You're probably looking at a deal right now where the purchase price works on paper, but the cash to close doesn't. The seller wants their number. The SBA lender wants a clean, compliant structure. You want to preserve liquidity so the business can breathe after closing.

That's where SBA seller notes become one of the most useful tools in acquisition financing.

Used properly, a seller note can help bridge a valuation gap, reduce the buyer's immediate cash burden, and improve the lender's comfort with the deal. Used poorly, it can break SBA eligibility, distort debt service coverage, or create years of avoidable conflict between buyer and seller. The biggest mistake I see is relying on outdated guidance, especially around standby rules that changed under SBA SOP 50 10 8 effective June 1, 2025.

Table of Contents

- What Is a Seller Note in an SBA Deal

- Why Seller Notes Are Critical for SBA Acquisitions

- The Main Types of SBA Seller Notes

- Understanding SBA Standby Period Rules

- Special Cases Forgivable Notes and Earnouts

- Negotiating the Seller Note and Managing Risk

- Practical Checklists for Your SBA Deal

- Frequently Asked Questions About SBA Seller Notes

What Is a Seller Note in an SBA Deal

A buyer lines up an SBA loan, expects to bring 10 percent down, and then learns the seller note may or may not count toward that injection. That is usually the first real lesson in SBA deal structure. A seller note is not just extra financing. Under SBA rules, especially after the June 2025 SOP update, its terms can change whether the deal closes at 10 percent down or 5 percent down.

The plain-English definition

A seller note is a promissory note from the buyer to the seller for part of the purchase price. Instead of receiving all sale proceeds at closing, the seller agrees to collect a portion over time under written note terms, including interest rate, repayment schedule, maturity, and default remedies.

In an SBA 7(a) business acquisition, that note sits inside the full financing package and has to satisfy both the lender's credit standards and the SBA's rules. The governing rulebook is SBA SOP 50 10 8. If the note is subordinated and put on full standby, it can serve a very specific purpose: helping satisfy part of the buyer's required equity injection.

That distinction matters.

A regular seller note is still seller financing, but it does not automatically count as buyer equity. To get credit toward the injection, the note has to meet the SBA's current standard for full standby, which means no principal and no interest payments are due during the standby period. The old workaround of a 24 month standby no longer does the job for equity treatment under the June 2025 update. Buyers who miss that point often structure the note correctly for cash flow, but incorrectly for SBA eligibility.

What the note does in a real deal

Here is a common example. A business sells for $1,000,000. The lender is willing to finance most of the project, but the structure still requires a buyer injection. The seller agrees to carry $50,000 on full standby, and the buyer brings $50,000 in cash. If the lender accepts that structure under SOP 50 10 8, the buyer gets to a 5 percent cash down acquisition instead of writing a larger check at closing.

Change the note terms, and the result changes too. If the seller note requires monthly interest payments from month one, or comes off standby too early, many lenders will not treat it as injection support. It is still debt. It just is not equity credit.

That is why first-time buyers need to stop viewing the seller note as a side promise between buyer and seller. In an SBA deal, it is part of the underwriting file.

Why each side agrees to it

The seller usually accepts a note for one of three reasons:

- To bridge a financing gap when the lender will not support the full negotiated price

- To widen the buyer pool by making the transaction financeable for qualified operators who do not want to drain all post-close liquidity

- To show confidence in the business during the transition period

The buyer agrees because a properly structured note can reduce cash due at closing and leave more working capital in the business.

The lender likes seller participation because it shows the seller still has financial exposure after closing. That does not make every seller note attractive. A weak business with a seller note is still a weak credit. But in a good deal, seller paper can improve structure and signal conviction.

One practical rule applies in almost every SBA acquisition. If the seller wants top dollar, the buyer should at least ask for seller participation. Terms decide whether that participation helps.

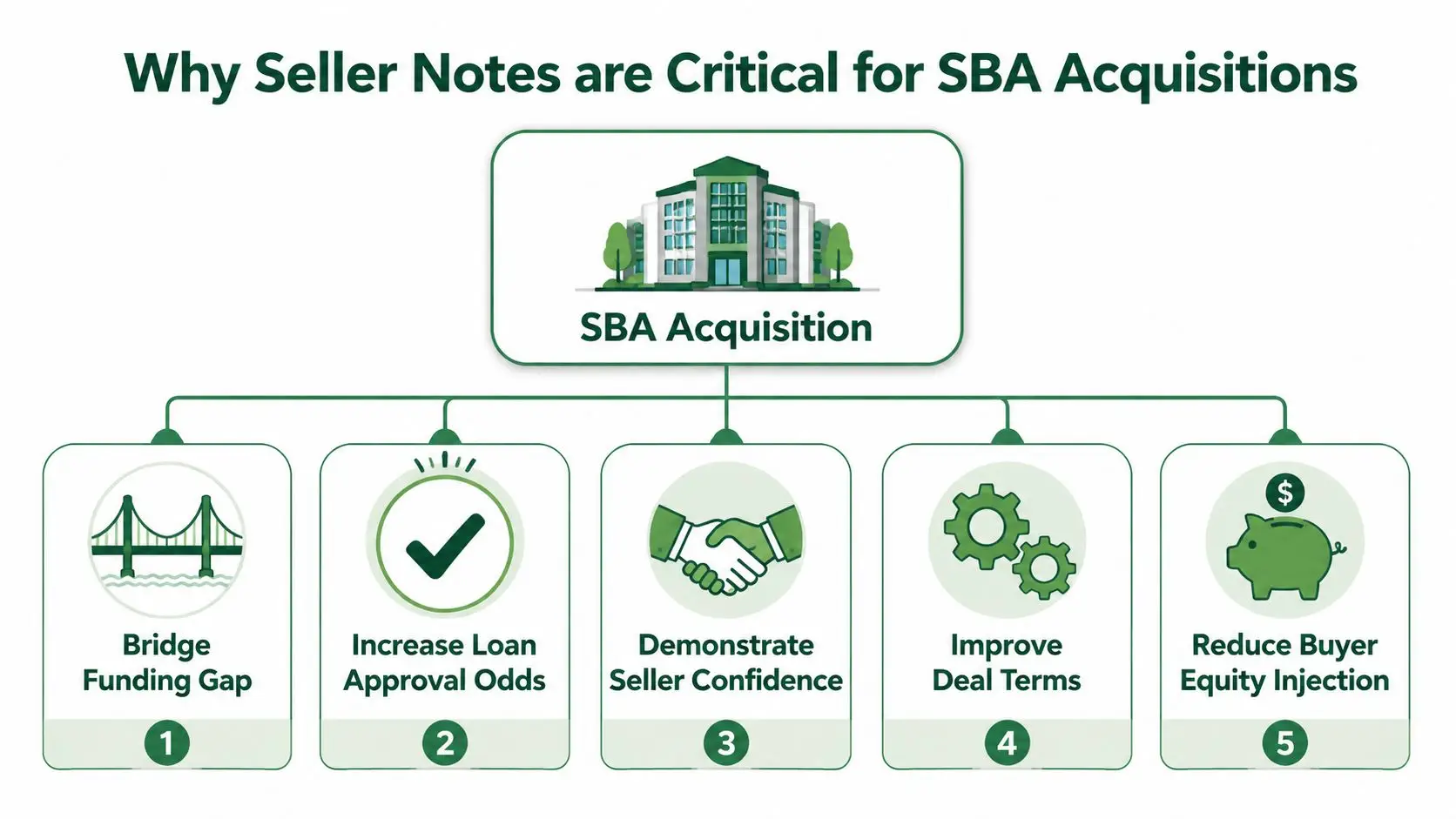

Why Seller Notes Are Critical for SBA Acquisitions

A first-time buyer agrees on a $1.2 million purchase, gets through lender screening, and then hits a core issue. The bank likes the business, but the buyer does not want to drain personal cash to the edge just to satisfy structure. The seller note often solves that problem, or kills the deal if it is drafted the wrong way.

Under SBA SOP 50 10 8, seller paper can do more than fill a pricing gap. A properly structured full standby note can help a buyer reach a 5 percent cash down acquisition. That point matters more after the June 2025 SOP update. The old approach of using a 24 month standby to support equity no longer works for that purpose. If the note is going to count toward the capital stack this way, it has to meet the SBA's full standby requirements.

That changes how buyers should look at seller financing. This is not side paper between buyer and seller. It is part of the loan structure, part of underwriting, and part of the lender's risk analysis.

Where the seller note changes the deal

Seller notes usually matter in five places:

- Closing a structure gap: The lender may support the business, but not every dollar of the negotiated purchase price.

- Reducing cash due at closing: In the right structure, the seller note can lower how much cash the buyer must bring personally.

- Protecting post-close liquidity: Cash left in reserve helps with payroll, inventory, repairs, and the surprises that show up in the first quarter.

- Supporting early cash flow: A note with no required payments during standby puts less strain on debt service coverage in year one.

- Keeping the seller invested in a clean handoff: A seller who still has money at risk usually pays closer attention to transition performance.

The trade-off is simple. Terms that help the buyer often delay the seller's payout and increase the seller's risk.

I see this mistake often. A buyer hears "seller will carry 10 percent" and assumes that solves the equity issue. It does not. If the note requires current payments, has the wrong standby language, or gives the lender too little control, many SBA lenders will treat it as ordinary debt. At that point, the note may still help bridge price, but it does not help the buyer the way they expected.

A practical example

Take a $1 million acquisition. A buyer wants to preserve cash for working capital and the lender agrees the business can support the senior debt. If the seller carries a note on full standby and the documents match SBA requirements, the structure may allow the buyer to close with less cash out of pocket than a standard deal.

If that same note requires interest-only payments from month one, the analysis changes. Now the lender has another debt obligation to underwrite, the buyer's cushion gets thinner, and the note may no longer support the equity structure at all. Running the projected payments through an SBA 7(a) loan calculator with amortization schedule makes that difference obvious fast.

Seller notes also help resolve valuation disputes without forcing one side to give up immediately on headline price. If the seller wants a number the lender will not fully support, part of that price can sit in seller paper instead of in the SBA loan. That does not remove risk. It reallocates it.

A strong acquisition structure leaves the buyer with enough liquidity to operate and enough margin to absorb a bad month. Deals fail after closing for ordinary reasons. Equipment breaks, customers pay late, a manager quits. Seller participation can give the transaction enough breathing room to survive those hits.

Lenders know that too. Real seller carry shows continued confidence in the business, but only if the file still makes sense on cash flow, transition risk, and management depth. A seller note improves a good deal structure. It does not rescue a weak business.

The Main Types of SBA Seller Notes

Not all seller notes do the same job. In SBA business acquisition deals, the structure drives underwriting treatment, standby requirements, and cash flow impact. The three main categories you'll see are full standby, partial standby, and amortizing notes.

Comparison of seller note types in SBA deals

| Feature | Full Standby Note | Partial Standby Note | Amortizing Note |

|---|---|---|---|

| Payment structure | No principal or interest payments during standby period | Some payment allowed, often interest-only or reduced payment structure | Regular monthly payments of principal and interest, or scheduled balloon structure |

| Equity injection eligibility | Can count toward required equity only if it meets SBA requirements | Generally not used to satisfy current SBA equity rules | Generally not used to satisfy current SBA equity rules |

| DSCR treatment | Often favorable because no current seller-note debt service may be counted during underwriting, depending on lender policy | Lender usually underwrites some or all payment burden | Fully counted as debt service |

| Best use case | Reducing buyer cash to close or improving early cash flow | Sharing risk while giving seller some current payment | Spreading purchase price over time when deal cash flow can support it |

| Seller experience | Highest deferral, least current cash flow | Moderate compromise | Most like a traditional financed payout |

Full Standby Seller Note

A full standby seller note means the seller receives no principal and no interest payments during the standby period. In this scenario, for SBA equity injection purposes, the June 2025 rule change becomes critical.

When a seller note is used to satisfy part of the equity injection, it must be on full standby for the life of the loan, and the seller can't enforce the note or collect principal or interest until the SBA loan is fully repaid, according to this SBA seller note discussion. In a typical SBA acquisition, that can mean the seller receives nothing on that note for the full loan term.

This is why lenders like it. From an underwriting standpoint, a true full-standby note removes near-term payment pressure from the business. In many deals, lenders also view it as a strong sign that the seller believes the business can support the transaction.

How it affects DSCR

When a seller note stays on full standby for the required period under a lender's policy, many lenders don't include payments on that note in the DSCR calculation during underwriting. That can materially improve cash flow coverage.

Some lenders may treat a full-standby note favorably if standby lasts long enough under their credit policy. Others will want a longer deferral before excluding payments. That's a lender overlay issue, not a universal SBA rule.

A practical example helps. If the operating business already has tight cash flow under the senior SBA debt, adding a monthly seller-note payment can weaken coverage. If that same note is on full standby, underwriters may look only at the senior debt burden during the standby period. That can turn a marginal file into an approvable one.

Partial Standby Seller Note

A partial standby seller note is a middle ground. The seller might receive interest-only payments, reduced payments, or deferred principal while some current payment still flows.

This structure can work when the seller wants continuing income and the buyer needs some flexibility, but it doesn't deliver the same underwriting benefit as full standby. Because money is still going out the door, lenders usually account for that obligation when analyzing repayment ability.

Partial standby makes sense when:

- The seller insists on current income: Some sellers won't agree to years of zero cash flow.

- The business has enough cushion: If cash flow is comfortably above required debt service, a limited seller payment may still fit.

- The note isn't being used for equity treatment: In that case, the negotiation can focus more on economics than on SBA injection rules.

The mistake here is assuming “some standby” equals “SBA-compliant standby.” It doesn't. Partial deferral may be useful economically, but it's different from the full-standby standard tied to equity treatment.

Amortizing Seller Note

An amortizing seller note works like a conventional loan between seller and buyer. The buyer makes scheduled monthly payments, and the note may fully amortize or end in a balloon.

Common structures include:

- 5-year amortization

- 10-year amortization

- 20-year amortization

- 25-year amortization

- 30-year amortization

- Balloon structures

Longer amortization lowers monthly debt service. Shorter amortization increases it. Balloon structures can reduce current payments but create a refinance or payoff event later.

For underwriting, this type of note usually has the clearest impact. If the buyer owes monthly payments, the lender will usually evaluate how those payments affect debt service and post-closing cash flow. That's where modeling matters. If you want to see how payment timing changes the deal, an SBA 7(a) loan calculator with amortization schedule is useful for comparing payment burdens across different structures.

The note that feels easiest to negotiate isn't always the note that gets through credit.

A five-year seller note can look reasonable in a letter of intent and still create too much monthly drag once the SBA payment, working capital needs, and transition costs are added. By contrast, a longer amortization or a balloon may preserve early cash flow, though it shifts more risk to the seller.

Understanding SBA Standby Period Rules

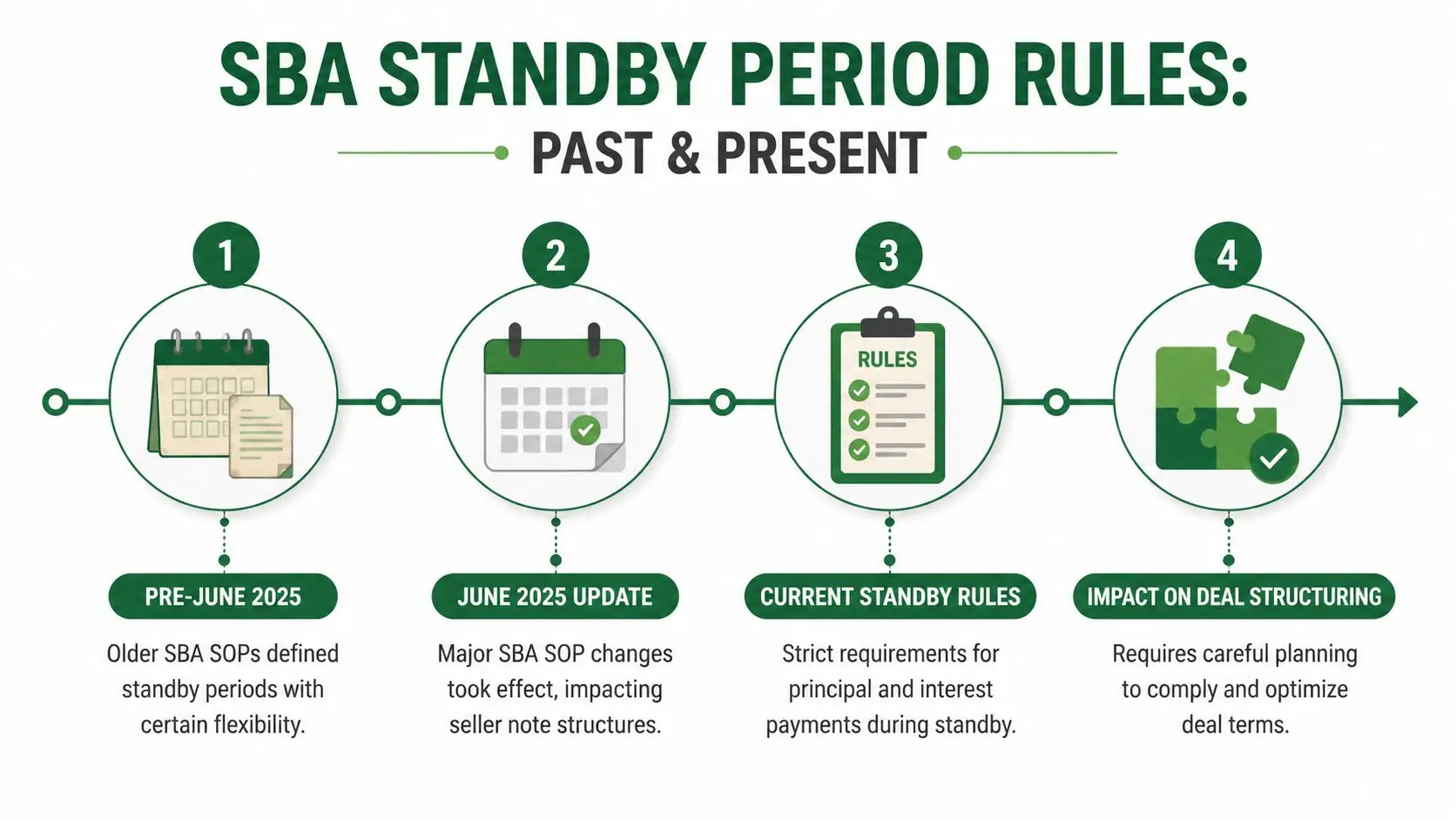

The most misunderstood issue in SBA seller financing right now is standby. A lot of online advice still refers to the old rule. That advice is outdated for current equity injection treatment.

What standby actually means

A seller note on standby means the seller's rights are subordinated to the SBA lender's rights. In practical terms, the seller waits. The seller doesn't get paid until the terms of the standby agreement allow it, and the lender remains in the senior position.

Under SBA SOP 50 10 8, standby isn't just a casual side letter. It has to be documented correctly. If the note is meant to count toward required buyer equity, the terms have to satisfy the SBA's standard, not just the preferences of the buyer and seller.

The June 2025 rule change that matters

Before June 1, 2025, sellers could defer payments for 24 months and then resume principal and interest. That older structure is what many buyers, sellers, and even some advisors still have in mind. After the rule update, that approach no longer works for equity injection treatment.

The current rule is this: to count toward equity, the seller note must be on full standby for the entire life of the SBA loan, typically 10 years, and it can only cover up to 5% of total project cost, as explained in this June 2025 SBA standby update.

That's the key clarification most articles miss. A 24-month standby may still be discussed in older material, but it no longer lets a seller-financed note satisfy the full required equity position.

Later in the process, it helps to hear the mechanics explained visually:

Why lender policy still matters

Here's where buyers get tripped up. The SBA rule and the lender's credit policy are not the same thing.

A lender may say a seller note won't hurt DSCR if it stays on full standby for a certain period under that bank's underwriting approach. Some lenders may exclude those payments from DSCR if the note remains on full standby for three years. Others want five years. That's a lender overlay. It isn't a universal SBA rule, and it doesn't replace the SBA requirement for equity injection treatment.

So ask two separate questions:

- Does this note satisfy SBA rules for equity injection?

- How will this lender treat the note in DSCR underwriting?

Those are different issues. The cleanest deals answer both before the LOI is final.

Special Cases Forgivable Notes and Earnouts

A buyer and seller agree on price, the SBA lender is comfortable, and then someone adds a side payment tied to post-close performance. That is one of the fastest ways to turn a workable SBA deal into a compliance problem.

Labels cause a lot of the confusion. Sellers call it a forgivable note, transition bonus, retention payment, rollover piece, or earnout. Under SBA review, the label matters less than the economics. The lender and closing counsel will look at what the payment does, who controls it, and whether it depends on future business results.

When a forgivable note shows up

A forgivable seller note usually is not true seller financing in the normal SBA sense. In practice, it often acts more like compensation for transition help or an incentive for the seller to stay involved after closing.

A common example is a seller who agrees to train the buyer for six months, introduce key referral sources, or help maintain a license or customer relationship, with part of the amount reduced or forgiven if those services are completed. That can be reasonable from a business standpoint. It also creates extra legal and underwriting work because the parties need to separate purchase price from employment or consulting compensation.

That distinction matters. If a payment is really compensation, the lender may not treat it like a seller note at all. If it is tied too closely to future operations, it can start to look like a prohibited contingent payment structure.

I tell buyers to ask three direct questions before they agree to any “forgivable” language:

- Is this payment part of the purchase price, or is it compensation for post-close work?

- Is forgiveness based on services rendered, or on business performance after closing?

- Will lender counsel and closing counsel describe it the same way in the loan file?

If those answers are fuzzy, the structure usually needs to be simplified.

Tax treatment also needs its own review. A buyer may want a deduction. A seller may want capital gains treatment. Those goals often point in different directions, and the legal documents need to match the intended tax treatment.

Why earnouts create problems in SBA 7(a) deals

Under current SBA rules, earnouts are the problem area. SOP 50 10 8 requires the change of ownership purchase price to be established and supported, and SBA 7(a) loans are not built for open-ended, contingent purchase price formulas based on future revenue, profit, or retention targets.

That is why performance-based payouts create trouble. In a conventional acquisition, an earnout can bridge a valuation gap. In an SBA 7(a) acquisition, it usually creates a structure the lender cannot close.

For example, if a seller says, “Pay me $200,000 at closing and another $100,000 if revenue stays above target for 12 months,” that second payment is an earnout. An SBA lender will usually reject it. If the seller instead carries a properly documented seller note with fixed terms, the deal has a path. Whether that note helps with equity injection is a separate question governed by the current standby rules, including the June 2025 update discussed earlier.

The practical rule is simple. If the seller's future payment rises or falls based on how the business performs after closing, treat it as a red flag until SBA counsel and the lender clear it. If you want a closer look at the issue, this guide to SBA loan earnout rules explains why these structures often fail in underwriting.

Clean deals close faster. In this part of the process, fixed price and fixed terms beat creativity.

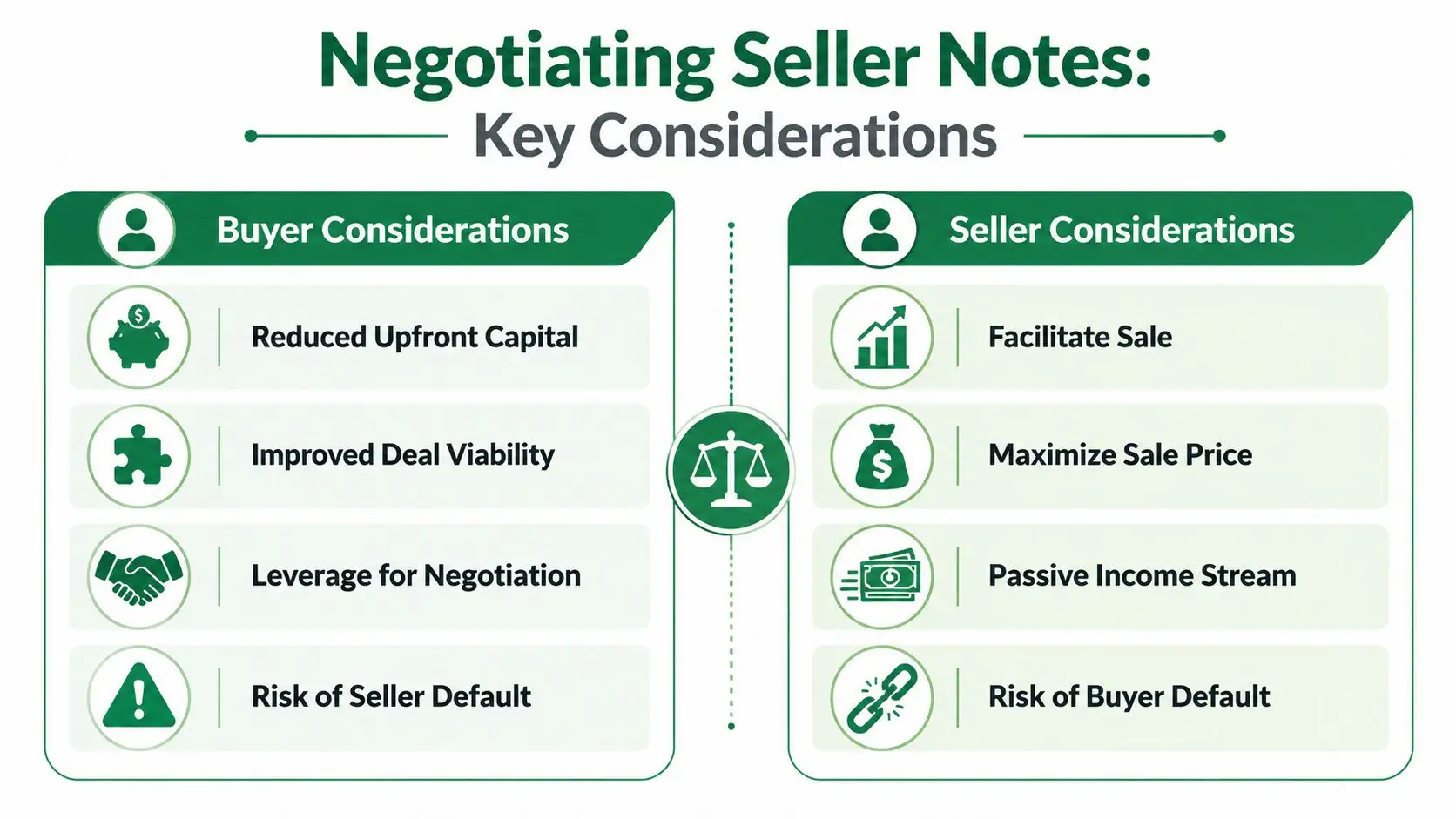

Negotiating the Seller Note and Managing Risk

A buyer and seller can agree on price, survive diligence, and still lose the deal over one page of seller note terms.

That happens all the time. The note looks simple until the lender asks whether it counts toward equity, whether payments hit cash flow too early, and whether the default language conflicts with SBA requirements under SOP 50 10 8. Since the June 2025 update, that review got tighter. A 24 month standby no longer gets a seller note counted toward the buyer's injection. If the structure is supposed to help a buyer get to a 5% cash down deal, the note has to be a true full standby note that meets the lender's documentation standards.

What buyers should push for

Buyers need terms that work after closing, not just at signing.

Start with the purpose of the note. If it is meant to reduce the buyer's cash injection, the language has to be precise. The seller cannot receive principal or interest during the standby period, and the lender will want the standby terms documented clearly in the note or in a separate standby agreement. If the note is not on full standby, treat it as ordinary seller debt and underwrite the business with that payment in mind.

A simple example shows the difference. Suppose the purchase price is $1 million. The buyer wants to put in 5% cash, and the seller is willing to carry another 5%. Under the current SOP framework, that seller note only helps the equity stack if it is on full standby for the required period under the lender's interpretation of SOP 50 10 8 and closing documents. If the seller expects monthly interest starting in year one, the buyer usually needs to bring in more cash because the note no longer functions as injection support.

Buyers should also press for terms that protect post-close liquidity:

- Clear standby language: If the note is part of the equity structure, the drafting has to match what the SBA lender will approve.

- Fixed terms: Fixed principal, fixed interest, and fixed maturity are easier to underwrite than side letters, consulting fees, or contingent payment language.

- Payment timing that fits cash flow: A note that looks reasonable on paper can strain working capital in the first slow quarter.

- Default provisions that match reality: Cure periods, notice requirements, and remedies should be specific enough to avoid a fight if performance dips.

Interest rate and amortization are negotiated points, not boilerplate. Better businesses with stable cash flow can support tighter pricing. Riskier deals usually get a higher rate, longer interest-only periods, or both. The lender may still haircut the structure if debt service coverage is thin.

What sellers should protect

A seller carrying paper is making a credit decision on the buyer.

If the note is on full standby and used to support the buyer's injection, the seller is giving up near-term payment rights in exchange for getting the deal closed. That trade-off can make sense, but sellers should price it consciously. A seller who accepts standby should understand how long repayment may be blocked, what events end the standby, and whether any refinance or prepayment restrictions affect timing.

Collateral is another point of confusion. Sellers often ask for a junior lien or UCC filing. Sometimes that is possible, but only if the senior lender permits it and the intercreditor terms do not conflict with the SBA loan documents. In practice, the seller remains behind the bank. If there is a default and the collateral is liquidated, the senior lender gets paid first.

Sellers should underwrite the buyer with the same discipline they used to build the business. Review the buyer's resume, post-close operator, liquidity after closing, and transition plan. If customer relationships still depend heavily on the owner, the seller should also think about continuity risk. In some deals, that is where an essential business life insurance guide becomes relevant to protect the company during the handoff.

Terms that deserve real negotiation

Three terms cause more trouble than buyers expect.

First, prepayment. Buyers want the right to pay the seller off early once cash flow improves or the business refinances. Sellers often want a minimum return. That can be solved with a short prepayment protection period or a modest premium, but it should be discussed before the LOI turns into documents.

Second, subordination language. Sellers sometimes agree in principle to subordinate, then resist the actual language once counsel explains how limited their remedies become during a default. Get that language in front of both sides early.

Third, seller involvement after closing. If the seller is staying on for training, sales introductions, or a transition period, define the role clearly and keep compensation separate from purchase price mechanics. Blending those items together creates confusion for underwriting and for taxes.

For a broader look at how these structures are set up in practice, this seller financing for business acquisition guide is a useful companion.

A clean seller note does two jobs. It gets through underwriting, and it still makes sense six months after closing when the buyer is making payroll and the seller is waiting to be repaid.

Practical Checklists for Your SBA Deal

A clean SBA acquisition usually comes down to preparation. The buyer, seller, and broker each have a short list of things they need to get right before the file reaches underwriting.

Buyer checklist

- Confirm the note's purpose: Decide whether the seller note is meant to support equity injection, bridge valuation, improve cash flow, or some combination.

- Model post-close payments: Run the SBA debt, seller note, and working capital together. Don't review them in isolation.

- Check lender treatment early: Ask how the lender will view standby, DSCR, and subordination before finalizing deal terms.

- Draft the LOI carefully: Put core seller-financing terms in the LOI so the parties don't renegotiate them during underwriting.

- Protect key risks: If the seller is central to relationships or operations, think through transition support, non-competes, and whether a resource like this essential business life insurance guide is relevant to the business continuity plan.

Seller checklist

- Know your standby tolerance: Be honest about whether you're willing to accept zero cash flow on a note for an extended period.

- Review the buyer as a credit risk: The buyer's plan and ability matter more than verbal confidence.

- Negotiate protections: Consider subordination language, documentation quality, and any lien or UCC rights that are allowed within the lender's structure.

- Separate transition pay from purchase price: Employment and consulting arrangements should be documented cleanly.

- Use experienced counsel: DIY note language causes expensive problems later.

Broker checklist

- Set expectations early: Many parties still believe outdated standby rules apply.

- Screen for structure fit: If the seller won't accept standby and the buyer can't increase cash, the deal may need a different capital stack.

- Present the note clearly to lenders: Spell out whether it's full standby, partial standby, or amortizing, and how it interacts with cash flow.

- Coordinate documents: LOI, note, standby agreement, and purchase agreement should all tell the same story.

- Watch for prohibited concepts: If someone starts describing a future performance payment, pause and verify it doesn't cross into noncompliant territory.

Frequently Asked Questions About SBA Seller Notes

A common June 2025 problem looks like this. A buyer shows up expecting to put 5% down, the seller agrees to carry another 5%, and everyone assumes a 24 month standby solves it. Under SBA SOP 50 10 8, that structure no longer works if the seller note is being used to satisfy part of the required equity injection.

Can a seller note count toward the SBA equity injection

Yes, but only in a narrow set of circumstances.

For a change of ownership loan, a seller note can support a reduced buyer cash injection only if the note is on full standby for the life of the SBA loan and requires no principal or interest payments during that period. In plain English, if the buyer is trying to get into the deal with 5% cash instead of the full required injection, the seller note has to sit completely dormant until the SBA loan is paid in full. The SBA publishes that rule in SOP 50 10 8, which lenders now apply to post-June 2025 approvals. See the current SBA SOP library here: SBA SOP 50 10.

That is the rule many buyers and sellers still miss. A 24 month standby may still appear in other contexts, but it does not let the seller note count as equity injection under the current ownership-change standard.

What happens if the buyer defaults

The SBA lender is almost always in the senior position, and the seller is behind that lender if the note is subordinated, which it usually is.

In a default, the lender controls the workout. If collateral is liquidated, the senior lender gets paid first from available proceeds. The seller may recover little or nothing, especially if the business value dropped after closing. I tell sellers to underwrite the buyer the same way a lender would. If the business cannot support the senior debt comfortably, the seller note is exposed even if the documents are drafted well.

Can a full-standby note be paid early

Sometimes, but only if the lender approves it and the loan documents allow it.

Do not assume early payoff is available just because the business performs well. With a true full-standby note that is being credited toward equity injection, the lender will usually expect the standby terms to stay in place unless there is a refinance, a sale, or another lender-approved event. If a seller is agreeing to full standby, that seller should price the risk with the actual payment delay in mind.

What about taxes

The tax treatment depends on the structure of the deal and the character of each payment stream.

A seller note is not taxed the same way as payroll, consulting fees, or a post-close bonus. That matters in deals where the seller is staying on for training, receiving a separate employment package, or discussing some form of contingent payment. If the parties blur those items together, they can create both tax problems and SBA compliance problems. The clean approach is to document each piece of compensation for what it is and have tax counsel or a CPA review it before signing.

Are earnouts or forgivable seller notes allowed in SBA deals

They need extra care.

A payment tied to future performance can create problems if it starts to look like an earnout that the lender cannot underwrite cleanly or that conflicts with SBA rules on change-of-ownership financing. A "forgivable note" also needs to be handled carefully because the lender will want to know whether it is really debt, really purchase-price consideration, or something else entirely. If a seller wants upside after closing, the structure has to be reviewed early, not the week before closing.

If you're evaluating an acquisition and need help structuring seller financing that works with today's SBA rules, GoSBA Loans can help you compare lender options, pressure-test the note structure, and avoid the standby and underwriting mistakes that derail deals late in the process.