SBA Real Estate Loans For Commercial Real Estate.

Our SBA 7(a) or SBA 504 loans – are the perfect choice for business owners looking to purchase commercial real estate or refinancing their existing loans. Our real estate SBA loans make it easy to buy office space, retail space and commercial buildings. Save money on rent, earn tax deductions and build your business net worth, while putting as little as 10% down. We are one of the very few services that can offer fixed rate financing for SBA 7(a) these loans.

- Purchase land, renovate buildings & refinance debt

- Competitive fixed rates starting at 6.3% APR

- Loan amounts up to $5M (SBA 7a) or $13M (SBA 504)

- 25 year fully amortizing loans

- 100% free service for borrowers.

We Make Small Business Loans Easier, Faster, And Affordable.

Experience fast, hassle-free funding tailored to your business needs with our efficient four-step process.

Step 1: Contact Us

Chat with our team about your financing needs and start the process.

Step 2: Multiple Lenders

We take your file to multiple lenders and get multiple term sheets.

Step 3: Choose Lender

Choose the term sheet with the best terms and rates. When lenders compete, you win!

Step 4: Loan Funding

Our team will assist you with the loan closing and any questions the lender might have.

SBA Loans For Real Estate.

- Purchase land, renovate buildings & refinance debt

- Competitive fixed rates starting at 6.3%

- Loan amounts up to $5M (SBA 7a) or $10M (SBA 504)

- Terms up to 25 years for real estate

- Low 10% down payment, 90% loan to value (LTV)

SBA 7(a) Real Estate Loan Requirements & Highlights.

To qualify for our SBA 7(a) Real Estate Loan, your business should meet the following requirements:

- Fixed rates starting at 6%

- Long amortizing terms of 25 years

- 10% downpayment, but 100% financing possible in some cases

- Minimum Debt Service Coverage Ratio (DSCR) of 1x

- Business must occupy 51% or more of the square footage

- Minimum annual profit of $100,000

- Minimum 3 years of operating history

- Decent to good personal credit

SBA 504 Real Estate Loan Requirements & Highlights.

The SBA 504 Loan is a small business mortgage loan program for “owner occupied” business real estate with a 2 loan structure that includes a first mortgage that can be fixed or adjustable and a 20 or 25 year fixed rate 2nd mortgage.

- Long-term, fixed rate financing for real estate & fixed asset

- 2-Loan structure: 50% first mortgage & 40% SBA CDC second

- 10% downpayment for most loans

- Fixed rates starting at 5.82% (lower than 7(a) loans)

- Loan amounts up to $11.25M or larger for "green" projects

- Business must occupy 51% or more of the square footage

- Suited for larger businesses with minimum profit of $500,000

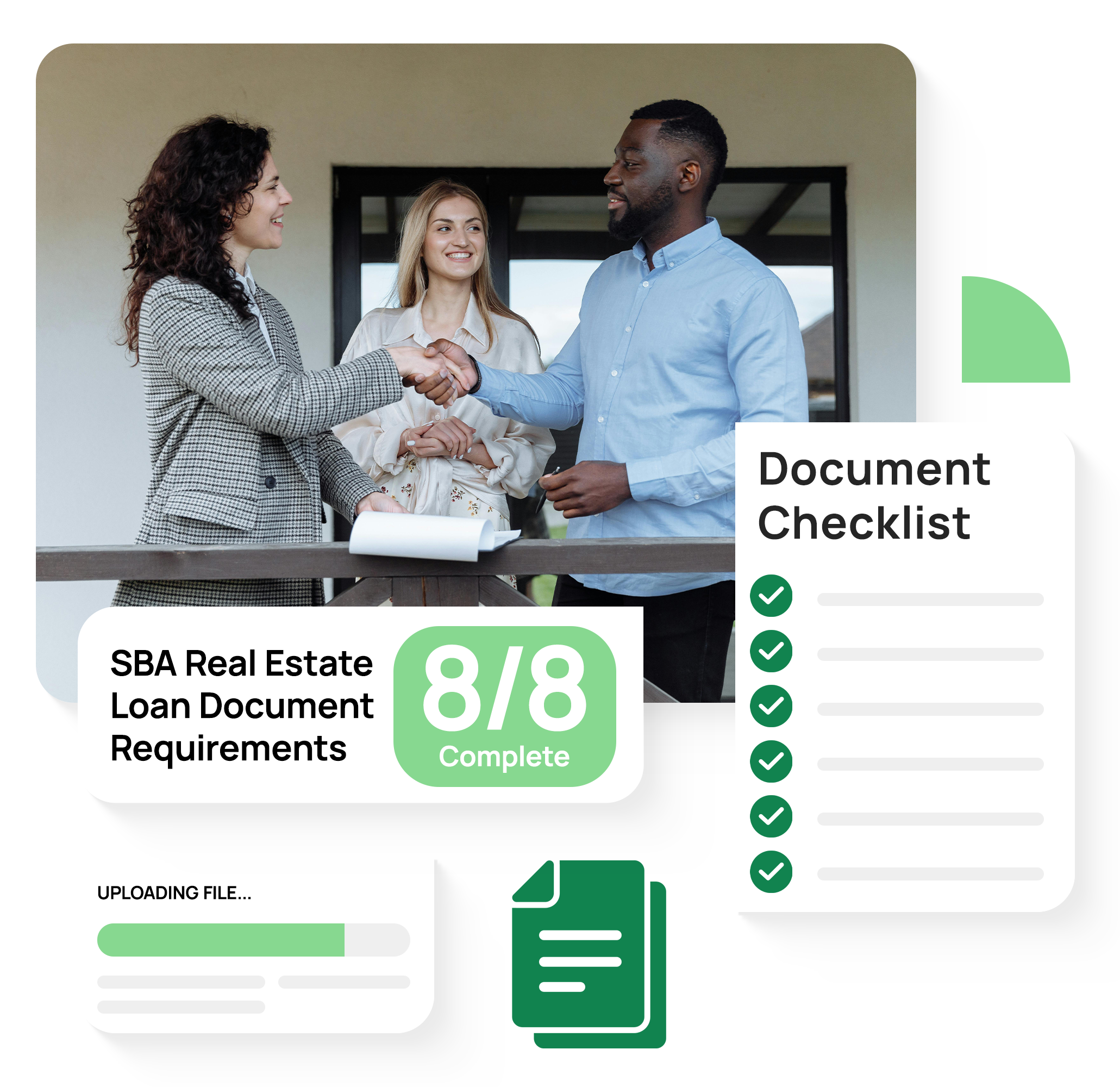

SBA Real Estate Loan Document Requirements.

- Signed real estate purchase agreement

- 3 years of business tax returns

- 3 years of personal tax returns

- Articles of organization or incorporation

- Current business debt schedule

- Year to date income statement and balance sheet

- Business bank statements for the last 3 months

Get funded at the best Rate & Terms.

Take advantage of our extensive network of 100+ funding partners. We understand the underwriting criteria and lending preferences of each bank. When lenders compete for your business, you win, save time and get better rates.

- Simple, hassle-free application

- Get funded at the best term & rate

- Get matched with the right lender

- Get multiple loan offers fast

- Special volume discounts not available to public

100% Free SBA Loan Service.

We are a 100% free success based SBA loan consultant that can help you find the best lender for your deal. We get paid by the SBA lender after closing, not by you the borrower.

- All your questions answered

- Get your loan package ready

- Get matched with the right lender

- Expert SBA loan help

- Get funded at the best terms and rate

- Fast and streamlined process

- 100% free service to borrowers

Best Rate & Terms Guaranteed.

When Lenders Compete, You Win!

Join the thousands of businesses that trust us with their SBA financing needs. Leave the heavy lifting to us, you’re in good hands.

SBA loan amount funded in 2025

Total SBA loans funded in 2025

Average time saved per loan

Average yearly interest saved

We'd love to hear from you.

At least three years of operating history and a minimum of $250K revenue is required. Have questions? We are only a call or email away.