You've found a business that fits. The cash flow looks solid. The seller wants to move forward. Your lender is open to an SBA acquisition loan.

Then the deal hits the wall most first-time buyers run into. You can afford the business, but you don't want to drain your liquidity at closing just to satisfy the equity injection.

That's where seller notes become more than a financing add-on. In seller notes in SBA business acquisitions, the note often decides whether a deal is merely attractive or becomes fundable. Used correctly, it can reduce cash required at closing, help the lender get comfortable with the structure, and solve underwriting issues that have nothing to do with the headline purchase price.

Table of Contents

- The Secret to Buying a Business with Less Cash Down

- What Is a Seller Note in an SBA Context

- The Full Standby Rule Explained

- Structuring the 5 Percent Down Acquisition

- How to Negotiate a Seller Note

- Advanced Strategies for Using Seller Notes

- Lender Requirements and Common Deal-Killing Mistakes

The Secret to Buying a Business with Less Cash Down

A first-time buyer gets a deal under LOI, lines up the SBA loan, and realizes the core problem is not approval. It is getting to closing without draining every dollar of personal liquidity.

That is where seller notes earn their place in the structure.

Used properly, a seller note does more than reduce the buyer's cash injection. It can solve specific underwriting problems that otherwise stall the deal. I see seller notes used to preserve buyer liquidity, support debt service coverage, bridge a gap between price and lender comfort on value, and offset weak collateral support. The basic 5 percent buyer injection structure gets the attention, but its true value is strategic. A well-documented seller note can make a marginal deal bankable.

In many SBA 7(a) acquisitions, the capital stack includes senior SBA debt, buyer equity, and a seller note. Under current SBA guidance, that note may allow the buyer to bring less cash to closing if it is structured correctly. This overview of seller financing for business acquisition explains the standard framework, but the practical question is simpler. Does the note make the deal safer for the lender, or just easier for the buyer?

That distinction matters.

A buyer who puts every available dollar into closing often leaves no room for the first six months of ownership. Payroll still hits. Inventory still has to be purchased. Customers pay late. Equipment breaks. The seller's historical numbers may hold up, but transition costs show up fast and usually in cash.

Why this matters to a first-time buyer

Lower cash down is useful. Preserved liquidity is often more important.

Cash left outside the deal can cover:

- Transition costs: Training overlap, professional fees, and early process fixes

- Working capital pressure: Payroll, inventory, rent, and uneven receivables

- Operational surprises: Repairs, customer concentration issues, or slower-than-expected handoff

- Underwriting friction: Cases where the lender wants more support in the structure before issuing final approval

The strongest seller-note structures do two jobs at once. They reduce the buyer's closing burden and improve the lender's view of the transaction. If a deal has tight coverage, an aggressive valuation, or limited collateral, seller paper can help address the weakness if the terms fit SBA rules and lender credit policy.

Many buyers hear “seller financing” and assume any note will work. It will not. In SBA deals, the note has to be set up in a way the lender can underwrite and the SBA will accept. If it is drafted loosely, requires payment too early, or conflicts with the senior lender's position, it can hurt approval instead of helping it.

What Is a Seller Note in an SBA Context

A first-time buyer often hears “seller note” and assumes it replaces cash at closing. In an SBA acquisition, that is too narrow. A seller note is deferred purchase price that can also help solve a weakness in the credit file, if the terms line up with SBA rules and the lender's underwriting approach.

At the document level, it is straightforward. The buyer signs a promissory note to the seller for part of the purchase price, and the seller agrees to collect that amount later instead of taking all proceeds at closing. What changes in an SBA deal is how that note gets treated. The bank underwrites it. The SBA rules affect it. The note can help the deal, hurt the deal, or sit in the file with little credit benefit, depending on how it is structured.

Where the seller note fits

The capital stack usually has three parts:

| Capital Source | Role in the deal |

|---|---|

| SBA loan | Senior debt funding most of the purchase |

| Buyer equity | Cash injected by the buyer |

| Seller note | Deferred purchase price that may support the structure if it meets lender and SBA requirements |

In many SBA 7(a) acquisition structures, the lender expects a buyer equity injection and may allow a properly structured seller note to satisfy part of that requirement. More important, the note can address issues that have nothing to do with the buyer's cash contribution.

That is the part many buyers miss.

A seller note can improve debt service coverage by reducing or deferring current payment burden. It can help close a valuation gap when the bank will not lend against the full agreed price. It can also support a deal with limited collateral by showing the seller is still financially tied to post-closing performance. None of those benefits happen automatically. The note has to be written in a way the lender can approve.

What lenders are really looking at

Lenders do not view seller paper as a generic sign of goodwill. They look at what problem it solves and whether it creates a new risk.

If projected DSCR is tight, a note with no current payment can preserve cash flow for the senior loan. If the appraisal or lender valuation comes in below the purchase price, the seller note may absorb part of the gap instead of forcing the buyer to bring in more cash. If collateral coverage is thin, seller financing can strengthen the story because the seller is leaving money in the business rather than cashing out completely on day one.

Those are practical underwriting uses. They matter more than the generic talking point that seller financing “shows confidence.”

What it is and what it is not

A seller note is still debt. The seller is taking repayment risk, and the buyer is agreeing to pay part of the price over time. Whether that note counts toward the required injection depends on its terms, not on what the parties call it in the LOI.

That distinction matters in real deals. I see buyers assume any carryback note gets them to a lower cash close, then find out late that the bank treats it as additional debt instead of equity support. At that point, the buyer either adds cash, renegotiates terms, or loses time rewriting documents.

The practical takeaway is simple. In an SBA acquisition, a seller note is a structuring tool. Used well, it helps the lender get comfortable with coverage, valuation, or collateral. Used poorly, it becomes one more issue the credit team has to fix before approval.

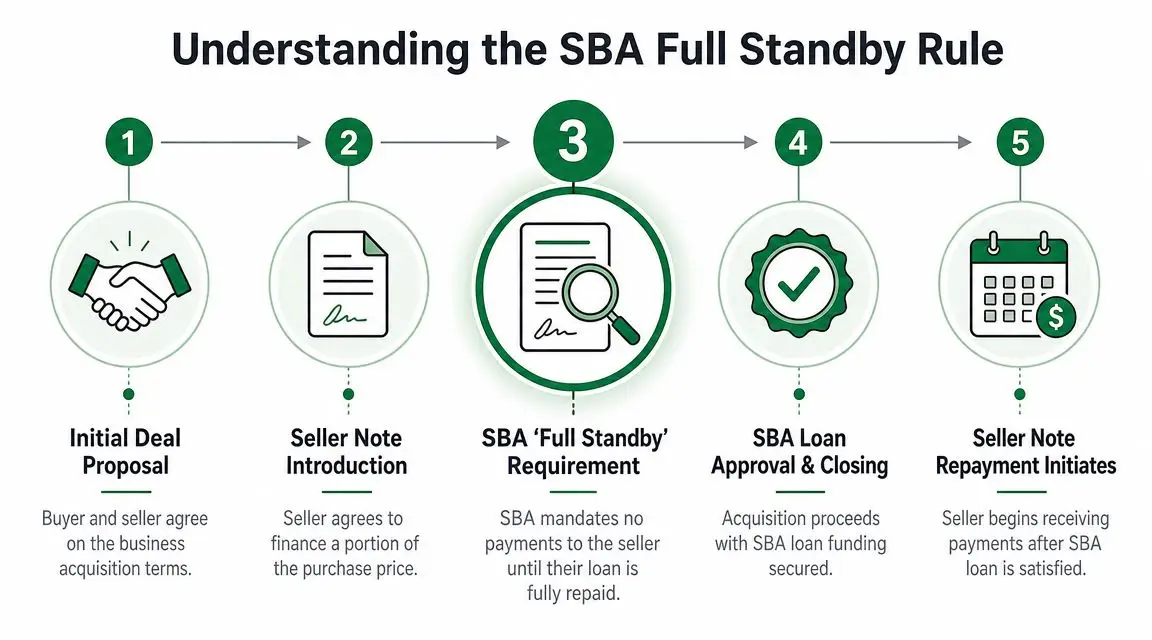

The Full Standby Rule Explained

The phrase that matters most in this topic is full standby. If you don't understand it early, you can negotiate the wrong note, draft the wrong LOI, and waste weeks fixing documents.

A seller note used to satisfy part of a buyer's required equity injection is typically subject to a full standby structure, meaning no principal or interest payments can be made while the SBA loan is outstanding, and the note must be subordinated to the SBA lender, as described by Always Bank's guidance on seller notes in business acquisitions.

Why lenders care about standby

From the lender's perspective, this is simple. If the seller gets paid too soon, the buyer's cash flow gets stretched, and the bank's loan takes more risk.

A lender underwriting an SBA acquisition wants the business cash flow focused on the senior debt first. If the seller note is being treated as part of the injection, the lender does not want that note behaving like a second live payment burden right after closing.

Subordination matters for the same reason. The SBA lender wants senior repayment priority. The seller can still have a note, but not one that competes with the bank's position.

The easiest way to explain full standby to a seller is this. The bank will fund the deal only if the seller agrees to wait behind the SBA loan for repayment.

What full standby means in practice

In practical deal terms, full standby means:

- No monthly payments to the seller: Not principal. Not interest.

- No side promises outside the note: Buyers sometimes try to offset standby with consulting payments that function like disguised debt service. Lenders notice.

- Subordination documents must be clear: If the language is sloppy, underwriting will push back.

The operational effect is important. A note on full standby can improve early cash flow because the business isn't servicing the seller debt while the SBA loan is outstanding. That can make the deal easier to underwrite than a structure where the seller note requires current payments.

Later in the process, this video gives a useful visual explanation of how these structures are commonly discussed in the SBA market.

For buyers, the practical lesson is clear. Don't negotiate seller note economics in isolation. Before the note amount, rate, or term becomes final, confirm whether the note needs to count toward injection. If it does, standby and subordination aren't optional drafting details. They are the core of the structure.

Structuring the 5 Percent Down Acquisition

The cleanest way to understand seller notes is to compare two versions of the same transaction.

A simple side-by-side example

A seller note that is counted toward the equity injection is generally capped at 50% of the required injection. In a standard acquisition, that means a buyer may satisfy a 10% injection with roughly 5% cash and 5% seller note, according to Financely Group's guidance on seller notes for SBA 7(a) acquisitions.

Using the article's required example of a $2M acquisition, the structure looks like this:

Deal Structure Comparison: $2M Acquisition

| Source of Funds | 10% Down Structure | 5% Down with Seller Note |

|---|---|---|

| Buyer cash | $200,000 | $100,000 |

| Seller note | $0 | $100,000 |

| SBA loan | $1,800,000 | $1,800,000 |

The most important line in that table is the buyer cash line. The seller note reduces the buyer's upfront cash outlay by $100,000.

What changes for the buyer

That saved cash can matter more than the headline price. It can stay in reserve for payroll, inventory, repairs, integration costs, or a working capital cushion. In practice, that's often what makes the buyer comfortable enough to proceed.

But there's a catch. The savings only help if the seller note is structured correctly and approved by the lender as part of the injection. If the note is drafted in a way that doesn't qualify, the buyer may still need to bring the full cash injection.

Here's how I explain the difference to buyers:

- A 10% cash structure is simpler on paper. The buyer writes the check and the lender sees the injection immediately.

- A 5% cash plus 5% seller note structure is more efficient, but it requires lender-compliant note terms.

- The wrong note structure creates the worst outcome. The buyer expects to bring less cash, underwriting rejects the note, and the deal has to be re-traded or recapitalized.

Buyers should never treat “5% down” as automatic. It's a possible structure, not an entitlement.

This is why seller notes in SBA business acquisitions are underwriting tools first and negotiation terms second. The note has to work inside the lender's framework. If it does, the reduced cash requirement is real. If it doesn't, the number in your model is fiction.

How to Negotiate a Seller Note

Most sellers don't object to a seller note because they hate the concept. They object because they don't want to feel like they're financing your weakness.

That's an avoidable mistake in how buyers frame the conversation. A well-negotiated seller note is usually presented as a deal-completion tool, not a plea for help. The business is financeable. The buyer is committed. The note helps the structure line up with lender requirements and preserves enough liquidity for a healthy transition.

What the seller is really worried about

Sellers usually focus on a few practical concerns:

- Repayment risk: They want to know what protects them if performance slips.

- Delay in receiving proceeds: Full standby can sound like dead money if it's poorly explained.

- Signal risk: Some sellers hear “I need a seller note” and assume the bank doesn't like the deal.

You address those concerns by being direct. Explain that SBA acquisition rules have evolved from older down payment norms of roughly 20% to 25% equity toward structures where the SBA can finance up to 90% of the deal, and that a seller note on full standby for 24 months can often be counted toward the buyer's equity, as summarized by SBA7a.loans in its review of seller notes.

That framing matters because it tells the seller this isn't an improvised workaround. It's part of a recognized acquisition structure.

Talking points that actually work

When a buyer asks for a seller note, the strongest talking points are usually these:

- You're helping the deal close: A seller note often expands the number of qualified buyers who can complete a transaction.

- You still get a committed buyer: A buyer putting in cash and signing for the acquisition still has meaningful skin in the game.

- The business benefits from preserved liquidity: A buyer who isn't overextended at closing is more likely to manage the transition well.

Then be honest about the trade-offs.

The seller is taking risk. The seller is waiting longer for some proceeds. And if the note must be on standby, the seller needs to understand that they won't receive payments during that period. Trying to soften or hide that point usually backfires later with counsel and underwriting.

A practical negotiation sequence works better than a hard ask:

- Start with purchase terms and broad structure.

- Confirm lender expectations before final papering.

- Explain why standby improves approval odds.

- Negotiate note economics after both sides accept the role of the note.

Sellers respond better when the note is presented as part of a financeable transaction, not as last-minute gap filling after the buyer runs short.

The best seller note negotiations feel collaborative. The seller keeps the deal alive. The buyer preserves liquidity. The lender gets a cleaner structure. That alignment is what gets deals to closing.

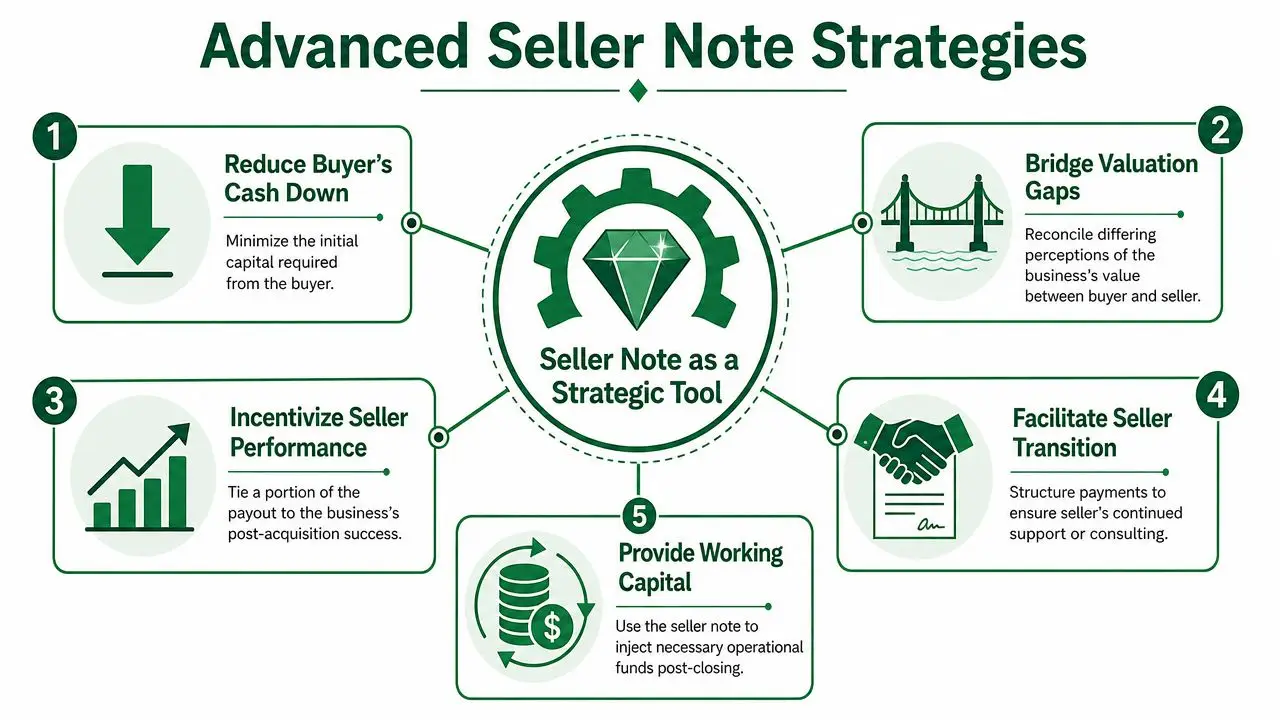

Advanced Strategies for Using Seller Notes

Most online explanations stop at one use case. Buyer brings less cash. Seller carries part of the injection. Done.

That's too narrow. In real underwriting, seller notes are often used to solve a different problem than buyer liquidity.

Lender guidance shows seller notes can be used differently depending on whether the deal is being resized for an appraisal shortfall, lack of collateral, or cash-flow constraints, which is why they function as more than a simple purchase-price bridge, as noted by Pioneer Capital Advisory's discussion of bridging the gap in SBA acquisitions.

When the issue is valuation not cash

A buyer and seller can agree on a price that the lender's valuation support doesn't fully back. When that happens, the seller note can help bridge the difference between seller expectations and what the lender is comfortable funding.

That doesn't make an inflated deal safe. It provides the parties with another lever. If the seller believes strongly in the business's future performance, carrying part of the price can keep the transaction together without forcing the buyer to overfund the gap in cash.

A similar logic applies to equity rollover structures. In some deals, part of the seller's economics stay in the business rather than being taken entirely off the table at closing. This overview of equity roll over structures is useful if you're comparing seller note dynamics with retained ownership mechanics.

When underwriting is tight

Seller notes can also affect how lenders view stress points in underwriting:

- DSCR pressure: If seller repayment is deferred, the business has fewer near-term obligations competing with the SBA loan.

- Collateral weakness: A seller who remains economically tied to the outcome may make a thin collateral story easier to present.

- Cash flow uncertainty: When a deal has transition risk, a seller note can show continued seller confidence.

Here's what doesn't work. Using a seller note to cover over a weak acquisition. If earnings are shaky, customer concentration is severe, or the post-close operator risk is obvious, the note won't rescue the file by itself.

The right use of a seller note is to solve a specific underwriting issue. The wrong use is to pretend it fixes all of them.

That's the distinction first-time buyers need to understand. Seller notes in SBA business acquisitions are best used like a precision tool. They work when matched to the actual problem the lender is trying to solve.

Lender Requirements and Common Deal-Killing Mistakes

The note itself doesn't kill most deals. Bad documentation does.

Lenders want to see the seller note structure early, not after the LOI, purchase agreement, and underwriting memo are already moving in different directions. If you're preparing for financing, it also helps to assess commercial credit scores before diligence gets deep, especially when trade history or business credit issues may influence how the lender views overall risk.

What your lender wants to see early

Get these points aligned as soon as possible:

- LOI language: State that seller financing is part of the proposed structure.

- Standby expectations: If the note is intended to support injection, make that clear early.

- Subordination terms: These shouldn't appear for the first time at closing.

- Clean sources and uses: The lender should be able to follow every dollar without guessing.

For a broader checklist, this guide to SBA loan requirements for buying a business is a useful reference point.

Mistakes that derail approval late

The most common problems are operational, not theoretical:

- Prohibited payment terms: If the note requires payments too early, the lender may disallow it as injection support.

- Missing or vague subordination language: Counsel then has to unwind terms late in the process.

- Side agreements that look like disguised debt service: Consulting or transition payments have to make business sense on their own.

- A seller asking for rights that conflict with lender priority: That usually triggers a hard stop.

The cleanest SBA acquisition files are boring. Everyone knows what the seller note is doing, when it gets paid, and where it sits in the repayment hierarchy. That's what you want.

If you're buying a business and want help structuring an SBA deal with the lowest realistic cash injection, GoSBA Loans can help you compare lender options, pressure-test a seller note structure, and get the transaction packaged correctly before underwriting turns into a fire drill.