You've probably found a business that looks right on paper. The seller says the numbers are solid, the broker says it's financeable, and you're already thinking about day one as the new owner. Then the hard part shows up. How do you get the deal funded without blowing up the timeline, overpaying in cash, or discovering too late that the lender won't approve the structure?

That's where most first-time buyers get stuck. They don't fail because the business is bad. They fail because the financing was treated like a formality instead of part of the deal itself.

An SBA loan to buy a business is often the best path for an owner-operator acquisition. The SBA 7(a) program is the most popular financing vehicle for acquiring an existing business, including buying out a partner or opening a franchise, and more than 10,300 closed transactions were reported through the BizBuySell marketplace platform last year. But the generic advice online leaves out the details that determine approvals. The specific DSCR lenders seek. The seller note rules that can undermine a deal. The working capital gap buyers miss in the LOI.

Table of Contents

- The First Step to Buying Your Dream Business

- Choosing the Right SBA Loan for Your Acquisition

- Decoding Eligibility and Borrower Requirements

- The Loan Process From Letter of Intent to Closing

- Common Pitfalls That Can Instantly Kill Your Deal

- Your Next Steps to Secure Acquisition Funding

The First Step to Buying Your Dream Business

A common buyer story goes like this. You've spent months sorting through listings, talking to brokers, and narrowing the field. Then you find one that clicks. The company has steady customers, the owner is ready to retire, and you can see yourself running it.

Then the questions start piling up. How much cash do you need? Will the lender count a seller note? Does your background fit the business? Is the timeline realistic if the seller wants to close fast?

That's the point where financing stops being an afterthought and becomes the center of the transaction. The SBA program exists for exactly this kind of acquisition. It gives buyers a way to purchase an operating business without bringing in the full purchase price in cash upfront, and it creates a framework lenders can underwrite with confidence.

Practical rule: The best buyers don't ask, “Can I get an SBA loan?” They ask, “Can this specific deal be structured in a way the lender will approve?”

That's a very different question.

Before you get too deep into lender conversations, make sure you're looking at the right target in the first place. A cleaner business, in a financeable industry, with usable records is easier to fund than a “great opportunity” with messy books. If you're still early in the search, this guide on how to find a business to buy is a good place to tighten your criteria.

The good news is that there is a path. Buyers use SBA financing every day to acquire service companies, trades businesses, distribution firms, franchises, and owner-occupied operating businesses. The bad news is that strong deals still die when buyers miss the unwritten rules. That's where experience matters.

Choosing the Right SBA Loan for Your Acquisition

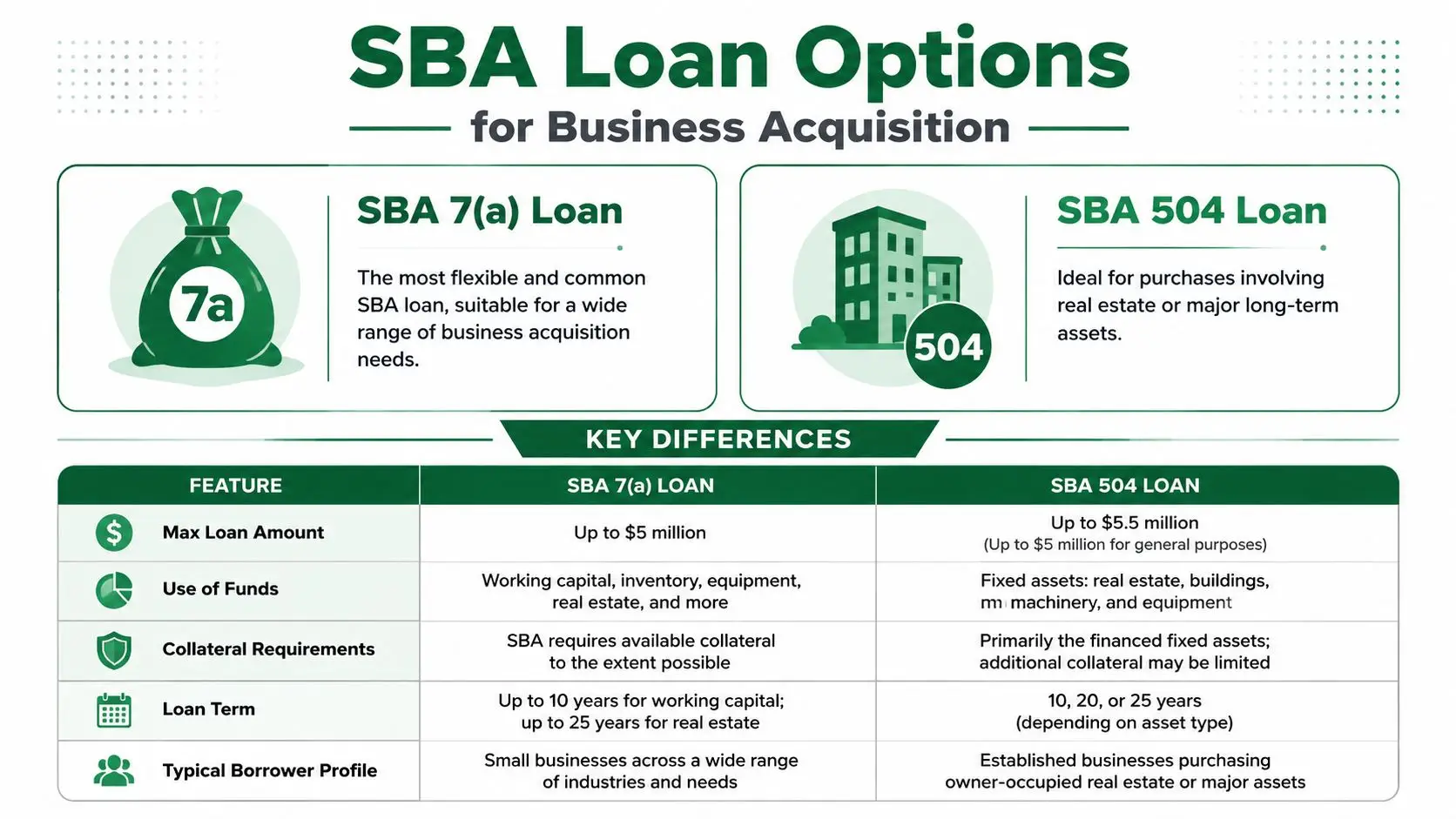

For most buyers, the choice comes down to SBA 7(a), SBA 504, or SBA Express. They are not interchangeable. The right one depends on what you're buying, how the assets are structured, and whether working capital needs to be part of the same financing package.

A defining feature of SBA acquisition financing is that it can fund up to 90% of the total purchase price, and the maximum loan amount for most 7(a) programs is $5 million, according to Banner Bank's SBA acquisition overview.

Which loan fits which deal

The 7(a) loan is the workhorse. If you're buying an operating company and need flexibility for goodwill, inventory, some closing costs, and working capital, this is usually where the conversation starts. It's also the program most buyers mean when they say they want an SBA loan to buy a business.

The 504 loan is more specialized. It works best when the acquisition includes significant owner-occupied real estate or major fixed assets. The structure is different. The private lender provides 50%, the SBA-backed CDC provides up to 40%, and the borrower contributes 10% for eligible projects involving fixed assets. That can be a strong option when real estate is core to the business and clearly tied to operations.

The Express loan is the small-cap version. It can be useful for simpler, smaller transactions, but it has a much lower cap than standard 7(a), so it isn't the right fit for most full business acquisitions unless the deal size is modest.

A side-by-side comparison

| Feature | SBA 7(a) Loan | SBA 504 Loan | SBA Express Loan |

|---|---|---|---|

| Max Loan Amount | $5 million | $5 million for fixed assets only | $500,000 |

| Use of Funds | Broad acquisition flexibility | Fixed assets, often real estate-heavy deals | Smaller transactions with tighter limits |

| Collateral Requirements | Business assets, plus other support as required | Fixed-asset focused structure | Similar risk review, but smaller scope |

| Loan Term | Varies by use, up to longer terms including real estate | Long-term fixed-asset financing | Shorter practical reach due to size cap |

| Typical Borrower Profile | Buyer acquiring an operating business | Buyer acquiring a business with owner-occupied real estate | Buyer with a small acquisition or limited funding need |

One mistake I see often is buyers picking the loan product by speed instead of fit. That usually backfires. A fast answer on the wrong structure doesn't help if the lender later says the use of proceeds doesn't work.

Another mistake is assuming 504 is a cheaper 7(a). It isn't. It has a narrower lane. The property must support the operating business, and the owner-occupied requirement matters. If the property isn't essential to the business model, the deal can get knocked out.

If you want a deeper breakdown of how the flagship program works, this guide to SBA 7(a) loans in 2026, including requirements and how to qualify gives useful context before you start structuring offers.

For pure business acquisition deals, 7(a) usually gives you the cleanest path. For real-estate-heavy transactions, 504 can be powerful if the occupancy and business-purpose story are solid.

Decoding Eligibility and Borrower Requirements

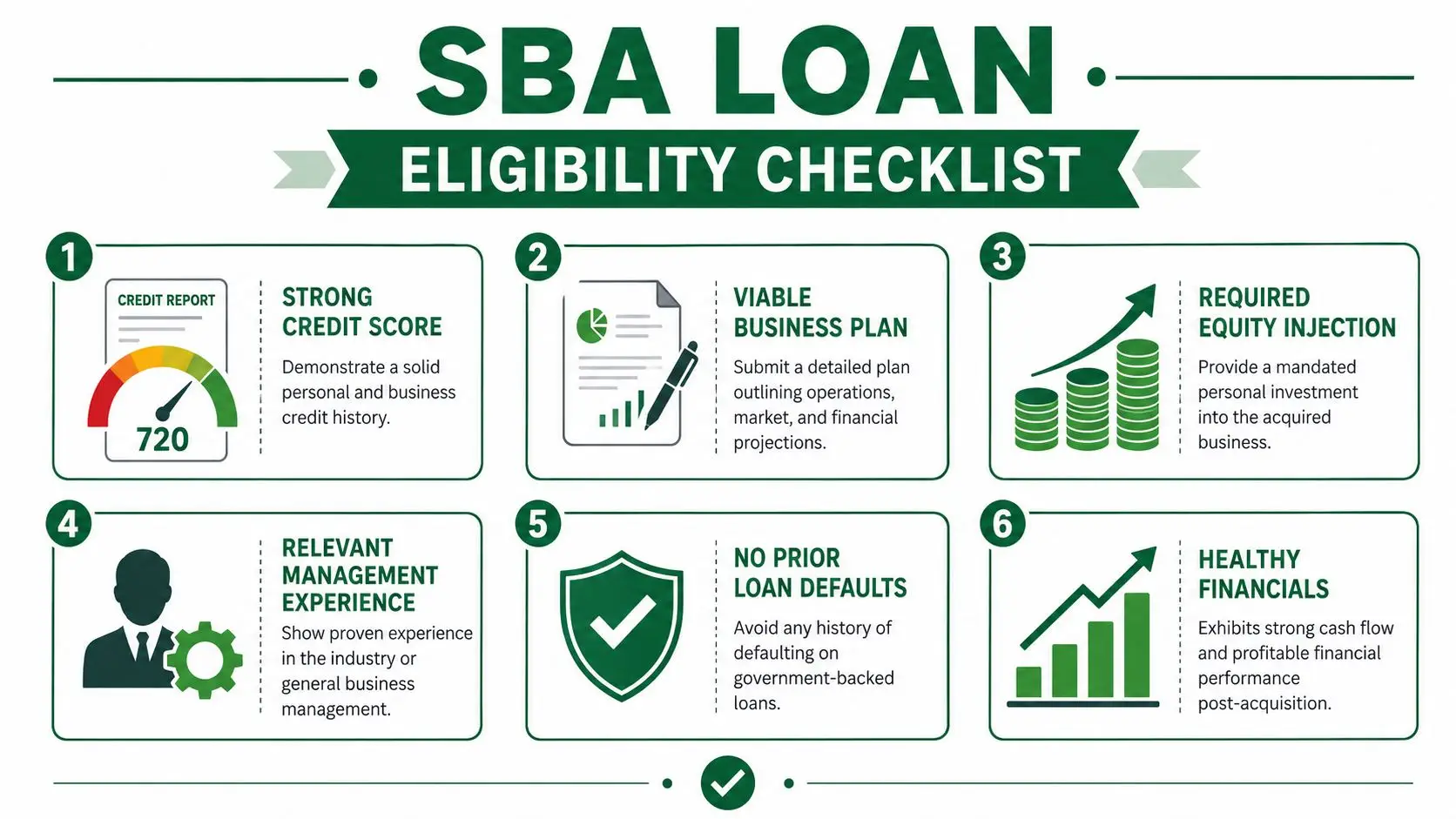

A buyer can find a good business, sign a reasonable LOI, and still get declined because the file fails on the borrower side. That happens more often than first-time buyers expect. Lenders are not only asking whether the company can produce cash flow. They are asking whether you can step in, keep that cash flow stable, and survive the transition.

That changes how a strong application is built. The file has to show a credible operator, a clean equity story, and enough post-close cash flow to satisfy both SBA rules and the lender's internal credit standards.

What lenders screen first

Underwriting usually starts with three questions.

First, can the borrower qualify personally? Credit still matters in acquisition lending, and many lenders want to see a score around 680 or better before they spend much time on the file.

Second, does the borrower meet SBA size standards? For many buyers, that is straightforward. But lenders still verify it because SBA eligibility is not optional, and a file with a size issue can stall late if no one checked it early.

Third, can the buyer run the business? This is one of the unwritten deal-breakers. A lender does not need perfect industry overlap, but they do need a believable management case. If you are buying a plumbing company after years in field service management, that can work. If you are buying a specialized manufacturer with technical processes, no operating background, and no retained management team, expect resistance.

For a baseline before you package the file, review these SBA loan requirements for borrowers and businesses.

A short explainer can help frame the basics before the deeper lender conversations start:

What counts as your down payment

For a business acquisition, the equity injection is often at least 10% of the total project cost. Buyers know that part. What they miss is that the structure matters as much as the percentage.

Cash is the cleanest option. Gift funds can work with proper documentation. Retirement funds and borrowed funds can work in some cases, but they create more diligence and more questions about repayment capacity.

Seller notes are where many deals get misread. A seller note may help satisfy part of the equity requirement if it is structured to meet SBA and lender standards, which often means full standby for a defined period. If the note has principal payments too early, monthly debt service, or unclear subordination terms, many lenders will not give it equity credit. The buyer thinks they have 10% in. The bank underwrites it as short.

A seller note can strengthen a deal or break it. The difference is usually in the standby language, payment timing, and whether the lender is willing to count it toward injection.

Why cash flow gets deals approved or killed

The headline number is DSCR, or Debt Service Coverage Ratio. On paper, SBA guidance may allow lower coverage in some cases. In bank credit committees, acquisition files usually need more cushion. In practice, submissions below the 1.20x to 1.25x range face much tougher odds.

That is one of the unwritten rules generic guides skip. Buyers often build projections to the floor and assume the lender will stretch because the industry is stable or the seller has done well for years. Many lenders will not. They know the first year after a change of ownership is where mistakes show up, customers drift, and expenses rise.

Working capital is tied to that same issue. If the deal uses every available dollar for the purchase and leaves the business tight on payroll, inventory, or seasonality swings, underwriting gets uncomfortable fast. I have seen decent businesses lose financing because the buyer focused on price and ignored the cash needed to operate in month one.

A bankable acquisition package shows more than eligibility. It shows margin for error. That usually means a buyer with relevant experience, a documented and acceptable injection source, a seller note that is structured correctly if one is included, and enough cash flow after closing to handle debt without relying on optimistic projections.

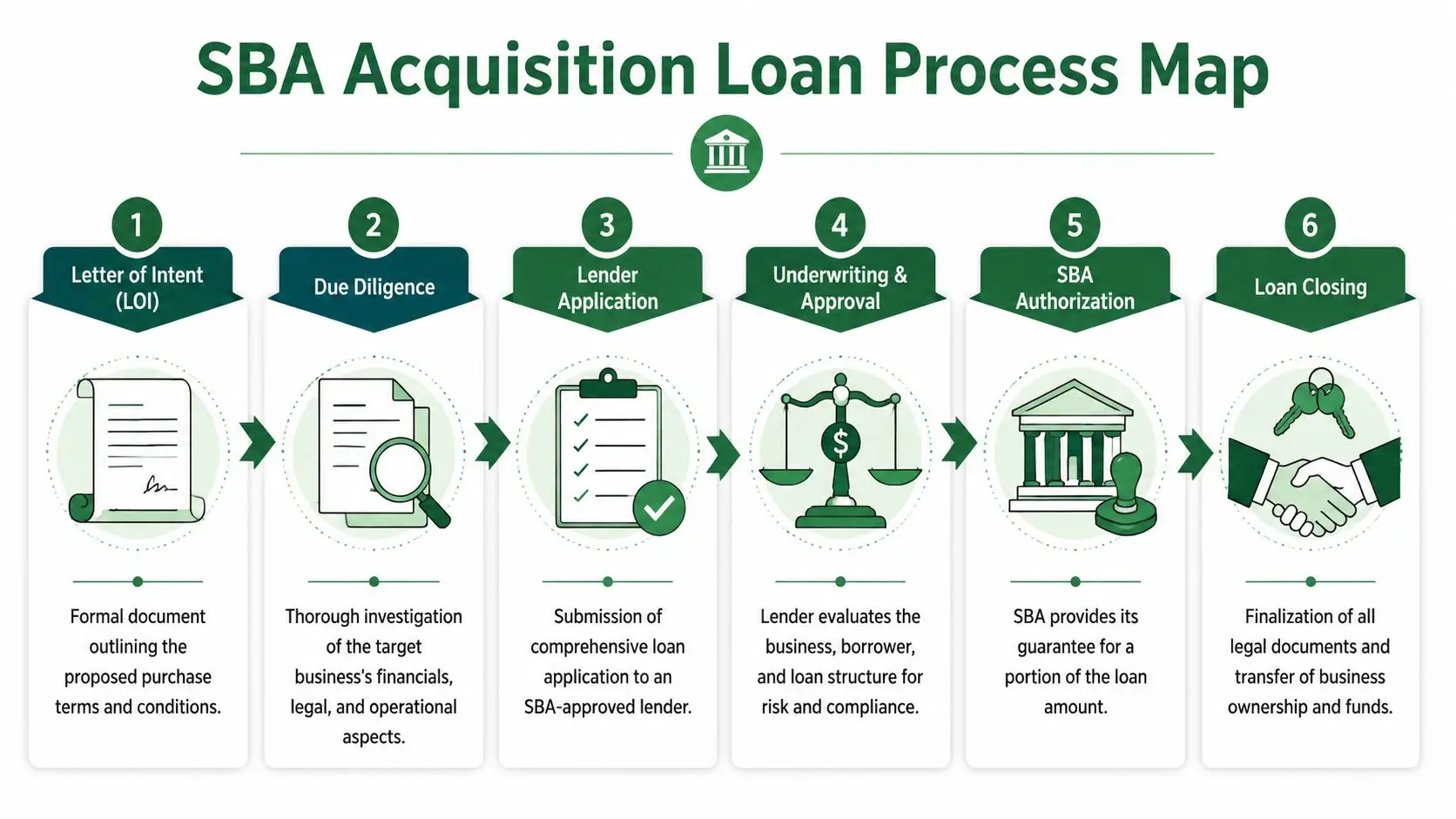

The Loan Process From Letter of Intent to Closing

Once your offer is accepted, the financing process turns into a document-and-timing exercise. The faster you get organized, the smoother the file moves. The slower you respond, the more chances the deal has to drift, get repriced, or die in underwriting.

The average timeline from application to funding is 45 to 90 days, and one of the biggest choke points is third-party valuation and underwriting review when the lender sees gaps or inconsistencies in the file.

What happens first

The process usually starts with the LOI, not the full purchase agreement. That LOI needs to be more than a rough price and closing date. It should already reflect how the financing is expected to work, especially if seller financing, working capital, or post-close support will matter.

After that, the lender wants a package that tells a coherent story. That includes your background, the target company's financial performance, the proposed sources and uses of funds, and why the business will remain stable after the ownership transition.

A clean sequence looks like this:

- Sign the LOI with acquisition terms that can be financed.

- Complete due diligence on financials, operations, legal documents, and customer concentration.

- Submit the lender package with buyer and business information.

- Go through underwriting while the lender reviews cash flow, structure, and compliance.

- Satisfy closing conditions such as valuation, entity documents, and any lender-specific requirements.

- Close and fund once approval conditions are cleared.

What underwriting actually checks

Underwriting isn't just checking if the business made money. It's testing whether the file holds together under scrutiny.

The lender will pressure-test:

- Cash flow coverage: Does the business support debt at the level the lender expects?

- Valuation support: If the purchase price is too aggressive, the value conclusion can create a gap.

- Management transition: Will customers, employees, and vendors stay stable after the sale?

- Capital structure: Are the buyer injection, seller note, and any outside investor funds documented properly?

- Working capital need: Is there enough liquidity built into the deal so the business doesn't struggle immediately after closing?

A lot of deals don't fail because the business is weak. They fail because the LOI promised a structure that couldn't survive underwriting.

The underwriting team also pays close attention to how the file was assembled. Missing schedules, unclear adjustments, or unexplained add-backs make the lender distrust the whole package.

Your document checklist

The buyers who move fastest are usually the ones who prepare most of the package before the lender asks. At minimum, expect to gather:

- Personal financials: Personal financial statement, personal tax returns, ID, and a current resume.

- Entity records: Formation documents for the acquiring entity and ownership breakdown.

- Target business financials: Business tax returns, profit and loss statements, balance sheets, and interim financials.

- Deal documents: LOI, draft purchase agreement, sources and uses, and details of any seller note.

- Narrative support: A business plan or operating memo explaining the transition, your experience, and the post-close plan.

- Third-party items: Valuation, and any other reports the lender requires during underwriting.

If you're buying a business with seasonality, customer concentration, or uneven recent performance, expect more lender questions. That doesn't mean the deal is impossible. It means the package has to answer those questions before the credit team asks them.

Common Pitfalls That Can Instantly Kill Your Deal

Most failed SBA acquisitions don't blow up in dramatic fashion. They fade out through friction. A weak LOI. Bad seller financials. A seller note that isn't structured to SBA rules. A valuation that comes in light. By the time everyone realizes the issue is fatal, weeks have already been wasted.

The seller note problem

Seller financing is common. Data shows 38% of small business acquisitions involve seller financing, but many deals fail because the SBA 7(a) program requires a seller note to be on standby for a minimum of 2 years if it's used to meet equity requirements.

That's where expectations collide. Buyers assume the seller note solves the down payment issue. Sellers assume they'll still get near-term payments. If the note has to sit on standby, the seller may reject the structure once they understand what they're agreeing to.

This is one of the most overlooked deal-breakers in acquisition lending. Fix it early. If the seller needs immediate liquidity, don't wait until underwriting to surface the standby requirement.

The valuation and financials trap

Another common mistake is treating the asking price like established value. The lender won't do that. If the valuation comes in below the price, the deal has to be restructured, repriced, or supported with more cash.

Messy financials create the same kind of problem. If the seller has inconsistent books, large unexplained add-backs, or weak interim reporting, the lender may stop trusting the cash flow story. Once that happens, approval gets much harder.

Watch for these warning signs:

- Unclear add-backs: If expenses are labeled discretionary but not documented, lenders discount them.

- Incomplete interim data: If the trailing period doesn't match the tax returns, expect questions.

- Working capital blind spots: If the business needs a reserve but the LOI leaves no room for it, the buyer can get squeezed.

- Dormant or unstable operations: Businesses without a solid operating history are much harder to finance as turnkey acquisitions.

If the seller's books require a long verbal explanation, assume the lender will haircut the story.

The legal details buyers rush through

Loan approval is only half the battle. The purchase agreement also has to line up with the financing. I've seen deals delayed because the asset list was vague, the transition support language was thin, or the non-compete terms created confusion about who was staying involved after closing.

This is why good legal review matters. If you want a practical outside reference on avoiding pitfalls in business purchase agreements, that piece is worth reading before you finalize deal documents.

A clean transaction usually has three things: financeable terms, supportable valuation, and documents that don't contradict the credit story. Miss any one of them and the whole file can stall.

Your Next Steps to Secure Acquisition Funding

If you're serious about buying a business, the next move isn't submitting random applications. It's getting your deal ready so the right lender can say yes.

What to do before you talk to lenders

Start with your own side of the file.

- Get your personal financial picture in order: Know where your injection is coming from and document it cleanly.

- Pressure-test the business: Review financials, customer concentration, margins, payroll, lease terms, and transition risk.

- Scrub the LOI: Make sure the purchase structure, seller note terms, and timing all fit an SBA-closeable deal.

Then look at the business through a lender's eyes. Can you explain why you're qualified to run it? Can you defend the price? Can the company support the debt after a conservative underwriting adjustment?

Why experienced guidance changes outcomes

Acquisition lending is technical. A buyer can have a strong target and still lose weeks talking to lenders that were never a fit for the industry, structure, or deal size.

That matters even more on layered transactions. Real-estate-heavy acquisitions, investor-backed deals, and structures involving multiple moving parts all benefit from lenders who know how to manage complexity. The same principle shows up in this piece on financing for complex real estate. The point carries over to business acquisitions. Experience reduces avoidable mistakes.

A strong financing process does three things well. It matches the deal to the right lender, packages the file so underwriting can follow it, and manages the closing path so small issues don't become fatal ones.

If you do that well, an SBA loan to buy a business becomes what it should be. Not a mystery. Not a gamble. Just a structured way to acquire a real company with smart financing and a realistic path to closing.

If you want expert help structuring and closing an SBA acquisition, GoSBA Loans helps buyers compare options across 50+ SBA lenders, package deals for maximum fundability, and manage everything from LOI to closing at no cost to the borrower.