You've probably had the same thought most first-time buyers have. The target looks right, the seller sounds reasonable, the broker says the business is “solid,” and the numbers seem good enough at first glance. Then the detailed work begins. Valuation gets murky, lender questions get technical, legal drafts get dense, and one loose assumption can put the whole deal at risk.

That's where business acquisition consulting matters. Not as a vague strategic service, but as practical deal execution. A good advisor helps you decide what to buy, what to pay, how to structure it, what to verify before closing, and whether the deal can survive SBA underwriting. General M&A advice often stops at the LOI. Buyers need more than that. They need someone who understands how transaction mechanics, due diligence, and SBA loan rules collide in practice.

The market reflects how important that role has become. The global M&A consulting services market is valued at about $50 billion in 2025 and is projected to grow at a 7% CAGR to roughly $85 billion by 2033 according to Data Insights Market's M&A consulting services report. That growth tracks with what buyers already feel on the ground. Deals are harder to evaluate, financing standards are tighter, and execution quality matters more than enthusiasm.

Table of Contents

- Why You Need a Guide for Buying a Business

- Core Services of an Acquisition Consultant

- Navigating the Business Acquisition Process

- How SBA Loans and Consulting Work Together

- Finding the Right Consultant and Understanding Costs

- Avoiding Costly Mistakes in Your Acquisition

- An Actionable Checklist for Business Buyers

Why You Need a Guide for Buying a Business

A first-time buyer usually enters the process with confidence and loses it somewhere between the teaser and the lender package.

One week you're reviewing a business that looks like a clean fit. The next week you're trying to make sense of add-backs, lease assignment language, working capital expectations, seller notes, and lender requests for documents you didn't know existed. Nothing about that is unusual. Buying a business is part financial analysis, part negotiation, part legal process, and part operational transition.

That's why business acquisition consulting works best when it acts like a co-pilot, not a cheerleader. The right advisor doesn't just tell you a business is attractive. They pressure-test your assumptions before you wire a deposit, sign a purchase agreement, or commit your personal liquidity to a down payment.

What overwhelms buyers first

The stress usually comes from three places at once:

- Price uncertainty: You need to know whether the asking price reflects earning power, risk, and realistic transferability.

- Execution risk: The seller's story, the books, the contracts, and the lender's requirements all need to line up.

- Post-closing reality: Owning the business on paper is one thing. Running it the day after closing is another.

A buyer may think the hardest part is finding a good target. Often that's the easiest part. The harder part is keeping discipline once emotions attach to a specific deal.

Practical rule: The deal isn't “good” because the business is attractive. It's good only if the price, structure, financing, and transition plan all work together.

Where consultants actually earn their keep

The value isn't abstract. An acquisition consultant helps stop common first-time buyer mistakes before they become expensive. They ask better questions during diligence. They coordinate with the CPA, attorney, broker, and lender. They translate a broad goal like “buy a stable business” into concrete filters, documented risks, and a workable closing path.

Without that guidance, buyers tend to overfocus on upside and underweight mechanics. The mechanics are what close the deal, satisfy the lender, and protect you after the seller leaves.

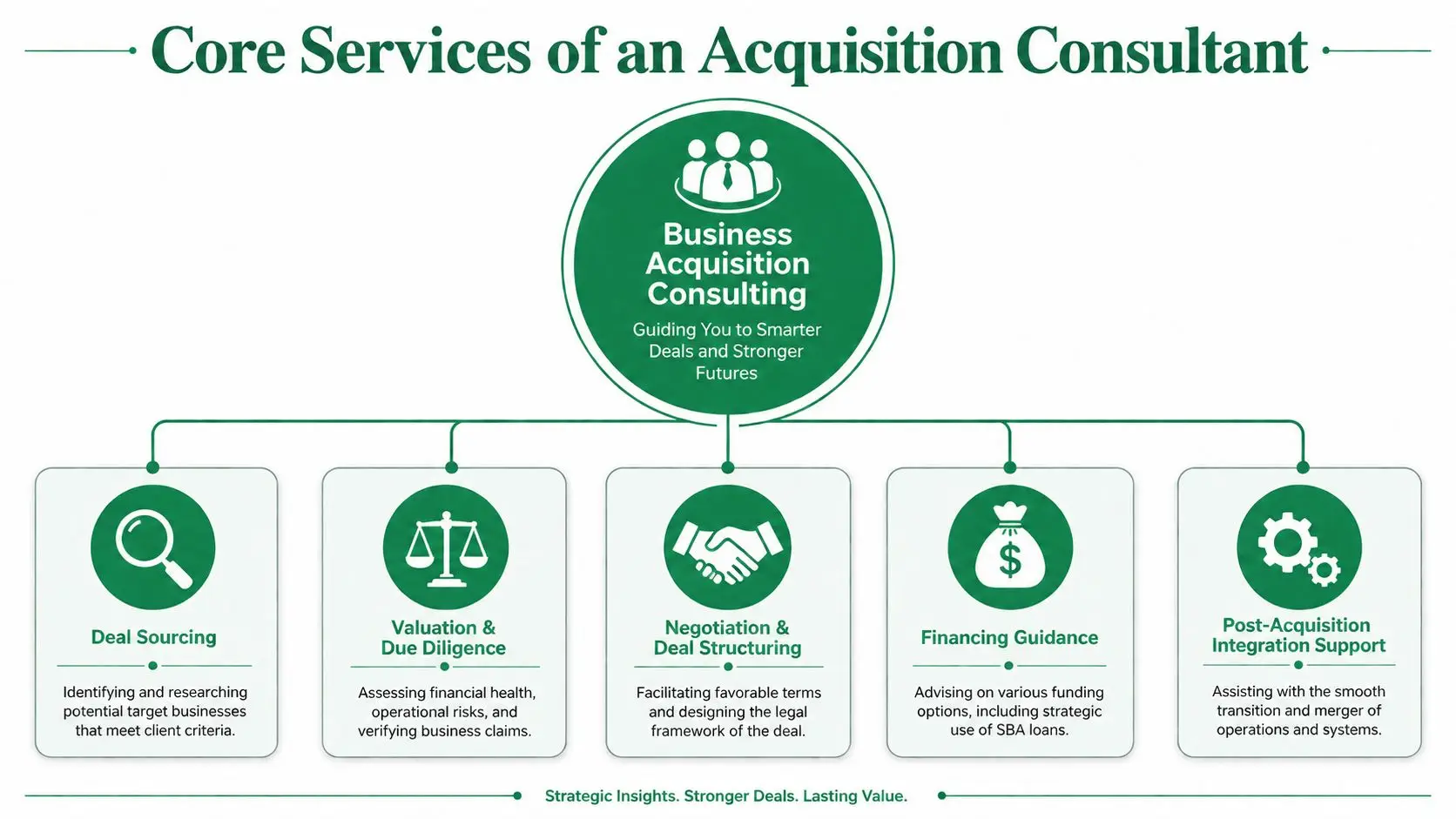

Core Services of an Acquisition Consultant

The consultant as your deal general contractor

The simplest way to understand business acquisition consulting is to think of the consultant as the general contractor for your deal. You still need a lawyer, a CPA, and a lender. In some deals you may also need an industry specialist, quality-of-earnings support, or operational diligence help. But someone has to keep those moving parts aligned.

When buyers don't have that quarterback, specialists work in silos. The attorney comments on contracts. The CPA reviews financials. The lender asks for cash flow support. Nobody owns the full picture. That's how avoidable issues survive into closing.

What each core service actually does

Deal sourcing

This starts before any NDA is signed. A strong consultant helps define target criteria that are specific enough to screen out weak opportunities. That includes industry fit, transferability, customer concentration concerns, seller involvement, and what kind of transition support the business will need.

Good sourcing is less about volume and more about fit. If your background doesn't match a business model, or if the company depends too heavily on the owner's relationships, that matters as much as the headline earnings.

Valuation and due diligence

Buyers need technical discipline. In business acquisition consulting, valuation benchmarks are anchored on industry-specific EBITDA multiples and price-to-earnings ratios, while DCF analysis projects future cash flows using a risk-adjusted discount rate and Comparable Company Analysis looks at market-based multiples such as EV/EBITDA from peer firms to avoid overpaying, as outlined in Aaron Hall's acquisition valuation benchmark guide.

That sounds straightforward until you apply it to a real small-business acquisition. Add-backs may be defensible or aggressive. Revenue may be recurring in appearance but fragile in practice. A consultant's job is to separate transferable earnings from seller-specific earnings.

A disciplined buyer also needs a scorecard. Practical playbooks recommend focusing executive attention on 10 to 15 top-level strategic and financial metrics, supported by 30 to 50 operational metrics to monitor synergy and risk realization, as discussed in that same valuation guide. That matters most when you're buying a company you plan to improve rather than holding it as is.

Negotiation and deal structuring

Price matters, but structure often matters more. A consultant helps shape the LOI, seller transition period, working capital treatment, training obligations, exclusivity terms, and how risks are allocated in the purchase agreement.

A buyer who “wins” on headline price can still lose badly on terms. If accounts receivable are weak, if a key contract isn't assignable, or if the seller exits too fast, a lower price won't save the deal.

Financing guidance

Many general advisors demonstrate a lack of depth here. Financing guidance means testing whether the transaction is likely to satisfy lender standards before you get deep into legal spend. It also means organizing the package the lender will underwrite, not just the story the broker wants to tell.

Post-acquisition integration support

Closing isn't the finish line. It's the handoff. Consultants who understand transition planning help map the first months of ownership, including who communicates with staff, customers, vendors, and key managers, and what systems or reporting changes should wait until operations are stable.

Buyers often underestimate transition strain. The business may keep operating, but cash flow can wobble quickly when staff uncertainty, customer churn, or process changes hit all at once.

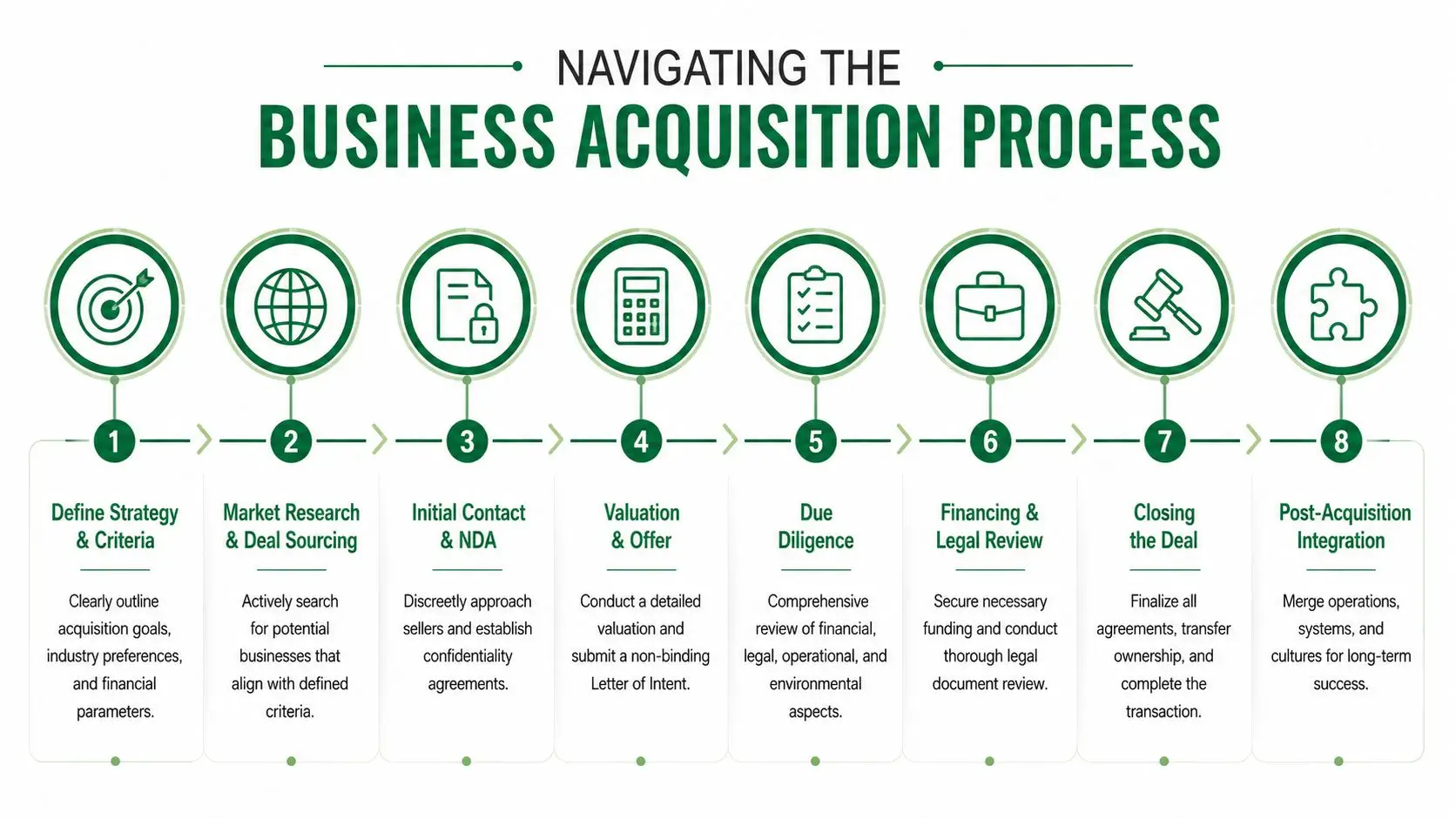

Navigating the Business Acquisition Process

A business purchase feels chaotic when you see it as one giant event. It becomes manageable when you break it into stages with clear priorities.

Strategy and search

Start with fit, not listings. Buyers who begin by browsing everything on the market usually waste time on businesses they shouldn't buy.

At this stage, the most important work is defining:

- Your acquisition criteria: industry, size, geography, owner role, and risk tolerance

- Your personal constraints: liquidity, guarantor strength, experience, and timeline

- Your financing lane: whether the deal is likely to work with conventional financing, SBA financing, or a more bespoke capital stack

A consultant's role here is mostly filtering and pattern recognition. They help you eliminate businesses that look good in a summary but won't hold up once you inspect customer concentration, owner dependence, or cash conversion.

LOI and due diligence

Once a target survives initial review, the process gets more document-heavy and much less forgiving.

The LOI should set expectations on price, structure, diligence access, timeline, and seller participation. It doesn't need to solve every issue, but it should prevent major misunderstandings from surfacing after both sides have spent time and money.

During diligence, the buyer needs to validate earnings, contracts, payroll, tax history, legal exposure, and operational dependencies. If SBA financing is involved, the standards get even more specific. For SBA 7(a) loans above $350,000 involving a change of ownership, lenders require three years of seller business tax returns and financial statements, interim financials dated within 120 days, and a detailed purchase agreement allocating the purchase price and documenting any seller financing terms, as outlined in this SBA documentation checklist for business buyers.

For buyers trying to understand how those stages connect in practice, this LOI to closing SBA acquisition timeline is a useful reference point.

A practical diligence lens

Not every risk sits in the financial statements. Look closely at:

- Revenue durability: Are customers tied to the company or to the owner?

- Labor dependence: Can the business operate if one manager or producer leaves?

- Contract transferability: Will key leases, clients, and vendor agreements survive closing?

- Cash flow quality: Do reported profits translate into debt service capacity?

Financing legal documentation and closing

This phase is where momentum can either carry the deal through or expose problems that should have been surfaced earlier.

The consultant's role shifts toward coordination. Lenders want a clean narrative supported by complete financials. Attorneys need commercial terms translated accurately into deal documents. The buyer needs to keep the process moving without making casual concessions that create trouble later.

A good closing process includes a few habits:

| Focus area | What needs to happen |

|---|---|

| Purchase agreement | Economic terms, assumed liabilities, and seller note treatment must match what the lender is underwriting |

| Lender package | Financials, projections if needed, and source-of-funds documentation must be organized and current |

| Transition plan | Employee, customer, and vendor communication needs to be thought through before closing day |

The final stretch is less about brilliance and more about consistency. Deals close when the facts, the structure, the documents, and the financing package all tell the same story.

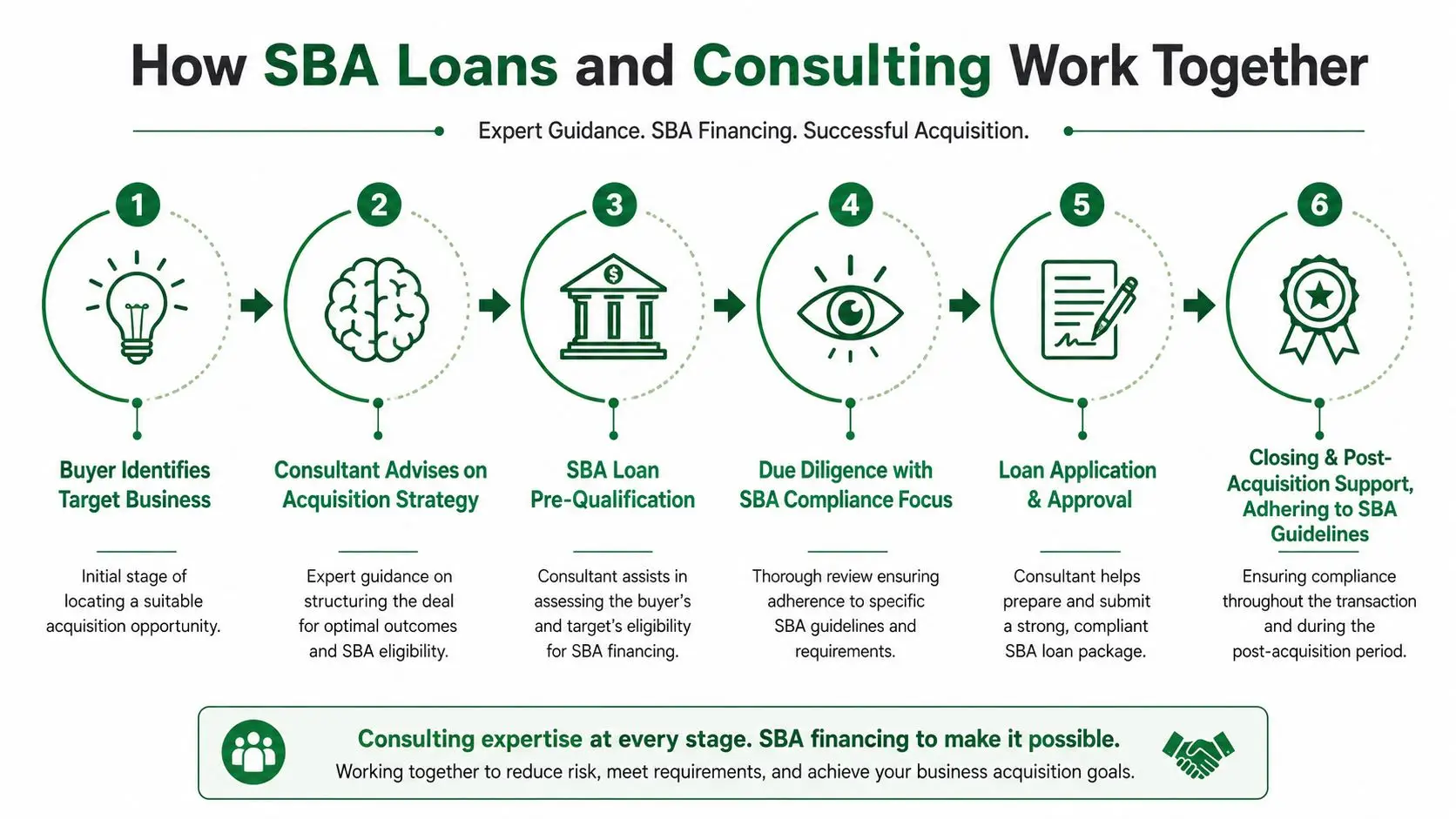

How SBA Loans and Consulting Work Together

It is at this stage that a lot of business acquisition consulting either becomes highly valuable or clearly inadequate.

A consultant who understands SBA lending doesn't just analyze the target. They shape the transaction so it has a realistic path through underwriting. That means thinking about buyer equity, debt service capacity, documentation, structure, and lender expectations before the deal terms harden.

Fundable deals are structured differently

Under SBA SOP 50 10 8, effective June 1, 2025, there is a hard 10% equity injection floor for complete changes of ownership, calculated on total project costs including purchase price, fees, and working capital. On a $1 million acquisition, that means a minimum $100,000 down payment, according to this SBA SOP 50 10 8 breakdown.

That single rule changes how buyers should approach negotiations. The consultant who knows SBA mechanics will evaluate not just price, but total project cost. Buyers often focus on the purchase price and forget that fees, working capital, and closing expenses can raise the required injection.

The same source also notes there's no minimum equity required if the transaction qualifies as a business expansion under the same NAICS code with identical ownership. That distinction matters because buyers sometimes structure the deal incorrectly by assuming every acquisition falls into the same bucket.

A strong primer on this financing lane is this guide to an SBA loan for business acquisition.

Underwriting reality: A lender won't rescue a weak deal structure. If the equity, documents, and cash flow story don't line up, the process slows down or stops.

What lenders need that buyers often miss

Lenders don't approve deals because the business is appealing. They approve deals because repayment looks supportable and documented.

For SBA transactions, historical cash flow has to support the proposed debt. Lenders typically require a post-acquisition DSCR of at least 1.25x on a pro forma basis, and if the historical cash flow doesn't show enough support, the lender must analyze two years of detailed financial projections with supporting assumptions, using operating cash flow defined as EBITDA, as described in this SBA financing overview for consulting firm acquisitions.

That's where consulting and financing intersect directly. A competent advisor helps assemble a package the lender can underwrite. That includes:

- Cash flow normalization: Defensible add-backs and realistic owner compensation assumptions

- Working capital planning: Enough liquidity to operate after closing, not just enough cash to get to the closing table

- Projection discipline: If projections are required, they need to be tied to identifiable assumptions, not optimism

- Document consistency: LOI, purchase agreement, source of equity, and lender narrative all need to agree

This is why buyers get into trouble when they hire pure deal-side advisors with no SBA fluency. The deal may look fine in an M&A memo and still fail in underwriting because the structure wasn't built with lender standards in mind from the start.

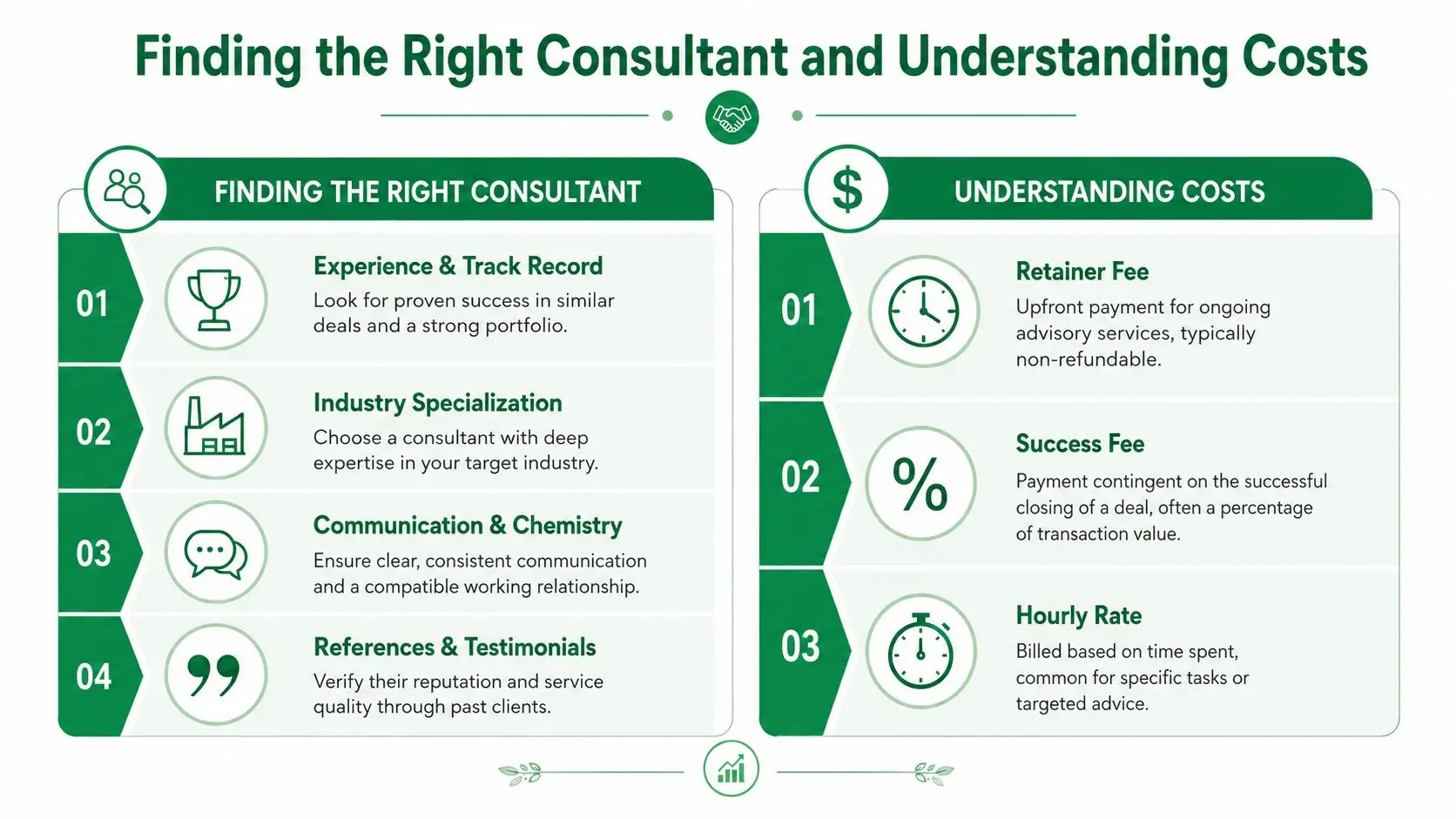

Finding the Right Consultant and Understanding Costs

The acquisition advisor market is crowded for a reason. Demand is strong, and the field is growing. As noted earlier, the global M&A consulting services market is projected to expand materially through 2033. That growth is good for buyers in one sense. There are more firms to choose from. It also makes selection harder because experience levels vary widely.

How to evaluate the advisor

A polished pitch deck doesn't tell you much. Ask questions that expose how the consultant thinks in live transactions.

Use a short screen like this:

- Relevant deal experience: Have they worked on transactions of similar size and complexity?

- SBA familiarity: Can they speak clearly about lender documentation, equity injection, and cash flow underwriting?

- Industry pattern recognition: Do they understand the operating risks of your target sector?

- Process discipline: How do they coordinate with attorneys, CPAs, and lenders when diligence gets messy?

If you're looking at consulting firms as targets or trying to understand who is active in that market, this Gritt.io investor search for consulting can help you see the investor environment around the sector.

One more useful filter is how they communicate bad news. Any consultant can sound confident when the target looks clean. The better test is whether they can tell you, quickly and clearly, when a deal should be repriced, restructured, or abandoned.

For buyers evaluating financing-side support in parallel, it also helps to understand what an SBA loan broker does versus what an M&A advisor does. Those roles overlap at points, but they are not the same.

Common fee models and buyer trade-offs

Most consultants work under one of three compensation structures.

| Fee model | Where it works | Buyer trade-off |

|---|---|---|

| Retainer | Best when the search is broad or the buyer needs ongoing guidance | You pay upfront, but you usually get more continuity and better access |

| Success fee | Common when the advisor is heavily involved in sourcing or closing | Incentives align around closing, but some advisors may become too deal-positive |

| Hourly | Useful for targeted review, second opinions, or limited-scope help | Flexible, but costs can drift if the scope isn't tightly defined |

None of these is automatically best. The right fit depends on whether you need full-process support or a narrower role. The key is scope clarity. Buyers get frustrated when they think they've hired a quarterback and discover they only hired a reviewer.

Ask for a written scope before you ask about price. A lower fee is expensive if it leaves core deal work uncovered.

Avoiding Costly Mistakes in Your Acquisition

Buyers rarely blow up a deal because they can't read a P&L. They get hurt because they miss the risk sitting behind the numbers.

The buyer who fell in love with the deal

A buyer sees a business in a familiar industry. The seller is charismatic, the office is busy, and the revenue trend looks stable. The buyer starts defending the deal before diligence is finished.

That's the danger point. Emotional attachment causes buyers to explain away weak gross margins, customer concentration, or unexplained add-backs. A good consultant slows the process down and forces comparison between what the business appears to be and what the records prove it is.

What works is disciplined skepticism. What fails is trying to “save” the transaction before the facts are in.

The diligence file that looked complete but wasn't

Another common problem is false confidence from a full data room. Buyers see folders, statements, contracts, and employee lists and assume the diligence is thorough because the file volume is high.

It often isn't.

A consultant should test for missing context, not just missing documents. If customer contracts don't show actual purchasing behavior, if vendor dependencies aren't mapped, or if background questions remain unresolved, deeper verification may be warranted. In sensitive situations, buyers sometimes add outside investigative support. Resources like corporate private investigations can help frame what that kind of diligence can look like when standard document review leaves unanswered questions.

If you want a broader view of where buyers commonly lose control of the process, this article on why business acquisitions fail is worth reading.

The transition plan that ignored key people

The hardest mistake to fix is a post-closing people problem.

A critical post-acquisition integration risk for small consulting firms is failure to retain senior consultants beyond the earnout period, exposing the buyer to key person risk if one important employee leaves, as explained in this roll-up analysis of consulting firms. That issue isn't limited to consulting firms. It appears in service businesses, agencies, specialty trades, and any company where customer trust sits with a few individuals.

The pattern is familiar. The buyer assumes the team will stay because the business has been sold. The seller assumes goodwill will transfer naturally. Nobody puts durable retention mechanics in place.

What works instead:

- Retention planning early: Identify the people whose departure would damage revenue before the purchase agreement is final

- Real transition agreements: Spell out the seller's handoff duties, introductions, and support period

- Aligned incentives: If the business depends on a few high-value operators, comp and retention terms need to reflect that reality

A buyer can survive a tough closing. It's much harder to survive a clean closing followed by a quiet loss of the people who actually produce the revenue.

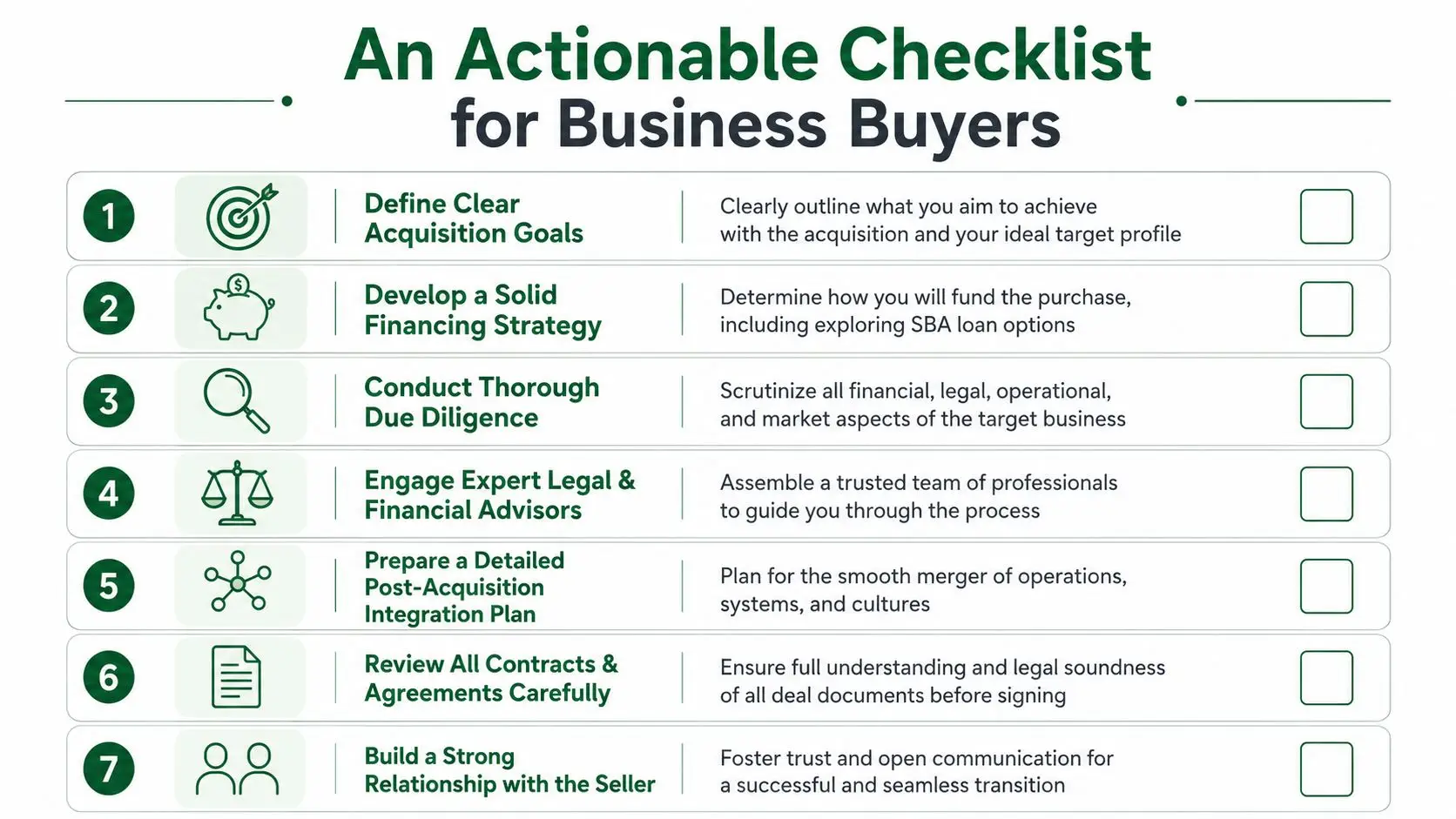

An Actionable Checklist for Business Buyers

A good acquisition process starts long before closing documents show up in your inbox. It starts with discipline, filters, and preparation.

Your immediate next steps

Use this as your working checklist:

- Define your target clearly. Decide what industries, business models, and owner roles fit your experience and risk tolerance.

- Set your real budget. Include not just the purchase price, but fees, working capital, and cash reserves after closing.

- Build your advisory bench. At minimum, that usually means an acquisition consultant, transaction attorney, CPA, and financing specialist.

- Get financing clarity early. Don't wait until late diligence to discover the structure won't work for your lender.

- Prepare your buyer file. Personal financial statement, resume, liquidity support, and source-of-funds documentation should be ready before you need them.

- Run disciplined diligence. If you need a practical framework, these essential due diligence templates can help organize your review process.

- Plan the first day after closing. Know who stays, who signs what, who talks to employees and customers, and how cash management will work.

For buyers using SBA financing, this business acquisition due diligence checklist for SBA loan buyers is a useful operational reference.

The buyers who do best aren't the ones who move fastest. They're the ones who stay structured when the process gets noisy.

If you're buying a business and want expert help aligning the deal structure, lender strategy, and closing process, GoSBA Loans can help you manage the financing side with practical SBA acquisition expertise.