You're probably reading this because your firm has hit a real inflection point. Maybe a partner is retiring and the buyout needs to happen on a business timeline, not a family-discussion timeline. Maybe you want to acquire a smaller practice, move into a better office, or stop using expensive short-term debt to cover uneven receivables. The legal work may be clear. The financing usually isn't.

That's where SBA lending gets misunderstood. Lawyers tend to approach it like any other commercial loan process, then run straight into issues that are specific to professional practices. Revenue caps get misread. Partner ownership rules matter more than people expect. Goodwill becomes a valuation fight. Buy-sell agreements that work fine internally can create problems in underwriting.

A good SBA structure can finance growth, ownership transition, working capital, or owner-occupied real estate with better terms than many conventional options. A bad structure wastes time, triggers avoidable lender objections, and can force a late-stage rewrite of the deal. The SBA SOP is the definitive rulebook, and if you're borrowing as a law firm, details matter.

Growth also doesn't happen from financing alone. If part of your plan is increasing intake and client retention after funding, this guide on law firm client newsletter strategy is a useful companion because it connects financing decisions to actual business development execution.

Table of Contents

- Financing Your Law Firm's Future Growth

- SBA Loan Eligibility for Law Firms

- Comparing SBA Loan Programs for Lawyers

- Real World Use Cases for Law Firm SBA Loans

- Navigating the Application and Underwriting Process

- Common Pitfalls and Underwriting Hurdles

- How to Improve Your Law Firm's Approval Odds

- Alternatives and Your Next Steps

Financing Your Law Firm's Future Growth

Law firm SBA loans work best when the firm has a clear business objective. “We want capital” is not enough. “We need to buy out a retiring equity partner, preserve working capital, and avoid disrupting compensation” is financeable because a lender can underwrite the use of proceeds and the repayment path.

For law firms, the strongest SBA requests usually fall into a few categories. Expansion into a larger office. Acquisition of another practice or a book of business. Partner transition. Refinance of debt that's pressuring monthly cash flow. Purchase of an owner-occupied building instead of continuing to lease. Each one requires a different story, and lenders can tell quickly whether the firm understands that.

Why lawyers often misread the process

A well-developed legal practice can still submit a weak loan package. That happens because attorneys often focus on the transaction documents while the lender focuses on repayment durability. The lender wants to see cash flow, management continuity, and a structure that complies with SBA rules. If the firm's story depends too heavily on future growth without showing operating discipline today, the file gets harder immediately.

Practical rule: The cleaner the purpose of the loan, the easier the underwriting.

The other issue is that legal practices aren't underwritten exactly like restaurants, contractors, or e-commerce businesses. A law firm may have partner compensation structures, contingent receivables, concentration in a few rainmakers, and a large share of value tied to goodwill. All of that can be financeable, but only if it's documented in a way an SBA lender can defend.

What works and what doesn't

Here's the practical split I see most often:

- What works: A firm with organized financials, a clear ownership chart, signed governing documents, and a specific use of proceeds tied to stable operations.

- What works: A partner buy-in or acquisition where management continuity is obvious and the post-closing structure is already thought through.

- What doesn't: Loose internal agreements, vague projections, or a purchase price that assumes goodwill but can't justify it.

- What doesn't: Treating underwriting questions like nuisances instead of the core of the approval decision.

A well-structured SBA loan is a strategic tool. A poorly prepared one becomes an avoidable due diligence exercise that drags on while the opportunity gets colder.

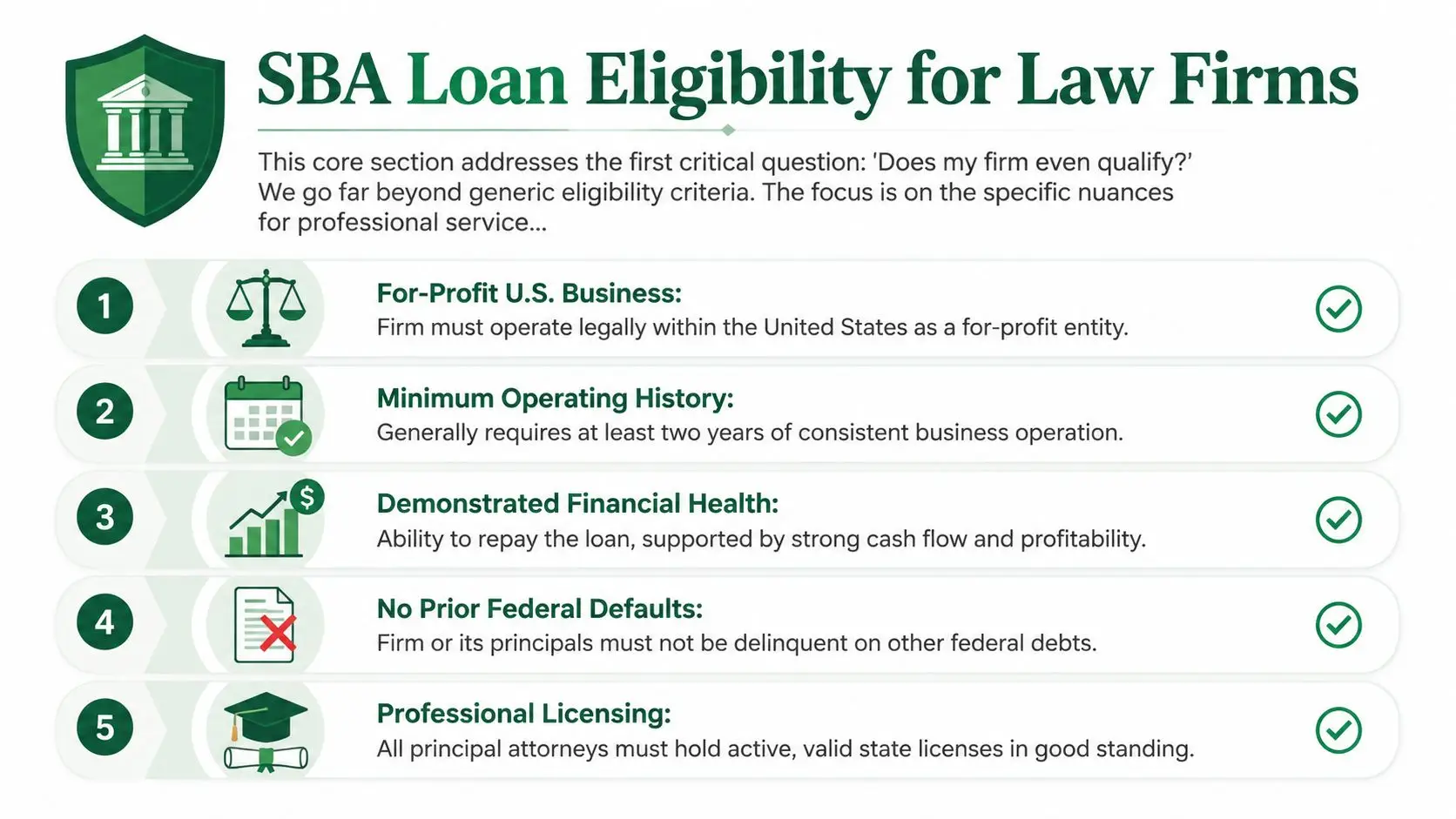

SBA Loan Eligibility for Law Firms

Eligibility is where a lot of law firm borrowers get surprised. They assume that because the firm is profitable, licensed, and for-profit, it should fit SBA rules. That's not always true.

The first screen is smaller than many firms expect

The most overlooked point is the size standard. For law firms, one critical issue is the revenue cap. A useful discussion of that nuance notes that law firms are considered “small” only if they are under $6.5M in annual revenue according to this law firm SBA eligibility discussion. That disqualifies some mid-sized firms that otherwise look like strong borrowers.

That one issue causes a lot of wasted effort. A partner may spend weeks gathering documents for a 7(a) request, only to learn the firm exceeds the applicable size standard. If your practice is near that line, you need to address eligibility first, before discussing structure, collateral, or timing.

The firm also needs to operate as a for-profit U.S. business. That sounds obvious, but lenders still verify legal entity status, where the business operates, and whether the firm's organizational documents align with the application. If your ownership structure has changed recently, expect questions.

Ownership, guarantees, and licensing issues

In professional practices, underwriting extends beyond the entity.

Lenders will review who owns the firm, who controls it, and who must stand behind the debt. In practice, that means the partnership agreement, shareholder agreement, or operating agreement matters early, not late. If those documents conflict with the proposed transaction, the lender may ask for amendments before issuing final approval.

A few issues show up repeatedly:

- Ownership thresholds: Any owner with a meaningful stake should expect scrutiny, especially if that person materially affects management or repayment strength.

- Personal support: SBA lending commonly involves personal guarantees in ownership groups, which means partner-level financial strength can matter even when the firm itself performs well.

- Professional credentials: Active licensing and good standing are not side notes for a law firm borrower. They're part of the lender's risk review.

- Federal debt history: Prior federal default issues can stop momentum fast.

If you want a practical overview of how lenders look at professional compliance, this guide to SBA loan licensing requirements is worth reviewing before you apply.

A law firm can be profitable and still be ineligible. Eligibility is not the same thing as credit quality.

The strongest approach is to treat eligibility like a gating legal issue. Confirm it first. Then build the financing request.

Comparing SBA Loan Programs for Lawyers

Not every SBA product fits a law firm the same way. Lawyers usually hear “SBA loan” and think of one category. In reality, the decision usually comes down to whether the need is operational flexibility, owner-occupied real estate, or a smaller credit request where speed matters.

How each program fits a legal practice

The SBA 7(a) loan is the most versatile option for a law firm. According to the official SBA 7(a) loan program page, the maximum loan amount is $5 million, and for 7(a) loans greater than $350,000, the interest rate cannot exceed the Prime Rate or SBA Optional Peg Rate plus 3%. That same source states the SBA guarantees 85% of loans up to $150,000 and 75% of loans above that amount. For a legal practice, that combination is why 7(a) remains the workhorse for acquisitions, partner transitions, refinancing, and working capital.

The 504 loan is more specialized. It's built for major fixed assets, especially owner-occupied real estate. If your firm is buying its office building and plans to stay put, 504 is often the more natural fit than using a general-purpose business loan for a real estate problem.

The Express option is usually part of the conversation when the borrowing need is smaller and the firm values speed and efficient processing over maximum flexibility. It can be useful, but it's not the answer to every short timeline. Some borrowers assume “Express” means easy approval. It doesn't. It still has to make sense to the lender.

For firms evaluating lenders, this roundup of best law firm SBA lenders helps frame how lender appetite can differ by use case and borrower profile.

SBA Loan Programs for Law Firms at a Glance

| Feature | SBA 7(a) Loan | SBA 504 Loan | SBA Express Loan |

|---|---|---|---|

| Best fit | Working capital, acquisitions, partner buyouts, refinance | Owner-occupied real estate and major fixed assets | Smaller requests where speed is a priority |

| Maximum amount | $5 million | Often used for projects involving long-term fixed-asset financing | Lower than standard 7(a) and generally used for smaller needs |

| Rate structure | Capped under SBA rules for larger loans | Structured for long-term fixed-rate real estate financing | Varies by lender within SBA framework |

| Primary strength | Versatility | Real estate focus | Faster turnaround path |

| Common law firm use | Practice acquisition, goodwill finance, operating cushion | Purchase of office building | Smaller capital need or quick access request |

The real decision point

Don't choose the program by headline. Choose it by asset type and repayment logic.

If the funds are going into goodwill, working capital, debt refinance, or a partner transaction, 7(a) is usually where the analysis begins. If the core objective is controlling occupancy costs through real estate ownership, 504 deserves a hard look. If the need is modest and time-sensitive, Express may be the practical route.

The mistake is trying to fit a law firm's real need into the wrong SBA box because someone heard one program is “faster” or “easier.” The right program is the one that matches the use of proceeds and survives underwriting.

Real World Use Cases for Law Firm SBA Loans

Most firms don't borrow because they like debt. They borrow because timing matters, ownership is changing, or a growth move needs capital before the payoff shows up in the P&L.

Four scenarios that come up repeatedly

A small litigation boutique wants to acquire an older solo practice whose founder is exiting. On paper, the assets look light. There's furniture, some equipment, and an office lease. Principal value stems from the client relationships, referral stream, and transferability of earnings. That's where SBA financing can work well, but only if the goodwill valuation is defendable and the transition plan is credible.

Another firm has outgrown leased space and wants to buy an office building it will occupy. That's a different underwriting conversation. The lender is looking at occupancy, stability, and whether the property supports the operating business rather than distracting from it.

A third firm isn't buying anything. It needs working capital because growth has created a lag between expenses and collections. That's common when headcount rises before revenue catches up in cash terms. In those cases, the loan has to support operating stability, not cover a business model problem.

Then there's the refinance file. A firm used costly debt or stacked short-term obligations to fund expansion. Revenue is fine, but monthly payments are ugly. SBA can sometimes reset the structure into something more manageable if the underlying business is still sound.

Where structure makes or breaks the deal

The most interesting development for larger law firm capital stacks is that, in May 2026, the cumulative loan limit for combining SBA 7(a) and 504 financing was officially increased to $10 million, according to the SBA announcement on the doubled cumulative 7(a) and 504 limit. That matters for firms that want one SBA-backed structure for both business needs and owner-occupied real estate.

That change opens up more strategic combinations. A firm can separate operating needs from the property component instead of forcing everything into one imperfect structure. For practices that own or plan to own their building, that flexibility can change the whole capital plan.

If your law firm wants both working capital and real estate, one blended strategy may be cleaner than trying to make one loan do two jobs badly.

Marketing often shows up alongside these growth decisions. A firm buying another practice or opening a second location usually needs a stronger intake engine too. For that side of the equation, this article on Cincinnati legal practice marketing is useful because it ties local visibility to actual growth execution.

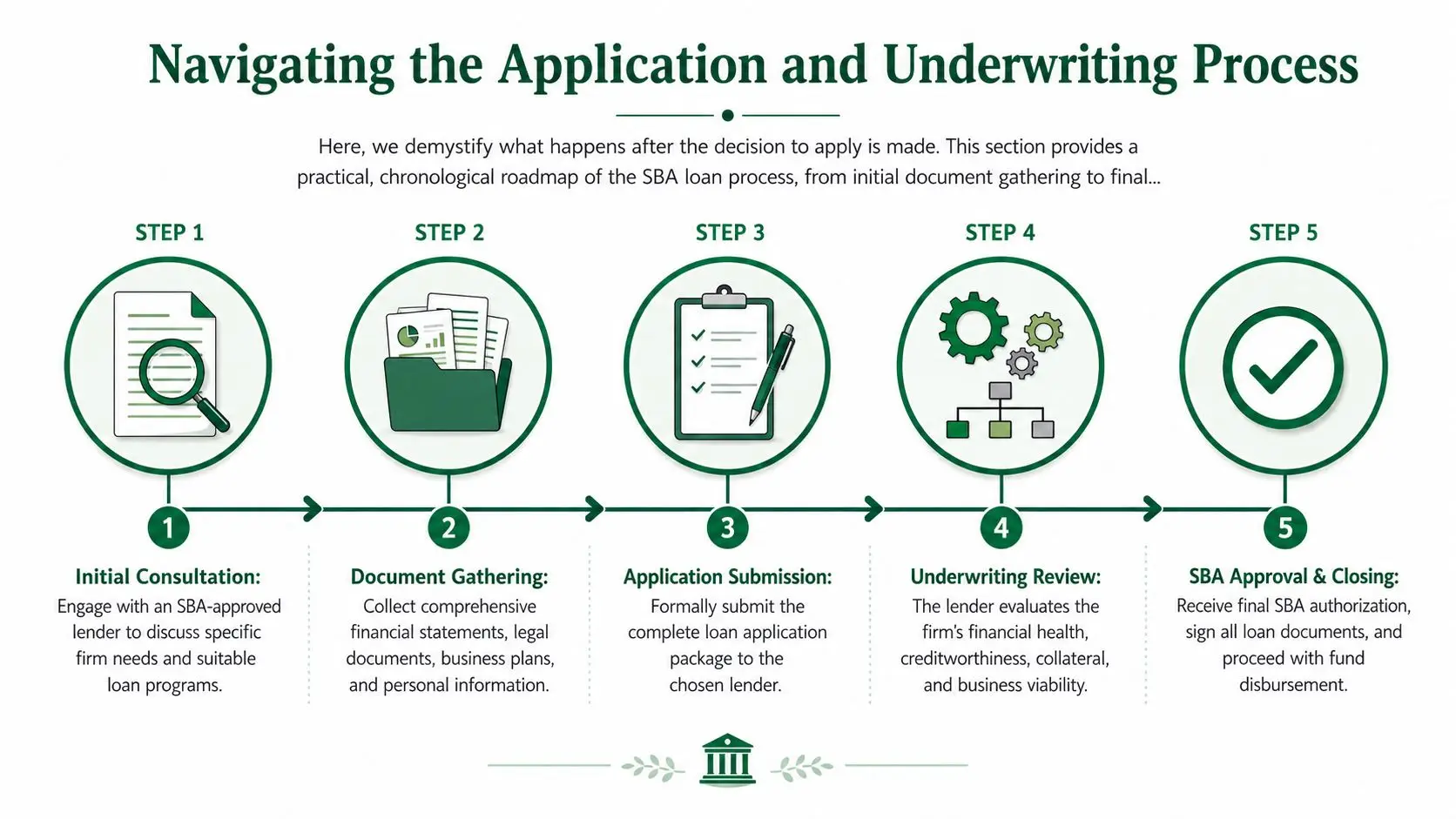

Navigating the Application and Underwriting Process

Once a law firm decides to apply, the process becomes document-driven fast. The easiest way to think about underwriting is this: the lender is trying to answer whether the firm can repay the loan, whether the ownership structure complies with SBA rules, and whether the collateral and transaction documents support the credit.

What lenders ask for and why

Expect the lender to request firm tax returns, interim financials, debt schedules, ownership documents, personal financial statements, and personal tax returns for relevant owners. If the deal involves an acquisition or partner transition, add the purchase agreement or buyout documents, valuation support, and a detailed use-of-proceeds breakdown.

Those requests aren't busywork. Each one serves a credit purpose.

- Tax returns and financials: They show earnings durability and whether the reported story matches reality.

- Ownership documents: They tell the lender who controls the firm and whether any restrictions conflict with SBA requirements.

- Personal financial statements: They help evaluate global repayment strength and guarantor support.

- Projections: They matter most when the deal changes the business, such as adding debt, buying a practice, or opening a new office.

A concise lender memo can help, but the actual work is in the quality of the support underneath it. If your file has internal inconsistencies, underwriters will find them.

How the file moves from inquiry to closing

The process usually follows a predictable sequence:

- Initial screening. The lender tests basic eligibility, use of proceeds, and borrower fit.

- Term sheet stage. If the deal is viable, the lender outlines proposed structure and conditions.

- Underwriting. During this phase, the file gets pressure-tested. Expect questions, clarifications, and revised requests.

- Third-party items. Depending on the deal, that can include valuation work, real estate reports, or legal review.

- Closing. Final documents are signed, conditions are cleared, and funds are disbursed.

A lot of delay happens between steps two and four because borrowers underestimate how much the lender cares about clean explanations. A partner buyout that seems simple internally can create a long underwriting trail if the governing documents are vague or the valuation is unsupported.

If you want a clearer picture of how credit teams think, this guide to how SBA lenders underwrite your deal is a strong primer.

The lender doesn't need a perfect law firm. The lender needs a file that makes sense, is documented, and can survive credit committee scrutiny.

Good borrowers move faster because they answer the next question before it's asked.

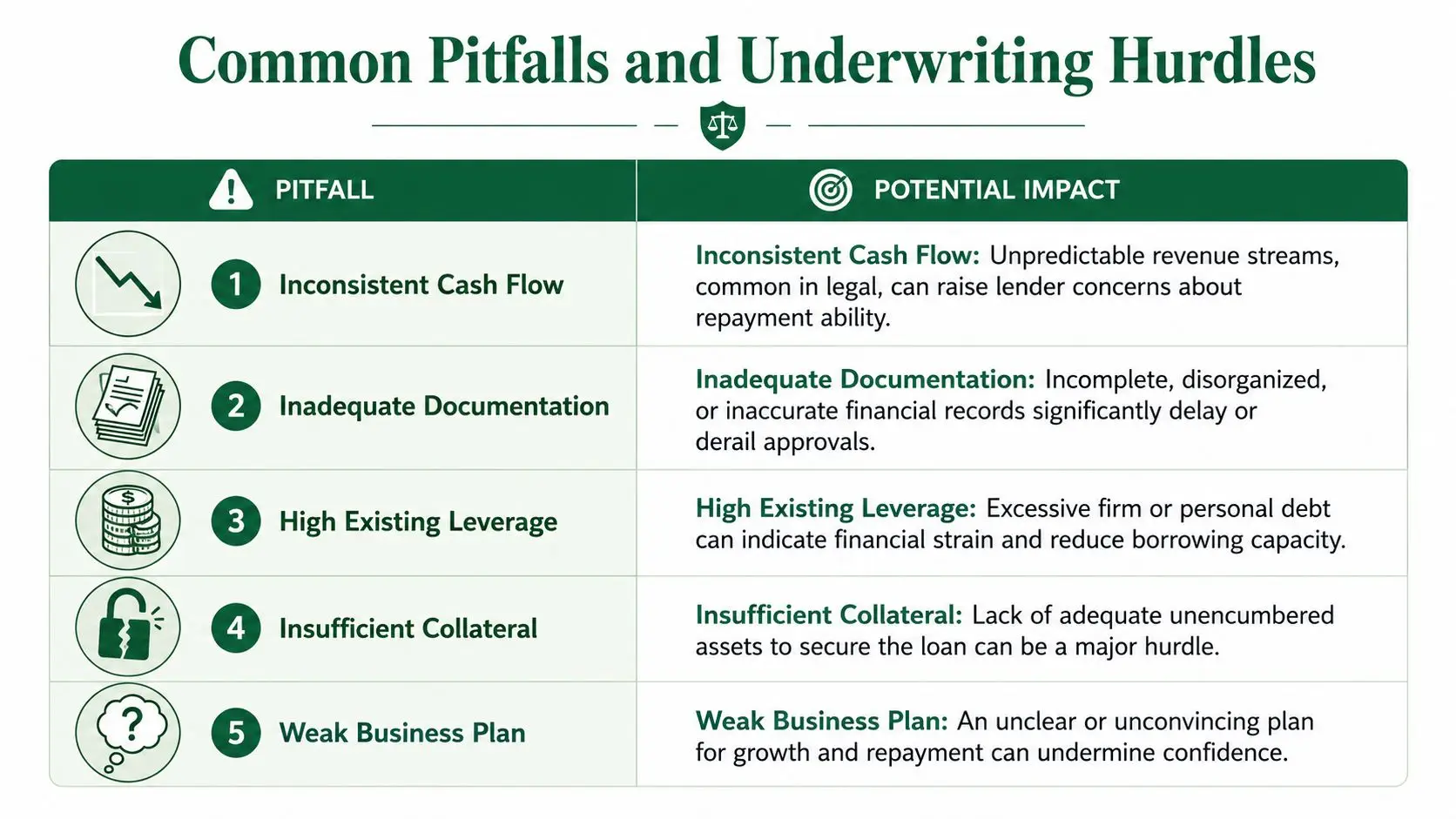

Common Pitfalls and Underwriting Hurdles

Law firms usually don't get stuck because the idea is bad. They get stuck because the file contains one of a handful of recurring problems that lenders know can blow up after closing.

The issues that stall law firm files

The biggest one is goodwill without support. Many law firm transactions are driven by intangible value. That's normal. The problem starts when the borrower treats goodwill like a conclusion instead of something that needs to be justified by earnings history, transferability, client retention logic, and management continuity.

Another common issue is uneven cash flow presentation. Law firms can have lumpy performance. That alone isn't fatal. What hurts the deal is when the borrower hasn't organized the story. If one large matter inflated results, say so clearly. If contingency timing distorted one period, explain it and tie it back to normalized operations.

Partner documents can also create unnecessary friction. I've seen buy-sell terms, compensation arrangements, and legacy governance provisions that made perfect sense for the partners but looked messy to a lender. If the agreement clouds who controls the firm, who can pledge what, or how cash can be distributed, underwriting gets harder.

Then there's client concentration. A firm can be successful and still look risky if too much revenue depends on one client, one practice niche, or one rainmaker whose future role is uncertain after closing.

Why SOP changes matter midstream

SBA rule changes can affect a file that would have worked under an older framework. One important example is the June 1, 2025 update under SOP 50 10 8, which reduced the maximum loan amount for a 7(a) Small Loan from $500,000 to $350,000 and raised the minimum SBSS score for expedited processing from 155 to 165, as described in this SOP 50 10 8 summary. That matters because some borrowers still assume a sub-$500,000 request will follow the older small-loan path.

If your structure no longer fits that lane, the lender may have to move the request into standard 7(a) processing or another route. That can change documentation, timing, and lender appetite.

If you've already been declined, don't assume the answer is final without understanding the reason. This guide to SBA loan reconsideration after denial is helpful when the issue is packaging or lender fit rather than an unfinanceable deal.

How to Improve Your Law Firm's Approval Odds

Approval odds improve long before the application goes in. By the time a lender has your file, the best outcomes usually belong to firms that already cleaned up the weak points.

What strong borrowers do before applying

Start with the firm's financial package. That means current financial statements that reconcile cleanly, a debt schedule that's complete, and an explanation for any unusual trends. Underwriters don't expect perfection. They do expect clarity.

Next, review governance documents before the lender does. If your partnership or operating agreement has transfer restrictions, unusual distribution rules, or unclear authority provisions, identify that now. A late-stage legal cleanup slows everything down.

The third move is simple and often neglected. Prepare a borrower narrative that explains why this loan makes business sense. For a law firm, that narrative should answer four questions:

- Why this use of proceeds

- Why now

- Why the firm can repay

- Why the post-closing management team is stable

How to present a law firm the way lenders need to see it

Law firms often describe themselves in legal terms. Lenders need a credit story.

That means translating your practice into underwritable language. If the firm is buying another practice, explain client retention, transition support, and who will own the relationships after closing. If the request is for working capital, explain what caused the gap and why debt solves it without creating a recurring dependency. If the goal is a partner buyout, explain why continuity improves rather than weakens after the transaction.

A few practical steps help materially:

- Clean up personal credit issues early: Even when the business is strong, owner-level credit problems can complicate guarantees and slow approvals.

- Show stable management: Lenders care about who's running the practice after the loan closes.

- Make projections defensible: A modest, well-supported forecast is more useful than an aggressive spreadsheet no one believes.

- Use the right lender fit: Some lenders understand professional practices better than others.

Working with a specialist can improve packaging, lender matching, and execution quality, especially in acquisitions and partner transactions where structure matters as much as credit. If you want to understand that role more clearly, this overview of what an SBA loan broker does is a good place to start.

Borrowers improve approval odds when they stop thinking like applicants and start thinking like underwriters.

That mindset shift changes everything. It forces you to organize documents, tighten explanations, and surface risks before the lender has to.

Alternatives and Your Next Steps

SBA financing is often the best tool for law firm acquisitions, partner transitions, working capital, and owner-occupied real estate. It isn't the only tool.

When something other than SBA makes sense

A conventional bank loan can work well if the firm is very strong, the collateral is straightforward, and the bank already knows the business. A business line of credit may be better for short-term operating swings that don't justify a full SBA term structure. Private funding can make sense when speed matters more than cost, or when the deal falls outside SBA eligibility. The trade-off is usually price, structure, or both.

For some firms, the right answer is also “not yet.” If the financial statements are messy, the ownership documents need revision, or the acquisition target hasn't been valued properly, forcing an application rarely helps. Better to fix the file and come back with a financeable story.

What to do next

The firms that handle this well don't treat financing as a side task. They treat it like a transaction. They verify eligibility early, choose the right SBA program for the use of proceeds, organize the ownership story, and support goodwill or transition assumptions with real documentation.

That's especially important for law firm SBA loans because legal practices carry underwriting nuances that generic small business advice usually misses. Revenue cap interpretations matter. Partner structures matter. Goodwill matters. The quality of the package matters.

If you're also thinking more broadly about leadership, hiring, or managing legal operations, these Resources for law firm leaders and GCs are worth bookmarking. Financing decisions tend to work best when they sit inside a bigger operating plan.

The bottom line is simple. SBA financing is navigable for law firms, but it rewards preparation and punishes vagueness. If the firm has a credible use of proceeds and the file is built correctly, these loans can be one of the most practical forms of growth capital available.

If you're evaluating a partner buyout, practice acquisition, working capital request, or owner-occupied real estate purchase, GoSBA Loans can help you assess eligibility, structure the deal, and facilitate lender matching through closing with more confidence.