You finally found the business.

The seller is engaged, the broker says other buyers are circling, and the financials look good enough to keep you up at night for the right reason. Then the deal shifts from exciting to heavy. The next decision isn't just whether to buy the company. It's how to structure a loan for business acquisition so you can win the deal, survive underwriting, and still have room to operate after closing.

That last part gets missed all the time. Buyers treat financing like paperwork that starts after the letter of intent. In practice, financing is part of the offer itself. It affects how much cash you need, how much flexibility you have during diligence, what terms you can ask from the seller, and whether the business can comfortably carry debt once you're in the seat.

A good financing strategy doesn't just get you approved. It helps you buy better.

Table of Contents

- The Hunt Is Over Now Comes the Hard Part

- SBA vs Conventional Loans The Core Financing Decision

- The SBA 7a Loan Your Ultimate Acquisition Tool

- Are You Fundable How Lenders Evaluate Your Deal

- Navigating the Acquisition Loan Process Step by Step

- Six Common Buyer Mistakes That Kill Deals

- Your Actionable Checklist for Getting Lender Ready

- Frequently Asked Questions About Acquisition Loans

The Hunt Is Over Now Comes the Hard Part

Most first-time buyers think the hard part is finding a business worth buying. It isn't. The hard part starts after you say, "This is the one."

At that point, every moving piece matters at once. You need a lender that understands change-of-ownership deals. You need a purchase structure that fits lender rules. You need financials that hold up under scrutiny. You need enough cash to close without starving the business on day one. And you need to move fast enough that the seller doesn't lose confidence and move to another buyer.

I've watched buyers lose solid deals for reasons that had nothing to do with the business itself. They offered the wrong structure. They assumed any bank could handle an acquisition loan. They waited too long to talk to lenders. Or they agreed to a price that looked workable in theory but didn't leave enough breathing room after debt service.

The best time to shape financing is before your LOI is fully baked, not after the seller has accepted terms that a lender won't support.

That doesn't mean financing should drive every decision. It means financing needs to sit beside valuation, diligence, and negotiation from the start. If you're relying on debt, your loan structure is part of your acquisition strategy, not an administrative task.

A buyer who understands that usually negotiates better. They know when to ask for seller participation, when to push for a cleaner transition plan, and when to walk from a deal that won't survive underwriting. That's the mindset you want. Not "How do I get a loan?" but "How do I build a financeable deal that still works after close?"

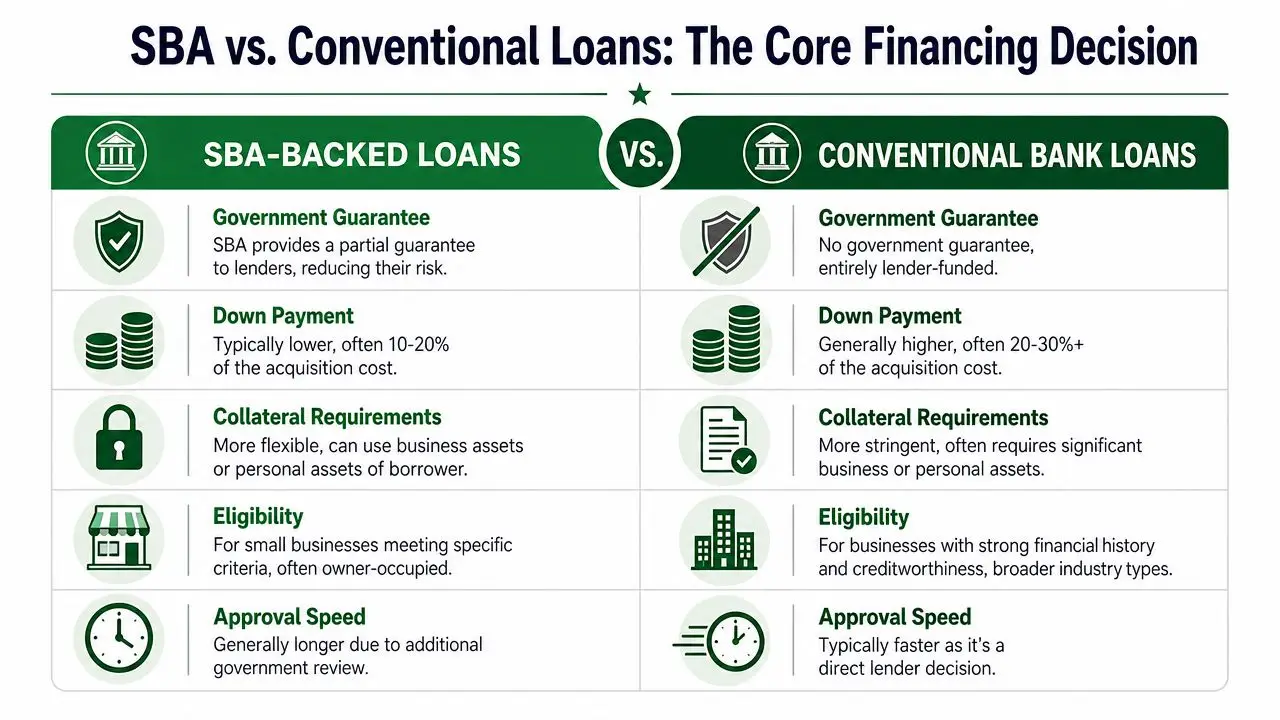

SBA vs Conventional Loans The Core Financing Decision

This decision affects more than approval odds. It affects how much cash you keep for working capital, how you structure the offer, and how much room the business has to absorb a rough first quarter after closing.

A conventional loan can look attractive because it may move faster and carry fewer program rules. But in acquisition lending, speed only helps if the structure survives credit review. Many first-time buyers find out too late that the bank wants more collateral, a larger down payment, or a stronger post-close cash flow cushion than the deal can support.

SBA financing changes that conversation because the lender has a government guarantee behind part of the loan. That support gives banks more room to approve change-of-ownership deals that do not fit a clean conventional credit box. From a buyer's standpoint, that often means lower cash in, longer repayment, and more flexibility when the business value sits in cash flow rather than hard assets.

Here is the practical comparison:

| Feature | SBA-backed acquisition loan | Conventional acquisition loan |

|---|---|---|

| Buyer cash required | Usually lower | Usually higher |

| Amortization | Often longer | Often shorter |

| Collateral pressure | More flexible if cash flow is solid | Usually stricter |

| Process | More documentation and SBA rules | Less program overlay |

| Best fit | First-time buyers, service businesses, limited collateral deals | Strong balance sheets, strong collateral, existing bank relationships |

The trade-off is straightforward. SBA gives you a wider path to approval, but you have to stay inside SBA rules on equity injection, eligible use of proceeds, and how the deal is structured. Conventional lending gives the bank more freedom to say yes, but also more freedom to say no unless the file is unusually strong.

That matters during negotiations.

If a seller wants a premium price, a conventional lender may ask you to fill the gap with more cash. An SBA lender may be open to a structure that includes a properly documented seller note, depending on how the injection and standby terms fit the SOP. That can turn financing into a deal tool, not just a funding source. If you are weighing that option, this guide to seller financing for business acquisition explains where seller notes help and where they create problems.

I tell buyers to choose based on the business they will own on day one, not the loan they hope to get approved. If the conventional option forces you to drain liquidity, shorten amortization, and start ownership with tight debt service coverage, it can be the riskier choice even if the underwriting feels simpler. If SBA terms leave enough cash for payroll, inventory, repairs, and a normal transition dip, that structure usually gives you a better chance to keep the business healthy after closing.

Practical rule: The better loan is the one that makes the acquisition both financeable and survivable.

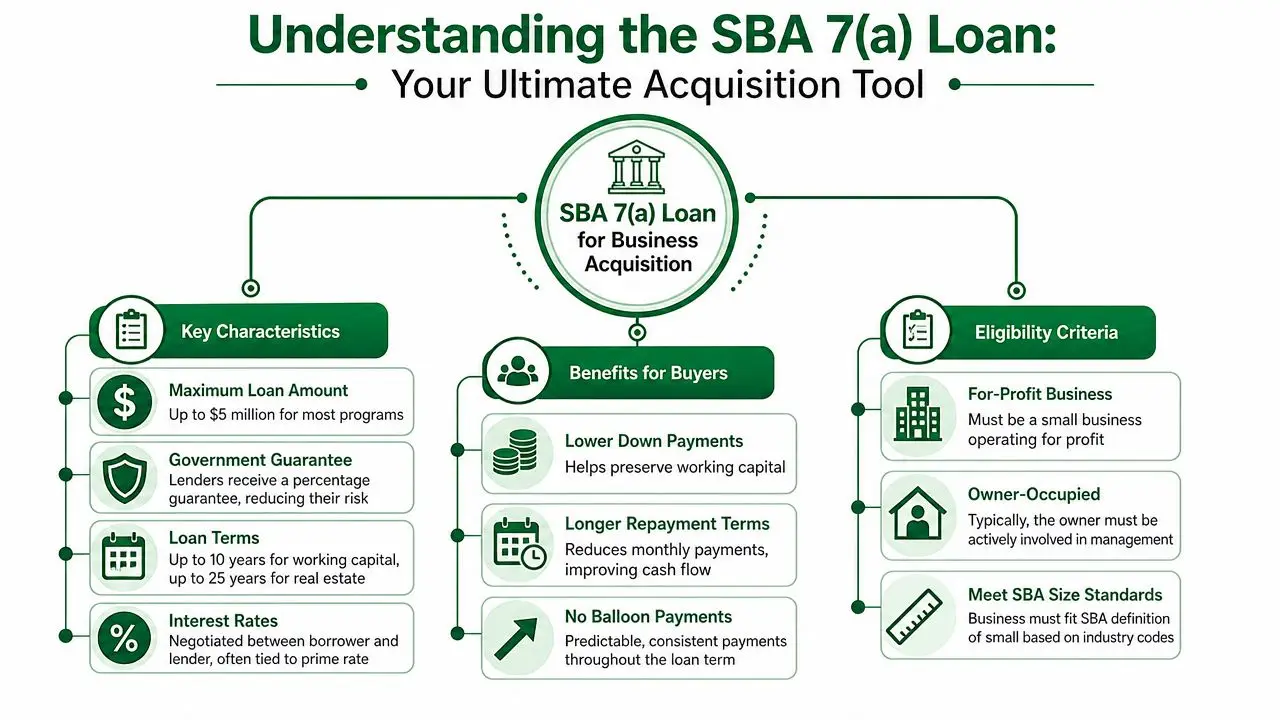

The SBA 7a Loan Your Ultimate Acquisition Tool

The SBA 7(a) loan is the tool that puts more acquisition deals within reach, then gives the buyer more room to operate after closing.

A first-time buyer usually feels the pressure in two places at once. The seller wants certainty and speed. The buyer needs a structure that does not drain every dollar at closing and leave the business short on cash a month later. The 7(a) program works well because it often solves both problems. It can support a full business acquisition, spread repayment over a longer period, and allow a deal structure that is often more flexible than a conventional bank loan if the file fits SBA rules.

That matters in real negotiations. A stronger financing structure can help you offer terms a seller will accept without creating a weak balance sheet on day one. In practice, that often means using the SBA framework to balance purchase price, buyer injection, seller participation, and enough working capital to survive the handoff.

Why 7(a) is often the right acquisition tool

The headline features matter, but the strategy matters more.

Buyers use 7(a) loans because the program is built for owner-operator acquisitions. Loan proceeds can often cover the business purchase, closing costs tied to the transaction, and working capital if the deal supports it. Repayment can stretch long enough to keep monthly debt service from choking the company during the transition period. That gives you a better chance to absorb ordinary post-close friction like employee turnover, slower collections, deferred maintenance, or a few months of uneven performance.

I tell buyers to judge the 7(a) loan by one question: does it leave the business strong enough to perform after the sale? If the answer is yes, it is doing its job.

The rate still matters, of course. But buyers often focus too hard on pricing and not hard enough on structure. A slightly cheaper loan with shorter amortization or a heavier cash requirement can create more risk than a properly structured SBA loan with a payment the business can carry.

How SBA structure helps you win the deal

A 7(a) loan is not just a source of funds. It is a way to shape the transaction.

If the seller expects a price at the top of the valuation range, the SBA structure may give you more options to close that gap without exhausting your liquidity. If the business needs extra cash for inventory, hiring, or repairs right after closing, the deal may be built with that reality in mind instead of pretending the business will run perfectly from day one. If seller financing is part of the stack, the note has to be documented correctly and handled under SBA rules. Standby terms, subordination, and repayment rights all affect whether the lender will give it credit in the structure.

That is where buyers get into trouble. They hear that seller paper can help, then assume any note will satisfy the lender. It will not. SBA lenders underwrite the details, not the label.

How equity injection really works

Equity injection is not just a down payment. It is your proof that you have real money at risk and enough liquidity left to run the company responsibly.

In many acquisitions, buyer cash is the foundation. In some files, a seller note can support the structure if it is set up in a way the lender and SBA will accept. The source of funds also matters. Lenders want a clean paper trail for any injection, and they will review whether your remaining cash reserves are enough for the post-close period.

Three practical rules apply in almost every good 7(a) acquisition:

- Bring enough cash to show commitment and keep the file credible.

- Document the source of every injected dollar clearly.

- Protect post-close liquidity instead of spending every available dollar to get to the closing table.

For a closer look at how lenders apply program rules, this guide to SBA 7(a) loan requirements and qualification covers the standards buyers usually run into. For a simpler outside perspective on how banks review borrower readiness, Stewart Accounting Services loan advice is also useful.

A well-built 7(a) acquisition file does not stop at approval. It sets the business up to make payroll, keep vendors current, handle the transition, and give the new owner a fair shot at success. That is why the 7(a) loan remains the main tool for small business acquisitions. It helps you get the deal done and keeps the business financeable after the ink dries.

Are You Fundable How Lenders Evaluate Your Deal

Lenders don't approve acquisition loans because a business looked attractive in a listing. They approve them because the transaction makes sense after the handoff.

What underwriting is really testing

Underwriting for acquisition loans is driven less by the target company's historical earnings alone and more by the post-close cash flow profile. Lenders typically require multi-year business and personal tax returns, interim financial statements, a business plan, projections, and an estimate of DSCR to test whether the combined buyer-seller transaction can service debt after closing, according to Sunwest Bank's acquisition financing overview.

That explains why lenders ask for so much paperwork. They aren't collecting documents for sport. They're trying to answer a few hard questions:

- Can the business carry the debt after the ownership change?

- Can you run this company credibly?

- Does the purchase price align with the financial story?

- If something softens after closing, is there enough cushion left?

Weak records kill momentum. If the seller's books are messy, customer concentration is high, or add-backs are too aggressive, the lender starts discounting the story quickly.

Clean financials don't just help valuation. They make the lender believe the cash flow is real.

What helps and what hurts

Relevant operating experience helps a lot. It doesn't always have to be the exact same niche, but the lender needs a believable management story. If you're buying a service business and have led teams, managed P&Ls, or sold into similar customers, that's easier to defend than a total leap into an unfamiliar field.

A grounded business plan helps too. Not a glossy deck. A practical operating memo that explains what you'll keep, what you'll change, how you'll handle the transition, and what assumptions sit behind your projections. Buyers who need a clearer lens on how banks read financial strength can also review Stewart Accounting Services loan advice, which is useful for understanding how lenders look at repayment ability and documentation.

Valuation is another pressure point. If your agreed price outruns what the lender and its third parties can support, the gap usually lands back on you through more cash or a revised structure. To avoid this, a focused resource on business valuation for SBA loans can save time before you get too attached to a shaky number.

What hurts most?

- Unclear transition plans

- Messy interim financials

- Projection models that don't match reality

- A buyer with no liquidity left after close

- Deal terms that were negotiated without lender input

Navigating the Acquisition Loan Process Step by Step

You sign the LOI on Friday. By Monday, the seller wants proof you can close, the lender wants a full package, and your attorney is asking whether the landlord will consent to the assignment. This is the point where buyers either create momentum or lose control of the deal.

The process gets easier once you treat financing as a transaction workstream, not a form you submit after the price is agreed. A good loan process does two jobs at once. It helps you win the deal, and it protects the business from starting day one undercapitalized or structured in a way the lender will not support.

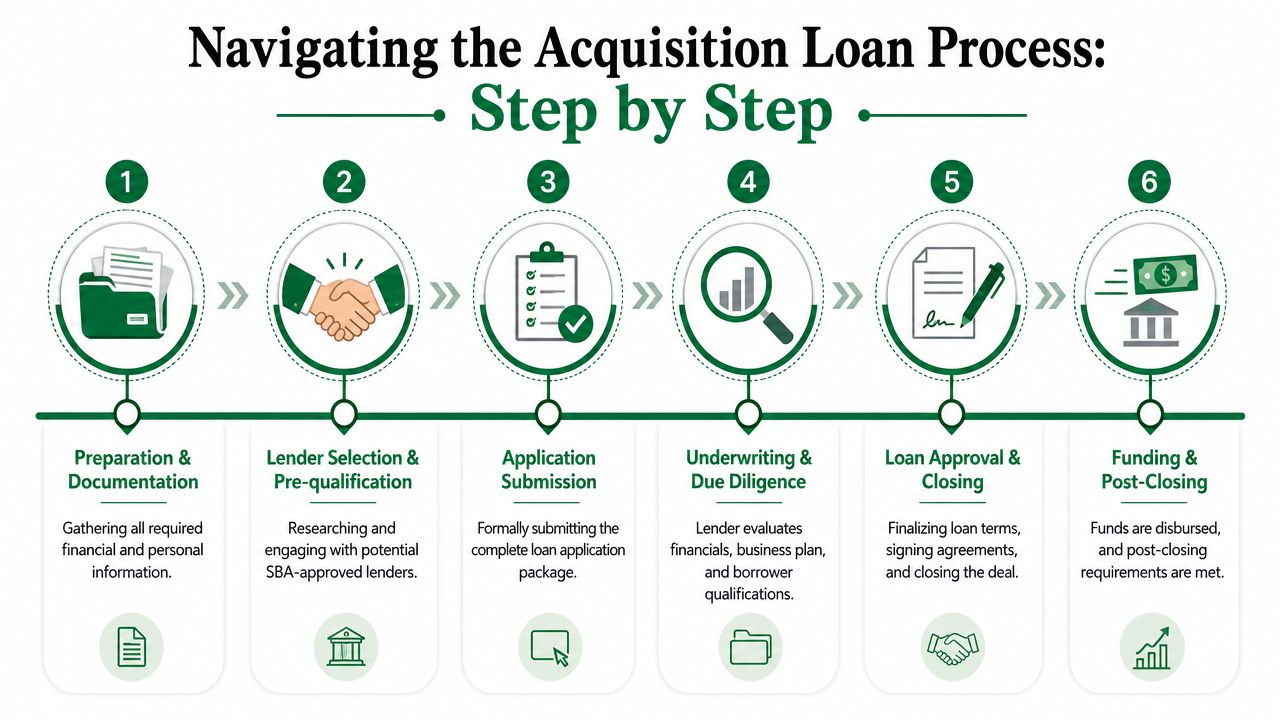

Phase one and two

Pre-qualification and lender matching happen before you get too far down the road with one version of the deal. The buyer's goal here is simple. Find out whether the structure can work under SBA rules, whether the cash injection is realistic, and which lenders like your industry, deal size, and background. SBA 7(a) loans are often the best fit for acquisitions because they can finance goodwill and business value that a conventional bank may not want to carry. But lender appetite still varies a lot from one bank to another.

This early stage is where smart buyers gain negotiating room. If a lender signals that debt service is tight, the fix may be a lower price, a seller note on standby, more working capital in the loan request, or a different transition structure. It is better to make those changes while the seller still wants the deal than after underwriting starts asking hard questions.

Application and due diligence start once the broad structure makes sense. Expect to provide the LOI, buyer financial statement, resumes, tax returns, interim financials, debt schedule, and a clear uses-of-funds summary. The lender is not just checking boxes. They are building the credit story they will have to defend internally and, for SBA loans, under SBA eligibility and repayment standards.

If the target's books are uneven, outside help can then save the transaction. A fractional CFO, quality of earnings provider, or cleanup accountant can turn messy financials into lender-ready reporting. Buyers who need that support during diligence may find AmbitionCFO's M&A insights useful, especially when the numbers need to be organized before underwriting reviews them.

Later in the process, some buyers find it helpful to hear how the pieces fit together in plain language.

Phase three and four

Underwriting and approval are where the lender tests whether your deal survives contact with reality. They review historical cash flow, assess add-backs, compare your projections to actual performance, and check whether the post-close business can support debt and still operate safely. If the seller is staying on for a transition, that plan matters. If key customers or licenses are concentrated around the current owner, that matters too.

This stage slows down for predictable reasons. Buyers submit partial answers. Sellers provide revised financials that do not match prior versions. The purchase agreement changes after credit approval. Every change creates new questions, and every new question can trigger another round of review.

Closing is a document and condition-clearing exercise. The lender will want final organizational documents, insurance, entity formation items, lease assignments or landlord consent if required, evidence of equity injection, and signed seller note terms if seller financing is part of the structure. Counsel may also need to confirm that the asset purchase agreement, stock purchase agreement, and ancillary documents match the approved credit structure.

A clean process usually looks like this:

- Start lender discussions while terms are still flexible. Financing should shape the deal, not chase it.

- Run diligence and loan packaging at the same time. Waiting for one to finish before starting the other burns calendar.

- Answer underwriting questions completely the first time. Half-answers usually create another credit pass.

- Keep one controlled data set. One outdated P&L or tax return can confuse the lender, attorney, and seller at once.

- Protect post-close liquidity. Ask for enough working capital in the structure before documents are final.

If you do not want to manage outreach to multiple banks yourself, GoSBA Loans acts as an SBA loan brokerage that helps coordinate acquisition financing, package the file, and match buyers with lenders that fit the deal.

Six Common Buyer Mistakes That Kill Deals

A lot of dead deals don't die because the business was bad. They die because the buyer made avoidable mistakes.

1. Waiting too long to address financing

Buyers often sign an LOI first and think they'll figure out financing during diligence. That's backwards. If your structure doesn't fit lender rules, you end up renegotiating under pressure.

2. Spending every available dollar on the close

A buyer can technically close and still be set up to struggle on day one. Businesses need cash after ownership changes. Vendors don't care that your bank account is thin because you used everything for the injection.

A deal that leaves you cash-starved isn't a win. It's a handoff to a solvency problem.

3. Treating seller financing as an afterthought

Some buyers are uncomfortable asking for a seller note. That's a mistake. Seller participation can improve alignment and make the structure more workable. It also gives the lender another signal about the seller's confidence in the business.

4. Choosing the wrong lender

Not all SBA lenders have the same appetite. Some like service businesses. Some prefer asset-heavy companies. Some move well on straightforward files and stall on nuanced ones. A buyer who picks based only on brand recognition often pays for it in time.

5. Believing every add-back without challenge

If the earnings story depends on aggressive adjustments, the lender may haircut them or reject them outright. Buyers need to validate what's normal, recurring, and transferable after the sale.

6. Ignoring the transition plan

A business can look stable on paper and still wobble after close if the seller vanishes too fast, key employees aren't addressed, or customer relationships are too concentrated around the departing owner.

The antidotes are simple, but not easy:

- Start lender dialogue early: Get deal feedback while terms are still negotiable.

- Preserve liquidity: Build your closing stack with post-close reality in mind.

- Negotiate structure, not just price: A lower-friction deal often beats a headline number.

- Pressure-test the story: Ask what happens if revenue softens or expenses rise.

- Document the handoff: Operations, staff, customers, and vendor continuity all matter.

Your Actionable Checklist for Getting Lender Ready

Buyers who arrive organized get taken more seriously. Before you formally apply for a loan for business acquisition, have these items ready:

- Personal financial statement: Current, complete, and consistent with your supporting documents.

- Resume or background summary: Show why you're a credible operator for this business.

- Draft business plan: Focus on transition, operations, and realistic projections.

- Target company financials: Clean historical statements, interim results, and tax returns.

- LOI or draft purchase agreement: The lender needs to understand the proposed terms.

- Source of injection memo: Be ready to show where your funds come from.

- Post-close cash plan: Explain what liquidity remains after the transaction.

- Questions for lenders: Ask about industry appetite, process, and likely friction points.

If you can package these clearly, you're already ahead of many buyers.

Frequently Asked Questions About Acquisition Loans

Can I get financing if I'm a first-time buyer

Yes, first-time buyers get acquisition loans. The lender will focus heavily on the business's cash flow, your transferable experience, your liquidity, and how realistic your operating plan is after close. A first-time buyer with a disciplined structure often looks better than an experienced buyer chasing a weak deal.

Is a turnaround business financeable

Sometimes, but it gets harder. Lenders prefer stable post-close repayment ability. If the story depends on fixing multiple problems immediately after takeover, the structure usually needs more equity, more support, or a different capital plan.

Should I work directly with a lender or use a broker

Direct can work if you already know which lender fits your industry and structure. A broker can help when you want broader lender access, a second opinion on deal structure, or help managing packaging and lender communication. The key is not the label. It's whether the person guiding the process understands acquisition underwriting.

How should I think about working capital

Treat working capital as part of the acquisition strategy, not an afterthought. Closing is one event. Operating the company starts the next morning. Your plan should account for payroll cycles, vendor timing, seasonality, and any disruption during the transition.

What if the seller's books are messy

Expect more friction. The lender may ask tougher questions, discount unsupported adjustments, or require stronger third-party validation. In some cases, the right move is to pause, clean up the file, and only then push forward.

If you're planning an acquisition and want help structuring the financing before the deal gets boxed into bad terms, GoSBA Loans can help you evaluate lender fit, package the file, and understand what your transaction is likely to look like under SBA underwriting.