If your commercial mortgage matures soon, you're probably looking at two uncomfortable facts at the same time. Your current payment may have been built on a cheaper rate environment, and the lender reviewing your refinance today is underwriting the deal on current cash flow, current value, and current risk, not on what the property looked like when you bought it.

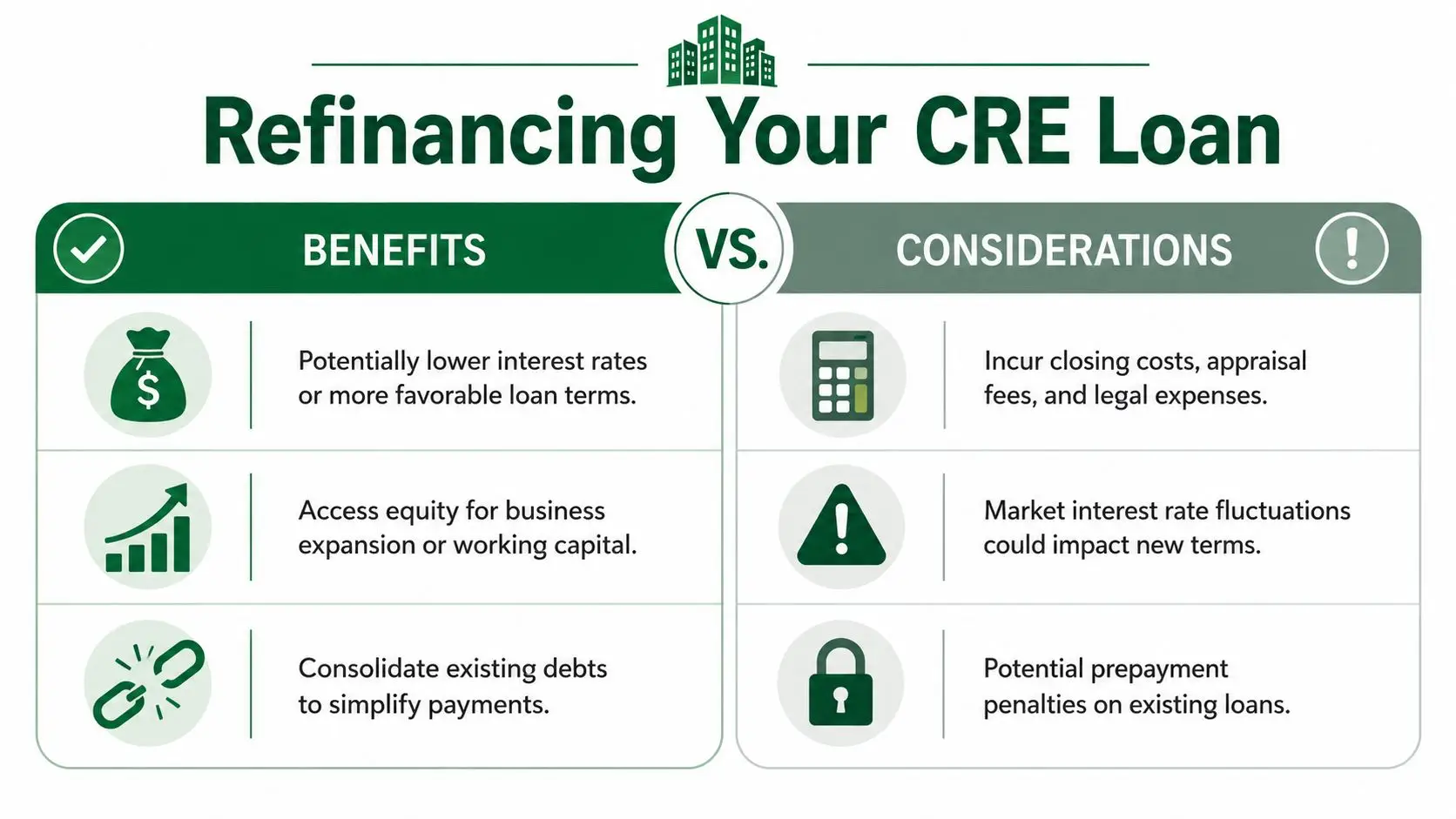

That's where many owners get stuck. They assume refinancing is a routine rollover. It often isn't. A smart commercial real estate refinance can improve monthly cash flow, extend amortization, pull out equity, or replace a loan that no longer fits the business. A bad approach wastes months, triggers appraisal surprises, and sends borrowers down loan programs they were never eligible for in the first place.

Table of Contents

- Why 2026 Is a Critical Year for CRE Refinancing

- Understanding Commercial Real Estate Refinancing Goals

- Comparing Your Commercial Refinance Loan Options

- The SBA Advantage for Owner-Occupied Properties

- Eligibility Costs and Key Approval Metrics

- Your CRE Refinance Timeline and Checklist

- Maximizing Your Refinance Success

Why 2026 Is a Critical Year for CRE Refinancing

A lot of owners are entering 2026 with the same problem. The note that looked manageable a few years ago is approaching maturity, the lender wants fresh underwriting, and the property now has to carry a refinance in a more demanding credit environment.

The reason this feels crowded is that it is. In 2025, approximately $957 billion in commercial real estate loans matured, nearly triple the 20-year average. With an additional $998 billion maturing in 2025 and a projected $1.148 trillion in 2026, the refinancing wall is expected to continue through 2028, according to CoreCast's refinancing trends update.

That market pressure changes borrower behavior. Owners who used to wait for a maturity notice are moving earlier, comparing structures earlier, and getting serious about debt strategy instead of treating refinance as paperwork. If you're reviewing options now, that's the right instinct.

For a broad sponsor-level overview, the Homebase guide for real estate sponsors is a useful companion read because it frames refinance decisions from the capital stack side rather than only from the borrower side. If your priority is payment planning, it also helps to keep an eye on current financing conditions through resources like this SBA loan rates overview.

Practical rule: A refinance gets harder when you start with urgency instead of options.

The owners with the best outcomes usually aren't chasing the single lowest headline rate. They're solving for fit. That means choosing a structure that matches the property, the occupancy profile, the business, and the amount of cash they want to keep in the company after closing.

Understanding Commercial Real Estate Refinancing Goals

Refinancing commercial property is a lot like trading in a vehicle. Sometimes you replace the old loan to get better terms on the same asset. Other times, you replace the old loan and pull cash out because the asset has built equity and the business has a better use for that capital.

Rate and term refinance

A rate and term refinance replaces the existing loan to improve the structure. The goal might be a longer repayment period, a better interest rate, a more stable payment, or a cleaner maturity schedule.

This is the right move when the business doesn't need to extract equity and the owner's main objective is monthly payment relief or debt stability. For many owner-users, this is the cleanest path because underwriters focus on whether the new debt works, not on whether the borrower is also trying to pull capital out.

A rate and term refinance usually makes the most sense when:

- The current loan is maturing soon. You need an exit before the existing note creates pressure.

- The payment is too tight. Extending amortization can improve monthly debt service.

- The old structure no longer fits. Balloon features, variable-rate exposure, or lender restrictions may be the actual problem.

Cash out refinance

A cash-out refinance does more. It replaces the existing loan and tries to return part of the property's equity to the borrower at closing. Owners commonly use that liquidity for equipment, expansion, partner buyouts, improvements, or working capital.

That sounds attractive, but it's where many deals break down. As soon as you ask for proceeds beyond paying off the old loan, debt limits and cash flow requirements become more important. The property must support a larger debt load, and the valuation has to cooperate.

Borrowers often focus on available equity. Lenders focus on supportable debt.

Picking the right goal before you shop lenders

This matters more than people think. If you present a deal as a cash-out request when your real goal is payment relief, you may push yourself into a harder underwriting box than necessary. If you present a deal as rate-and-term when the business needs liquidity, you may close the wrong loan and still have a capital problem a few months later.

Use this simple lens:

| Refinance goal | Best fit when | Main concern |

|---|---|---|

| Rate and term | You want stability, lower payment pressure, or a new maturity structure | Whether the property supports the replacement debt |

| Cash out | You want to unlock equity for business use | Whether valuation and cash flow support the larger loan |

The strongest refinance strategy starts with one clear answer to one question. Are you trying to improve the loan, or are you trying to improve the business balance sheet with property equity?

Comparing Your Commercial Refinance Loan Options

The right loan type depends on occupancy, speed, recourse tolerance, property quality, and how forgiving the lender will be when the story isn't perfect. A borrower refinancing an owner-occupied building should not shop the market the same way an investor refinancing a multi-tenant asset does.

Here's a practical comparison.

| Loan Type | Best For | Typical LTV | Key Feature |

|---|---|---|---|

| Conventional Bank Loan | Stable properties and strong borrowers | Varies by lender | Relationship-driven underwriting |

| CMBS Loan | Larger investment properties needing fixed structure | Varies by lender | Securitized execution with less flexibility |

| Bridge Loan | Time-sensitive or transitional situations | Varies by lender | Speed and temporary relief |

| SBA Loan | Owner-occupied properties | Up to 90% for eligible owner-occupied structures | High leverage with long terms |

For owners comparing a wider set of debt products, this roundup of 2026 commercial real estate financing is useful because it lays out how lenders position different capital sources across property and borrower profiles. If your building is owner-occupied, the key product family to understand is the SBA 504 loan structure.

Conventional bank loans

Banks are often the first call because they're familiar. If the property is clean, the business financials are strong, and the borrower has liquidity, a bank refinance can work well.

The trade-off is flexibility. Banks usually want a straightforward credit story. If the debt service is tight, the appraisal comes in soft, or the collateral position is thinner than expected, many banks will either reduce proceeds or decline the request. They can be very effective for stabilized deals and very unforgiving for edge cases.

CMBS loans

CMBS can fit certain investment-property refinances, especially when the borrower wants fixed structure and can live with a more rigid servicing environment. The issue is usually not getting the deal closed. The issue is what happens later if the borrower needs a modification, consent, or some flexibility around unexpected events.

That's why CMBS usually isn't my first recommendation for owner-occupied borrowers. It can solve a pricing problem and create an operating problem.

Bridge loans

Bridge debt is useful when timing is the main problem. If a loan is maturing and the property needs more time to stabilize, lease up, or complete a business transition, bridge financing can buy breathing room.

It's a tool, not a destination. The mistake is treating bridge debt as a long-term fix. It works best when there is a clear next step, such as a later refinance into bank or SBA debt after the property and financials are cleaner.

A bridge loan is often the right answer when the real refinance isn't ready yet.

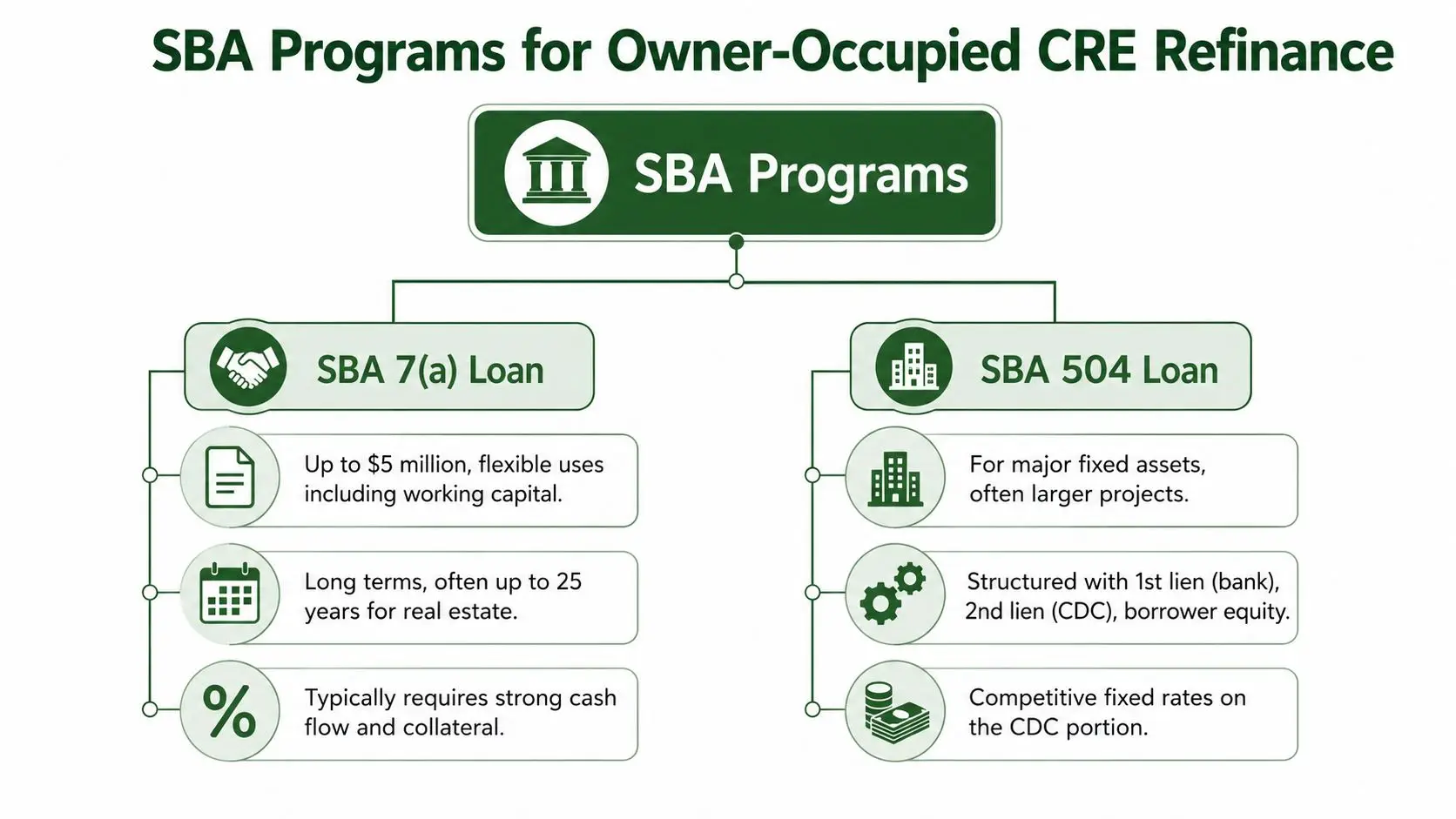

SBA loans

For owner-occupied properties, SBA often deserves the first serious look, not the last. According to Clearhouse Lending's discussion of commercial cash-out refinance structures, SBA 504 and 7(a) programs can offer up to 90% LTV with fixed rates and terms up to 25 years for owner-occupied properties, compared with the 75% cap typical of conventional bank loans for investment properties.

That difference changes outcomes. More debt financing can reduce cash required at closing. Longer terms can improve monthly debt service. For business owners who need the building to support the business, not the other way around, that's often the deciding factor.

The SBA Advantage for Owner-Occupied Properties

A common refinance scenario looks like this. The business is healthy, the building is central to operations, and the owner wants lower payments or cash out for expansion. The bank offers a tighter loan amount, a shorter amortization, and more cash due at closing than the borrower expected. For many owner-occupied properties, that is the point where SBA should move to the top of the list.

Why SBA often wins on structure

SBA lending tends to work better for owner-users because the loan is underwritten around the operating business and its use of the property, not just the property as stand-alone collateral.

That changes the structure in practical ways. Longer amortization can lower monthly debt service. Higher allowable financing can reduce the cash the borrower has to bring in. Under 7(a), the proceeds can also be more flexible, which helps when the refinance needs to solve more than one problem, such as real estate debt plus working capital or business cleanup.

Borrowers who are still sorting out whether their property qualifies should review this guide to owner-occupied commercial real estate loans. Owner occupancy is the first screen, and it determines whether SBA belongs in the conversation at all.

The 504 rule that trips people up

Many borrowers hear that SBA 504 is a strong refinance option and assume any owner-occupied building can fit. SBA SOP rules are tighter than that, and 2026 borrowers need to screen for them early.

According to TMC Financing's explanation of 504 refinance eligibility, the debt being refinanced must be at least two years old and cannot already carry a government guarantee. That creates a frequent problem for owners who bought with SBA 7(a) financing and expect to move into 504 later.

That assumption burns time. I have seen borrowers spend weeks gathering documents and ordering third-party reports for a 504 refinance that was never eligible because the original note missed one of those gates.

Use a simple triage process before comparing rates:

- Verify the original loan type. Existing government-guaranteed debt can block a 504 refinance.

- Verify the seasoning period. If the debt has not aged long enough, strong revenue and strong credit will not cure the issue.

- Verify owner occupancy and business use. Program fit comes before pricing.

Underwriting reality: SBA eligibility rules are pass-fail. Strong cash flow does not override a disqualifying program rule.

When 7(a) makes more sense

A borrower does not need 504 to have a strong SBA refinance option. In many cases, 7(a) is the better fit because it gives more flexibility on use of proceeds and debt restructuring.

That matters when the primary objective is broader than replacing a property note. A 7(a) refinance can work better if the transaction also needs to address partner buyout pressure, higher-cost business debt, or liquidity strain that is hurting operations. I tell borrowers to choose the program that matches the problem, not the one with the best headline rate.

That same discipline applies to debt service analysis. Borrowers who need help navigating business funding should pay close attention to how the new payment interacts with company cash flow, because the best refinance on paper can still fail if the structure strains the business after closing.

The SBA SOP controls the answer more than summary articles do. A good refinance strategy starts with program eligibility, then moves to structure, then pricing.

Eligibility Costs and Key Approval Metrics

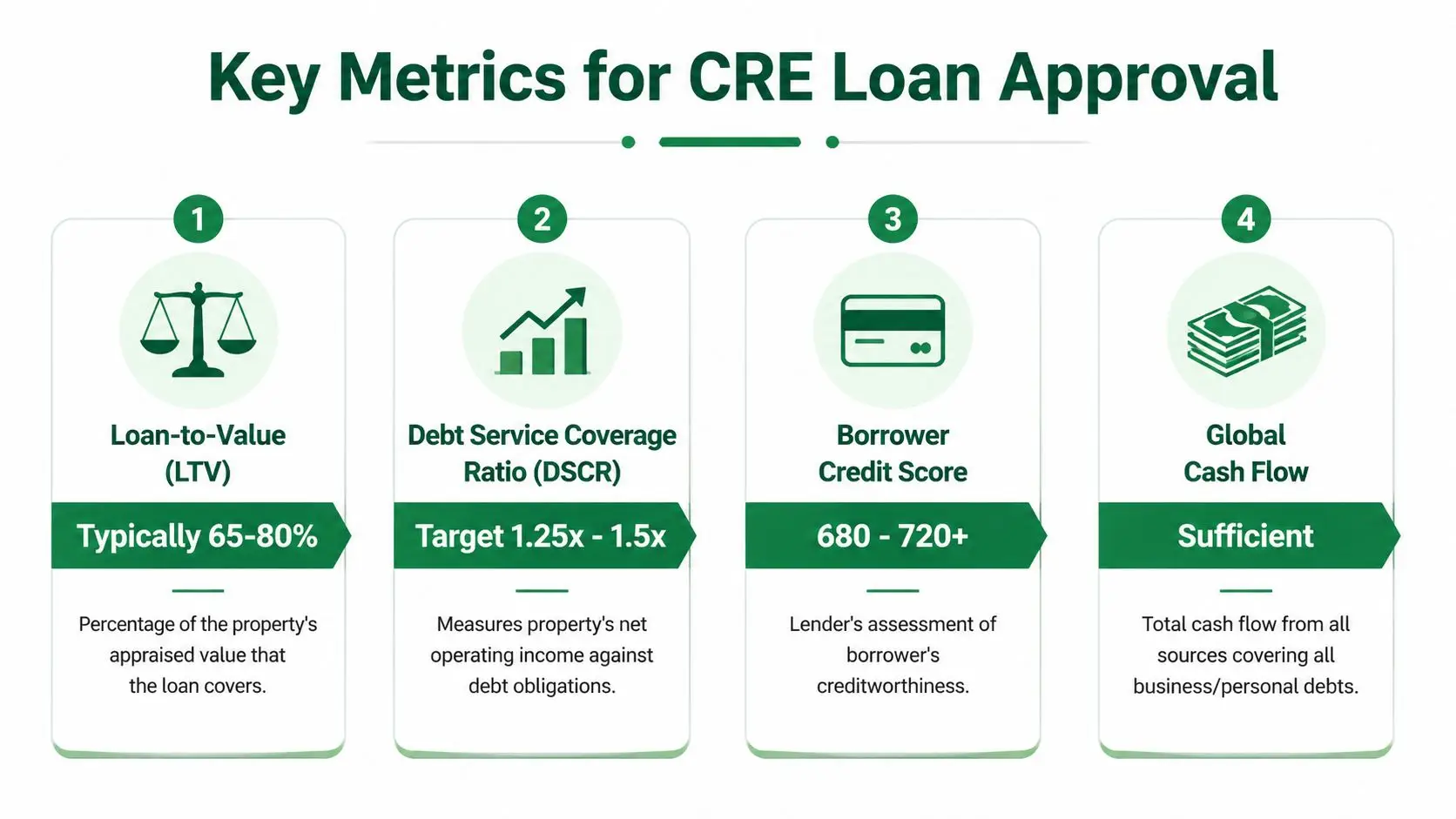

Approval usually turns on four numbers. Value, debt service coverage, global cash flow, and liquidity. Borrowers who test those numbers before applying waste less time and give themselves a better chance to negotiate structure instead of reacting to lender conditions.

What lenders are measuring

For commercial cash-out refinances in 2026, lenders typically cap LTV between 65% and 75% and require DSCR of 1.20x to 1.35x, according to Axiant Partners' commercial refinance guidance. In practice, that means one limit comes from value and the other comes from income. The lower result usually decides the loan amount.

Owner-occupied borrowers should look at those metrics through an SBA lens, not just a conventional one. Conventional lenders often focus heavily on property cash flow and tighter equity standards. SBA lenders still care about repayment, but they can be more flexible for operating businesses that occupy the property, especially when a refinance improves payment pressure or consolidates business debt into a structure the company can carry.

DSCR is where many deals tighten up. A property or business can look strong until the proposed payment is underwritten at the lender's rate, term, and stress assumptions. Borrowers who want a clearer picture of the calculation should review this guide on what DSCR means for SBA approval. For a broader explanation of payment coverage, this explainer on navigating business funding is also useful.

A few practical takeaways matter here:

- LTV sets the upper boundary. If appraisal value drops, proceeds drop with it.

- DSCR sets the supportable payment. If income is thin, the lender may cut loan size even when equity is strong.

- Liquidity still matters. A borrower who empties operating cash to close a refinance can create a new problem right after solving the old one.

- Global cash flow can matter more than property-level income in SBA deals. That is a major reason SBA can outperform conventional financing for owner-users.

What the Transaction Costs

Closing costs change the net benefit of a refinance, especially in cash-out requests where every dollar of proceeds already has a job. I tell borrowers to underwrite the full transaction, not just the interest rate.

One line item that gets underestimated is the appraisal. A new commercial appraisal is commonly required, and Axiant notes a typical range of $3,000 to $10,000 for that report. Add title charges, legal fees, filing costs, and lender closing expenses, and the out-of-pocket number can move fast.

SBA refinances also need a harder look at use of proceeds. If the file only works because value comes in at the top end, closing costs stay lighter than expected, and cash flow gets treated generously, the structure is too thin.

Use this screen before you sign an application:

- Model cash left after closing. Low reserves can hurt operations even if the payment improves.

- Use trailing results, not optimistic projections. Underwriters credit documented performance.

- Match the structure to the objective. A payment-relief refinance should be underwritten differently from a cash-out transaction.

- Check whether SBA reduces your cash requirement. For many owner-occupied properties, that is where the program has a clear edge over conventional debt.

The best refinance offers enough savings or enough strategic benefit to justify the fees, while still leaving the business with room to operate.

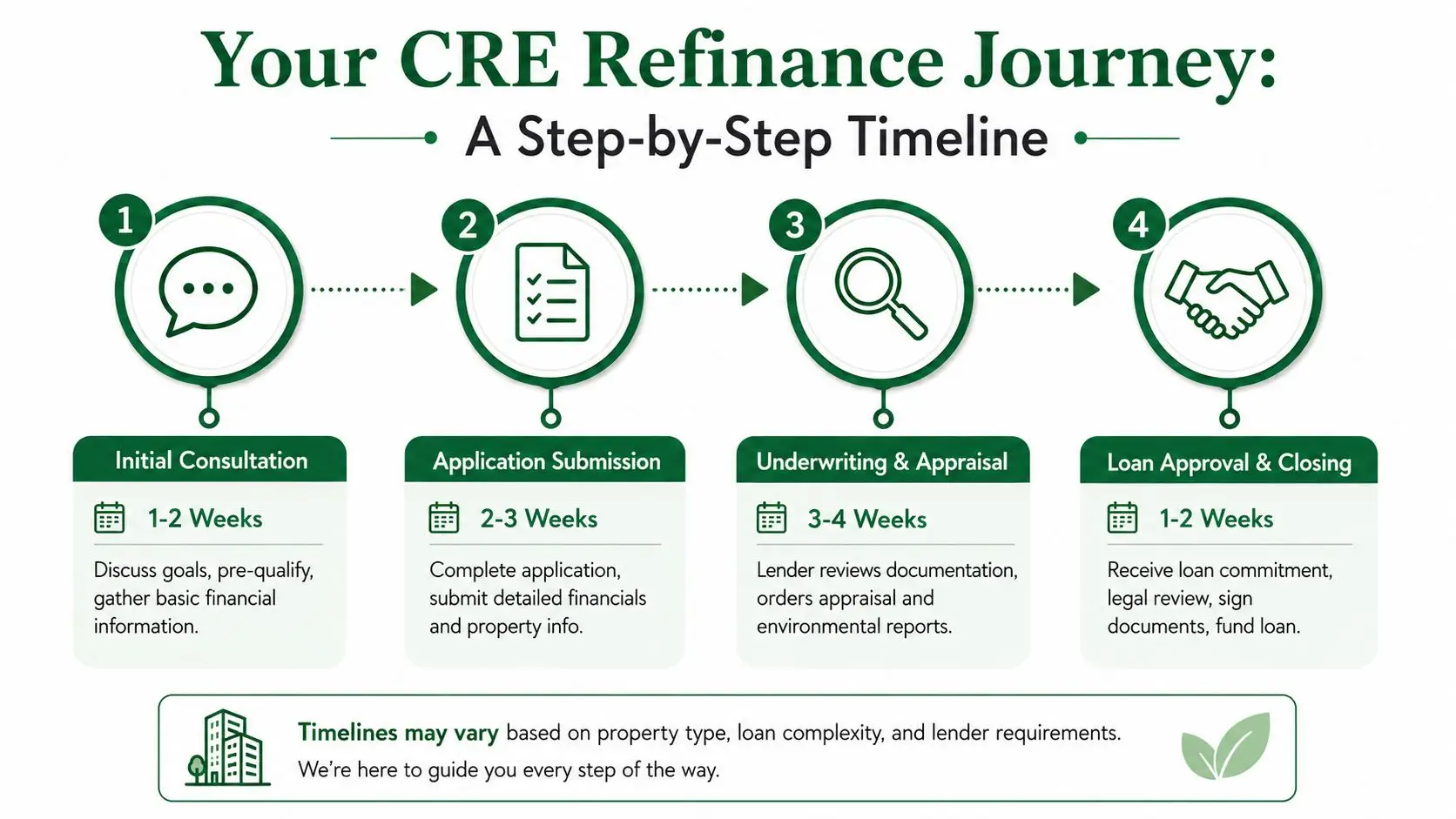

Your CRE Refinance Timeline and Checklist

Most refinance delays aren't caused by one big issue. They're caused by small missing pieces. A stale rent roll, unclear payoff statement, entity documents that don't match, or a borrower who learns too late that a required appraisal must meet a specific standard.

Phase one and two

Start with lender fit, not with a full application blast. The first job is matching the deal to the right lane. A conventional bank, a bridge lender, and an SBA lender will ask different questions because they are solving different problems.

Then build a clean package. That means current business financials, property operating information, debt statements, ownership documents, and a clear written explanation of why the refinance is being requested.

The process is easier when you think in stages:

- Initial review

Confirm your goal, property use, current loan type, and any timing pressure tied to maturity or prepayment. - Lender matching

Choose lenders based on structure fit, not familiarity. - Application package

Submit complete financial and property documents in one organized batch when possible.

For borrowers who want a realistic view of timing expectations, this guide on how long an SBA loan can take helps set expectations around the approval and closing sequence.

Phase three and four

Once the file reaches underwriting, third-party reports become critical. At this juncture, many borrowers discover that “an appraisal” isn't generic enough for the loan they're seeking.

For SBA 7(a) loans used to refinance commercial real estate, lenders must obtain a USPAP appraisal by a state-licensed or certified appraiser, and the appraisal must be dated within 12 months of the guaranty application as a mandatory condition for funding, according to Starfield & Smith's summary of SOP 50 10 7 appraisal requirements.

That means you should treat appraisal ordering as a gating item, not as an administrative detail.

Order the right third-party reports for the right loan program. Reusing an old report often creates more delay than ordering the correct one at the start.

A practical closing checklist looks like this:

- Payoff verification: Confirm the exact payoff, timing, and any lender conditions tied to release.

- Entity review: Make sure ownership documents, leases, and borrowing resolutions are current and consistent.

- Insurance and title coordination: These items often become last-minute bottlenecks if no one owns them early.

- Cash to close analysis: Review final sources and uses before signing, especially if the structure changed during underwriting.

A refinance moves fastest when the borrower treats it like a transaction, not a renewal.

Maximizing Your Refinance Success

A commercial real estate refinance is rarely just about replacing one note with another. Done well, it improves debt structure, protects operating cash, and gives the business more room to grow. For owner-occupied properties, SBA financing often stands out because it can offer stronger borrowing power and longer terms than conventional alternatives, but only when the deal fits the program rules.

The best results come from getting clear on the goal early, choosing the right loan type, and testing eligibility before spending money on the process.

If you want help structuring an owner-occupied commercial real estate refinance, GoSBA Loans can help you compare SBA options, manage SOP-driven eligibility issues, and line up the lender fit that minimizes cash outlay while improving approval odds.