You're probably looking at a deal right now and asking the only question that matters at this stage: how much down payment is needed to get this closed without draining your operating cash.

Most borrowers start with the wrong math. They assume there's a single percentage, they multiply it by the purchase price, and they call that the answer. That shortcut creates problems late in underwriting, especially in SBA deals where lenders care about the full capital structure, not just the buyer's wire amount on closing day.

The better question is this: what total equity injection does the lender require, and how much of that must come from your cash? Those are not always the same number.

That distinction matters whether you're buying an existing business, opening a startup, adding a new location, or financing owner-occupied commercial real estate. In some deals, cash to close is straightforward. In others, seller financing, collateral strength, and transaction structure can materially change what you need to bring in personally.

Table of Contents

- The Real Answer to Your Down Payment Question

- Down Payment vs Equity Injection A Critical Distinction

- Down Payment Requirements by Loan Type

- Sample Scenarios and Calculations

- Strategies to Minimize Your Cash to Close

- Your Next Steps and Documentation Checklist

- How GoSBA Loans Reduces Your Cash Outlay

The Real Answer to Your Down Payment Question

If you want the short answer, here it is. There isn't one universal SBA down payment number. The requirement depends on the use of proceeds, the risk in the deal, and how the transaction is structured.

For SBA 7(a) loans, acquisitions of existing businesses typically require 10% to 20% equity injection, while startups or new locations often land in the 15% to 25% range because lenders view unproven cash flow as higher risk, according to Port 51's breakdown of SBA 7(a) down payment requirements. That same source notes that businesses with less than two years of history may need up to 30% down.

That's the headline. The part that helps you plan is this: lenders are underwriting equity injection, not just a down payment line item. Cash is one component. Deal structure is another. Seller participation can matter. So can collateral and operating history.

Practical rule: Stop asking only, “What percentage down?” Start asking, “What counts toward equity, what must be cash, and what will the lender accept?”

A borrower who understands the capital stack usually negotiates a better purchase structure. A borrower who only focuses on a raw percentage often shows up at closing short on liquidity.

What usually works

Strong deals usually share three traits:

- Clear historical cash flow: Lenders get more comfortable when repayment isn't hypothetical.

- Reasonable total project costs: The cleaner the budget, the fewer surprises late in underwriting.

- Thoughtful structure: Seller notes, reserve planning, and documented liquidity often make the difference.

What usually does not

Borrowers run into trouble when they:

- Calculate only from purchase price

- Ignore closing costs and reserves

- Assume every lender interprets flexibility the same way

That's why the answer to how much down payment is needed starts with the whole transaction, not one percentage pulled from a checklist.

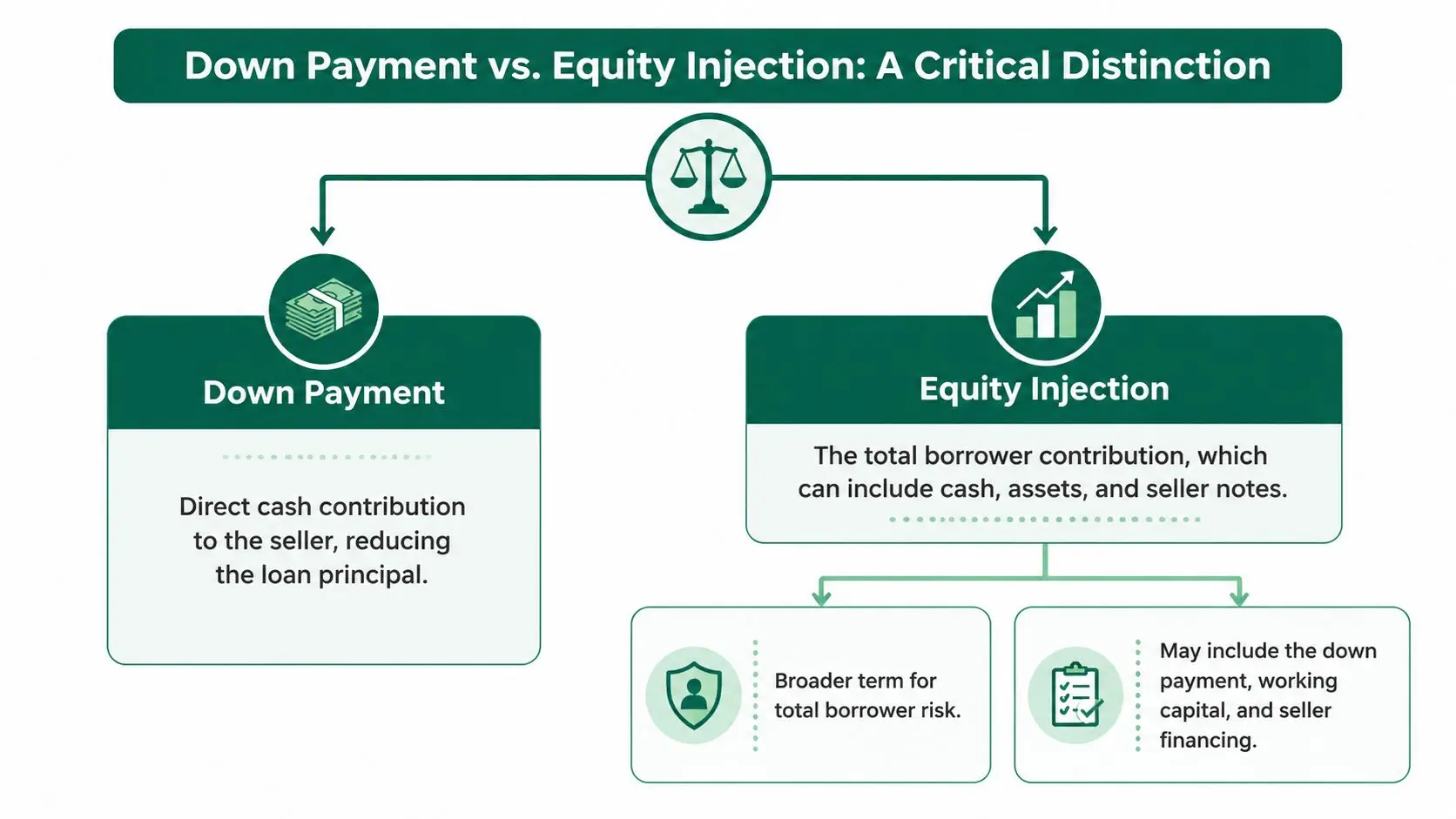

Down Payment vs Equity Injection A Critical Distinction

Most confusion starts because people use down payment and equity injection as if they mean the same thing. They don't.

A down payment is the cash you bring into the transaction. Equity injection is the broader lender requirement. It measures how much real borrower-side contribution exists in the deal and how much risk the borrower is taking alongside the lender.

Why this distinction changes your math

In real underwriting, lenders don't look only at the business purchase price. They look at the total project cost. That can include the acquisition price, closing expenses, working capital built into the transaction, equipment, and renovation or improvement budgets.

Imagine building a house. You don't budget only for the land. You also budget for permits, materials, labor, and everything else required to finish the job. SBA equity works the same way. If your project cost is larger than the base purchase amount, your required contribution is larger too.

That's why many buyers underestimate their need.

According to CDC Small Business Finance's explanation of SBA startup down payment calculations, most borrowers mistakenly calculate their down payment against the loan amount, but the SBA requires the equity injection to be based on the TOTAL PROJECT COST, which includes closing fees, working capital, and renovations. On a $750,000 project with $100,000 in other costs, the 10% requirement is $85,000, not $75,000.

What lenders are actually testing

The equity injection requirement is really a risk test. A lender wants to know:

- Will the borrower stay committed if the first year is uneven

- Does the borrower have enough liquidity left after closing

- Is the project budget complete, or are there hidden funding gaps

A buyer who empties every account to satisfy a nominal down payment can still look weak if post-closing liquidity disappears. On the other hand, a borrower who structures the deal intelligently may look stronger even with less cash out of pocket.

A thin cash contribution doesn't always kill a deal. An incomplete capital plan often does.

The mistake that causes late-stage problems

The most common failure point is simple. The borrower gets comfortable with one number early, then underwriting rebuilds the project budget and the required injection rises.

That's why experienced borrowers map the capital stack before they sign final loan terms. They identify purchase price, fees, reserves, and any non-cash support early. If you don't do that work up front, you end up negotiating under pressure when the closing clock is already running.

Down Payment Requirements by Loan Type

Different loan categories treat equity differently. Some borrowers expect one universal standard and get frustrated when one lender asks for more than another. That usually happens because they're comparing unlike transactions.

For SBA 7(a), the clearest hard rule in acquisition lending is this: for business acquisition loans over $500,000, the SBA mandates a minimum 10% equity injection. At the same time, startups or businesses with less than two years of history often require 15% to 25%, while loans under $350,000 may have no SBA-mandated minimum down payment at all, as summarized in LendingTree's overview of SBA business loan down payment rules.

Typical down payment by loan type 2026

| Loan Type | Typical Down Payment Range | Primary Use Case |

|---|---|---|

| SBA 7(a) business acquisition | 10% minimum on qualifying acquisition deals over $500,000 | Buying an existing business |

| SBA 7(a) startup or new location | 15% to 25% is often required by lenders | Startups, expansions, new units |

| SBA 7(a) working capital or equipment | 0% to 5% may be possible with strong collateral and robust cash flow | Working capital, equipment financing |

| SBA 504 | Varies by project structure and risk | Owner-occupied commercial real estate |

| Conventional commercial loan | Varies by lender, property, and borrower strength | Real estate, business-purpose financing |

| Specialized acquisition structures | Depends heavily on seller note and underwriting support | Leveraged business acquisitions |

SBA 7(a) is flexible, but not loose

The SBA SOP is the main source of truth, and in practice the rule set is narrower than many online summaries suggest. Lenders still have room to interpret risk. That's why two institutions can look at the same deal and land in different places on required liquidity, reserves, and acceptable sources of injection.

For acquisitions, one important rule from the market is stable. A lender wants to see real borrower commitment and a structure that leaves the business with enough operating cushion after closing. That's why a buyer with a good balance sheet but no reserve planning may still lose ground in underwriting.

If you want a broader operating overview of program rules, eligible uses, and qualification standards, review this SBA 7(a) guide for 2026.

Where borrowers get tripped up

Three patterns come up repeatedly:

- Existing business purchase: Buyers hear “10% down” and assume that ends the analysis. It doesn't. The lender still evaluates total structure, source of funds, and post-close liquidity.

- Startup financing: Borrowers underestimate how much operating history matters. If there's no proven repayment track record, lenders usually want more borrower equity.

- Working capital and equipment: Some deals can be structured with very limited cash in, but only when the file is otherwise strong. Good collateral and strong projected repayment matter.

Key takeaway: The requirement isn't just about loan type. It's about what you're buying, how proven the cash flow is, and how the deal is assembled.

What to expect in real conversations with lenders

If you ask ten lenders, “How much down payment is needed?” you may get a short answer that sounds clean. Don't stop there. Ask follow-up questions:

- Is the requirement based on purchase price or full project cost?

- Does any part of seller financing count?

- Will reserves be required outside the stated injection?

- Is the lender treating this as acquisition, startup, or expansion risk?

Those questions usually reveal the actual answer much faster than the headline percentage.

Sample Scenarios and Calculations

Here's where the structure becomes tangible. Assume you're buying a business for $2,000,000 and the lender requires a 10% equity injection. There are two very different ways that can look at closing.

Scenario one with full buyer cash

In the plain-vanilla version, the buyer contributes the full 10% in cash.

That means the buyer brings $200,000 to satisfy the injection requirement, and the SBA loan finances the rest of the transaction. This structure is simple. It's also the version that puts the most pressure on the buyer's liquidity.

The problem isn't just the wire amount. It's what happens after closing. If that cash represented most of the buyer's available liquidity, the business may open undercapitalized from day one.

Scenario two with a seller note on standby

Now take the same $2,000,000 acquisition and split the required 10% injection into 5% buyer cash and 5% seller note on full standby.

That means the buyer contributes $100,000 in cash and the seller carries $100,000 in a standby note that supports the required equity. Cash to close drops materially even though the total required injection remains the same.

If you want a deeper look at how these structures work in practice, this guide on seller notes in SBA business acquisitions is worth reviewing.

Side by side comparison

| Structure | Buyer Cash | Seller Note on Standby | Total Equity Injection |

|---|---|---|---|

| Standard cash injection | $200,000 | $0 | $200,000 |

| Split injection structure | $100,000 | $100,000 | $200,000 |

That's why buyers who ask only how much down payment is needed often miss the better question. The actual issue is how much of the required equity must come from your own liquid cash.

A short explainer helps here:

What this example actually teaches

This isn't magic. It's structure.

The lender still wants a properly supported deal. The seller note has to be documented correctly. The business still needs debt service coverage, and the buyer still needs enough liquidity to operate after closing. But when the file is strong, reducing buyer cash from $200,000 to $100,000 can be the difference between a strained acquisition and a healthy one.

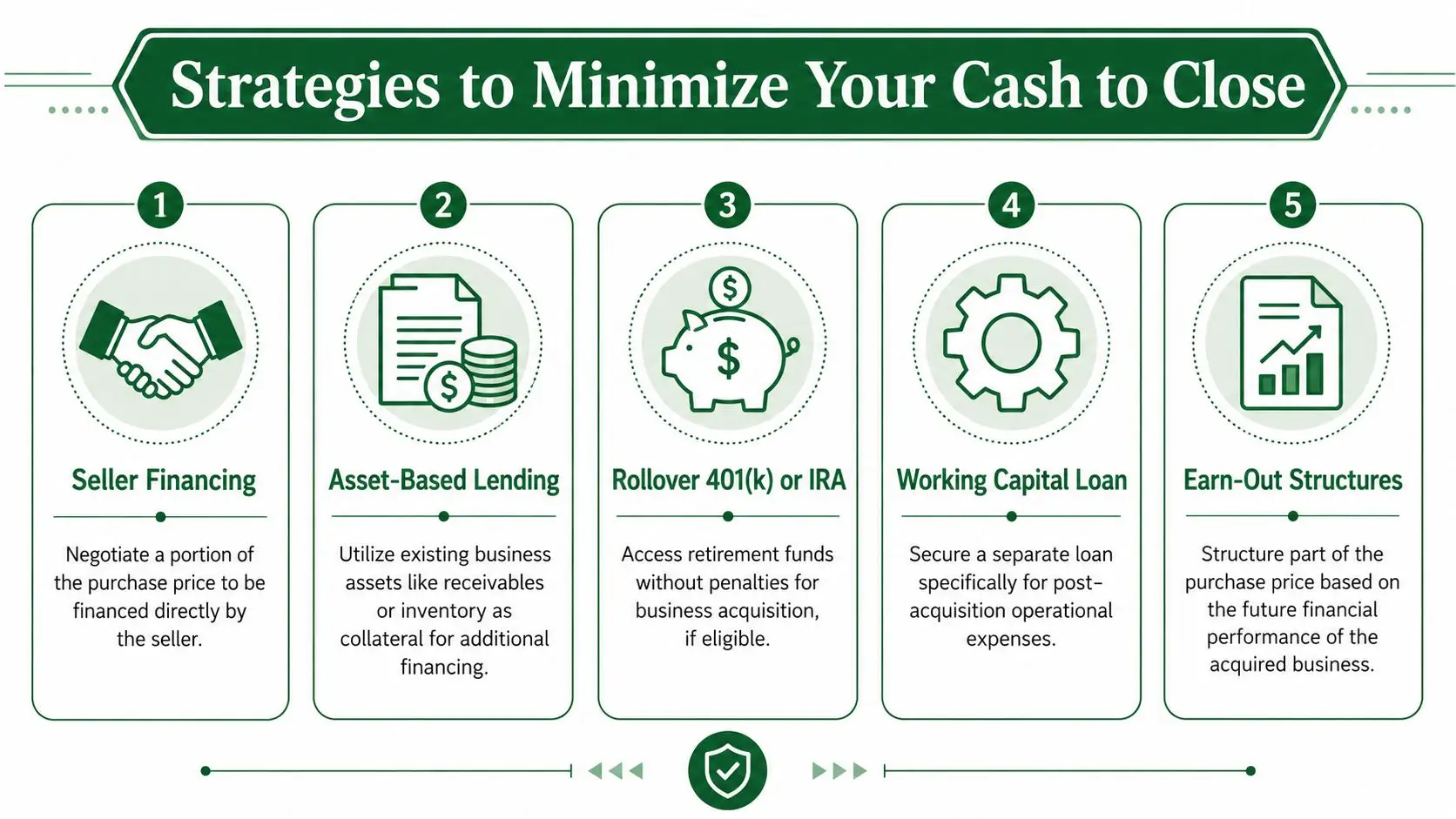

Strategies to Minimize Your Cash to Close

The strongest SBA structures don't try to eliminate borrower commitment. They try to preserve liquidity while still satisfying the lender's equity requirement.

The cleanest tool for that is seller financing. According to Bay Street Lending's explanation of SBA loan requirements, the SBA permits up to 50% of the required 10% equity injection to come from a seller note on full standby, meaning no payments are made on that note for the entire term of the SBA loan. This structure is what enables the popular 5% down payment strategy for business acquisitions.

Start with the seller note

A standby seller note works because it aligns incentives. The seller keeps some exposure in the business. The lender sees support behind the valuation. The buyer preserves working capital.

What matters is the phrase full standby. In plain English, that means no payments on that seller note for the life of the SBA loan. If the note requires payments too early, many lenders won't count it toward required equity in the same way.

Often, deals go sideways. The buyer says there's seller financing, but the note terms don't satisfy standby treatment. The concept is right. The documentation is wrong.

Seller notes save cash only when they're structured to fit SBA rules and lender credit standards.

Add other legitimate equity sources carefully

Seller financing isn't the only tool in the capital stack. Depending on the transaction, borrowers may also layer in:

- Investor capital: Outside investors can reduce the direct cash burden on the operating buyer, but ownership structure and guaranty expectations need to be handled correctly.

- Subordinated debt: Junior capital can support the transaction if the lender accepts the terms and subordination.

- Gifted funds or personal transfers: These can work in some files if the source is clear, documented, and acceptable to the lender.

None of these options fixes a weak acquisition. They help support a strong one.

Preserve liquidity for day-two operations

Borrowers sometimes push so hard to lower the down payment that they ignore the bigger objective. You don't win by closing a deal with minimal cash if the business starts life starved for working capital.

That's why operational planning matters as much as deal structure. Good cash discipline after closing is often what protects the transaction from early stress. If you want a useful operational framework, HireAccountants' cash flow insights offer practical ways to think about reserve management and day-to-day liquidity.

You should also model non-purchase expenses early. Fees, reports, legal costs, and lender-related charges can change the true cash requirement long before closing. A helpful primer is this breakdown of SBA loan closing costs and fees.

What works best in practice

The most reliable cash-saving structures usually share a few traits:

- The seller is cooperative. Standby financing requires negotiation, not assumption.

- The buyer has some liquidity left. Lenders prefer preserved operating cash over a heroic last-dollar injection.

- The sources of funds are clean. If the paper trail is messy, underwriting slows down fast.

- The valuation is supportable. Creative structure won't rescue an overpriced deal.

The right strategy isn't always the one with the lowest buyer cash. It's the one that gets approved, closes cleanly, and leaves the business in a position to perform.

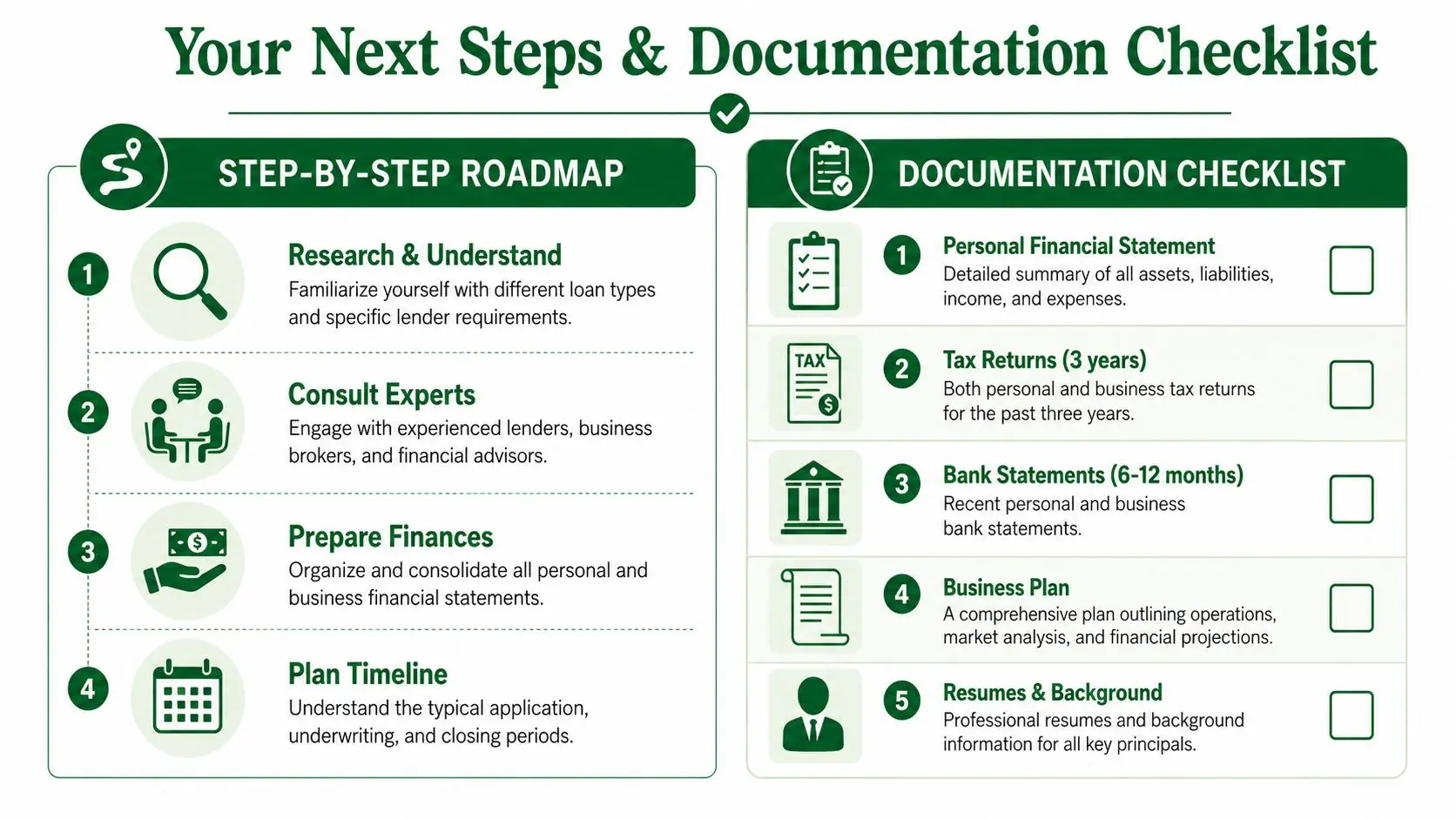

Your Next Steps and Documentation Checklist

Once you understand the equity rules, the next job is getting lender-ready. Good borrowers don't wait for underwriting questions to assemble their file. They build the package early so a lender can issue a term sheet without chasing missing pieces.

A realistic path looks like this: first conversation, preliminary screening, lender matching, term sheet, full underwriting, then closing. Some files move smoothly. Others stall because basic documentation is incomplete or the source of funds isn't clear.

The documents lenders usually want first

Start with the core items below. If you have these organized, the lender can usually assess your file much faster.

- Personal financial statement: A current snapshot of assets, liabilities, income, and contingent obligations.

- Tax returns: Personal returns and business returns, if applicable.

- Bank statements: Lenders want to verify liquidity and source of funds.

- Resume or experience summary: This matters more than many first-time buyers expect, especially in acquisition lending.

- Business details: Purchase terms, business summary, and current financials from the target company if you're buying an existing business.

The documents that often decide speed

These items don't always get discussed first, but they frequently control timeline:

- Source of equity documentation: If funds come from savings, a transfer, a gift, or another approved source, document that early.

- Organizational documents: Entity paperwork, ownership breakdown, and any investor information.

- Transaction support: Letter of intent, purchase agreement, rent roll or real estate details when relevant, and explanation of any seller financing.

- Projections and assumptions: Lenders want to see how the business performs after debt service, not just before it.

Underwriting reality: The cleaner your file, the easier it is for a lender to focus on the opportunity instead of the missing paperwork.

A practical borrower checklist

Before you submit anything, confirm four things:

- Your equity source is documented and traceable.

- Your budget includes more than the headline purchase number.

- Your operating experience is clearly presented.

- Your post-close liquidity still makes sense.

Borrowers who do that work upfront usually get more useful lender feedback and fewer unpleasant surprises later. If you're serious about terms, preparation is what turns a rough conversation into an actual offer.

How GoSBA Loans Reduces Your Cash Outlay

A buyer can know the SBA equity injection rules and still bring too much cash to closing.

The difference usually comes down to structure. On many deals, the primary question is not just, "What down payment does the lender want?" It is, "What counts toward equity injection, and how much of that has to be the buyer's cash?" That is where good SBA packaging changes the outcome, especially if the deal can support a properly documented seller note on full standby.

GoSBA Loans works as a full-service, no-cost SBA loan brokerage for business acquisitions, working capital, and owner-occupied commercial real estate. The firm works with a large network of SBA lenders and helps borrowers pursue structures that may include standby seller notes, outside investors, and smaller SBA loans with a faster process. That matters because not every lender reads the same file the same way. One bank may ask for a straight 10 percent buyer injection. Another may give credit for a seller standby note that lowers the buyer's cash required at closing.

That difference is real money.

A well-structured file can reduce the buyer's cash outlay while still meeting SBA rules and lender policy. In practice, that means clarifying whether the transaction is a startup, whether there is a change of ownership with a 10 percent or 15 percent injection requirement, whether seller financing can count toward equity injection, and how the full capital stack should be presented before underwriting starts forming its view of the deal.

GoSBA Loans helps on the parts that usually decide terms. Lender matching, equity injection positioning, coordination with the seller note terms, packaging of investor contributions, and support through closing all affect whether a borrower preserves liquidity or burns cash unnecessarily.

That liquidity matters after closing. Buyers need cash for payroll, inventory, repairs, slow receivables, and the problems that show up in the first few months of ownership.

If you're trying to figure out how much down payment is needed for your deal, and how to reduce your actual cash to close, GoSBA Loans can help you structure the transaction, compare lenders, and present the strongest possible SBA file.