The SBA itself doesn't set an official minimum personal credit score for SBA 7(a) loans, but most lenders want to see a personal FICO of 650 to 680+. That said, your SBA credit score isn't the whole decision. Cash flow, loan type, ownership structure, and the difference between personal FICO and SBSS often matter just as much.

A lot of the advice online gets this wrong. It turns the question into a single number, as if 680 means yes and 679 means no. That's not how real SBA underwriting works. The SBA's published rules and lender behavior are related, but they are not the same thing, and borrowers get in trouble when they treat them as interchangeable.

For a serious business buyer, this distinction matters. You might be looking at a good acquisition with healthy earnings and still worry that a less-than-perfect credit profile will kill the deal. Sometimes it does. Sometimes it doesn't. The difference usually comes down to whether the file gets viewed as a clean credit approval, a cash-flow approval, or an exception request that needs a strong narrative.

The main source of truth is the SBA SOP, which governs program rules. But in practice, lenders still apply their own overlays, especially on personal credit. That's why one lender may decline a file that another lender will structure and approve.

Table of Contents

- Decoding the SBA Credit Score Myth

- The Two Scores That Matter FICO vs SBSS

- Minimum Credit Scores for Each SBA Loan Program

- Whose Credit Is Checked and Why It Matters

- How Lenders Look Beyond Your Credit Score

- Action Plan to Improve Your Fundability

- Your Partner for Navigating SBA Credit Nuances

Decoding the SBA Credit Score Myth

The most common SBA credit score question sounds simple. “What score do I need?” The honest answer is that there isn't one magic number.

A buyer can have a solid target business, relevant operating experience, and a reasonable use of proceeds, then get spooked by conflicting advice online. One site says 620. Another says 680 minimum. A banker says “it depends.” In this case, the banker is the one closest to the truth.

What borrowers usually get wrong

The first mistake is assuming the SBA and the lender use the same credit standard. They don't. The SBA sets program rules. The lender decides whether your file fits its own credit box.

The second mistake is focusing only on personal credit and ignoring the larger underwriting picture. For many deals, the lender cares just as much about the business's ability to service debt, the quality of the financials, and whether there's a credible explanation for any past credit issues.

Practical rule: Don't ask only, “What's the minimum score?” Ask, “What score does this lender usually need for this exact loan type, and what can offset it?”

That's why broad credit-score articles tend to mislead. They flatten a layered process into a single benchmark. If you want a useful reality check, it helps to start with common misunderstandings around SBA financing, including credit myths, lender overlays, and approval assumptions in this guide to SBA loan myths.

What actually determines fundability

In real underwriting, your file is closer to a mosaic than a pass-fail quiz. Lenders look at:

- Personal credit quality: Late payments, charge-offs, collections, and overall FICO trend still matter.

- Business cash flow: If the company can clearly support the debt, a lender has more room to work.

- Loan program fit: Express, 7(a), 504, and microloans do not live in the same credit universe.

- Ownership and guarantees: The wrong partner on the ownership chart can derail an otherwise strong file.

A serious borrower should treat credit as one part of a complete lending case, not the whole case.

The Two Scores That Matter FICO vs SBSS

Most borrowers hear “credit score” and think only about personal FICO. In SBA lending, that's only half the conversation. The other score that often comes up is SBSS, short for Small Business Scoring Service.

Personal FICO is the score lenders live by

Think of personal FICO as your standard driver's license. Every lender checks it because it tells them how you've handled debt personally. It reflects your payment history, existing obligations, and general credit behavior.

In the SBA world, this is the score that usually drives lender comfort. According to Crestmont Capital's SBA loan requirements guide, there is no official minimum credit score mandated by the U.S. Small Business Administration for its 7(a) loan program; instead, the SBA utilizes the Small Business Scoring Service for pre-screening, requiring a minimum score of 155-165 for certain small loans, while individual lenders set their own personal FICO score requirements, typically preferring 680 or higher.

That last point matters most in practice. A borrower may say, “The SBA doesn't require 680.” True. The lender still might.

SBSS is a separate screen

SBSS is closer to a commercial driving test. It isn't just your personal score under a different name. It's a separate scoring model used in SBA lending to evaluate business creditworthiness using a blend of factors that can include personal credit, business financial information, and public record data.

When lenders talk about automated pre-screening on smaller SBA files, this is often the score in the background. Borrowers often confuse it with personal FICO and assume they're interchangeable. They're not.

A strong personal credit profile can help a file, but it doesn't always answer the specific underwriting question the SBSS model is trying to answer.

Why the distinction matters

Serious buyers can save time. If your personal FICO is solid but the lender still pushes back, the issue may not be your personal score alone. It may be the broader business-risk profile reflected in the lender's internal process.

If your credit is weaker, knowing the difference matters even more. Some borrowers get declined too early because they hear a lender preference and mistake it for an SBA rule. Others assume a passable personal score means they're fine, then discover the lender is more cautious than they expected.

The right question isn't “Which score matters more?” It's “Which score is this lender using to make the first cut?”

Minimum Credit Scores for Each SBA Loan Program

Different SBA products attract different lender behavior. That's why asking for one universal SBA credit score is the wrong starting point.

Here's the cleaner way to look at it.

Typical SBA Loan Credit Score Requirements 2026

| SBA Loan Program | Minimum FICO Score | Competitive FICO Score |

|---|---|---|

| SBA 7(a) | 650+ | 680+ |

| SBA Express | 650+ | 680+ |

| SBA 504 | 680+ | 680+ |

| SBA Microloans | 620+ | Varies by microlender |

The ranges above reflect typical lender behavior and program-specific patterns cited by LendingTree's SBA credit score guide, which notes that SBA Express loans typically require a personal FICO of 650+ with top rates requiring 680+, SBA 504 loans often demand 680+, and SBA Microloans can accept scores as low as 620+.

What the table doesn't show

The table gives you a fast screen. It does not tell you how a file will be treated.

For a standard 7(a) request, many lenders will talk as if 680+ is the benchmark because, functionally, that's where files get easier. Below that level, the lender usually wants compensating strength elsewhere. On 504 deals, lenders often apply a stricter personal credit standard because the transaction is usually larger, more document-heavy, and tied to owner-occupied real estate. On Express, lenders often want cleaner borrowers because the speed of the product leaves less appetite for complexity.

Program fit matters as much as score

A borrower buying a clinic, dental office, or veterinary practice shouldn't just ask whether the score clears a minimum. The better question is whether the chosen program fits the transaction. For example, if you're evaluating acquisition financing and comparing structures, this overview of Veterinary Practice Loans is useful because it frames loan options in the context of practice purchases, rates, and use cases.

If you want a broader view of baseline eligibility before worrying about nuance, review the core SBA minimum requirements.

How I'd read these numbers as a borrower

If your score is 680 or better, you're usually in the conversation for mainstream SBA lenders, assuming the rest of the file makes sense.

If you're around 650, you may still be bankable, but lender selection matters more. Some lenders will want stronger business cash flow, more liquidity, or cleaner explanations for any prior credit events.

If you're looking at Microloans, the mission-based lending model can be more forgiving. That doesn't mean easy. It means the underwriting lens can be different.

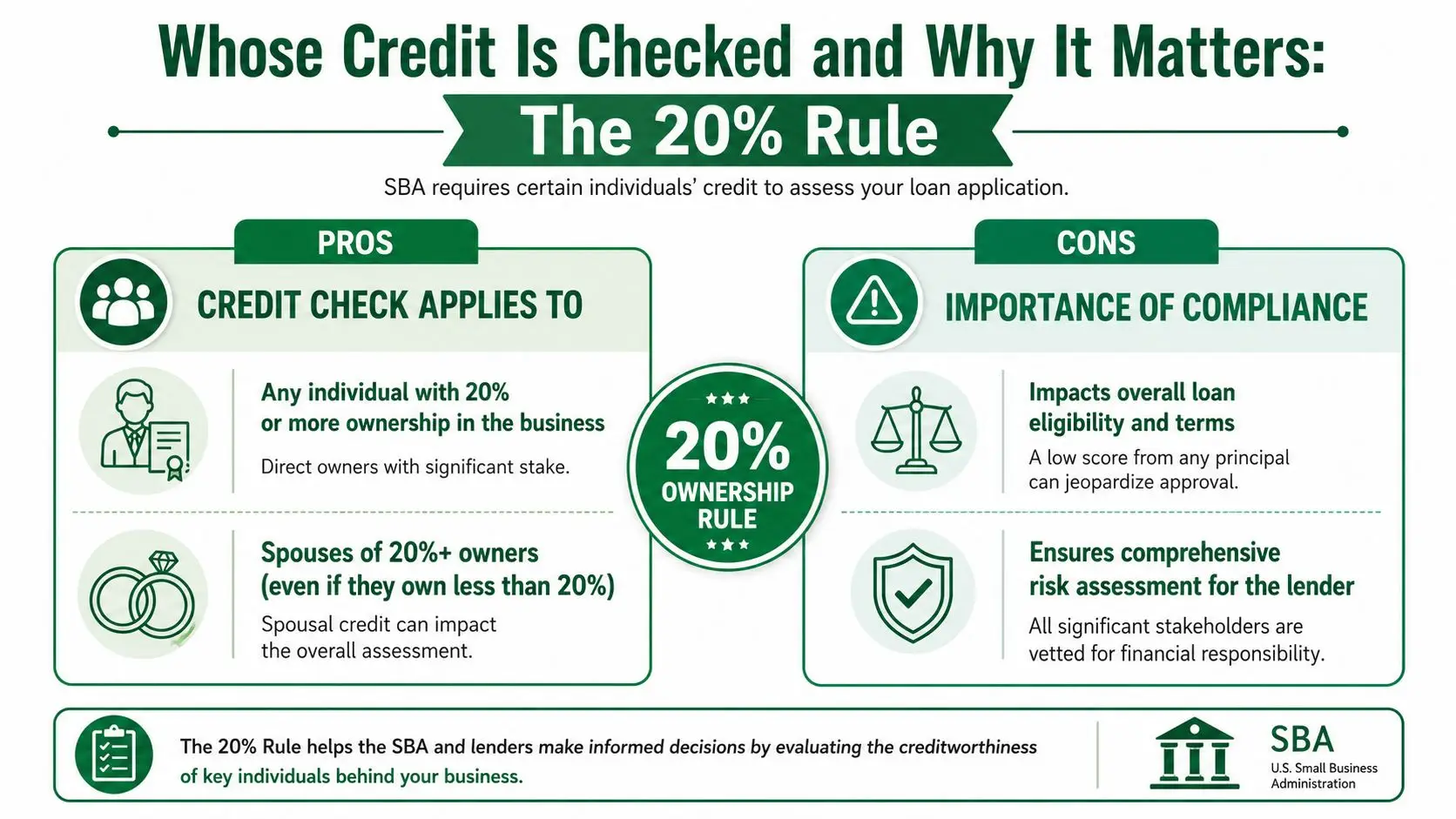

Whose Credit Is Checked and Why It Matters

A lot of borrowers assume the lender only checks the lead buyer's credit. That's not how SBA lending works when multiple owners are involved.

For SBA purposes, ownership drives personal guarantee requirements, and guarantee requirements drive whose credit gets scrutinized.

The 20 percent rule changes the file

According to The Credit People's overview of SBA 7(a) requirements, for any applicant owning more than 20% equity in the business, a minimum personal FICO score of 640 is required by most lenders, with 680+ considered optimal. This 20% ownership rule is a mandatory SBA policy, meaning all major owners must provide a personal guarantee and have their credit individually evaluated.

That means a deal doesn't rise or fall on one person's score alone. It rises or falls on the guarantee group.

One weak guarantor can hold up everyone

Here's the practical problem. Suppose a business has three partners. Two have clean credit and one has major unresolved issues. The lender doesn't ignore the third owner because the other two look strong. That weaker profile can force a decline, a restructure, or a request to change ownership percentages.

When a lender says, “We have a credit issue,” that often means “someone on the guarantee side doesn't fit our box,” not “the business is bad.”

This comes up often in family businesses, partner buyouts, and newly formed acquisition entities. If you're still early in the process and working through ownership and entity setup, this guide on forming a business in California is a useful legal primer for structuring decisions that can affect financing later.

What to do before filing an application

Borrowers do themselves a favor by checking the full guarantor group before the lender does. Don't wait for underwriting to discover the issue.

A few practical steps help:

- Map the ownership tree: Identify every direct owner who crosses the guarantee threshold.

- Pull credit early: Every required guarantor should know where they stand before the file goes out.

- Address structure issues upfront: Sometimes ownership percentages, holdco arrangements, or timing of transfers need legal and lending review before submission.

- Review guarantee obligations: This overview of SBA personal guarantee requirements helps clarify who is likely to be on the hook and why.

This part of SBA credit screening is mechanical. It isn't personal, and it isn't optional.

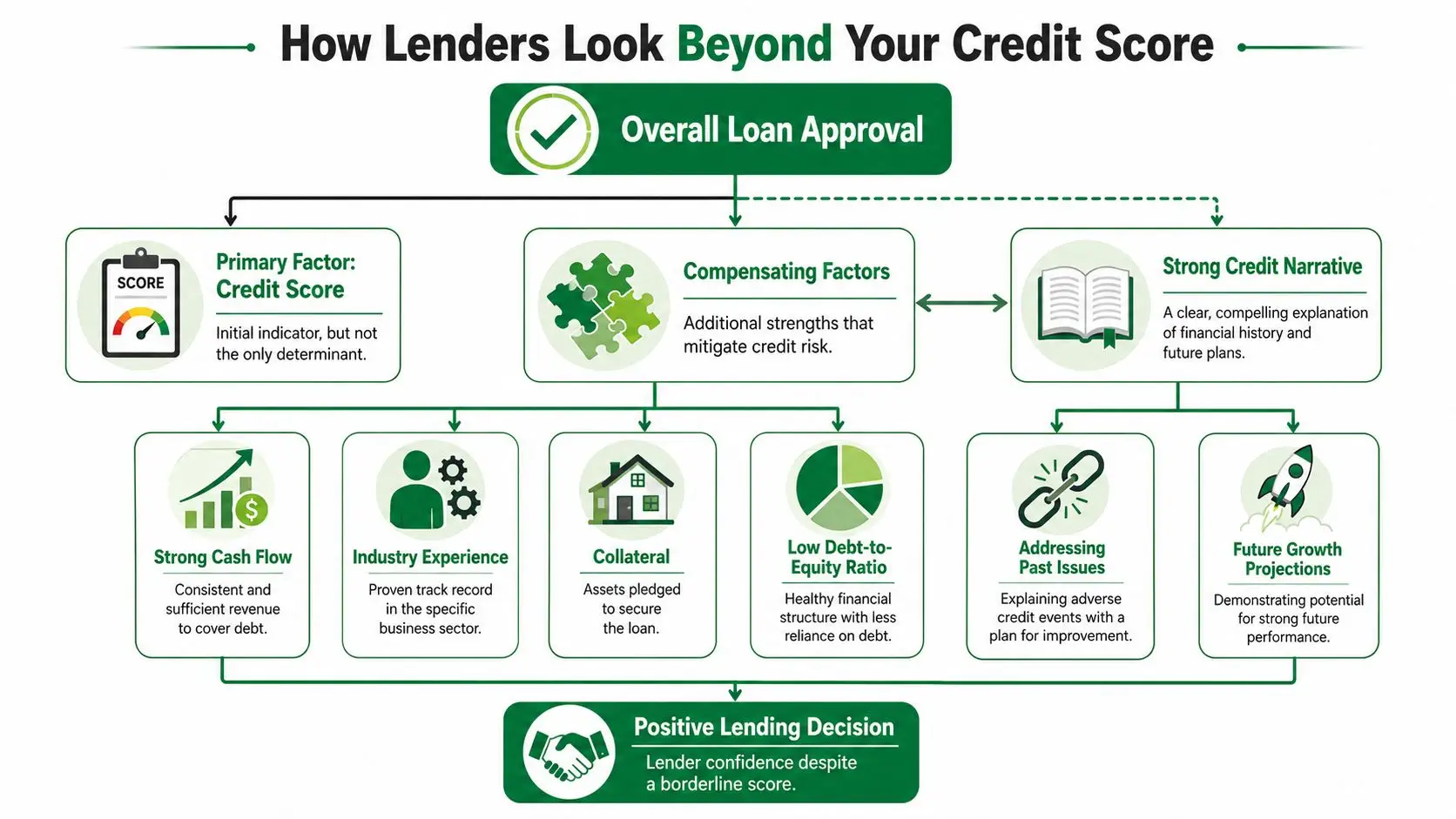

How Lenders Look Beyond Your Credit Score

Borderline credit doesn't automatically kill an SBA deal. But once a file drops below a lender's preferred FICO range, the lender needs another reason to say yes.

That reason is often cash flow.

DSCR is the compensating factor that actually moves credit policy

In standard SBA underwriting, DSCR, or Debt Service Coverage Ratio, is one of the most important offsetting strengths a borrower can have. According to Bay Street Lending's SBA loan requirements guide, for standard SBA 7(a) and CDC/504 loans, a DSCR of 1.15 is the critical compensating factor that allows lenders to accept personal FICO scores down to 640–650, overriding the typical 680+ benchmark. Without this cash flow buffer, scores below 650 often lead to rejection.

In plain English, a 1.15 DSCR means the business generates $1.15 in cash flow for every $1.00 of debt obligation. That margin doesn't make a weak file perfect, but it gives a lender a rational basis to approve a borrower who's outside the ideal credit box.

What lenders will still ask themselves

Even with acceptable DSCR, lenders don't stop thinking about credit. They ask a different set of questions:

- Was the credit issue isolated or habitual? A single event with a clean recovery story is easier than repeated sloppiness.

- Does the borrower understand the business? Industry experience can calm lender nerves.

- Is there collateral support? Collateral rarely fixes a bad deal, but it can help support an exception.

- Does the file make sense as a whole? Clean tax returns, orderly financial statements, and consistent explanations matter.

Underwriting reality: A lender approves a story it can defend. Strong cash flow plus a coherent explanation beats a weak narrative with a slightly better score.

What doesn't work

Borrowers often overestimate the value of two things.

First, they assume collateral alone will save the deal. Usually it won't if the credit and cash flow profile are both weak.

Second, they assume a verbal explanation is enough. It usually isn't. Once a credit profile is borderline, the file has to be documented well. If you want to understand how lenders stack these factors in real underwriting, this breakdown of how SBA lenders underwrite your deal is worth reading.

A serious buyer should think of credit as the opening screen and DSCR as the evidence that can reopen the conversation.

Action Plan to Improve Your Fundability

If your credit is excellent, preparation still matters. If your credit is borderline, preparation is the difference between a quick decline and a real review.

The goal isn't to manufacture a perfect file. The goal is to present a file that a lender can underwrite with confidence.

Start with the credit file you actually have

Pull your personal credit reports and read them line by line. Don't rely on memory, and don't assume the lender will overlook obvious errors.

Then work the file in order:

- Dispute factual errors: Wrong balances, duplicate accounts, and outdated derogatory items can drag a file down unnecessarily.

- Pay attention to revolving balances: High utilization signals stress even when payments are current.

- Avoid fresh inquiries: A lender reviewing an SBA file doesn't like seeing a borrower shopping for unrelated debt at the same time.

For borrowers trying to strengthen the business side of the profile as well, this resource with actionable advice on business credit is a practical companion to the personal-credit work.

Write the explanation before the lender asks for it

If you've had late payments, collections, a prior hardship, or any other blemish, prepare a clear Letter of Explanation. Keep it factual. Keep it short. Most important, show what changed.

A useful explanation usually includes:

- What happened: Job loss, medical event, partnership dispute, or another concrete cause.

- When it happened: Tie the issue to a specific period.

- Why it won't recur: Improved liquidity, reduced debt, stable operations, or a resolved dispute.

Don't write a defensive essay. Write something a credit officer can summarize in a credit memo without needing to decode it.

Use the 2026 small-loan shift strategically

One of the most important recent changes affects smaller 7(a) requests. According to FastWay SBA's review of 2026 SBA loan requirements, a critical 2026 regulatory shift removed the mandatory SBSS pre-screening for 7(a) loans under $350,000. This allows borrowers with weaker personal credit, such as 640–650, but strong business cash flow with DSCR above 1.25, to bypass the automated rejection that previously occurred, giving lenders more discretion to approve the loan based on other strengths.

That creates a real opening for borrowers who used to get screened out too early.

If your deal falls into that size range, lender selection matters even more because some institutions will still use conservative internal scoring while others will spend more time on the actual merits of the file.

A borrower with imperfect credit and strong cash flow is no longer automatically boxed out of every small 7(a) conversation.

Build the package lenders want to see

Good borrowers often lose momentum because the package is messy. Clean packaging helps lenders take risk more confidently.

Focus on these items:

- Financial statements that tie together: The tax returns, P&L, balance sheet, and bank activity should tell the same story.

- A clear use of proceeds: “Working capital” by itself is weak. A specific use is easier to underwrite.

- Ownership clarity: Make sure percentages, guarantees, and legal documents line up.

- Financial discipline: This guide to small business finance management is a useful checklist for borrowers who need to tighten operations before they apply.

Fundability improves when the lender doesn't have to guess.

Your Partner for Navigating SBA Credit Nuances

The lesson on SBA credit score requirements is simple. There isn't one rule. There are SBA rules, lender overlays, program-specific standards, and deal-specific exceptions.

That's why the most popular advice tends to fail serious borrowers. It treats personal FICO as the full answer when the actual decision often depends on a layered review. Personal credit matters. So does the distinction between FICO and SBSS. So does the ownership group. So does cash flow. And on smaller 7(a) loans, recent rule changes create room for lenders to use more judgment than many borrowers realize.

A buyer who understands those moving parts can make better decisions early. That includes choosing the right SBA product, identifying credit problems inside the guarantor group before underwriting, and presenting a file that emphasizes the strengths lenders care about most.

Most failed SBA applications don't fail because the borrower had no chance. They fail because the file was mismatched to the lender or packaged without a strategy.

If you're evaluating an acquisition, refinance, partner buyout, or owner-occupied real estate deal and want help matching your profile to the right lender, GoSBA Loans can help you understand the credit nuances, structure a stronger file, and improve your odds of getting funded on workable terms.