You're probably looking at a deal where the purchase price works, the business fits, and the lender is interested, but the capital stack still feels tight. That's where equity roll over enters the conversation. In the lower middle market, it's often the difference between a deal that dies over cash at close and one that gets done with both sides still aligned after closing.

For buyers using SBA financing, this topic gets more nuanced fast. A seller keeping equity is not the same thing as a seller note on standby. Lenders care about that distinction. So do lawyers, accountants, and anyone trying to avoid an ugly surprise after closing.

Table of Contents

- What Is an Equity Rollover in a Business Sale

- Key Motivations for Using Rollover Equity

- Structuring an Equity Rollover Deal

- Equity Rollover and SBA Loan Requirements

- Navigating Tax and Legal Implications

- How to Negotiate Rollover Equity Terms

- Equity Rollover FAQs

What Is an Equity Rollover in a Business Sale

A buyer agrees to pay $4 million for a company. The seller takes $3.2 million in cash at closing and reinvests $800,000 into the new ownership entity. That $800,000 is rollover equity.

An equity rollover means the seller sells the business but keeps part of their value invested after closing instead of taking all proceeds in cash. In practical terms, the seller converts a slice of sale proceeds into ownership in the post-close company.

A simple example helps. If the business grows and sells again in a later recapitalization or exit, the seller can share in that future gain because they still own part of the company. If performance slips, that rolled equity can also lose value. That is the trade-off.

In lower middle market deals, rollover equity is often negotiated as a percentage of the seller's total proceeds. There is no fixed market rule. The amount depends on deal risk, how involved the seller will remain, the buyer's capital structure, and whether the senior lender will accept the proposed terms.

That last point matters in SBA acquisitions. A rollover is equity in the new company. It is not the same as a seller note, and it is not the same as a seller note on full standby for SBA injection purposes under the SBA SOP. Buyers mix these up all the time. Lenders do not. If you are using SBA financing, that distinction affects how the lender underwrites the borrower's injection, control, and post-close ownership structure.

Practical rule: Rollover equity should be treated as a new investment by the seller, with real upside and real downside, not as delayed purchase price dressed up with a different label.

What it usually looks like

Most rollover structures are straightforward on paper but sensitive in execution. The seller receives cash at closing, then receives equity in the buyer's holding company or the post-close operating company based on the agreed structure. The governing documents define voting rights, distributions, drag-along rights, tag-along rights, transfer limits, and what happens if the seller leaves the business early.

In sponsor-backed deals, rollover equity often sits alongside outside investor capital. In some independent sponsor transactions, the capital stack can also include minority equity checks from outside groups such as minority equity capital for independent sponsor-led acquisitions. That can make the rollover more attractive, but it also means the seller needs to understand where their equity sits in the post-close structure and who controls the next exit.

Why the distinction matters

A seller note creates a debt claim. Rollover equity creates an ownership interest. Debt has a repayment schedule and negotiated priority. Equity gets paid after debt and depends on company value.

That difference becomes especially important if the transaction is being structured for a lender-approved closing and a successful business ownership transition. The cleanest deals match economics, documents, and SBA lender expectations from the start, rather than trying to force a rollover into the role of a standby note or borrower injection substitute.

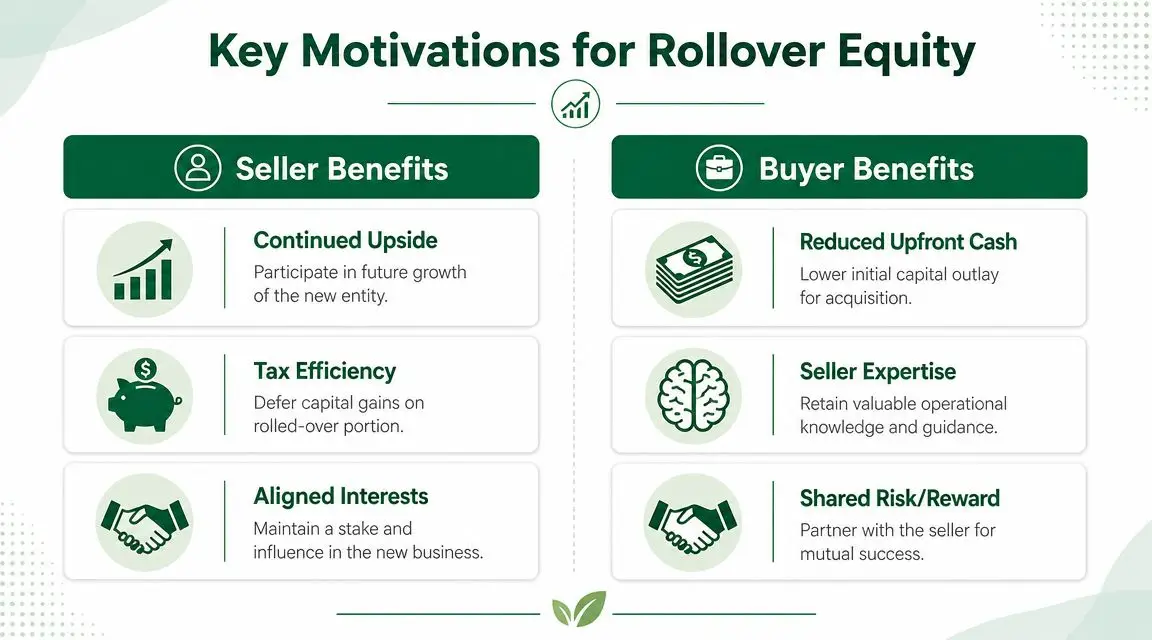

Key Motivations for Using Rollover Equity

Rollover equity has moved from niche structuring tool to standard deal language in many private transactions. One industry report says private equity deals involving rollover equity rose from 46% in 2020 to 57% in 2023, and that rollover equity appeared in about 70% of lower middle market deals for businesses with $5 million to $50 million in annual revenue, according to City Different Investments' rollover equity analysis.

That trend tracks with what buyers and lenders care about most. Cash efficiency, continuity, and alignment.

Why buyers push for it

A buyer usually asks for a rollover when one or more of these are true:

- The debt package is tight: Less cash at closing can make the full acquisition stack more workable.

- The seller still matters operationally: If the seller knows the customers, staff, vendors, or systems, keeping them invested can reduce transition risk.

- The lender wants confidence: A seller who keeps equity is signaling belief in the company's future, not just trying to maximize day-one proceeds.

This is one reason rollover often shows up in sponsor-backed and independent sponsor deals. If you want a useful adjacent example of how minority capital can support acquisition structures, see this review of minority equity capital for independent sponsor-led acquisitions.

Why sellers agree to it

The seller's motivation is different. They're usually asking a harder question: “Am I getting paid enough today, and am I protected enough tomorrow?”

Common seller motivations include:

- Future upside: The seller may participate in a second exit.

- Tax treatment: The rolled portion may receive different tax treatment than cash proceeds, depending on structure and advice.

- Relationship advantage: If the seller remains involved, equity can preserve influence that pure cash does not.

Later in the process, many buyers benefit from seeing how experienced investors frame this. This video offers a useful discussion of rollover mechanics and incentives.

The strongest rollover deals work because each side is solving a different problem with the same tool.

What does not work

Rollover equity fails when the parties use it as a vague compromise instead of a defined investment term.

A weak structure usually has one of these flaws:

| Problem | Why it hurts the deal |

|---|---|

| Seller rolls equity without clear rights | The seller may own paper with little control or visibility |

| Buyer treats rollover as substitute trust | Equity doesn't fix poor diligence or weak transition planning |

| Lender sees unresolved structure questions | Ambiguity around ownership, governance, or source of funds slows approval |

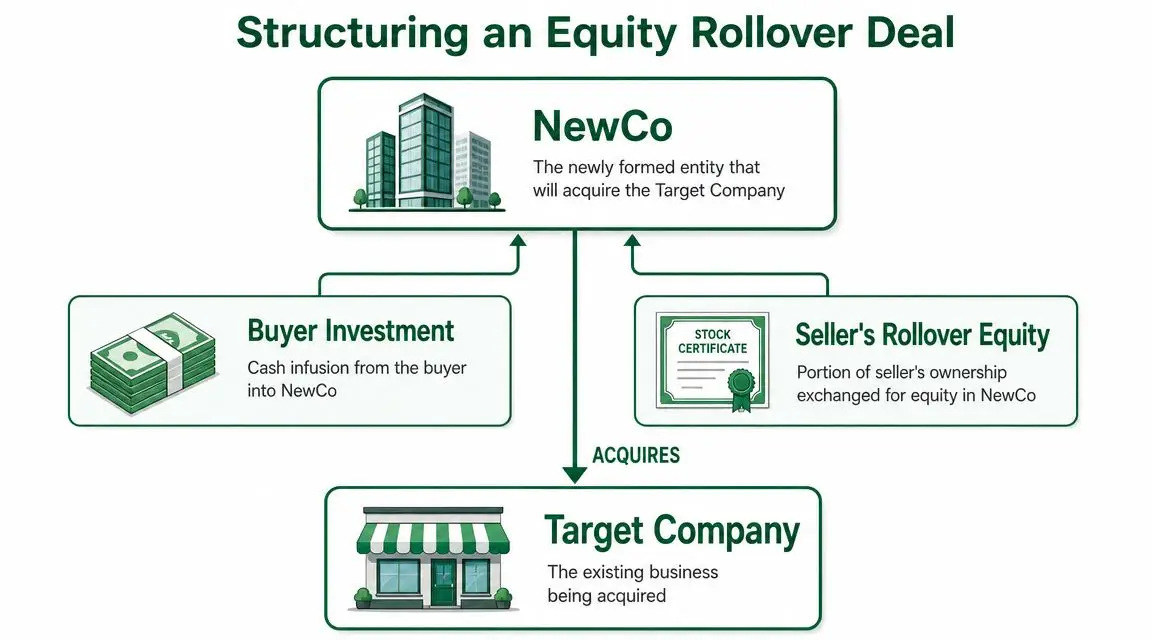

Structuring an Equity Rollover Deal

Most rollover deals are built through a new acquisition entity, often called NewCo. NewCo raises the money, buys the target business, and issues ownership interests to the buyer group and, if negotiated, to the seller.

The mechanics matter because “seller kept equity” can mean very different things depending on where that equity sits and what rights attach to it.

The basic build

A standard structure usually has four moving parts:

- Buyer cash equity goes into NewCo.

- Senior debt is raised by NewCo or a related borrower.

- Seller rollover equity is issued by NewCo to the seller.

- Target company is acquired by NewCo.

In some deals, the seller rolls into the direct acquisition vehicle. In others, the seller receives equity higher up in the holding company chain. That distinction matters because rights can change based on where the equity sits.

A simple sample structure

Below is a basic illustration. The numbers are only an example to show mechanics, not a market benchmark.

| Sources of Funds | Amount | Uses of Funds | Amount |

|---|---|---|---|

| Buyer equity | Buyer cash contribution | Purchase price paid at closing | Cash paid to seller |

| Senior loan | Lender financing | Fees and closing costs | Transaction expenses |

| Seller rollover equity | Portion reinvested by seller | Equity retained in NewCo | Seller's post-close ownership |

This framework helps buyers visualize the capital stack. It also forces the right questions early: What is cash? What is debt? What is true equity? What gets repaid first? Who has control?

For transactions that also use seller debt, it helps to compare rollover equity with seller financing for business acquisition. They are related tools, but they behave very differently in underwriting and at exit.

Cap table questions that matter

A cap table is just the ownership table after closing. But buyers shouldn't stop at percentages.

Focus on these issues:

- Common vs preferred equity: The same percentage can carry different economics.

- Pari passu vs subordinated economics: If the seller's rolled equity sits on equal footing with the buyer's equity, the parties share upside and downside more evenly. If it's structurally or economically subordinate, the seller may recover value only after other investors do.

- Waterfall mechanics: Sale proceeds may not flow strictly by ownership percentage. Distribution rules can shift value materially.

- Repurchase rights: If the seller stays on as an employee, check whether the company can buy back their equity on departure.

Buyers often focus on how much equity the seller rolls. Sophisticated sellers focus on what that equity can actually do.

What works in practice

The cleanest rollover structures usually have these features:

- Clear entity placement: Everyone knows whether the seller owns in the opco, holdco, or acquisition vehicle.

- Simple economics: Avoid exotic preferences unless there's a specific reason.

- Aligned documents: The LOI, purchase agreement, operating agreement, and lender package all describe the rollover consistently.

- Realistic governance: Minority equity with no information rights becomes a source of conflict later.

A rollover structure works best when the parties can explain it on one page before the lawyers turn it into fifty.

Equity Rollover and SBA Loan Requirements

Often, many buyers get tripped up. In an SBA 7(a) acquisition, equity rollover is not automatically the same thing as equity injection. And it is definitely not the same thing as a seller note on standby.

Those differences matter because the SBA and the lender are analyzing eligibility, borrower injection, change of ownership structure, and post-close control. If you blur those categories, you can create avoidable underwriting friction.

Rollover equity versus seller note on standby

A pure rollover means the seller keeps ownership in the post-closing business. The seller is still an equity holder after the deal closes.

A seller note on full standby is debt, not equity. The seller is owed repayment, but agrees not to receive principal or interest payments during the required standby period under the loan structure.

That distinction is critical in SBA deals because the SBA has specific rules for when standby seller debt can help satisfy part of the required injection. Buyers who are working through this issue should understand the current framework around SBA equity injection for acquisitions.

Why lenders care

From a lender's perspective, rollover equity can be a positive sign. It shows the seller remains exposed to the future performance of the business. That often supports the lender's comfort around continuity and transition.

But lenders still want clean answers to practical questions:

- Will the seller remain an owner after closing?

- If yes, what percentage will they own?

- Will the seller have control rights that conflict with SBA rules or lender expectations?

- Is the seller also carrying a note?

- If there is standby debt, does it satisfy SBA requirements?

The common misunderstanding

A lot of buyers hear “seller staying in the deal” and assume all seller participation helps the injection requirement the same way. It doesn't.

A seller who rolls equity is making an ownership investment. A seller who takes a note on full standby is extending credit under a constrained payment arrangement. Those are not interchangeable just because both reduce buyer cash at closing.

If your lender asks whether the seller is rolling equity or carrying standby debt, “both” can be a valid answer. But each piece has to be documented and underwritten on its own terms.

What usually works better with SBA lenders

In SBA-backed acquisitions, the most lender-friendly structures are usually the ones with plain logic:

| Structure feature | Why lenders tend to like it |

|---|---|

| Clearly documented buyer control | It avoids confusion around who runs the business post-close |

| Seller's role defined in writing | It reduces ambiguity about transition and affiliation concerns |

| Standby note terms separated from equity terms | It keeps injection analysis cleaner |

| Operating agreement aligned with loan documents | It prevents late-stage legal conflicts |

A practical takeaway for buyers

If you're using SBA debt, don't negotiate rollover equity in isolation from the financing. The ownership terms, injection rules, standby note treatment, and control provisions all need to line up before you get deep into documents.

That's why a structure that works in a private equity deal may need to be simplified or adjusted in an SBA 7(a) deal. SBA lending is not anti-rollover. It is anti-ambiguity.

Navigating Tax and Legal Implications

The biggest mistake sellers make with equity roll over is assuming that if the headline valuation looks good, the rollover must also be good. That's not how these deals work.

The rollover piece is a separate investment with its own legal terms, tax consequences, liquidity limits, and downside risk. A seller can get an attractive purchase price and still receive weak rollover paper.

Tax upside is real, but structure drives the result

Rollover equity is often attractive in part because the rolled portion may be structured in a tax-deferred manner, while the cash portion is typically the amount taxed at sale. But “may” is doing a lot of work there.

The tax result depends on deal structure, entity type, contribution mechanics, and how counsel papers the transaction. Buyers shouldn't promise tax outcomes. Sellers shouldn't rely on assumptions.

Illiquidity is not a footnote

A seller who takes cash can use cash immediately. A seller who takes rollover equity usually cannot.

That matters more than many founders expect. Credible sources repeatedly emphasize that liquidity timing is a core risk, and that sellers often don't get clear answers about when they can convert the rollover into cash, how preemptive rights work, or how dilution plays out if new capital comes in, as discussed in PCE Companies' overview of rollover equity considerations.

The legal terms that change the economics

The key legal risk is that ownership percentage alone doesn't tell you the value of the investment.

Look closely at:

- Preemptive rights: Can the seller buy enough new equity to avoid dilution?

- Tag-along rights: Can the seller participate if the majority owner sells part of its stake?

- Drag-along rights: Can the majority force the seller into a sale?

- Call rights or repurchase rights: Can the company buy back the seller's units, and on what terms?

- Information rights: Will the seller receive financial reporting?

A practical way to review these issues faster is to use tools that flag ownership, payment, and repurchase provisions before final markup. Something like AI legal contract analysis can help a buyer or seller spot terms worth escalating to counsel, though it doesn't replace an M&A attorney.

Sellers should treat the operating agreement like part of the purchase price. Because it is.

Control can disappear faster than value

After closing, the seller is usually a minority investor. That means limited control, even if the seller built the business and still works in it.

If the buyer raises more equity, acquires add-ons, restructures management, or changes distributions, the seller may have little practical ability to stop it. That doesn't mean rollover is bad. It means rollover is a negotiated minority investment, not a sentimental continuation of prior ownership.

How to Negotiate Rollover Equity Terms

The percentage rolled is only the opening bid. The actual negotiation starts after that.

Neutral advisory sources note that rollover can be as little as 5% and as much as 49%, while typical rolled equity today is often 20% to 35%, and they also warn that valuation is not just about headline price but about class rights, waterfalls, and liquidity timing, as explained in GHJ Advisors' discussion of rollover equity trends.

What sellers should press on

A seller should negotiate the rollover as if they were making a fresh investment into an unfamiliar private company. Because that's what they're doing.

Start with these pressure points:

- Valuation equivalence: Is the rollover priced on the same basis as the buyer's equity?

- Security class: Are the seller's units economically equal to management or sponsor units?

- Exit participation: Does the seller share proportionally in a future sale?

- Reporting access: Will the seller receive regular financials and tax documents?

What buyers should keep clean

Buyers often hurt themselves by overengineering the rollover. A structure can be technically brilliant and still impossible to finance or explain.

What tends to work better:

- Keep the ownership story simple.

- Define governance rights early.

- Match the LOI to the final legal documents.

- Avoid offering “same economics” if the documents don't deliver that result.

Terms worth naming directly

These terms shouldn't be left vague:

| Term | Why it belongs in the negotiation |

|---|---|

| Board or observer rights | They define visibility and influence |

| Tag-along rights | They protect minority holders in partial exits |

| Drag-along rights | They determine whether a minority can be forced to sell |

| Distribution policy | It affects whether paper gains ever turn into cash |

| Dilution protections | They matter if new equity is later issued |

A good rollover negotiation doesn't try to eliminate all risk. It prices the risk clearly and allocates it knowingly.

Equity Rollover FAQs

Can rollover equity count the same as the buyer's SBA down payment

Not automatically. In SBA deals, rollover equity and seller standby debt are different concepts. The lender and SBA analysis will focus on ownership, control, and whether any seller note satisfies the applicable standby and injection rules. Don't assume one can be substituted for the other without lender review.

What happens to the seller's rolled equity if the business performs badly

The seller is still an equity investor. If the business loses value or fails, that rollover can lose value or become worthless. Equity sits behind senior debt. That's why sellers need to evaluate rights, dilution exposure, and liquidity limitations before agreeing to roll.

When does the seller usually get cash for the rollover piece

Usually at a later liquidity event, not on demand. That could be a resale of the business, a recapitalization, a buyback if documents allow it, or another negotiated transaction. The timing is often uncertain, which is why liquidity terms matter as much as headline valuation.

If you're buying a business with SBA financing and need to pressure-test the capital stack before signing, GoSBA Loans can help you evaluate lender fit, seller note standby options, investor structure, and closing strategy early enough to avoid a broken deal later.

Drafted with Outrank