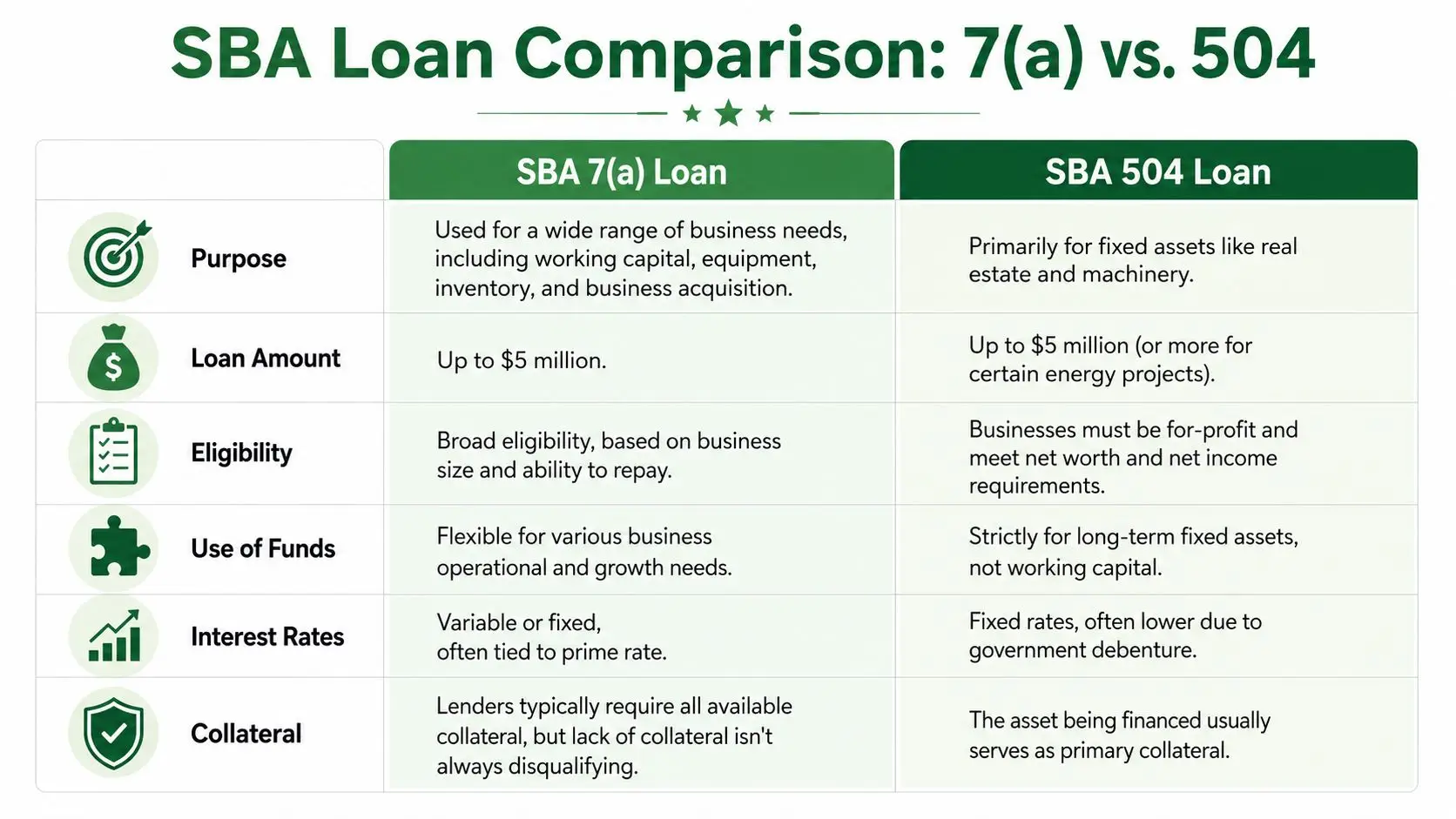

Choosing Your Path SBA 7(a) vs 504 Loans

Picking between SBA 7(a) and 504 is not a paperwork decision. It changes how much cash you keep, what the funds can cover, and whether the deal still works after closing.

A 7(a) loan gives an owner more room to build a real expansion budget. It can cover working capital, inventory, equipment, leasehold improvements, hiring, and in many cases an acquisition tied to growth. That flexibility is why I start many expansion conversations with the 7(a) program, especially when the project includes both hard costs and operating needs. If you need a current breakdown of eligibility, structure, and common lender expectations, this 2026 SBA 7(a) loan guide is a solid reference.

A 504 loan is more targeted. It is built for owner-occupied real estate and long-life equipment. If the project is primarily a building purchase, ground-up construction, or a major equipment buy, 504 often produces a cleaner capital stack and a longer-term fit for the asset.

That distinction matters in underwriting. A lender will usually look at a mixed expansion project and ask a simple question: is this primarily an operating expansion, or primarily a fixed-asset purchase? The wrong answer can force the file into avoidable friction.

Here is where borrowers often get sideways:

- Trying to use 504 for short-term operating needs. 504 is not designed for payroll cushion, inventory buildup, or launch marketing.

- Using 7(a) by default for a real estate-heavy project. That can be fine, but it should be a conscious choice after comparing it to 504.

- Ignoring ownership and entity structure issues until the bank asks. Lenders want a clean borrowing entity, clear affiliates, and a documented ownership story. If that piece is still being sorted out, Allied Tax business formation advice is a useful primer.

- Treating equity injection as if every SBA expansion works the same way. It does not. Some projects require cash in. Some 7(a) expansions, if they stay within the same six-digit NAICS code and meet the other conditions, can be structured far more efficiently than many owners realize.

That last point gets missed all the time.

A second location in the same line of business is not underwritten the same way as a new concept, even if both are called "expansion." If the new unit looks like a continuation of an operating model the owner already runs well, 7(a) can become much more attractive than owners expect. By contrast, if the project is mostly a building and the business already has enough liquidity for startup costs outside the loan, 504 may be the better fit.

The practical question is not which SBA program sounds better on paper. It is which structure matches the actual use of funds, the collateral, and the lender's risk view of the expansion.

The 0% Down Expansion A Game Changer for Growth

A 0% down SBA expansion loan is real, but only for a narrow set of deals. The owners who get it are usually opening another unit of a business they already run successfully, not testing a new concept.

The detail that drives this structure is the same six-digit NAICS code rule. If the expansion stays in the exact same line of business, keeps the same ownership, ties the existing operating company into the loan, and shows believable management control across both locations, lenders can often treat the request much more favorably on equity injection.

That matters because cash is usually tighter than projections suggest during an expansion. Opening costs run long. Hiring takes longer than expected. Working capital gets eaten up fast. Keeping that cash in the business instead of putting it in as down payment can materially improve the odds that the new location stabilizes.

The rule lenders actually underwrite to

Lenders do not approve this structure because the borrower found a clever interpretation of the SBA rules. They approve it when the file shows a repeatable operating model.

A second location has to read like a continuation of an established business. Same service mix. Same customer type. Similar staffing model. Similar day-to-day oversight. If the new unit starts to look like a different business wearing the same brand, the 0% down case gets weak quickly.

Four conditions usually need to line up

| Requirement | What it means in practice |

|---|---|

| Same 6-digit NAICS code as the existing business | The expansion must stay in the exact same line of business, not a nearby category. |

| Identical ownership structure | The ownership percentages and borrowing structure need to match, or the lender may treat it as a different risk. |

| Existing business joins as co-borrower | The operating company with the track record stands behind repayment. |

| Management can control both locations in a realistic way | The lender needs to see actual operating capacity, not just optimism. |

If one of those pieces is off, the deal often shifts back to a standard equity injection discussion.

I see two trouble spots more than any others. First, borrowers assume a related concept counts as the same business. It often does not. Second, they change ownership for the new location by adding a partner, investor, or family member, then wonder why the 0% down structure disappears.

Where borrowers lose the argument

“Close enough” is not a strong credit memo.

If the current company is a full-service restaurant and the new site is a grab-and-go cafe, the lender may view that as a different operating model. If the first location is owner-operated and the second is two states away with no proven district manager in place, the daily-control story gets harder to defend. The same issue comes up when one entity has a clean history but the expansion is being placed into a new structure with different ownership percentages.

These are not technicalities. They are risk signals.

When the facts fit, though, this is one of the best SBA expansion structures available. The business keeps more liquidity for payroll, inventory, and post-opening surprises. If seller carry or owner rollover is part of the capitalization, this guide to equity rollover strategies is a useful reference. If real estate is included in the project, review the SBA loan hazard insurance guide early, because insurance requirements can slow closing if nobody addresses them until the end.

Underwriting Demystified What Lenders Really Look For

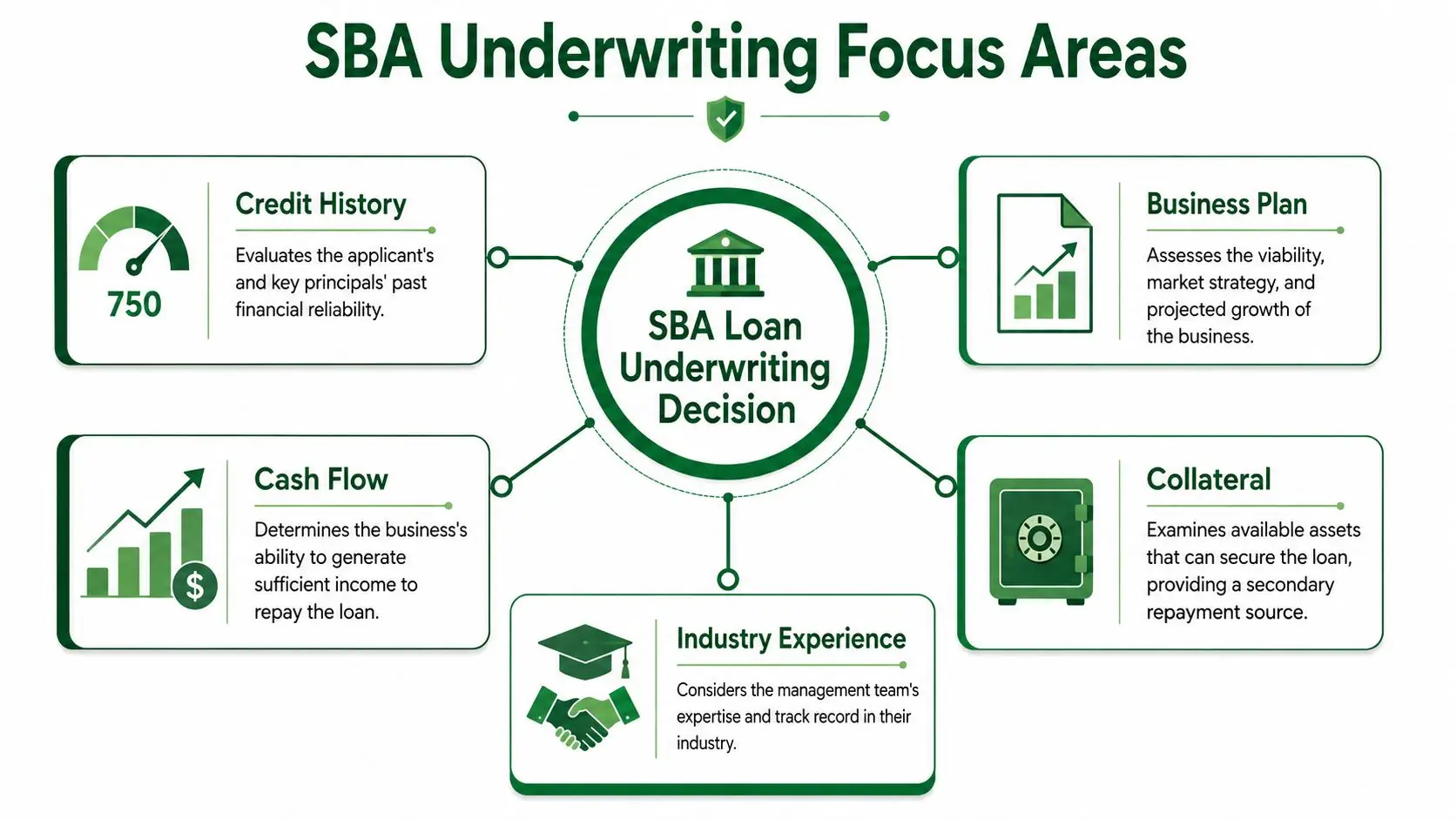

Lenders fund expansion when the file shows two things clearly. The business can carry the debt, and the owner can execute the plan without stretching operations too thin.

Cash flow is the first screen

Every strong SBA expansion file starts with repayment ability. Underwriters calculate debt service coverage by comparing business income to the full annual debt load after the new loan is in place.

DSCR = Net operating income / Total annual debt service

If coverage is too thin, the deal usually stalls early. A lender may still discuss structure, collateral, or guarantor support, but weak cash flow is the issue that drives the decision.

They also test whether that cash flow is dependable. Clean month-to-month reporting helps. So do stable gross margins, repeat customers, and a use-of-funds plan tied to revenue production. Build-out costs, equipment, hiring, and working capital each need to make operational sense.

For expansion deals tied to the same NAICS code strategy, this matters even more. The 0% down story is stronger when the borrower is not just opening another location, but showing a lender that the second unit follows the same operating model, the same revenue logic, and the same management playbook as the first.

Experience and execution matter more than borrowers expect

A lender does not underwrite an expansion plan on enthusiasm. The credit team wants proof that management can control another location, another crew, and another fixed-cost base.

That is why operators expanding within the same line of business get a better hearing. If the existing company already performs well in that NAICS code, the expansion case is easier to defend. If the new project starts to look like a different business, underwriting gets tighter fast. I see this issue all the time with restaurants, retail concepts, and service companies trying to pitch a related but not entirely identical model.

The practical question is simple. Does the new site behave like an extension of a business that already works, or does it behave like a startup wearing an expansion label?

The rest of the file still has to hold up

Strong cash flow and a familiar business model will not rescue a messy file. Underwriters still review:

- Credit history. They look for patterns, not perfection.

- Management depth. A second location needs clear oversight, especially if the owner cannot be in both places every day.

- Financial reporting quality. Incomplete books create doubt about margins, add-backs, and debt capacity.

- Ownership and guarantees. Anyone at 20% or more ownership should expect to sign a full personal guaranty.

That last point often affects structure. Owners sometimes add a passive partner or change equity splits for the new location, then find out they changed the approval path too.

Insurance also comes up earlier than many borrowers expect. On any deal involving real estate, lease requirements, or pledged collateral, this SBA loan hazard insurance guide is a useful reference because insurance conditions can delay closing if nobody addresses them until the credit approval is already in motion.

If you want a clearer view of how credit teams stack these factors and write the approval, read this guide on how SBA lenders underwrite your deal.

Your SBA Expansion Loan Application Timeline

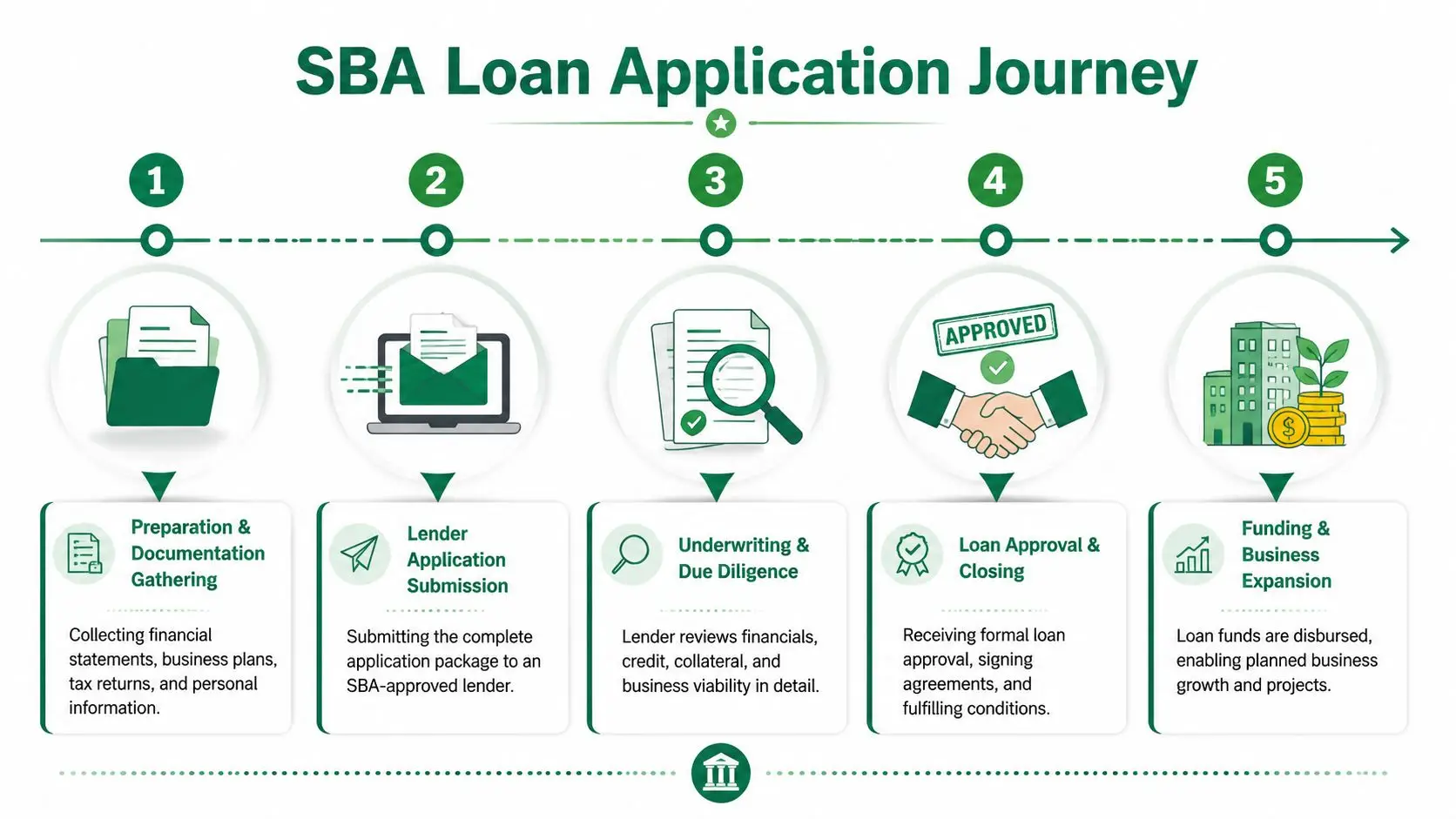

Expansion files do not stall because SBA lending is mysterious. They stall because the borrower submits documents in the wrong order, picks the wrong lender, or waits too long to answer routine credit questions.

A well-run file usually moves through five stages: preparation, lender selection, underwriting, closing, and funding. The timeline can be reasonably fast or painfully slow. The difference is rarely luck. It usually comes down to how well the deal is framed before it ever reaches credit.

Stage one and two getting lender ready

Preparation starts before the application. Gather business tax returns, interim financials, debt schedules, ownership documents, a current rent roll or lease if the project involves a new site, and a line-by-line use of funds. If the request includes working capital, build that number from actual hiring, inventory, equipment, or ramp-up needs. Vague requests create extra review.

For expansion deals, the narrative matters almost as much as the paperwork. If you are pursuing a 0% down structure, the file should show early that the new location operates under the same NAICS code as the existing business and follows the same operating model. That point should not appear halfway through underwriting after the lender has already viewed the deal as a startup.

Lender selection comes next. Some SBA lenders like owner-occupied real estate. Some are comfortable with multi-unit expansion. Some will spend time on a same-NAICS-code argument for a second or third location, and some will not. Choosing the right credit box at the start saves weeks. A good SBA loan broker for expansion financing helps by packaging the request for lenders that fund this type of deal.

A strong package answers four practical questions right away:

- What is being financed

- Why this expansion fits the existing business

- Who will run the new operation day to day

- How the business will support the new debt during ramp-up

Stage three through five from underwriting to funding

Underwriting is where the lender tests the story against the documents. They reconcile tax returns to interim statements, review debt obligations, confirm ownership, and compare projections to the performance of the current operation. On a 0% down expansion request, they also examine whether the new site is an expansion of an established business rather than a new concept under the same ownership.

That distinction affects timing. If the lender agrees the new location matches the existing business under the same NAICS code, the file often moves more cleanly because the expansion case is clear. If the file is mixed, new menu, new service line, different customer base, different staffing model, expect more questions and a slower path.

Approval is only credit approval. Closing still requires insurance, entity verification, signed leases or real estate documents, and any third-party reports tied to the collateral. Funding happens after those conditions are cleared, not when the term sheet is issued.

Here is the practical sequence I give clients:

- Prepare the file. Submit complete documents the first time.

- Match the lender. Send the deal to a bank or nonbank SBA lender that likes expansion credit.

- Respond during underwriting. Answer questions quickly and with documents, not long explanations.

- Clear closing conditions. Track insurance, entity documents, leases, and deposits in parallel.

- Fund and deploy proceeds. Use the money exactly as approved.

Fast responses matter. I have seen strong borrowers lose two or three weeks because nobody owned the checklist after approval.

Common Pitfalls and How a Broker Streamlines the Process

A surprising number of SBA expansion deals are fundable in principle but fail in presentation. The business may be healthy. The owner may be experienced. The expansion plan may even be reasonable. Then the package goes out incomplete, the wrong lender sees it first, or the borrower frames the deal in a way that creates avoidable credit concerns.

Mistakes that kill solid deals

Here are the errors I see most often in expansion financing:

- Incomplete projections: A lender can't rely on a growth story that has no disciplined assumptions behind it.

- Weak explanation of use of funds: “General expansion” is vague. Lenders want specific deployment.

- Wrong lender fit: Some lenders are comfortable with multi-unit expansion. Others are not.

- Messy ownership records: Entity mismatches and unclear ownership percentages create immediate friction.

- Late-stage surprises: Unresolved tax issues, insurance gaps, or collateral questions often surface when the deal should be closing.

These mistakes don't always produce a hard decline. Sometimes they produce something slower and more frustrating. The file just stalls.

What an experienced broker fixes

A strong broker improves more than convenience. Its primary value is in translation and fit.

A broker can help by:

- Packaging the deal correctly: The narrative, projections, and use-of-funds schedule need to match lender logic.

- Directing the file to the right credit box: Industry appetite matters. So does loan purpose.

- Managing follow-ups: Borrowers often slow deals by answering questions loosely or inconsistently.

- Reducing lender shopping fatigue: One organized process is better than sending partial files to multiple banks.

This is especially true in SBA lending, where the surface-level facts of a transaction often matter less than how the file is documented and positioned. If you want a clear sense of what a specialist does in that process, this guide to working with an SBA loan broker lays it out well.

Real World Expansion Financing Scenarios

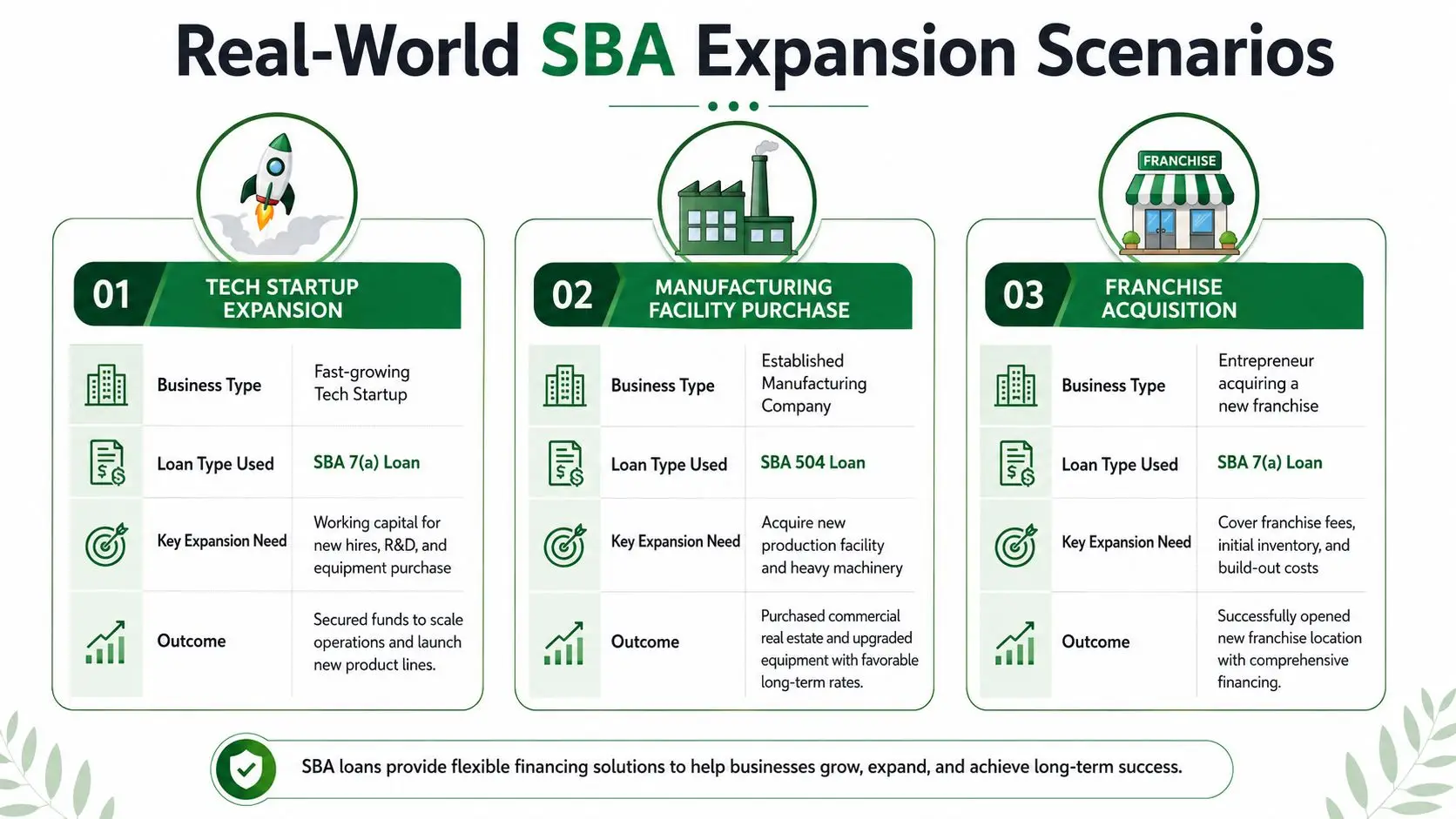

The right SBA expansion structure depends less on the word "expansion" and more on what the business is doing, what it is buying, and whether the new location or operation clearly stays within the same NAICS code.

Three ways owners actually use these programs

A pizzeria with one profitable location wants to open a second store across town. Same menu, same ownership, same supplier relationships, same operating model. That is the cleanest kind of file for the 0% down argument discussed earlier, because the expansion looks like a continuation of the existing business rather than a new venture. In practice, this works best when the borrower can show the new store will operate under the same line of business and fit the same NAICS code.

A machine shop needs a larger building, added production space, and new equipment to take on more contracts. A 504 structure often fits better here because the project is tied to owner occupied real estate and long-life equipment, not just working capital. The trade-off is straightforward. The borrower usually brings equity into the deal, but gets fixed-asset financing built for that purpose.

A digital marketing agency wants to add staff, expand sales, and cover the ramp-up costs tied to onboarding new clients. There may be no real estate purchase at all. A 7(a) working capital loan usually makes more sense in that case because it gives the business flexibility to fund hiring, operating expenses, and growth costs that do not fit neatly into a fixed-asset structure.

I see owners get tripped up when they assume all three scenarios should be financed the same way.

They should not. The strongest approvals come from matching the loan structure to the actual expansion plan, then documenting why the plan is a continuation of the current business, especially if the borrower is trying to qualify for a 0% down expansion.

Frequently Asked Questions About Expansion Financing

Strong expansion files get approved faster when the borrower asks the right questions early. These are the ones I hear most from owners trying to add a location, buy a larger building, or fund growth without putting unnecessary cash into the deal.

Can I use an SBA loan for expansion if I'm not buying real estate?

Yes. A 7(a) loan can cover hiring, inventory, equipment, leasehold improvements, marketing, and working capital tied to the expansion plan. Real estate is only one use case.

Is expansion financing the same as acquisition financing?

No. Lenders underwrite them differently. But for equity injection, some expansion deals can qualify for the same favorable treatment if the new operation is clearly a continuation of the existing business.

That point matters more than many owners realize.

Can I get 0% down for a new location?

Sometimes, yes. The cleanest path is when the new location stays within the same line of business and the same NAICS code. If the expansion looks like the business you already run, with the same services, customers, suppliers, and operating model, the 0% down argument is much stronger.

Can I expand into a completely different industry and still get 0% down?

Usually no. A restaurant owner opening a manufacturing company is not an expansion in the way lenders want to see it. That looks like a new business venture, and new ventures typically bring a higher equity requirement.

Do all owners have to sign personally?

For 7(a) loans, any owner with 20% or more of the business is generally required to provide a personal guaranty. Minority owners below that threshold may still be asked for limited support in some deals, depending on lender policy and deal strength.

How long does my business need to be operating before I apply?

There is no single minimum that fits every lender. What matters in practice is whether the business has enough operating history to show repayment ability, stable management, and a believable expansion case. A clean, profitable business with a clear plan gets a much better reception than a newer company with thin margins and vague projections.

What if I ask for more than the lender wants to offer?

That happens all the time. Good borrowers build a plan with room to adjust. If the lender trims the working capital request, lowers the equipment amount, or requires a smaller phase-one rollout, the deal can still move forward without forcing a rewrite of the entire expansion strategy.

Is a 504 loan ever the better expansion tool?

Yes. If the project is driven by owner-occupied real estate or heavy equipment with a long useful life, 504 often fits better than 7(a). The trade-off is flexibility. A 7(a) loan usually handles mixed-use expansion costs better, while 504 is built for fixed assets.

If you're planning an expansion and want to know whether your deal fits a standard SBA structure or a true 0% down path, GoSBA Loans can help you evaluate the options, match the deal with the right SBA lender, and move from idea to a lender-ready package without wasting time on the wrong structure.